Lately I found this stock worth buying and would like to share my reasons for this view.

Crompton Greaves is an electrical behemoth with more than 2 Billon Dollars sales. It is present in more than 85 countries having manufacturing facilities across the world. Presently the stock is available @190, giving a market cap of 12K crores. There is negligible debt in parent listed company books, however on consolidated basis the company has debt around 2200 crores.

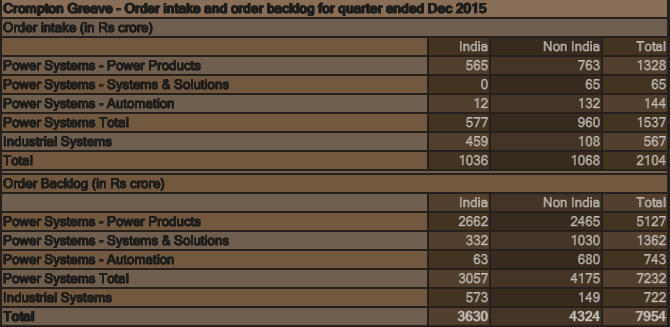

The company business is divided into three parts. The first is power system where company manufactures transformers and switchgears. It also have service elements like maintenance, diagnostics, system, turnkey services etc. The second part is industrial systems where company manufactures motors, generators, traction machines etc. The third vertical is consumers where company manufactures fans, lights, domestic pumps, appliances, power solutions, security system, coolers etc. Recently the company decided to demerge its consumer business into separate entity and this demerger can be expected to take place in next few quarters.

The company has a powerful consumer business and the brand is a household name in India. It is market leader in fans and pumps. In lighting it is one of three largest player. Appliance business is relatively small where last year it garnered a turnover of 180 crores. The size of consumer business is around 2800 crores growing at a healthy pace with EBIDTA of 330 crores. This demerged entity shall be a focused player on consumer segment and ought to be valued around 6000 crore on a conservative basis. Nearest competitor is valued around three times sales, and 35 times earning. We are giving it a conservative valuation of 2 times sales. Generally after demerger some operation efficiency and focus is gained which is good for the consumer business going forward.

The left over sales is more than 10000 crores on consolidated basis. There appears to be turnaround in power business and EBIDTA has improved to 14% in Indian operations. ROCE of power business has improved to 30% which is better among the pears. Industrial verticals is still in degrowth phase but likely to improve with turnaround in manufacturing sector. If we see the size, margin, ROCE of this business it is equivalent to peers. All the pears are valued at multiple of sales. Even if we give it a price to sales multiple of 1, it ought to be valued around 10K crores.

Thus demerger is likely to unlock value of around 4000 crore, i.e. 33%.

After demerger, the consumer business is likely to be more focused, consumer centric and operationally efficient. It can create a investment opportunity in the demerged business on its own, if the demerged entity is listed a steep discount.

The power and industrial business is showing signs of turnaround. Company recent foray into automation to promote smarter grids for increased energy efficiency is showing tremendous growth and management is very hopeful in this segment. The company is consciously trying to go up the value chain, and lately its critical products have been approved by Power Grid. Research activity is also going on well and they were granted two patents last year. On the whole appears to be a turnaround as 2014 EBIDTA has been manifold of earlier year. With expectation of revival in manufacturing sector, the company is likely to do well in future.

Some corporate governance issues are there. A couple of years back the Managing Director purchased an aircraft attracting severe criticism. Later he sold all his holding when left the MD post. But I think this is a thing of the past. Company has rewarded shareholders with generous dividends and last year a decent buy back of shares was also made. However, I request value pickers to share any corporate governance issue related to the company.

With these, I think the stock is worth a look for conservative investment.