Yes because they take the lead in product development and that is what the margins are for. Their ppt makes that clear.

Anyone still following this Company? How is the management quality here, are they walking the talk? apparently on Honeywell business it seems they are over committing and under delivering? Any thoughts please?

1 Like

Q2 FY24 Concall Notes

- OCF Is negative as Quarter end had many holidays, the cheque and payment got cleared on the very First week of this quarter

- Will Explore the debt financing to Increase stake in Creative Subsidiary

- 30 Crores Will be alone from Air Purifiers, They are more of a life style product rather than the Need product, Price point generally comfortable between 12-14k Buck

Lifestyle product example can be many real estate company that intends right now to accompany Air conditioner with Property Might also Accompany Air purifier Considering the new Pollution Problems

The Air purifier Sales is around 40% Online, 14%-15% Offline and Rest through Branded Show rooms such As reliance Retail

There is shift in Behaviors’ of Big showrooms too, Earlier the norm was to Buy back the remaining Air-purifier left After December or Winter Per say. from last 2 Years No particular demand like that as such - Also type of razor blade business model i.e. Air purifier filter for corporates after every 6 months for retail after every year or so

- generally For Honeywell they are trying many SKU and from this many SKU, 2 product has to turn out big and Air purifier seems to be the very first one

- 2030 they intended to generate more than 2500-3000 Crores from Honeywell products only (Ofc many licencing brand will also be onboarded)

- Current Position of Ckart is just for cross selling purpose but they also intend to Commercialize the same in medium term where the transaction fee will be charged

- the above Can be in 2 Ways 1) Creative finances out of 10% bottom line or 2) On boards the investor who can finance the same take over the co. operation since the matrix of Creative is very different than that of market place

- Generally Op. leverage not available right now as product development cost is Not capitalized. After the line of products are complete the same will not be incurred and likely the same will be completed by the time company Reaches 2,000 Crore of Revenue (Probably by next Year) and then the fireworks will Start

- H1 Honeywell Sales can be around 70 Crores odd. They can easily achieve around 180 Crores of sales this year since the December Quarter can be generally Heavy for them

- Current Stake stands at 70% in Hong Kong Subsidiary Plans to increase up-to 77%. There is No tax nor Interest payment in Hongkong so 15% EBITDA Margin is safe to assume for Hongkong Business

My Analysis States that they can Easily do 500 Crores of Honeywell Sales in Next to Next Year Considering many SKU being approved by Honeywell recently

If I’m Correct those 500 Crores can fetch them 15% EBITDA and their 70% Stake (Might go upto 77%) For Shareholders bring the PAT to 50 Odd Crores and Remaining 1600 Crores of revenue From EB if gives 1.5-2% PAT Gives the PAT Around 25-32 Crores, therefore Trading at around 12x 2 year Forward Earnings

