would someone know why the dilution?

Disc: Invested at lower levels

would someone know why the dilution?

Disc: Invested at lower levels

after languishing for a while, stock is showing a strong movement today. Is there any news recently?

Control Print Ltd announces resignation of Ms. Nyana Sabharwal

http://equitybulls.com/admin/news2006/news_det.asp?id=214140

Do we know the reason for resignation? Does any one know why is the company raising capital? albeit an enabling provision. Given the profitability is there as well as the market is not something which would help them buy anything in their space. My sense it may be for printer ink manufacturing. I tried checking with the CFO but got standard response which were prompt.

Discl: Invested

Any views on the recent QIP that the company has closed recently?

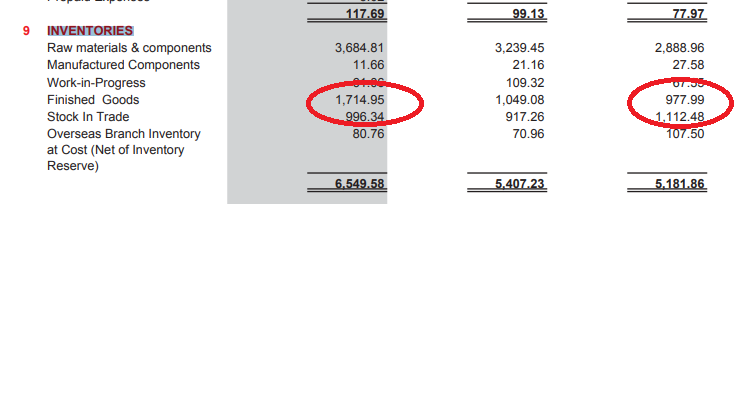

Inventory held is more than the cost of goods sold. Isn’t that alarming?

There is a continuous increase in “Finished Goods” in Inventories in last 2 years (Almost doubled).

Clearly company is not able to sell the products

The cumulative free cash flow generation from past 5 years is 0.37 cr… This implies company is unable to convert profits into cash… It is a negative sign for me. Big enough to give this company a pass.

The inventory is 65.5 cr vs sales of Rs 174 cr on annual basis. One must not compare quarterly sales with inventory. IMHO, this wont give out any meaningful statistic.

I think more relevant will be the FUTURE Free Cash flows that would be likely generated by the Company.

In the past few years, the Company has used the cash from operations to repay debt, set up a new manufacturing facility in Guwahati. Now there is no more debt left and how often will the company have to make capex of such size?

It has invested in Inventory - Yes. But one mustn’t forget it has paid at least 33% of its annual profits as dividend to shareholders in each of the last 3 years (FY16- 36%, FY 17 - 48%, FY 18 - 34% as per screener.in)

I was referring to the cost of goods sold, not the sales. Material expenses are in the 5000s whereas inventory is more than that.

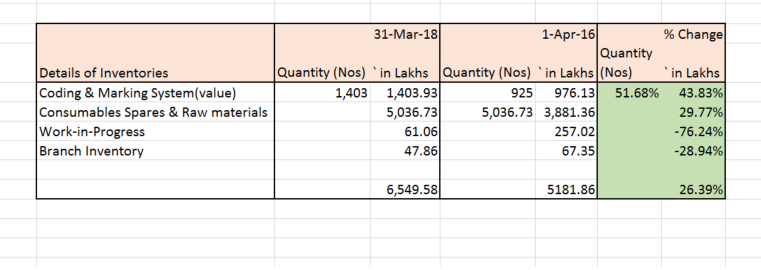

Did a further analysis of the Inventories from the latest annual report.

It seems that increase in number of printers is actually double(51%/43%) then then number of consumables spares+rawmaterials(29%–consumables spares will be much less than 29%). So what looks to be more blocked in inventory is the unsold printers(more than the consumables).

Plz share your thoughts on this if you think otherwise

Hi thanks.

I am unable to open Annual Report file on my mobile and away from laptop due to Ganesh Chaturthi festivities at home.

In the first image that you posted, Raw material and consumables represent the material used by Control Print to manufacture printers, ink and other consumables. (ie it is CPs Consumables)

The subject of the discussion is the Finished Goods - which includes consumables manufactured by CP and sold to its customers. (It is a consumable for the customers whereas for CP it is still FG)

As far as printer component in FG is concerned - if it has grown - is the increase in line with sales? or has there been extra blockage of inventory in printers - that can be figured out by a relative comparison with sales

Happy Ganesh Chaturthi

If the printers are being rented, are they accounted under inventory? I am not an accounts person and it will help if someone can clarify. Ideally, only saleable printers should be under inventory?

Princevegeta,

Thank you for pointing out the proper decorum to be maintained for a healthy discussion.

I am no expert in this industry and certainly haven’t done a lot of scuttlebutt because of the initial bias that I have for this company, due to its cash workings.

Looking at the screener data,

By just looking at the numbers, it feels like the company is not able to perform business on its terms. Offering credit to overcome competitors (as mentioned in the thread above) cannot be a long term strength.

Can this company keep on generating cash with a consistent growth, expand its capacity and get more market share in the long term without affecting its margins? Is there a good margin of safety for the same?

Please do suggest alternative viewpoints if any which can help in further analysis.

