Thanks for your insights.

What is your view on Valuations?

Currently trading at high PE compared to historic valuations.

Do you feel that will it will sustain current valuations?

Disclaimer: Not invested but tracking

Thanks for your insights.

What is your view on Valuations?

Currently trading at high PE compared to historic valuations.

Do you feel that will it will sustain current valuations?

Disclaimer: Not invested but tracking

Why is the stock falling? Anything related to the fundamentals or just a correction?

Quarterly results aren’t great

I have analysed the company with the available public information since 2010.

Following of my observations have led me not to consider investing in it:-

Size of the industry is small - Approx. 1500-1700 crore, which is not too big for a company to grow enough, and become a great wealth generator.

Frequent capital raise by the company - warrants to promoters in 2010, 2011, 2013, 2014, 2015. Till 2018, all the cash generated was getting stuck in WC, as such company needed constant capital from outside. The situation improved from 2019 onwards, although, but needs constant vigil.

Active investment in direct equity - It seems like equity investing is a core business of the company as a considerable portion of PAT is from capital gains from equity investing. Also, sometimes the equity investment is for very short period - it sold stakes in different companies within 01 year. In 2020, there was a net loss too from equity investing. As such, equity investment operation becomes a distraction.

Independent director does seem a related party - Mr. Vivek Himatsingka, Independent director seems like is brother of Chairman’s Son-in-law. I have tried all the public information available to come to this conclusion but correct me if I’m wrong. If my point is correct, it is very poor corporate governance and a big RED.

Promoters are very opportunistic - They wanted to diversify into Real Estate during 2008-12 boom, tried manufacturing Masks after COVID, investing company’s money in Venture capital funds.

Promoters almost every year went for the maximum remuneration possible under the law, but for many years, could not spend CSR amount as designated.

There are some favourable points for the company like expected growth in Packaging sector, it being only Indian company in the industry, formalisation of various sectors after GST etc., but the negative points outweigh the good ones for me.

Fy 24 Results-

Conclusion of latest earnings call is, management or especially shiv kabra is conservative in the cash cow which is their core business but aggressive on new verticals which they have acquired ( Vshapes, Codeology, Markprint B V). They are committing atleast 50Cr for RnD on Vshapes to reduce per sachet cost and to use recyclable materials and this business is similar to the biggie “Tetrapack”. Shiv is very pessimistic on this which is unexplored and they have 2 to 3 million euro of sales as of now, if this clicks they can do wonders but the probability is quite less according to me.

Exited fully @ 865

200 DMA broke down

Is there anything fundamentally wrong with the company now? The co is down 25% from its ATH and currently trading below the 200DMA.

Any particular reasons or a good time to add more?

Hi, There is no Independent Director by the name of Mr. Vivek Himatsingka on the company’s Board. There is one Mr. Gaurav Himatsingka however. Are you referring to the same person, and if yes, where did you find that he is the brother of Chairman’s Son-in-Law? Mr. Gaurav Himatsingka’s appointment resolution clearly states he is not related to any other Director. Can you please recheck and confirm?

The company is in transition, and in the Q3 & Q4 concalls, Mr. Shiv Kabra has given a detailed account of what he is trying to do, which is worth reading. The company has limited scope to grow in its traditional market, and Mr. Kabra is tapping several adjacencies – both in India and Europe – to make the business grow. Not all of them may succeed, but not all of them will fail either, one hopes. Even within the traditional business, the model is changing from Size to Quality. The frequent capital raise of the past has ended, and in fact reversed - company did a buyback last year. The transition will take time, and until then the results may not be to the market’s liking. But doing nothing is worse, I guess.

A few highlights from the Q4 FY24 concall:

Current operations: Pipes, food, cement, FMCG and beverages are our top five earning sectors. Target is around INR 400 crores sales by FY '25. It may be achieved or may not. The industry growth rate is normally about 1.5x GDP growth, about 12 % a year. Gross margin range should be consistent at 60 %.

There is a substantial increase in the coding and marking machines on a rental basis for this year. Some of the larger companies prefer leasing the machines on a per printer - per code basis and paying on a per print basis or on a per machine per year, per line basis. It is like an alternative model to the existing sales process. But because of the way it is structured, the fixed asset of those machines comes into CPL’s books and then it gets depreciated. This type of business is done with customers who are high-profile customers because normally, the company prefers to selling the machines. Margins in these are slightly better than normal margins.