Disclaimer - Invested and Biased

1 Like

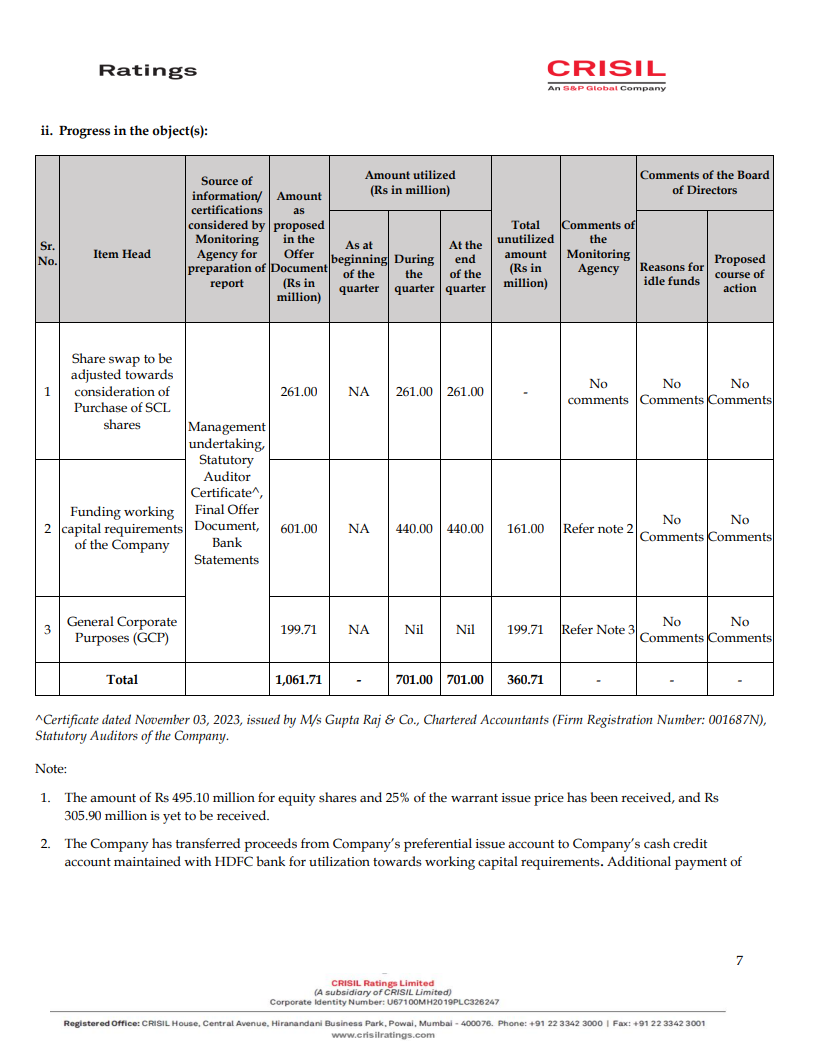

The report covers various aspects related to the utilization of issue proceeds and includes the following key points:

- Issuer Details:

- The issuer is Creative Newtech Limited.

- The promoters are Ketan Chhaganlal Patel and Purvi Ketan Patel.

- The industry/sector it belongs to is Computers Hardware & Equipments.

- Issue Details:

- The issue period was from August 10, 2023, to August 14, 2023.

- It was a preferential issue involving Equity Shares and Convertible Warrants.

- The issue size was Rs 1,061.71 million, comprising a share swap of Rs 261.00 million, the issue of equity shares of Rs 393.23 million, and the issue of convertible warrants of Rs 407.48 million.

- Details of Monitoring Arrangements:

- The report checks whether the utilization is as per the disclosures in the Offer Document.

- Shareholder approval is checked for material deviations from expenditures disclosed in the Offer Document.

- Changes in the means of finance for the disclosed objects of the issue are monitored.

- Major deviations from earlier monitoring agency reports are reviewed.

- Government/statutory approvals related to the object(s) are checked.

- Arrangements pertaining to technical assistance/collaboration are reviewed.

- Any events, favorable or unfavorable, affecting the viability of the object(s) are examined.

- Any other relevant information that may affect investors’ decision-making is considered.

- Details of Object(s) to Be Monitored:

- Cost of the objects, both original and revised, is listed.

- Reasons for cost revision are provided.

- Proposed financing options are outlined.

- Progress in the Object(s):

- The amount proposed in the Offer Document and the amount utilized are compared.

- Total unutilized amounts are noted.

- The reasons for idle funds are discussed.

- Proposed courses of action are suggested.

