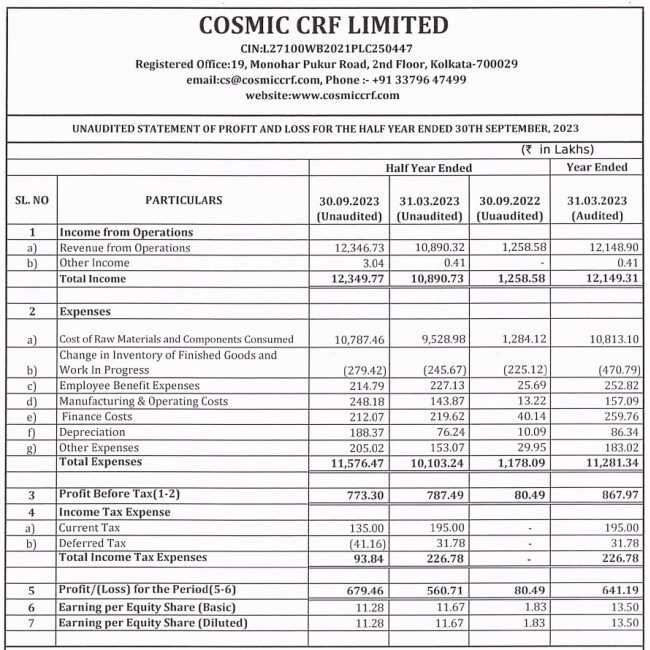

Good set, margins maintained. (Due to tax though, but not much impact)

Relevant notes. I was not aware of note 8.

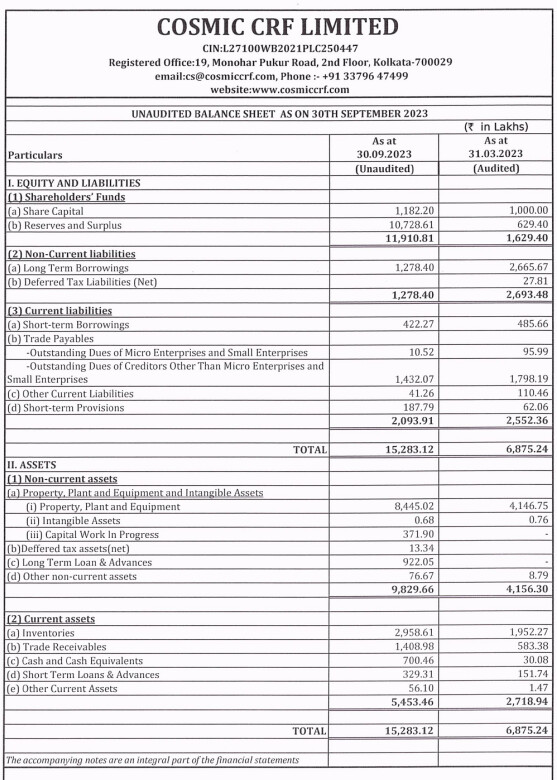

LT Borrowings reduction followed as per RHP.

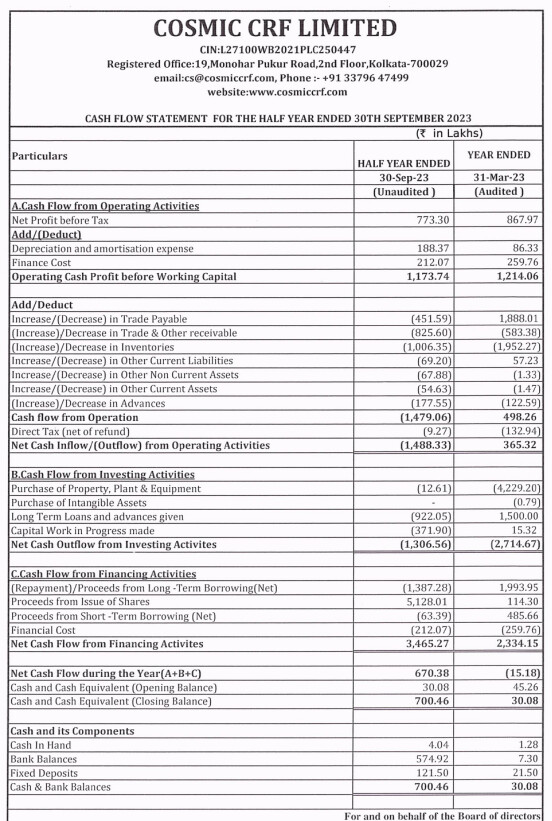

OCF negative

The long term advance of 9 cr is questionable or I am not aware of.