There is more and more focus on the top few hundred - top 1,000 - 2,000 customers of India. It may lead to a smaller number of printers sold but the value of the sale in terms of the amount of business it generates over the lifetime of the printer will be much higher (Comment: this strategy was described extensively in the previous concall)

The company has gained some market share over the last 3 - 4 years. The entire coding and marking business last year in India was about INR 2,000 crores - 2,100 crores. CPL is already at about 17 % market share. The amount it charges for print is literally like INR 0.1 or something. It is quite low. So, there is a limit to how fast it can grow because it depends on how fast the volume of its customers grow. They have done 3 different types of expansions - One was digital printing of coding plus business (Markprint). The second part is entering the Track and Trace business with software division, where not only do people want to print information, but they also want to trace the entire supply chain (How this works is explained in detail in the Q3 concall). The third part is to look at some new geographies.

CPL is expanding into newer areas as the management feels they are sort of done with coding and marketing. R & D and innovation is more where they think their core is. They want to be in a space which is more around innovation, more around IP, where you are creating new needs for customers. There is some risk, but in the end if one must do something new there is always going to be a certain amount of risk.

Not planning any more acquisitions for another 24 months at least.

Markprint: This is the “coding plus” area which is beyond the date code and batch code where people want to print out a larger amount of information on products. The Markprint products were quite expensive for the Indian market. But now some products have been developed off the support or the expertise from Markprint which can be leveraged in the Indian market, and we the company has a better idea where Markprint products can be sold directly.

Codeology: That is more specialized. Here, printing happens directly on to the products. They do not use the printers which print on to label and then apply the label on to the products. Codeology has a good market in that specific business. Codeology also feels that there is a market for CPL’s products in the U.K and they are interested in expanding sale of its products in their geographies.

V-Shapes: It is in the sort of single dose, single use or single-serve space. V-Shapes is a company that has a lot of patents around this space. They already had a JV with them. CP Italia S.r.l bought all the assets of V-Shapes including intellectual property and the trademarks and the customer base and so on. This is more in the core packaging machinery how to make single doors type product which has applications in pharmaceutical, cosmetics especially the higher end cosmetic and in certain low food condiments and certain types of sauces. So, it can be used for any type of liquid packing and there is a development for powder packing option which again is only primarily for the pharmaceutical industry.

CPL was working with V-Shapes for about 1.5 years. And has a fair idea of the interest in this product from customers in India. They have a huge customer base in the packaging space.

The addressable market is quite large because there is a massive area of single or low single serve. It is more expensive than cheaper areas like sachets. But it can be cheaper than certain other areas like the single serve glass bottles or the types of things. But space must be created for that. So that makes this sort of a longer-term play. Like tetra pack created its own market. They are competing with glass bottles or with HDP bottles or with pouches. So out here also, it must create its own market. The management says the scope is significant. A lot of R & D will be required for reducing the cost of the material, developing the recyclable option, getting all the certifications, and keeping that technical knowledge base live in Italy and developing sales - these all are significant expenses and investments. It is going to take two years to put everything in place.

(Disc.: Have a tracking position)

Just a layman question out of curiosity, why hasn’t this company forayed into 3D Printing?

Recently, Promoter buying has been seen. Price also moved up from bottom.

It will be Interesting to see the coming quarters and business development.

Adding concall notes from Q4FY25.

FY25Q4

Disclosure: Not invested (no transactions in last-30 days)

Hey everyone, hope you all are doing good.

I am researching about this company from last few days and it’s definitely worth of your time to track.So, basically company is in the " reverse aging " phase of its corporate cycle, Its old and traditional business-(Manufactures & supplies Coding and Marking Machines, related consumables) seems to be matured and there is not much runway for growth there.

Now they are making some intersting as well as some weird acquistions which I will talk about-

European Expansion: Acquiring Technology and Market Access

A cornerstone of the diversification strategy is the acquisition of specialized European companies. This approach provides Control Print with immediate access to proprietary technology, established intellectual property, and a launchpad for international market presence, leapfrogging years of internal development.