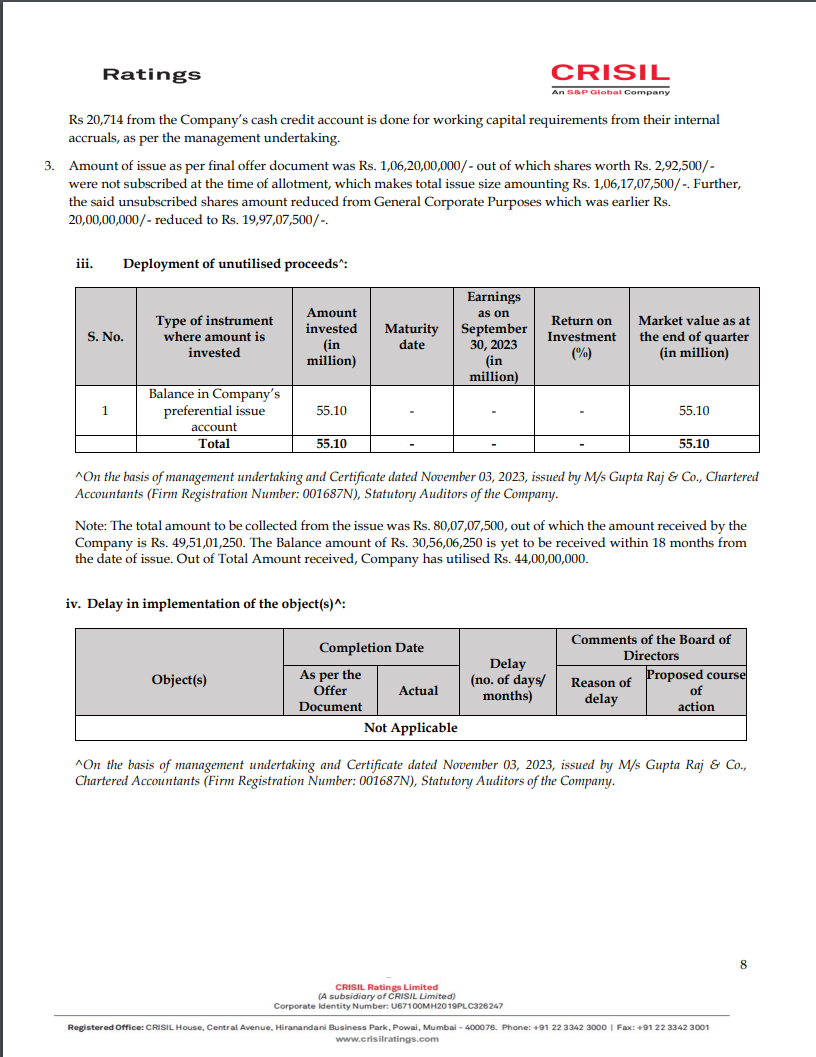

- Deployment of Unutilized Proceeds:

- The type of instrument where unutilized funds are invested is mentioned.

- The maturity date, earnings, return on investment, and market value at the end of the quarter are presented.

- Delay in Implementation of the Object(s):

- Completion dates for the object(s) are specified.

- Any delays in implementation are noted.

- Details of Utilization for General Corporate Purpose (GCP):

- Information regarding the utilization of proceeds stated as General Corporate Purpose is provided.

2 Likes

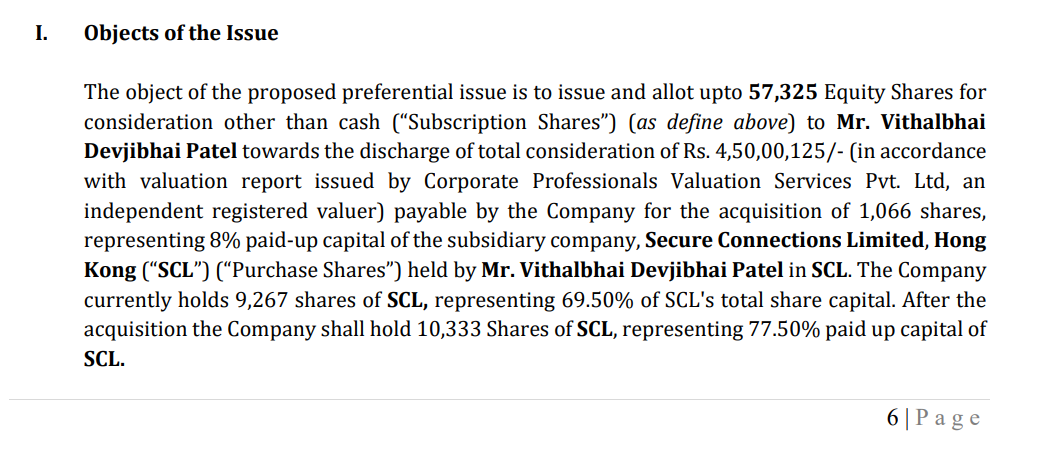

Company Has Entered into share swap agreement where the shares of subsidiary are swaped for 8% stake

Subsidiary is value at 56 Crores.