Overall Good set of numbers.

1 Like

As for the Notes given-

The company is planning to acquire a NCLT company having similar line of business.

This will lead to expansion of production capacity - beneficial for the company.

6 Likes

Can you please share the financial impact this litigation could have on the company ? If you are aware about it.

Finally the news is here which we were waiting for. The NCLT order for the takeover.

This will enhance the capacity as well as the client base of the company.

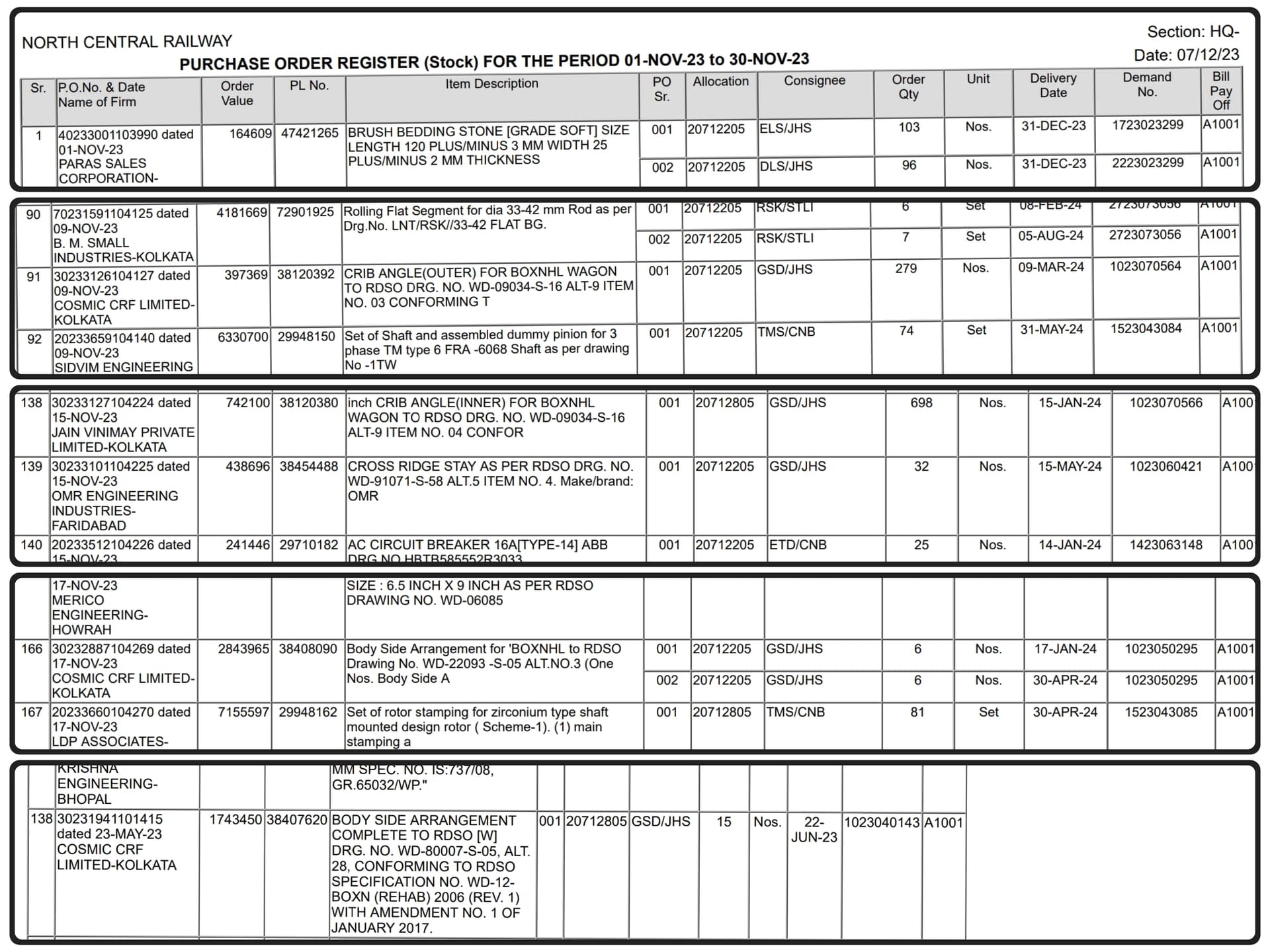

cosmic order.pdf (4.3 MB)

1 Like

Bulk deal - Cosmi CRF (Credits : Bulk deals daily log by Devesh Gaur)

Entering Entity: YUGA STOCKS AND COMMODITIES PRIVATE LIMITED

Entry Price: 371

Entry Quantity: 20,000 shares

