I guess its time the company deserved its own thread. I’ve been following the Company since around May and invested at 140 levels. Brief below:-

About the Company

Creative Newtech is a distribution company that sells Samsung / GoPro / PNY and other products. They categorise them into Imaging (Zeiss, GoPro), IT (Samsung, Cooler Master) and Lifestyle (Fitness brands // Health, etc.). Since FY 2018-19, Company has forayed into two new business segments:-

Licensing business - They entered into an agreement with Honeywell under which they license manufacture the products for honeywell and then sell them in the markets assigned to them. Currently, they have the license to sell Honeywell Air Purifier and audio products in around 30 countries (India, SEA and Middle East).

Online Platform business - (Grow Your Profits With Ckart) is a B2B platform like Udaan where buyers & sellers can sell to each other. The “sell” functionality was activated in 2021. Right now, most of the partners that have onboarded onto ckart are Creative’s own distribution partners. It is essentially the distribution business getting conducted through ckart.

Consistent growth in revenue - mainly due to increased onboarding of brands every year.

Wafer thin margins, which is typical of a distribution business

Future Triggers / Positives

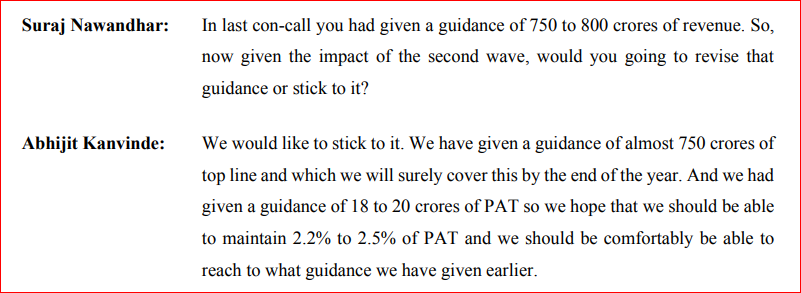

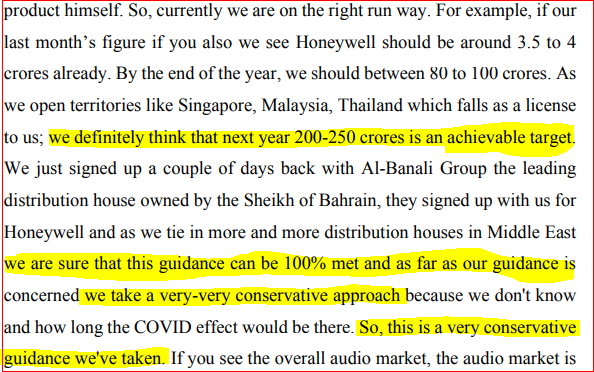

Management has guided for 80 to 100cr of Honeywell licensing revenue in FY 2021-22 and have remarked in Q4FY21 con-call that this can lead to 15 to 17% EBITDA margins. Honeywell for them is 40% gross margin product in India and 50% GM in other locations. More recently in Q1FY22 con-call, they’ve stuck to that 80 to 100cr guidance. SFor FY2022-23, the management has guided for 200 to 250cr business from Honeywell. What EBITDA it can fetch considering the scale economies is everyone’s guess. But even at 15% number, it yields INR 30cr EBITDA.

Ckart - this is a B2B platform like Indiamart and Udaan. Launched in 2020, Creative has onboarded their existing channel partners onto ckart and have also launched a “seller module” to the platform whereby the channel partners can show their own invnetory and sell to other customers on the platform.

The platform is relatively small with only 200cr worth of orders placed since inception (August 2021) and bulk of which is Creative’s own business moving to ckart but as the management says, this is their “blue ocean”. In Q1FY22 con-call, they’ve said that they are consulting with their board (which has IIM prof teaching social networks) on the right skill set and organisation structure for this business and will come to a decision in quarter’s time.

Management is relatively transparent with investor con-calls and presentations and updates. So information asymmetry if any can be bridged by the investing community.

Negatives / Risks

Company does not execute well and Honeywell sales do not pick up and the company misses its guidance. In that case, profitability will get hurt and future prospects of more licensing deals will hurt too.

Distribution business - 3rd wave COVID could impact their imaging segment, which was the biggest contributor until a year-ago and where they had good numbers under the Go-Pro product.

Inability to extend product portfolio and add more high margin / fast moving brands. For eg: Creative is currently absent in the mobile phone (mobility) category, which restricts its market size.