The Transaction seems fairly valued considering the whole business of Honeywell is Under the Subsidiary’s Name (I can be wrong)

FY-22 Hong Kong business did the PAT of almost 7 Crores (Couldn’t find data about 2023)

the implied multiple is mere 7-8x

The Subsidiary itself could be worth 25-30x Minimum

Seems Minority interest is taken care of in this transaction

2 Likes

The company has entered into another brand licensing contract with Cyberpower PC

The interesting thing to note is

- The company had mentioned earlier that they’ll only enter into new brands once honeywell toiches 220-230 crores of revenue - H1 was 90 crores so if they standy by their words H2 will bring big delta

- The contract entered is i guess with Hongkong Subsidiary where they pay 0% Tax

Certain questions on agreement too

Will ask them on concall

Disclaimer- Invested since 500s and adding

1 Like

| Description | Net profit | Rationale |

|---|---|---|

| Enterprise Business | 35 | Steady Cash cow business the company can do 2% margin and management has presented it’s content to continue to do the same since the same is -Ve working capital cycle business Implying the growth rate of 4-5% the company can do 1750 crores of EB sale which is bare minimum |

| Brand Licensing Business | 60.9 | Assuming that company does 500 crores of honeywell business and 300 crores of Cyber power business the NP margin can be 12% (15% EBITDA and 16% tax for Hongkong) @77% stake and for cyberpower @51% stake doing 10% PAT margins |

| 95.9 |

Did a bit modeling for picture how the same will look 2.25 years down the line

I think 1750 crores of sales is extremely possible in EB segment can even go above 2000 crores

Now for Honeywell They have targeted the sales of 500 crores 2.25 years down the line but 270 crores 1 year down the line, couldn’t get the chance to ask non linear Jump in earnings

Execution to be tracked in Cyber power did some review check from gamer friends of US who said it’s comparatively cheap and hence less performance but low or middle income house hold in US prefer the same buying the same from Costco

One thing to be kept in mind that there is still B2B market place model Just like Indiamart which is capitvely used and management have given their intention to expand it or spin it off

B2B startup generated around 400 crores of internal revenue (notional revenue) for Creative the same if valued at 2.5x will be 1000 crores and if not listed safely applying 50% DLOM it’ll still be worth 500 crores

So if you are valuing using Table above please include above 2 lines also

Disclaimer - Invested, Biased and Can sell anytime

Please do your own Due diligence

2 Likes

In reference to the above captioned subject, the Board of Directors of the Company, in their

meeting held on today i.e. March 11, 2024, has considered and approved the sale of its Business

division- ckartonline – an online B2B eCommerce platform for all supply chain partners

(‘Business undertaking’)to World Goods Marketplace Private Limited for a cash

consideration of INR 10,00,00,000/- (Rupees Ten Crores only), on slump sale basis as per the

terms and conditions mentioned in the Business Transfer Agreement (“BTA”), which is to be

executed between the Company and World Goods Marketplace Private Limited.

The detailed disclosure as required under Regulation 30 of the Listing Regulations, read with

Circular SEBI/HO/CFD/CFD-PoD-1/P/CIR/2023/123 dated 13th July, 2023 is enclosed

herewith as Annexure.

1 Like

New to this company but any idea why the cash flows are consistently so poor?

I have written a detailed note on Creative Newtech. Seems like a good day to publish it here. The note is dated 15th August.

Here’s the link - Notion – The all-in-one workspace for your notes, tasks, wikis, and databases.

Will also publish it as a new post/or write everything here soon.

Disc: Holding

6 Likes

@Administrator can I start a new thread on this topic to publish my detailed note?

Stock is up 30% in less than a month. Anyone aware of what is happening?

I’m tracking this stock closely. No news/corp announcement updates as such.

They might have made some progress in Cyberpower ( my best guess).

I went through your research as well, I have a slightly different view.

Would like to learn from your view too.

I have met the management last month, management wasn’t expecting much from CyberPower in this quarter.

This is a fairly illiquid name so some big buyer can skew the price.

More fundamentally, as they expand products under the Honeywell brand, wouldn’t other brands be less likely to give them licensing deals?

If they make speakers for Honeywell wouldn’t JBL steer clear of Creative?

1 Like

Brand management isnt just job of passing the product,

As Indian we have been fairly big notion that brabd management just includes trading,

But what goes behind manufacturing the brands and eastblishing it is something we steer away from understanding,

Ill say if they exceute Honeywell well, its more likely that they’ll get more business from other brands rather than less,

Its foot in the door,

Something requires second level thinking and instead of just poping 1st competition thoight this is something i think can happen in fairly long term

I.e., 2-3 brands + Cyberpower under one roof

I can be wrong though,

Its just a estimate i guess

4 Likes

Both Mr.Ketan Patel and Purvi Ketan Patel have shareholding ~3-4% in DC Infotech & Communication Ltd… Could anyone throw some light on this? Is there a connection? Or is it just a personal investment?

1 Like