Hi

1 &2 - Yes you are right. The profits have been spent on Inventory and debtors. CFO is clearly lagging behind earnings. When you are a no 3-4 player in the industry and want to gain market share - it is one way of growing incremental market share. How much of credit one is okay with is a subjective call.

Personally I am fine with increase in inventory and receivables days if they are

3 - Cash ROE at first glance looks a lot lower - because of the same reasons as mentioned above. Again one has to take a call on how much reinvestment in Working capital is required for growth. I feel this is the reason market is not pricing the stock to its full potential

4- ?

Let me rephrase your question. Suppose you are the management and want to grow the business and market share, what would you do?

Would you keep a steady state growth of ~ 10% without taking risk of Inventory obsolescence and credit risk ?

Or would you aim for ~ 20% growth by trying to manage the two to an acceptable level.

My answer to that question is - if one is fine with

10-12% growth, there are better and safer opportunities in the market and real life to deploy your money.

For a business like CP - there are long term tailwinds like rise in consumer goods sales, formalisation of economy, rising per capita etc.

Hence it makes sense to take some bit of risk and aspire to grow at higher rates.

Same logic applies to an investor - CP to me remains an opportunistic bet with potential to compound at 15-20% + with some degree of risk attached.

Can such a growth be sustainable? What is the distinguishing factor? Receivable days are around 88. Inventory days are around an year. (This might not be an accurate calculation)

One is essentially relying on the assumption that-

Of course the risk-reward topic is subjective but can loading up on inventories and receivables be considered a moat at all to begin with? Why can’t competitors have the same strategy?

While the management might try to do the best in the situation they are in, the question is if that situation is suitable for an investor who might have the advantage of several other investment opportunities which offer a growth prospect with a margin of safety.

c85e48f7-47dd-4293-b2bc-67475dcd9d26.pdf (469.7 KB)

Hi All,

Does management indicated anything regarding the poor result shown by company … Sales also not increased much

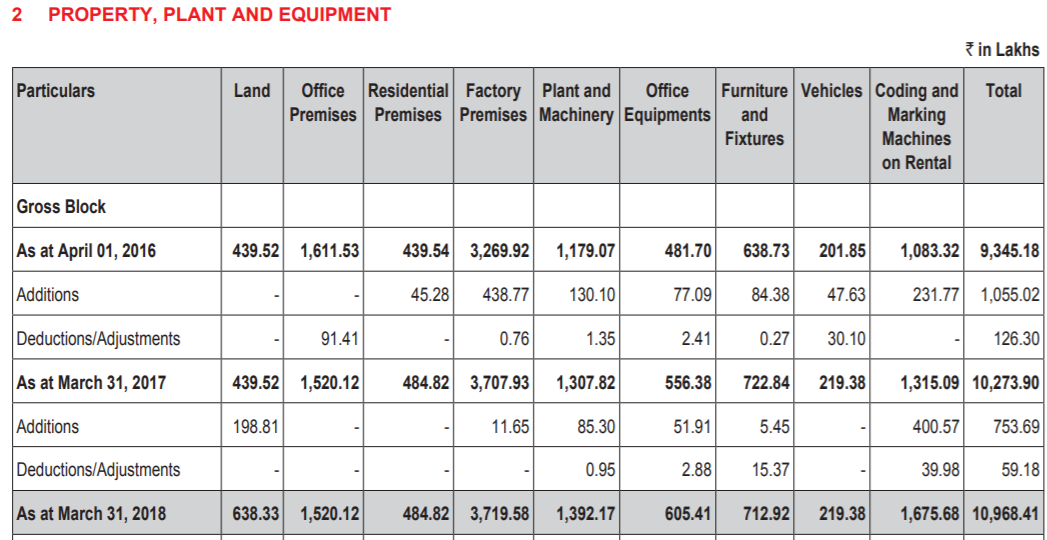

Sharing this for everyone’s sake. Machines on rental are classified under PP&E. See the snip from FY18 annual report below.

Does anyone here have info on how many machines out of the installed base of ~10,000 are on rental?

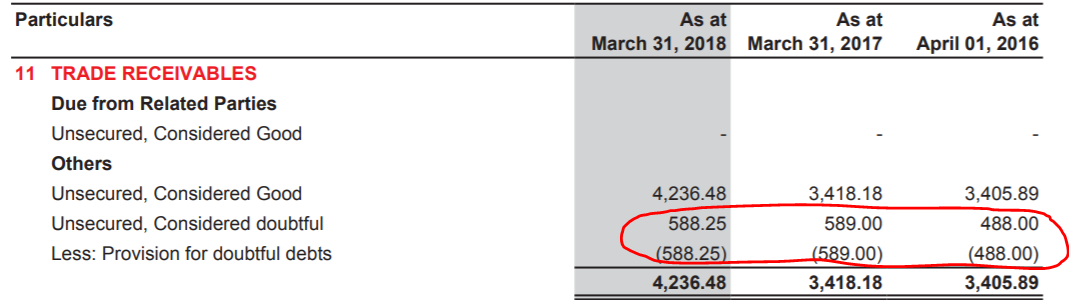

Another concern that needs to be pointed out is that the company’s provision of doubtful receivables is very high in the range of ~15% of total receivables.