My notes from Crompton Consumer AR 2019:

Financial and Business Performance

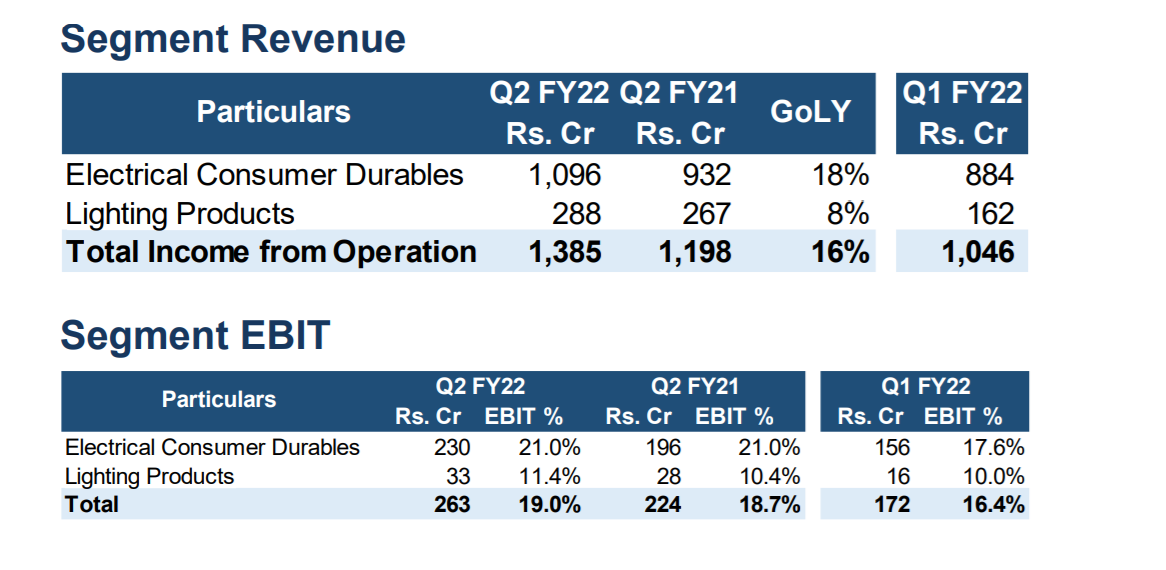

• Total Income stood at 4,478.91 crore, growing by 11.1%, against comparable revenues last year. Profit After Tax stood at 402.52 crore, compared with ` 323.79 crore in the previous year with 23% growth

• Strong growth in the Electrical Consumer Durables (ECD) segment, with comparable revenues growing 15.9%

• Your Directors are pleased to recommend a dividend of 2 per Ordinary (Equity) Share of the face value of 2 each,

• With focus on premiumization and delivering superior consumer value, we launched a new range of decorative fans like Air 360 Deco, Calibre and Aura 2.0. Under Pumps, the Mini Crest range of products, launched a year ago continued to drive growth. Under Consumer Appliances, revamped our entire range of Water Heaters during the year, which led to our total Water Heater volumes growing 25%.

• In Lighting, the core LED business, excluding sales to EESL, grew 13% in value terms. This was despite continuing price erosion across the range.

• The launch of ANTI-BAC bulb, a truly unique innovation, is one example of this approach. The bulb kills up to 85% germs, providing a healthy and safe home environment.

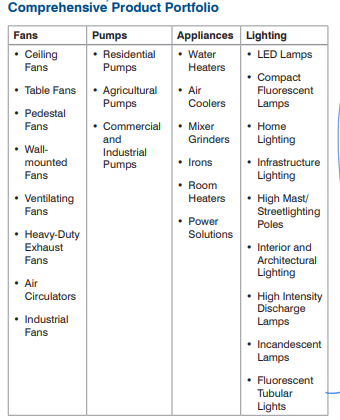

Fans

- The domestic fan market is estimated at 50 million fans per year with volumes growing around 6-7%.

- Market leader in Fans segment and has reported faster than industry growth during the year

- Air 360 is one such innovative product which covers 50%* more room area. Another revolutionary product “VSenseTM” delivers high speed in voltage as low as 115 volts*, specifically targeted at regions with power fluctuations

- It pioneered the launch of Air Buddy, a unique product that doesn’t disturb the cooking process and enables sweat free cooking. It launched Aura new which combines fluidic aesthetics and improved durability with 5 years DuratechTM warranty.