This is a railways related business, so this might be late to the party, but does look statistically cheap at about 2X sales multiple. Definitely worth a look

2 Likes

Yuga appears to be trading entity…lots of trades in their Screener page…so would not give any credence to this.

1 Like

In Nov 23, Cosmic got some small quantities of orders through tender form in one railway zone.

Of course it’s in very small quantities but the CosmicCRF is actively participating in local tenders also.

3 Likes

This acquisition seems to be a good move. Huge wagon orders lead to good earning visibility for cosmic and this acquisition may add more top line and bottom line.

With thanks

2 Likes

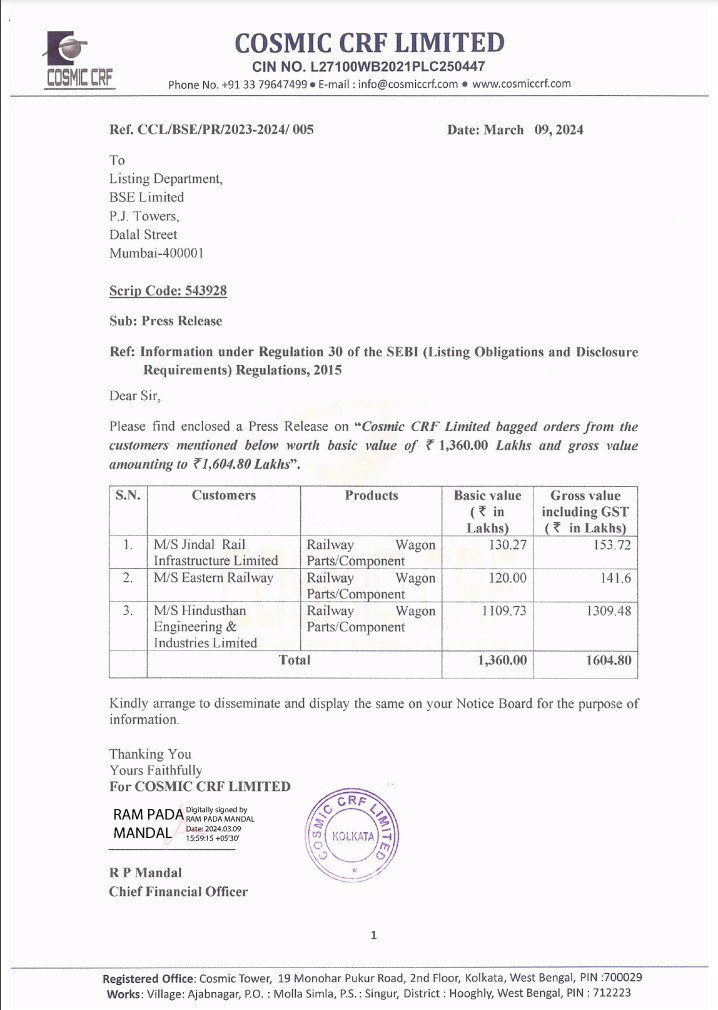

Cosmic CRF Limited bags orders worth Rs. 16crore.

