Cosmic CRF FY25 Concall Highlights:

FY 2026 & Future Outlook

FY 2026 & Future Outlook

Consolidated Revenue:

Consolidated Revenue:

Projects FY26 revenue of 650–700cr from existing operations, assuming current steel prices (₹80,000/MT average, including stainless steel contributions)

Cosmic CRF (Standalone): Expected to contribute ~400–450cr, based on 38,000–45,000 MT

Cosmic CRF (Standalone): Expected to contribute ~400–450cr, based on 38,000–45,000 MT

NS Engineering: Projected to contribute ~150–200cr, scaling to 70–85% capacity ( 20,000–25,000 MT)

Cosmic Springs and Engineers: 50–100 cr at 25% utilization in FY26, scaling to 85% by FY27

Forging Unit New unit to add 150cr in revenue by FY27, with limited contribution in FY26 (~50cr) due to setup phase (45cr Capex)

Consolidated PAT Margin:

Expected 6–7% for Cosmic CRF and NS Engineering

Expected ~15% for Cosmic Springs and Engineers

due to high-margin spring and forging businesses

If Amzen acquisition is completed (10-15% PAT), it could add 1,500–1,600cr at full capacity, potentially pushing total revenue to 2,000–3,000cr by FY27, with FY26 as a setup year {6–8 months for refurbishment and Dedicated Freight Corridor (DFCC) setup}**

Backward integration (springs, forging, potential liquid metal asset) expected to reduce raw material costs by 3.5–4%, enhancing profitability

Exceptional costs (e.g., 3.25cr in legal and deferred tax expenses in FY25) expected to normalize, supporting higher PAT margins

Management committed to more frequent updates to counter misinformation and enhance stakeholder trust. Addressed perceptions of overexposure, emphasizing focus on business-building over publicity

Current order book and pipeline:

Current : 550cr;.50% execution expected in the next two quarters (Q1–Q2 FY26)

Railways (52%):.~286cr, primarily stainless steel-based orders, less sensitive to price fluctuations

Infrastructure (48%): ~264cr, based on mild steel at ₹72,000–74,000/MT

Execution Capacity: At 75–85% utilization of 110,000 metric tons total capacity (Cosmic CRF: 45,000 MT, NS Engineering: 20,000–25,000 MT, Cosmic Springs: 14,400 spring sets), projecting 82,000 MT output

Cosmic CRF Standalone upgraded Singur plant with a 6,000 sq. ft. shed, producing 20–22 wagon bodies/day

Pipeline:

Amzen Transportation Industries:

Lead bidder, with resolution plan submitted on May 27, 2025, post concall. Investment: 265cr (including DFCC setup). 6–8 months for setup post-NCLT approval, with limited FY26 contribution

Re-iterated confidence in Amzen acquisition (99.9%), with fallback plan of 650–700cr top line from existing operations if unsuccessful

Liquid Metal Asset:

Planned acquisition (<100cr) to secure 1–2 lakh tons/year of specialized steel (e.g., IS2062 E450, 3.2–3.3 mm). Aims to reduce LC costs and supply chain risks

Railway Tenders:

Anticipated tenders for 25,000–50,000 wagons by Sept–Dec’25, driven by a 45,000–50,000 wagon backlog. Targeting 100cr in new railway orders and 250cr in infra orders to maintain a 550–600cr order book

Others :

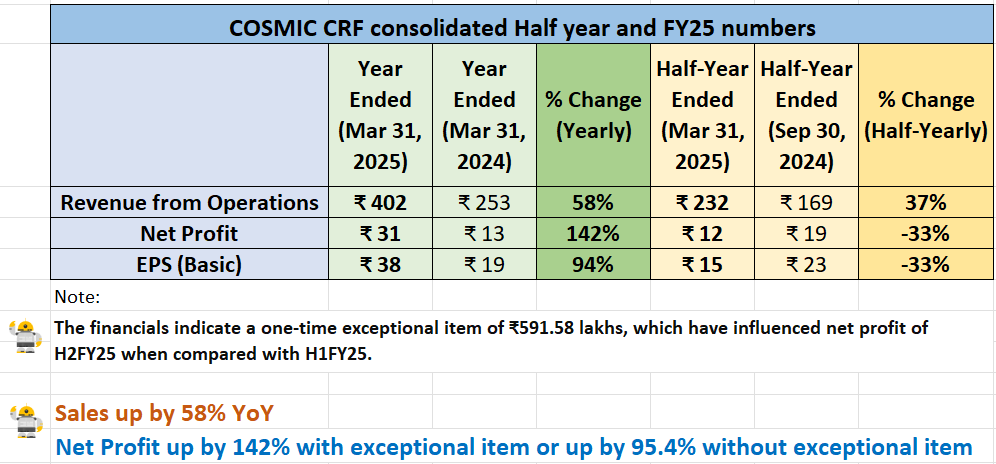

Steel Price Volatility: FY25 revenue shortfall (402 cr vs. 500cr guidance) due to a 22–23% drop in mild steel prices and a shift to 70% mild steel mix from 82% stainless steel

Wheelset Shortages: Railway wagon production slowed (950–970 wagons/month vs. 3,400–3,600 previously), impacting order offtake

CapEx Plan: 20cr for springs plant, 45cr for forging unit, 265cr for Amazon (including DFCC setup), totaling 330cr

Debt: Current debt of 70cr (65cr working capital, 5cr term loan). Future debt of 200cr (150cr term loan, 100 cr working capital) planned over 1.5–2 years. Future debt (10–13% of projected revenue) aligns with a 50:50 debt-equity ratio

Equity Raises: Raised 172.5cr via preferential equity in FY25 (84cr for NS Engineering). Additional 38.5 cr in promoter warrants to be triggered post-Amzen acquisition. No Dilution Commitment: Promoter pledged no further equity dilution until March 2028

Cash Flow Challenges: Negative operating cash flow in FY25 due to NS Engineering investments and delayed receivables. Expected to normalize by Q1 FY26

R&D conducted at the component level, collaborating with steel majors (e.g., Jindal’s mild steel-stainless steel blend trials)

Expects a rebound in stainless steel demand with box wagon tenders (post-Sept’25), as they are critical for coal, manganese, and iron ore transport, potentially raising average selling prices.

Forwarded message:

With thanks