The acquisition of V-Shapes represents the most ambitious and transformative bet in Control Print’s recent history. The transaction was structured through the company’s European holding subsidiary, Control Print B.V., which established a 100% step-down subsidiary, CP Italia S.r.l., to acquire all the assets of V-Shapes, including its intellectual property, trademarks, and customer base. This move marks a significant diversification from printing solutions into the capital-intensive domain of packaging machinery, specifically focusing on the innovative single-dose packaging segment.

Management’s strategic rationale is to enter a large, IP-driven market where it can create new customer needs rather than compete in a commoditized space. The business model is explicitly compared to that of Tetra Pak: the company sells not only the proprietary packaging machine but also the patented, consumable laminate material required for its operation. This creates a powerful, recurring revenue stream that aligns with Control Print’s core competency in aftermarket sales.

The addressable market for this technology is described as “very large” and “significant”. The initial target segments are well-defined: the pharmaceutical industry, where the higher cost of the material is less of a barrier; the high-end cosmetics sector; and the premium food condiment market. Management has expressed confidence in the market potential, stating there is “strong demand for this product if this is done well,” based on their experience and customer feedback in India over a 1.5-year period working with V-Shapes prior to the acquisition.

The financial commitment to this venture is substantial. At the time of acquisition, V-Shapes had annual sales of EUR 2.5-3 million, a significant drop from its peak of EUR 12 million per year during the COVID-19 hand sanitizer boom. Despite the revenue decline, the business was reported to be cash-flow positive by approximately EUR 1 million in the last year. The investment from Control Print has been considerable, with an asset capitalization of approximately INR 18 crores for land, building, machinery, and patents. Furthermore, management has outlined a forward-looking annual operating expenditure budget of approximately EUR 4 million. This budget is allocated towards critical growth initiatives: EUR 1.5 million for R&D, over EUR 1 million for expanding the global sales force, and another EUR 1.5 million for general operational costs.

Management has been transparent about the formidable challenges ahead. The first is the high cost of the proprietary packaging material, which must be reduced to penetrate the price-sensitive food and cosmetics segments. The second is the urgent need to develop a recyclable version of the packaging material to meet global sustainability demands, as the current laminate is a non-recyclable aluminum-polymer composite. Finally, building a global sales and service infrastructure is a significant undertaking. Acknowledging these hurdles, management has clearly set investor expectations, stating a 24-month investment phase is required to bring the V-Shapes business to a breakeven or “no-profit, no-loss” position.

This acquisition marks a fundamental shift in Control Print’s business model and risk profile. The company’s core business is asset-light, cash-generative, and operates in a predictable market. The V-Shapes venture, in stark contrast, is capital-intensive, requires substantial ongoing investment, and involves creating a new market category. Management’s own language—describing it as a “longer-term horizon play” where the “reward is worth the risk”—signals a strategic move towards a venture capital-style investment in a high-potential but unproven technology. The explicit 24-month timeline to breakeven indicates a multi-year period where this division will likely be a drag on consolidated profitability, a calculated trade-off for the potential of a transformative, long-term growth engine.