2 Likes

@ca.ankitarathi Any views on Competition?

Who are its peers, how Cosmic is better than its peers?

Well didn’t look at the competitors very closely.

The exact competitors are all the companies who make CRF(Cold Rolled Formed ) steel products-

namely JSW steel, TATA Steel, JIndal Steel etc

3 Likes

Beneficial move by company.

Good move reflects in next result.

Money is stuck in inventory and receivables. Has anyone here done work on cash flows? Would appreciate any views.

NCLT Verdict summary:

NCLT Verdict summary:

Key Issues:

Key Issues:

Cosmic CRF Limited (Applicant) challenged their disqualification as a Resolution Applicant and the forfeiture of their ₹1.50 crore earnest money deposit.

Myotic’s Current Status:

Highest bidder with:

Final bid: INR 272.15 Crores

NPV: INR 255.28 Crores

Part of consortium with Fortune Global Solutions Limited

Unconditionally accepted Challenge Mechanism Framework

Raised concerns about Cosmic’s eligibility.

Main Developments:

- Energy Watchdog (NGO) raised allegations about Applicant’s (CosmicCRF) ineligibility under Section 29A

- Two agencies (AHSK & Co. and Priyanka Sharma & Associates) submitted reports declaring the Applicant ineligible Committee of Creditors (CoC) declared Applicant ineligible under Sections 29A(a), (c), (h), and (j)

Court’s Decision:

Partly allowed the application

Found violation of natural justice principles as the Applicant wasn’t given opportunity to respond to new grounds of ineligibility

Directed:

Resolution Professional and CoC to give Applicant fair opportunity to respond Matter remanded to CoC for reconsideration Applicant to be allowed to present justification regarding eligibility criteria

The court emphasized the importance of following proper procedures and maintaining natural justice principles in the insolvency resolution process.

Procedural Challenges:

Limited time to respond to multiple allegations Need to address findings from two professional agencies Complex multi-layered verification process Multiple grounds of ineligibility to contest Navigating CoC’s decision-making process

Legal Challenges:

Proving eligibility under four sections of 29A:

Section 29A(a)

Section 29A(c)

Section 29A(h)

Section 29A(j)

Addressing all legal aspects simultaneously Meeting burden of proof requirements

Immediate Actions:

Prepare comprehensive response to reports dated 18.10.2024 Gather all supporting documentation Request formal hearing before CoC Maintain EMD status and rights

Engage with Resolution Professional for process clarity

Legal Strategy:

Utilize court’s favorable order on natural justice

Focus on addressing all four sections (29A a, c, h, j)

Present structured defense against each allegation

Maintain rights in Swiss Challenge Mechanism

Keep legal options open for future recourse

Documentation Preparation:

Compile corporate structure evidence

Gather ownership and control documentation

Prepare management credentials

Collect financial records

Organize compliance certificates

Address concerns of all committee members:

UCO Bank (53.31% voting share)

Prudent ARC Limited (41.12%)

WLD Investments (5.57%)

Process Participation:

Continue participation in resolution process Maintain eligibility for Swiss Challenge Mechanism Keep the bid position active

Follow procedural requirements

Meet all compliance needs

Counter-Strategy:

- Address Energy Watchdog allegations

- Challenge negative agency reports

- Provide counter-evidence

- Demonstrate clear eligibility

- Maintain competitive position against Myotic Trading

My conclusion:

My conclusion:

- This verdict is allowing to give representing chance to CosmicCRF before CoC (as CoC disqualified CosmicCRF)

- Initially i expected that this verdict is giving chance to takeover the Amzen. In fact such orders are reserved for Myotic (they submitted a bid for Rs.277cr).

- CosmicCRF has to prove the allegations made on them are wrong.

- It’s a very long story but the chances of winning looks limited to cosmic as this is already in favor of Myotic.

Disc: Had holding

With thanks

3 Likes