Management makes more minority investor unfriendly moves such as private placement at substantial discount.

Ckart is key for future rerating and to even justify its name change. In case ckart venture fails, the company is back to distribution & licensing business, which have relatively lower market / opportunity size as compared to ckart.

Valuations

The stock is currently trading at 275 (~315cr mcap), which is approximately 10x FY22 EBITDA and 4/5x FY23 EBITDA.

Profitability in future will mainly be driven by the two new age businesses and it remains to be seen how well they can execute

Disclosure – Invested since 140 levels.15% of invested PF.

Thank you @luckbychance for starting this thread. For easy reference, I am pasting here from the “Smallcap hunters” thread, a couple of posts related to the recent preferential issue at Rs 110 price by Creative Newtech:

In continuation of this discussion, I would like to give an example of another company that I am invested in. They waited for an ongoing upmove to stabilize before going ahead with the preference issue pricing—quite friendly to the minority shareholders.

I feel around Rs 150 to even Rs 200 could have been a reasonable price. Such preferential issue price acts as a support level for the stock price but now this support has been set too low. Even though prospects of the company look bright, the low issue price can become a self-fulfilling prophecy if there are large market corrections.

The preferential allotment actually was finalized in June when the price was trailing at around 110/- so I don’t find anything fishy in this transaction.

