-

These three FOCO screens are a one-off, management has clarified in interviews that all future screens will be FOFO.

-

Your concern about quality standards in a FOFO model is fair, I had the same concern initially. It is a genuine risk. To assess this, I went through reviews of their cinemas, and so far the feedback looks encouraging. SOPs appear to be holding up, otherwise, such consistent reviews across locations would be unlikely.

-

I also recently learned that each cinema has a manager on the company’s payroll whose role is to ensure quality standards are maintained.

-

Another important point is the degree of control the company retains over franchisees. Content, ticketing, and F&B are all controlled by the company, which gives it leverage in discussions. If SOPs are not being followed, the company can push for corrective action, something that is not always possible in many FOFO models.

One of my friends shared an interesting insight, and I thought it would be worth noting it here to see how things play out over time.

He pointed out that today Connplex is making a significant portion of its money from EPC, which ideally acts as a barometer of inefficiency in the system. As the network scales to around 300–400 screens, royalty income should start becoming the dominant contributor. At that stage, it would make sense for Connplex to run the EPC business at near-zero margins. This would position it as the lowest-cost franchiser for branded cinemas, potentially flushing out competition, or at least making it very difficult for competitors to survive due to lack of scale. This, again, is a product of first-mover advantage.

As an outcome of this, franchisee ROI would improve meaningfully, creating another layer of resistance for franchisees to partner with alternative operators.

Over time, this could evolve into a moat, where Connplex becomes the cheapest and most profitable option for franchisees to partner with.

That was his thesis. I’m not sure how much of this ends up being true, but it’s worth noting it here and revisiting in the future (if still holding till then ![]() ).

).

Recent twitter company analysis post.

Its an interesting business. What bothers me is that I am not able to answer convincingly , if this takes off, why PVR cannot come into this market? They are deeply embedded in the movie distribution ecosystem equipped with more resources. Its not like they are wedded for life to their current model of opening huge capital intensive multiplexes in large cities.

No one is stopping anyone from doing anything.

Every company has its own systems and processes. New players innovate, larger ones take notice, and they adopt those strategies if it suits them.

Reliance Retail shifted its strategy from traditional retail to quick commerce. Titan is exploring more franchisee-led expansion after observing Kalyan.

So, everyone ends up following everyone.

PVR will, and I think has already started franchisee operations.

But that doesn’t mean Connplex’s business is finished. India is still underpenetrated in terms of screens per capita.

So everyone gets room to expand. The one that is more agile and moves faster will win more than the others.

In the end, it’s business as usual.

Sorry but this is wrong. Titan EBO/Tanishq has always been franchisee-led. So has Titan Eyeplus. They do own stores but those are more for understanding the market and pilot testing.

I believe this X post satisfactorily answers the question raised above

Thanks for sharing.

PVR’s attention validates that there is a market for mini-plexes in Tier-2 and Tier-3 cities, which were earlier ignored.

Connplex is clearly addressing this gap.

From here, it’s about disciplined execution, customer experience, and faster expansion.

One thing this article doesn’t talk about is the kind of expansion PVR will pursue. It will likely be either COCO or FOCO. In both cases, all operating expenses and lease expenses will pass through PVR’s P&L and balance sheet. This is not a royalty-based expansion model.

Also, their target of 20-25 screens seems modest given their size, leaving plenty of room for other players to fill the gap, Connplex itself will add over 100 screens in FY27.

How competition evolves over the next few years can only be judged with time.

For now, I don’t think it’s something we need to dwell on.

Thank you all for the great discussion so far. It has been very insightful!

I’m not sure about competition coming late though. PVR is planning to add 100+ screens every year under its FOCO/Asset light model. These smart screens are going to have seating capacities of ~300 seats. They have transitioned to this model very recently (2023 or 2024)

The model sounds very similar to what Connplex is doing. But Connplex definitely was the first mover.

Now if both PVR and Connplex are pursuing the same model, I think PVR will have a definite competitive advantage due to the brand and scale.

Scale in particular provides a great advantage i.e., they can negotiate the best distribution rate, better F&B rates etc. This can make it hard for Connplex to compete.

The only way I see Connplex scaling is if they move very fast in areas untapped by PVR in the next few years. This will be tough. PVR is not going to sleep on this.

But scaling so fast in a business they have little experience in comes with its own risks.

That’s my 2 cents anyways. But curious to hear your thoughts.

Honestly, sir, it’s too early to say. There is hardly any consumer category that doesn’t have competition. Tier-2, Tier-3, and Tier-4 markets in India run too deep for any single player to cover.