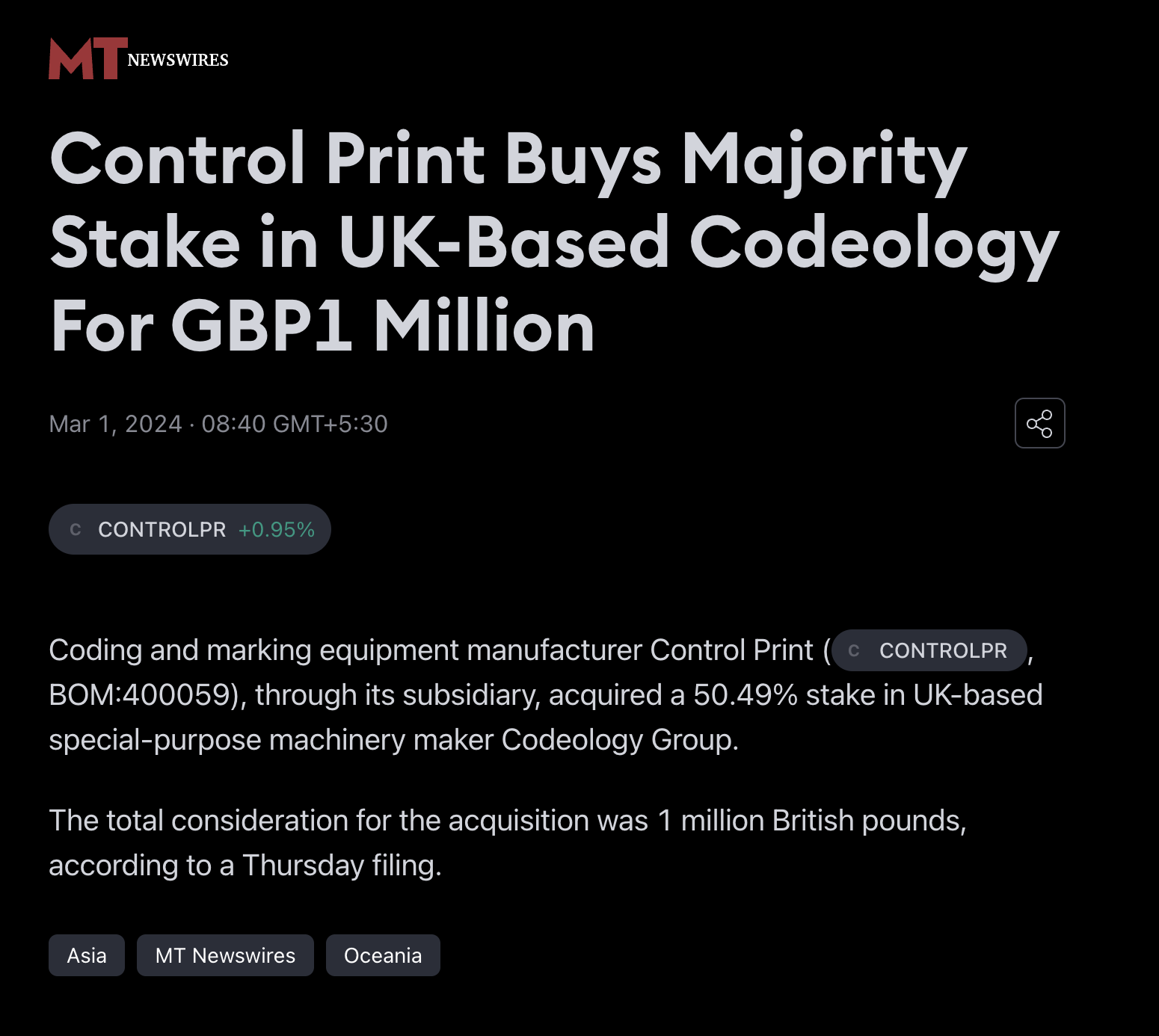

In sharp contrast to the high-risk nature of the V-Shapes venture, the acquisition of the Codeology Group is a classic, strategically sound “bolt-on” acquisition. In February, Control Print acquired a 50.49% stake in the UK-based company for approximately GBP 1 million.

The strategic rationale for this deal is clear and dual-pronged. First, it addresses a key gap in Control Print’s product portfolio by adding Codeology’s proven “print and apply” label applicators. This technology is distinct from Control Print’s direct-to-product printing and caters to a specific need within its existing customer base, particularly for outer carton labeling. Second, the acquisition creates immediate market access synergies. Control Print can leverage its extensive network in India to sell Codeology’s products, while Codeology provides a ready-made channel to sell Control Print’s core coding and marking products into the UK market, leveraging its established customer relationships.

Financially, Codeology generated revenue of approximately GBP 700,000 last year. The business was loss-making on a consolidated basis, but management provides a crucial piece of context: this was partly because Control Print had requested Codeology to pre-invest in expanding its team and operations in anticipation of the acquisition, which was ultimately delayed due to tax structuring issues. This suggests the underlying business is likely healthier than the recent financials indicate, mitigating the financial risk. The total investment was the acquisition cost of approximately GBP 1 million.