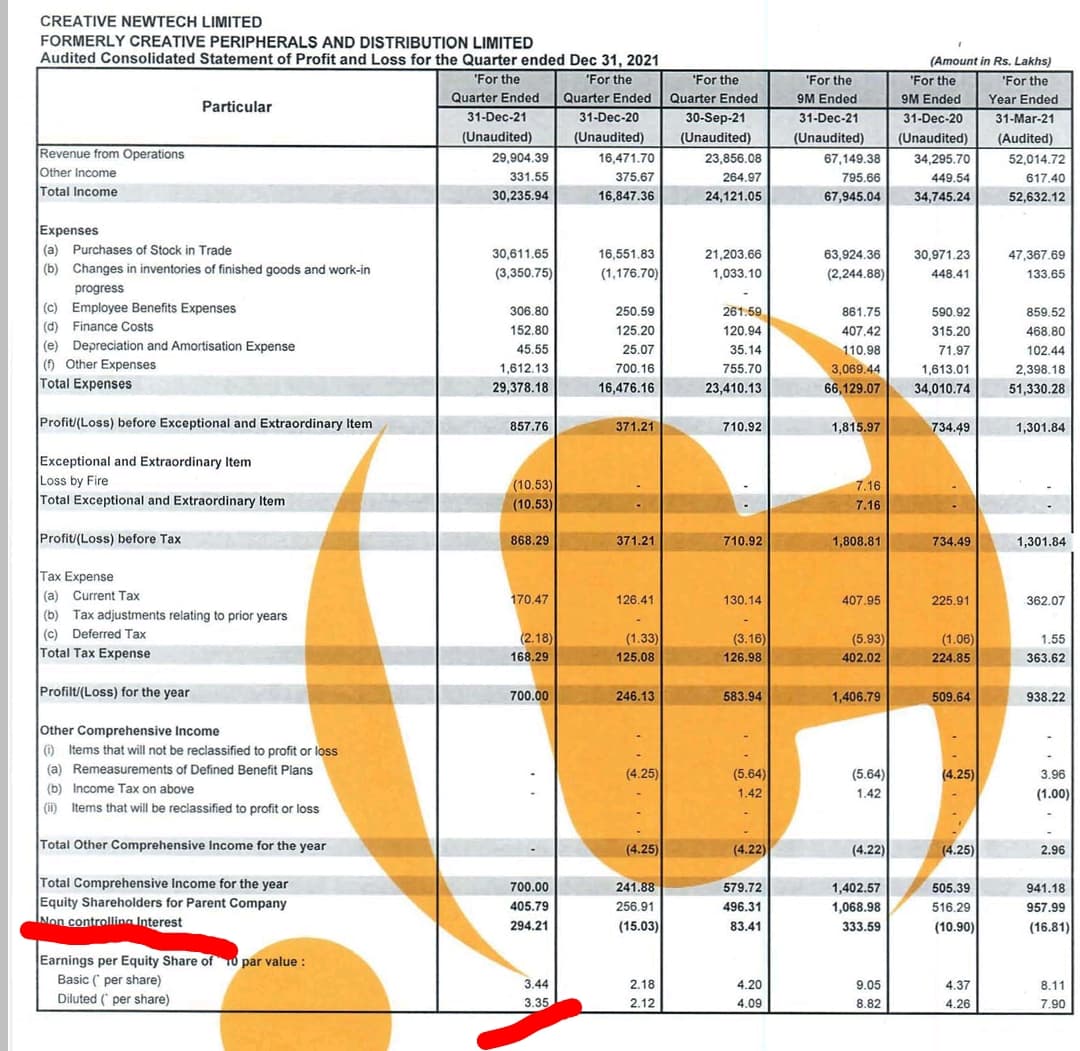

If you see the last few quarters results, the company does seems to execute all the planned activities in a right manner - resulting in better PAT & EBIDTA Margins and going forward should exceed more.

Imaging products (viz. GoPro Products and others) are the products which are of higher margins for the company and considering the unlocking happening and the revenge travel gearing up, sales for these products will go up, and thus company is expected to show better EBIDTA & PAT Margins and the ending of the COVID effect should also help. Management has already confirmed on the call that the month of July was the best ever month for the company.

I feel that development of Ckart is overhyped and is quite a long shot looking at the current platform features and the onboarding process and Honeywell business is underhyped since the Air purifiers are already in great demand from hotel chains (Co. has confirmed the tie-up with Marriott Hotels) and other retailers considering winter season coming in and the pollution fear gripping north states.

This is an interesting bet for coming two quarters at least and if Ckart clicks…This might be a multibagger stock to look out for…

Re air purifiers, the management in Q1FY22 con call indicated that while earlier air purifiers were more of a North India thing, but because of COVID and HEPA technology of Honeywell which has filters designed to stop the flow of COVID virus, they’re seeing a broad based demand.

Honeywell and other potential licensing agreement if they execute well are definitely the interesting aspects to watch out for.

Anyone has any insights as to who gets the sale revenue from product sales on amazon etc? I see Honeywell purifiers listed there and the seller being Cloudtail. The Company says that they have an exclusive licensing and distribution arrangement with Honeywell for such products.

I’m a little confused then with Cloudtail selling these products on Amazon? Or does Creative sell these to Cloudtail as the retailer?

The tone looks very conservative. In June they did around 70crs of business, assuming that to be the new normal, they should do 70*9 ~ 630crs. 120 crs already done this quarter. Thats 750 crores.

And i’m not even taking Honeywell business into account, which should be an extra 80 to 100 crs as guided earlier. Co should most likely exceed its guidance for FY22

Guidance for FY23 for the Honeywell business

So we are looking at close to INR 30cr EBITDA from the Honeywell business (assuming 15% EBITDA margins)

On brand licensing business

On ckart

3% royalty payable to Honeywell or a certain fixed value, whichever is lower. Beyond a certain level of sales, operating leverage should kick in and royalty would become redundant. Right now, the Honeywell agreement is till FY 2025.

Hi, I think they are into “brand licensing” arrangements. This is slightly different from contract manufacturing. A dixon doesn’t do any marketing and doesn’t create its own marketing channel to sell products. Creative does that for Honeywell. That is one.

Secondly, Creative has clarified on their con call that they don’t own the manufacturing facility, but, they scout third party manufacturers under the standards of Honeywell and then Honeywell inspects the facility. The products are then manufactured and sold by Creative.

The revenue from Honeywell business (sole brand licensing business) is guided to be INR 100cr in FY22.

Not sure what has happened in this counter. But this is now at lifetime highs. I expect Q2 results to be good and here are my expectations:-

Consolidated revenue: 210crs of revenue (70cr *3)

EBITDA margin: To improve to 3.5 to 4% on a consolidated basis (reason: expecting higher go-pro sales which is relatively higher margin product for them). Standalone EBITDA margins could cross 5%.

Key watchouts

Progress on Honeywell business: Sales were slated to commence mid Sept.

Update on imaging business and particularly Go-Pro sales

Q2 revenue at 240crs (Honeywell sales got delayed due to audio SKUs not being in there).

Honeywell sales starting from Nov and the management is sticking to guidance of 80 to 100cr for FY22.

GoPro have terminated their agreement with Creative and Creative has a tieup with Insta360 instead.

H2 to be better than H1 both in terms of sales and margins as higher margin products (Honeywell licensing, Hyperice etc) to kick in. Hyperice exclusive agreement for 3 years.

Next year guidance is around 1100 to 1300 crs of revenue with better margin profile. Officially they said 4 to 5% EBITDA. But that they would like to do “better”. Conservative guidance.