My view remains the same here,

Yeah that’s the only way I see it being positive for Connplex i.e., both players dominate and don’t get competitive (like Pepsi and Coke). But that’s very rare.

That said, I think there is a good short term upside if the scale quickly and execute well. Although I think long term PVR will reign.

First I want to clarify where I am coming from

-

I have previously invested in a company called Kontor spaces based on the social media buzz and now sitting on heavy losses. There were several red flags in the accounting which were evident but I didn’t go into the details at that time.

-

I read a lot about PVR inox and convinced myself that a cinema business can earn only 15-17% ebitda in India but I was surprised to see a new company making 30% EBITDA margins(double the industry average) despite giving ‘fair share’ to the franchisees.

-

The analysis is to understand this 30% and where it is coming from.

The H1 of 25-26 was one of the best period for the exhibition industry in last 3-4 year, so an analysis for this period would be a reliable proxy for the annualized performance (±10%).

Now let’s see how are the results that were declared for H1 25-26 and whether those numbers justify the payback periods and royalty claims mentioned in the previous threads.

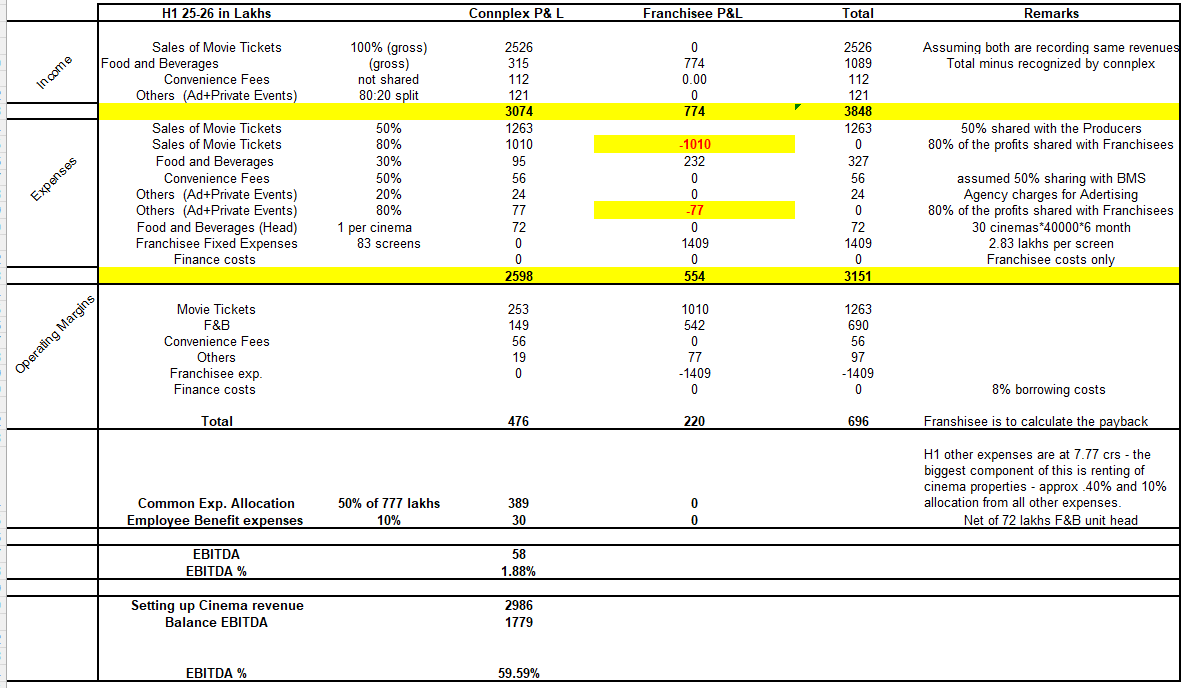

Consolidated = Connplex + Franchisees

Sale of Movie Tickets

Income - With H1 admits of 12.16 lakhs and the ATP 243 (inc. GST) - the Consol. revenue should be 25.04 crs. ( 12.16 x 243/118 x 100) - Since Connplex reported 25.26 crs revenue in H1, it is evident that that they are reporting 100% of gross revenue and not just the commissions.

Expenses:

- Producer Share (~50%): ₹12.63 Cr.

- Operating Profit (Consolidated): The remaining amount for the entity.

- Connplex Share (20%): ₹2.62 Cr.

- Franchisee Profit (80%): ₹10.10 Cr.