- Working on products with improved technology, and also IoT and Artificial Intelligence-based products.

Pumps

-

The Water Pump industry is estimated to be ` 7,000 crore. The market for water pumps in India is expected to witness robust growth, driven by increasing urbanisation, depletion of groundwater and decline in water table.

-

Your Company has been amongst the fastest growing pump manufacturers, with a dominant share in the domestic segment. Both domestic and agricultural pumps segment have grown in double digits. Through its Channel Expansion programme, it is increasing its focus on Tier 2 and 3 cities.

-

Mini Crest, launched in December 2017, has been an initiative that enabled your Company to deliver industry-leading growth.

-

Expanding the market by leveraging the Mini Crest range of products. It is evaluating the Brushless DC Motor technology, which is a new technology for manufacturing solar pumps.

-

Monobloc (2HP) and open well (3 to 7.5 HP) pumps with wide voltage design, which perform effectively in wide fluctuations of supply voltage in rural areas. This variety is useful to farmers as there are no frequent repairs required and there is lesser downtime.

-

Many parts of the country have high TDS (Salty) and more sand content in borewell water where normal materials of construction do not sustain. Hence, 4WSS series of pumps with stainless steel impeller and diffuser for better reliability as well as efficiency were developed by your Company.

-

Solar pumping systems with MNRE certifications were developed in AC (5, 7.5, 10 HP) as well as BLDC (5 HP) motors and further development is in process. These Solar pumps deliver minimum 10 to 15% more discharge than MNRE guidelines.

Water Heaters

- The Water Heater industry growth will be largely led by an increasing number of new residential units, coupled with rising per capita disposable incomes. As the share of households using branded water heaters rises, there is a robust runway for growth.

- During the year, entire range of water heaters were relaunched, adhering to your Company’s strategy of providing innovative products to consumers. Five new aesthetically designed Storage Water Heaters and four Instant Water Heaters were launched.

.

Air Coolers

India’s Air Cooler industry is projected to grow robustly, driven by low penetration and conversion from unorganised to organised segment. The industry is increasingly witnessing a shift towards models with better features, advanced electronics and better performance.

Recorded double-digit growth in Air Coolers and revamped the portfolio. One of these new offerings is a Desert Cooler with auto-drainage facility and a mosquito net filter, which enables humidity control and offers easy cleaning.

In Air Coolers, a unique model “Optimus” which stands out in performance as compared to its peers was launched. It has features like Auto Drainage, easy cleaning, humidity control, thicker honey comb and highest air delivery in its class. This summer, new range of plastic window and tower coolers were also introduced.

Lighting

Lyor LED Lamps: Lyor LED Lamps, India’s first BEE rated 5-star energy-efficient lamps were launched during the year. It offers 20% energy savings, compared to 3-star rated LED Lamps, and 50% savings compared to conventional lamps.

e ANTI-BAC lamps. This anti-bacteria bulb is a health proposition which kills up to 85% of bacteria in the house and is certified by Indian Medical Association (IMA). The bulb, a true market differentiator, is priced at 15-20% premium

5-dimensional growth strategy

Brand Excellence:

Company has been investing in the brand to create awareness and develop the market with innovative products

Portfolio Excellence

- Company remains focused on product innovation with consumer needs.

- The Aura Anti Dust Fan with a 5-year DuratechTM warranty (the first Fan with a 5-year warranty) is one such example where the promise to the consumer is not just aesthetics, but reliable performance for many years

- Entire range of Desert Coolers and our flagship product Optimus, with best-in-class air delivery and

- Unique self-cleaning feature is reinventing the category

- Launched a range of wide voltage pumps. These pumps which provide the desired water output, despite fluctuating voltage alleviates a current consumer pain-point.

Further, improving our design capabilities and building entry barriers in this space by registering our patents and designs

Go-To-Market Excellence

- Your Company’s Go-To-Market strategy is aimed towards expanding distribution reach beyond Tier 1 and 2 cities and increasing market presence in untapped markets.

- This initiative is now being deployed pan-India and supported with IT enablement. The focus of IT enablement includes creating a portal for dealers for automated ordering, secondary sales data integration and enabling sales field force.

Operational Excellence

Your Company’s aim is to deliver the best product quality, at lowest cost and improve product availability. The drive on cost optimization is aimed towards value engineering, new designs, alternative material usage and negotiation with vendors.