Honeywell agreement could be expanded to cover Africa

FMSG (fast moving social goods) share in product mix to improve. This is high margin segment as is also reflected in the segmented financial (9crs ebit profit on 40cr sales)

EBITDA for FY22 could be 50 to 60cr - official guidance - but we could be in for a positive surprise since Honeywell itself could be a 40 to 45 cr EBITDA business next year.

Ckart - they’re in a fix as of now as to what to do with it - the balance sheet can’t support a cash burn so next step decision will take more time - conundrum around balance sheet strength highlighted and hence no fixed guideline given.

10/12 cr of incremental debt maybe taken next mainly for the Honeywell business.

Valuations

12. Price has moved up a lot - currently trading at a mcap of 457crs which is 10x officially guided EBITDA for FY23.

13. Due to diversified nature, need to do a SOTP analysis here. Page industries is valued at 50+ FY23E PE. That is also because of the certainty on long term licensing arrangement it has (Page has licensing agreement with Jockey until 2040 whereas Creative Honeywell agreement is until 2025 for now)

Let us assume a 15x FY23E PE for the brand licensing business.

FY23E EBITDA from Honeywell business = 40 crs (conservative)

FY23E PAT from Honeywell business = 25crs (conservative)

15x PAT = 375crs

Distribution business

Redington is valued at 10x FY23E earnings (PAT) and has a richer and wider profile than Creative. Let’s take 5x FY23E earnings multiple for Creative on a conservative basis.

FY23E distribution business guidance = 900crs (conservative again)

FY23E distribution business PAT % = 2% (conservative)

FY23E PAT = 18crs

Distribution business valuation = 18*5 = 90crs

Overall SOTP = 375+90crs = 465crs

Imo, fairly valued right now. Although all estimates that i’ve assumed are very conservative and upside is likely here. Key focus area to track is the FMSG business which includes the Honeywell licensing business.

Yes, it is strange. There is no detailed description of the ownership structure of the subsidiaries anywhere in the investor presentation or the results.

I found the following statement in the latest results:

The consolidated financial result of the company includes the results of the wholly owned

subsidiary namely “Creative Peripherals and Distribution Limited (Hong Kong)”, “Secure

Connection Limited (Hong Kong)” and “Creative Ecommerce Ventures Private limited”.

(emphasis added)

To confuse matters, non-controlling interest should not arise if all of them are wholly-owned subsidiaries. Furthermore, in the last quarter results, the notes and the auditor comments do not mention “wholly-owned subsidiaries” but only “subsidiaries”.

A few months back I did not like the very low price given for preferential allotment to particular persons when they could have allotted at 3-4x price simply by waiting for a few weeks. Now, it is very important that the company clarify on this increasing non-controlling interest.

In the last concall, it was discussed that the company’s holding in the Hong Kong subsidiary named Secure Connection Ltd reduced from 70% to 52%. The details of this transaction are unclear and probably was not even notified to the exchanges. I could not find the details of the other shareholders of this subsidiary. This explains the increase in non-controlling interest.

As one can see in the last Annual Report, there is another related-party company named Secure Connection Private Limited seemingly based in India. Two companies by the same name, one subsidiary and another held by the promoters looks suspicious. Furthermore, there are 2-3 more related-party companies doing transactions with Creative.

My image of good corporate governance in this company has gone for a toss after I got to know the above information. Most likely I will exit the stock soon.

Standalone revenue does not matter much if a major portion of the profit is accrued to the obfuscated subsidiary.

Subsidiary may have substantial revenue even if there is not much difference between standalone and consolidated revenue. If there are substantial transactions between the standalone business and the subsidiaries, the consolidated revenue will be much lesser than the sum of revenues of the standalone and the subsidiaries.

The full picture can be clarified only by the management but I have my doubts about whether they will clarify, given their past record.

Try to buy or sell a small quantity. You will observe instant new orders. The counter seems to be a favorite of algorithmic traders. The trading activity is unrelated to the company management/promoters, although previous observations show that they appear to be quite ‘creative’.

Was just wondering why should a brand licensing arrangement with Honeywell command an EBITDA margin of 15%+ eventually? Read somewhere that this can be scaled up to 18-20% margins (basis revenue growth). Can anyone help me draw a parallel here with another listed brand licensing entity?

I would have thought a 15%+ EBITDA margin in Honeywell would make sense if they were manufacturing in-house. Here they outsource that as well. Are gross margins so high that they can get such a margin?