Food and Beverages

The Spend per head for F&B were 94(inc. 5% GST)

Consolidated revenue is =94 x 12.16/105 x 100 = 10.89 Crs.

Connplex should be ~royalty = 10.89 x 70%(net of COGS) x 20% = 1.52 crs

Connplex here have shown a Sales 3.15 Crs ( ~28% don’t know why ) So they have reported here the gross sales instead of royalty.

Consol is 10.89 crs, connplex reported 3.15 crs the balance 7.74 Crs is franchisees Revenues.

Expenses - I assumed to be in the range of ~30% ( material cost + transportation+ packaging+spillages ) for both connplex and Franshisee’s

Interestingly here Connplex deploys one unit head per cinema to oversee all the operations. Assuming their salaries to be 40k per month - this is an additional exp. for this segment at 0.72 crs ( 30 x 40000 x 6 months)

Convenience fees

-

Income: Typically, 40–45% of tickets are booked online. Assuming a net rate of ₹25 per ticket, the gross revenue should be ₹1.21 Cr (12.16 { lakhs} x 40% x 25) - Connplex reported ₹1.12 Cr, which aligns with this assumption.

-

Expenses: 50% of this is typically shared with aggregators (e.g., BookMyShow), leaving ₹0.56 Cr.

Advertising fees and private events

Income: Reported revenue is ₹1.21 Cr. Based on a calculation of ₹50,000 per cinema per month, the total comes to ₹0.99 Cr (50,000 *33 cinemas *6 months). This suggests the reported ₹1.12 Cr is Gross Revenue, not just royalty income.

assumption in previous threads were with 100000 per cinema of Ad+ convenience Fee . So i have considered 50k per cinema for the calculation income.

Expenses - assumed 20% as agency costs ( ad aggregators).

The profits then are to be shared between franchisee and Connplex in 80.20 split.

Franchisee Fixed expenses

2.83 lakhs per screen = 2.83 lakhs836 = 14.09 crore for H1 25-26.

Connplex Fixed expenses - It can’t be said that all the other expenses reported in the P&L are purely for the purpose of the EPC business. let me tell you why -

-

around 7.7 crs were reported as direct expenses in the H1 , last year FY 24-25 this expense was 9.56 crs & out of this 3.87 crs was for “rent for cinema properties” ~41% if we allocate even 10% of the balance costs - roughly 50% of this other expenses is for the recurring business.

-

Employee benefit expenses are 3.75 Crs - 10% can be allocated ( this is pure assumption) but just taking a very conservative estimate . ( 3.75-72)*10% = 0.3 Crs to recurring business.

Now if we try to simulate a P&L for the recurring business - based on H1 2026 results which is one the best H1 for the exhibition industry in last 4 years. It would look like this .

------ 58 lakhs EBITDA and 1.88% margins from the recurring business - hardly a break even . I haven’t considered any marketing/Brand promotion expenses otherwise it would be even lower.

------ 60% reported margins on the EPC/Franchisee fees income.

The franchisees have earned an EBITDA of 2.2 crs for H1 - annualized - 4.4 crs.

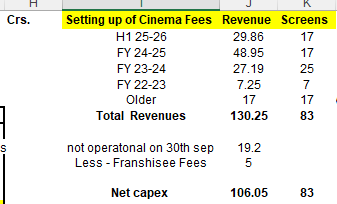

The EPC income of connplex = Investments of Franchisee’s

-

now let’s find out how much is the revenue earned by connplex untill Sep’2025 - that will be cumulative investment of franchisee’s. Before 2023 - I assumed only 1crs/screen capex.

-

I have reduced 19.2 Crs from the capex because management has said that 16 screen which were completed in H1 - the revenue is booked in H1 but those are not operational.

-

someone has pointed that the H1 includes 5 crs for franchisee fee and those screen are not operational - So I have reduced that as well .

-

Let’s calculate a payback period - Annualized incomes 4.4 crs - capex - 106 crs

-

Payback period comes at 24 years - if we follow discounted cash flow method it will be much higher.

-

the numbers can’t be correct - does that imply that reported numbers are not right.

Infinite ROCE’s -

the gross block in H1 has increased by 60% (inc. CWIP) and one of the reason for this increase was the purchase of LED screens and Projectors. The infinite ROCE argument doesn’t hold good if the capex is incurred for the recurring business. Even if the business is asset light the EBITDA% has to reasonable to show a modest ROCE. the 2% EBITDA margins doesn’t make any sense.