The primary challenge identified by management is the successful integration of the product line, which requires a level of mechanical expertise that is currently nascent within Control Print’s predominantly electronics and fluid-focused engineering teams. The ambition is to overcome this learning curve and have a clear strategy for utilizing the new product line by the end of the current financial year.

This acquisition represents a more traditional and lower-risk approach to growth. Unlike V-Shapes, which necessitates creating a new market, Codeology serves an existing need within Control Print’s current customer ecosystem. The two-way market access synergy offers a much faster and more predictable path to revenue generation. This low-risk, synergistic play provides a valuable balance to the company’s overall diversification portfolio, complementing the high-stakes bet on V-Shapes.

The acquisition of Markprint B.V. is a strategic move to capture capabilities in the higher-value segment of the digital printing market. Control Print initially acquired a 75% stake in the Netherlands-based company in July 2022 and subsequently increased its holding by another 5% in Q4 FY24, bringing its ownership to 80%.

The primary strategic goal is to acquire technology for what management terms the “coding plus” space. This involves high-resolution, single-pass digital printing that allows customers to print more complex and variable information—such as ingredients, logos, and barcodes—directly on the production line, offering greater flexibility than traditional pre-printed packaging.

Markprint’s financial performance has been stable. The company generated revenue of approximately EUR 750,000 last year and was at breakeven, supported by a strong gross profit margin of 53%. In the first nine months of FY23, it reported a net profit margin of 11% on revenues of EUR 0.5 million. The total investment made by Control Print in Markprint to date amounts to EUR 1.7 million.

The journey with Markprint illustrates the practical challenges of technology integration. A key hurdle has been adapting Markprint’s products, which were developed for European markets, to the highly price-sensitive Indian market. Management has candidly described this process as being “slower than expected”. This has led to an evolution in strategy. The initial plan of directly selling Markprint’s products has shifted towards a more nuanced approach of leveraging Markprint’s underlying expertise to develop new, more cost-effective products specifically for the Indian market. Management’s ambition is for this venture to contribute positively to the financials in the current fiscal year (FY25) and to serve as a long-term technological enhancement for the core business.

This evolution from a simple “import and sell” model to a more integrated “absorb and innovate” strategy demonstrates an adaptive and realistic approach. It reflects a learning process in which the company has recognized market realities and pivoted its strategy to maximize the long-term value of the acquired technology, rather than forcing an unsuitable product into a challenging market.

In parallel with its European acquisitions, Control Print is undertaking strategic initiatives within India that signal a deliberate evolution from a product-centric to a solutions-centric business model.

The development of the Track & Trace division, branded as QRiousCodes, is a cornerstone of this domestic strategy. This in-house developed division provides end-to-end software and automation solutions for supply chain traceability.

The market opportunity was initially catalyzed by a government mandate requiring the top 300 pharmaceutical brands in India to implement QR code-based traceability on their packaging. This created a significant, compliance-driven market. The potential revenue from a full primary, secondary, and tertiary implementation on a single production line is substantial, estimated by management to be betweenINR 25 lakhs and INR 45 lakhs.

After an initial investment phase, the business has recently reached a critical inflection point. Management reported that in the last few months of FY24, the division has turned from being loss-making to achieving breakeven or contributing positively to the bottom line. The revenue model is particularly attractive as it moves beyond one-time hardware sales. It includes significant upfront implementation fees for the complete solution—encompassing printers, vision systems, conveyors, and software integration—and is supplemented by a recurring revenue stream from Annual Maintenance Contracts (AMCs) for the entire system.

Management’s ambition for this division extends far beyond fulfilling a regulatory mandate. They aim to provide a “superior solution” that helps customers actively improve their business operations through better inventory management, prevention of product diversion, and enhanced marketing capabilities. With the business now on a stable footing, the expectation is for it to contribute positively to the company’s financials in the current fiscal year (FY25).

The Track & Trace initiative is strategically crucial as it fundamentally alters Control Print’s relationship with its customers. It elevates the company from a transactional supplier of hardware and consumables to an embedded, high-value solutions partner. The integrated nature of the system, combined with the recurring AMC revenue, creates significantly higher customer stickiness and integrates Control Print deeply into the operational workflow of its clients. This shift towards a solutions-based model is a key element in building a more resilient and profitable long-term business.