Organizational Excellence

Other Key Analysis/Information:

Online auctioning of services has been implemented with the help of SAP Ariba.

- Vendor Scorecard Monitoring, which identifies strategic vendors and drives performance; and Vendor Portal, which is an automation software to interact with vendors, were also kick-started.

- In the process of digitalising its dealer experience through implementation of a dedicated dealer portal. The portal is aimed to improve customer satisfaction resulting in ease of doing business.

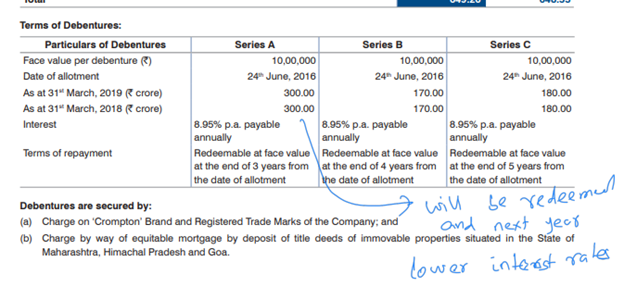

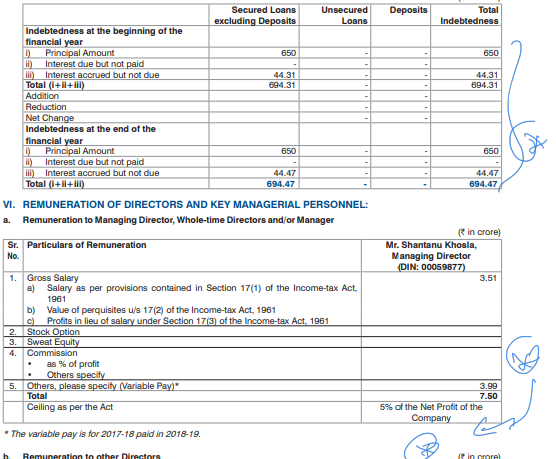

- Finance costs of

59.50 crore represents the interest cost on the Non-Convertible Debentures of 650 crore. However, 300 cr of debentures will be paid in July considering company is generating enough cashflows (having 650 cr of cash and investments) and hence next year expecting interest cost to come down to 30 Cr which should help in PAT margin expansion. Also, with reduced debt, slowly pledge should go off

• Your Company has initiated vendor rationalisation, emphasis on in-house manufacturing and scorecard evaluation of vendors has been put in place.

• Your Company has decided not to pursue ESCO projects. • However, your Company is standardising the process for assessing the tenders/business opportunities througha) Defining Process framework & Go-No-Go parameters along with Authority Matrix; b) Digitalising Lead to Order process

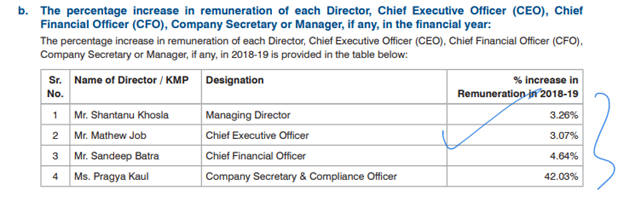

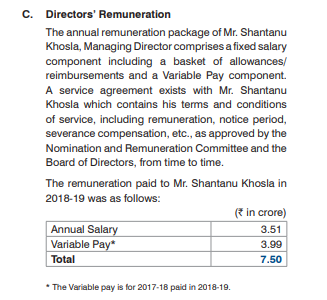

• Management salary growth and remuneration as a % of PBT well under control. Good to see employee remuneration growth higher than management remuneration growth. Also, management remuneration has performance based variables component and still within limits

FII decreased their holding and mutual funds increased their holding

Despite of 34% promoter holding, individual shareholders constitute only 8-9% of overall shareholding

Amansa increased stake but smallcap fund exited

Management Outlook

Your Company remains focused on three key objectives – growing sales faster than the market, operating profits in line with sales and converting all of the profits to cash. It expects growth to remain robust across all key segments with a combination of product innovation and driving go-to-market better and across more geographies.

Personal View

Since, Mr khosla did a 1-page communication to shareholders 2016 with simple, clear and measurable deliverables, he has walked the talk and continued the good work this year too visible both in financial numbers and overall business deliverables. Hoping double digit growth to continue with bit of additional benefit coming from debt reduction and interest reduction

Disc: Invested