The receivable Issue

Receivables in H1 has increased by 9.5 crs in the H1

-

see the recurring business doesn’t have any receivables and out of the 29.86 Crs EPC revenue - 5 Crs is the Franchisee Income - which is an upfront payment - No receivable here as well.

-

the balance revenue of 24.86 crs is similar to H2 of 25-26, so the receivable should not go up for this stream as well.

-

The management has guided for 45 days credit period for EPC receivables - so the receivable at the end of H1 should have been = 6.12 crs. { 24.86 crs*2 (annualized)*45/365 } whereas the actual receivables are 22.55 CRS.

-

not only this the Management expects further increase in trade receivable at ~33 crs. don’t see any reason for this level of receivables for kind of the business that they are in.

Conclusion

This is all I could find on the accounting - Although I was interested in the business initially but there are several problem with the reported numbers. The high margins are entirely driven by one-time EPC (construction) income, while the actual cinema operations are struggling to stay profitable.

The H2 results will be very significant - The high margins are entirely driven by one-time EPC (construction) income, while the actual cinema operations are struggling to stay profitable.

If receivables do not decrease and recurring margins do not improve, the EPC income remains a major “grey area” with no clear competitive moat.

Hi Abhishek,

Thanks for posting your doubts. I tried to clear most of these earlier, but since you’ve shared them here again, I’m re-addressing them.

1. Connplex Recurring Income

- Ticket Income

Producer share is assumed at 50% in your calculations, but if you check historical data, it is actually closer to 43%. The 50% cut applies only in Week 1 and reduces as the movie runs for more weeks.

Based on this, Connplex makes:

0.2 × (0.57 × 25) = ₹2.85 crore

- F&B Income

F&B sales are booked in the franchisee’s books, and after all expenses, the royalty portion is paid to Connplex.

Actual F&B royalty for Connplex in H1 should have been around ₹1.6 crore, calculated in the same way as you have. However, the reported H1 royalty is closer to ₹3 crore, because some screens operate on a revenue-share basis.

In my original calculation, I have scaled numbers using only the ₹1.6 crore figure.

- Convenience Fees

There are a lot of assumptions in your calculation here. I’ll rely on management commentary and data from the PPT for my calculation.

Convenience fees for H1 = ₹1.12 crore

- Advertisement Fees for H1 = 1.12Cr

- VPF for H1 = 1.7Cr

So, total recurring income =

2.85 + 3 + 1.12 + 1.12 + 1.7 = ₹9.8 crore

This is at a time when the company had an average of

(66 + 83) / 2 ≈ 75 screens, or roughly 25 cinemas, considering screens were added gradually over the six-month period.

2. Expense occurred for the recurring income streams.

Your calculation here is wrong. These are royalty income streams, so there is no direct expense against it. Yes, basic corporate costs exist, but those don’t scale with royalty income and are largely taken care of through EPC income.

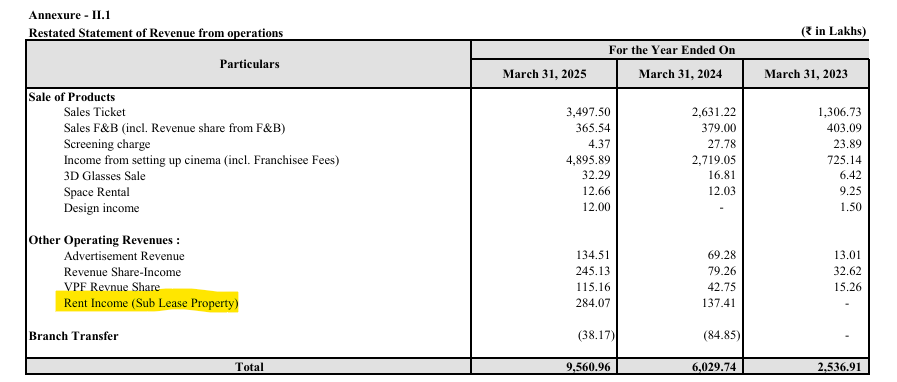

- That ₹3.87 crore shown as “rent for cinema properties” is not Connplex’s expense. It is a pass-through item because they have tri-partite lease agreements for some properties.

The rent expense you’re referring to gets offset by the rent income shown in the screenshot below, which supports my point.

So out of the blue, you’ve assumed that 50% of “other expenses” is for the recurring business, which isn’t the case. The fact that these are royalties already means the expenses are accounted for at the franchisee level. I tried explaining earlier as well how royalties work. This is where your calculations go off the rails.

- There is indeed one expense that I didn’t include in my original calculation, the manager’s salary, as I myself learned about it only later.

Which would be about = 40,000 × 6 × 25 = ₹60 lakhs.

So now, adding it all together: ₹9.8 crore − ₹0.6 crore = ₹9.2 crore.

This is the recurring income, which makes up only about 14% of revenue but contributes roughly 50% to EBITDA and profits.

So your claim that “ The high margins are entirely driven by one-time EPC (construction) income , while the actual cinema operations are struggling to stay profitable.” is unfounded and illogical.

When royalty income is suppressed from ₹9.2 crore to just ₹0.5 crore, it’s no surprise that the EPC business appears questionable.

On top of that, management itself has stated that once the operational screen count crosses 200, around 70% of income will come from royalties, which makes complete sense

3. Infinite RoCE argument.

It’s a way of looking at it. I think the EPC business makes the cinema business working-capital free and capex free, so it’s almost like an infinite ROCE.

It’s subjective. I have nothing more to add here.

4. Receivables

Your observation is correct, I have this on my watch, but I can’t take a single quarter’s data point and extrapolate it, as I said earlier.

5. All other points

Well, if you correct your calculations from above, everything else will fall into place. So I don’t want to write another 1,000 words on this, you already have my original calculation.

Even basic common sense would help here. The people taking these franchisees are business-class families in small cities. From no angle are they naive. Do you seriously think that if the payback period were 24 years, anyone would go ahead and sign such a contract? And even if someone mistakenly did, do you think they would continue operating the business? Seriously.

That said, small companies carry unknowable risks by definition, and Connplex is no different. I also have my own questions on accounting across many companies. Investment decisions are personal and change over time. What happened with your investment in Kontor is not my concern.

Finally, you are overly fixated on EBITDA margins, which is the wrong lens here, as I’ve explained above.

If you need further clarity, you should reach out to the management directly. My views are based on public disclosures and my understanding of the business, both of which continue to evolve.

Hi Vedansh, If we rely too much on the management commentaries then there is no need for independent analysis.

I have given 2 perspectives in my calculation, one is for the company and other is for the franchisees.

If you assume all the reported numbers to be true then it will further reduce franchisees share from the total income.

The more we justify the royalties income for Connplex, like you have claimed that they have revenue share agreements with few franchisees, the less will be the profits on the table for Franchisees.

Total revenue is fixed , So Franshisees income (always) = total - Connplex income

You have comfortably choose to ignore a detailed revenue break up given for franchisees, which indicates only 2.2 crs of income for H1 26 on a capex of 106 crs. This indicates a payback period of 40 years ( discounted cash flows)

I know that nobody would take such type of Franchisees, so this brings an another question whether the numbers are really true or not.

Even I don’t write another 1000 words on this topic.

Giving one more example - If we believe management’s number of 1.12 crs for Ad income then the total revenue should be ~ 6 crs. ( 1.2 / 20% ) and 10% agency costs. which makes revenue per screen/Per month at 1.33 lakhs. this doesn’t fall in place with your calculation - you have assumed 5000 per seat/year as ad income ( 5000*80/12 ) = should have been 33000 per screen/month. the deviation can’t be of 70% .

Abhishek, I have already done the calculations in my original post, which show a franchisee payback of around 4–5 years.

I mean, we can’t doubt everything; that would make any investment impossible.

Since these are small companies, the ratio of unknowns to knowns is always high. As and when clarity emerges, the market prices it accordingly.

So, like a sane investor, I will continue analyzing performance quarter by quarter.

Small companies are high-risk, high-reward bets. Also, these are promoters who have not seen full market cycles and haven’t faced intense competition yet, all of which is bound to happen over time.

Accounting, in many such companies, is more of a basic compliance exercise initially. Systems and processes evolve with time.

Accounting for all this, my eyes are always on the numbers. Personally, I’m okay with them as of now. Some others may not be, and that’s totally fine. I respect that.

Yes, we can clear it up with management. Also, the numbers involved here are too small, so a 70% deviation is not the right metric. We don’t know what the prior arrangements were exactly.

Anyway, I have assumed the lower number in my calculations wherever possible, as you rightly pointed out. So if the actual numbers turn out to be higher, that would ideally make me happier.

There is only so much information one can derive from a single concall, so I agree with you on a few of your questions. This is exactly why I started this discussion. We’ll keep these questions ready for the next call, whenever it happens.

(post deleted by author)