What makes you bullish on Emerald Finance? What is its right to win in this crowded market ?

ALL,

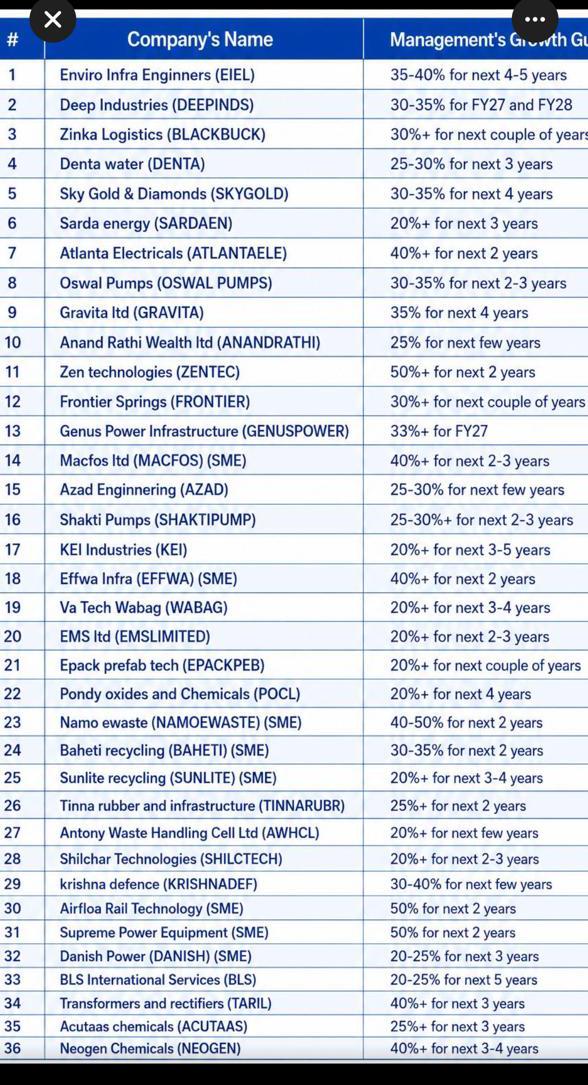

This topic is about Management giving 20% growth guidance publicly.

Do not post about stocks where you think it will do 20% while management has not stated it.

If any such posts are found violating the above guideline please flag them for further moderation.

6 Likes

I made a post here stating the names of 3 companies which will grow at 20% or more.

I did word it like this - “I think they will grow at” which I now realised is incorrect after my post got deleted. I read the title of this thread again and realised my mistake. Sorry about that.

I will merely state the MANAGEMENT GUIDANCE now. This is public guidance as Satish asked for.

-

Arman Financial - 25% AUM growth guidance for FY 27.

-

Emerald Finance - EPS of 8 guidance by Q2 end of FY 28.

-

RBZ Jewellers - Sales guidance of 2000 crores by 2030. (500 from Surat 400 from Rajkot. 600+ existing and rest 500cr from 2 smaller stores and B2B business growth - as per the breakdown by management)

Also disclosure: I am invested in all 3.

6 Likes

This thread carries a detailed discussion and analysis on Emerald Finance. I would suggest that you paste this link on Claude ask all the questions you want. You will pretty much get a summarised yet thorough answer.

1 Like

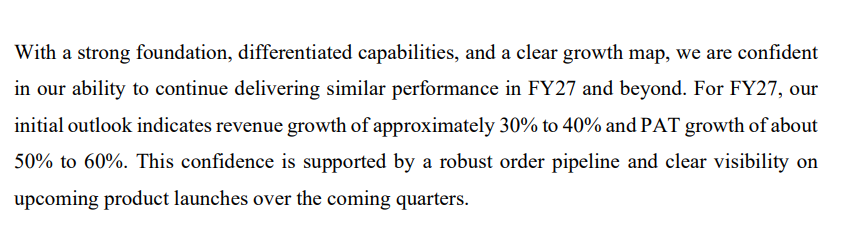

Senores Pharma management provided clear guidance of 30-40% topline and 50-60% bottomline.

VP thread on Senores:

Discl: Invested

4 Likes

NPST is projecting 70% CAGR for the next three years.

4 Likes

What is the source @Pujan_Shah

Shree Refrigerations has guided 40% CAGR for 3 to 5 years aided by industry tailwind, strategic tie-ups and capacity expansion. The guidance excludes new Datacenter vertical.

Link to Q4 concall transcript: https://www.bseindia.com/xml-data/corpfiling/AttachLive/e03070fc-2650-4efd-b33d-574e52a0395b.pdf

VP thread on Shree Refrigeration: Shree Refrigerations - SME

Discl: invested

6 Likes

Eternal has guided for 60% topline growth in Quick Commerce, 20% topline growth in Food Delivery and 40%+ topline growth in the Going Out (District) business.

Market leader in Quick Commerce. Market leader in Food Delivery.

Actively gaining share in movies from Book My Show. Market leader in Restaurant Bookings.

Quick Commerce break even achieved well ahead of peers.Food Delivery is a cash machine.

18,000 crore cash on balance sheet.

Good time to look at it. :)

4 Likes

might be good for short term, but for long term it’s a big no for me personally.

- Highly commoditised industry.

- There is no customer stickiness. If a new app with same technology comes tomorrow and says they’ll charge lesser, customer won’t think twice to shift. Same across food delivery, quick commerce.

The same cash you are talking about is sitting on mutual fund and other related investments , Other income is earned on the same, moreover question is not about earning other income , the main thing is they are buying just time by hiding behind other income because core profitability from operating business is still loss making , still at one stage if it becomes profitable, the question i ask you and other fellow members is at ‘ What Cost?’ because numbers seems to unmatch. how can someone give a valuation of 2.15-2.3 lakh crore against a mere 630 crore operating cashflow, just think about it? . However if someone doesn’t agree with my point that’s fair but on a such valuation even 6300 crore of operating cashflow is also not justified and the 6300 crore as per the economics is never going to happen. sometimes a tag of ‘Market leader’ is really unjustified because such a company is already on the moon. Hope I may be wrong.

Disclaimer - I am not an financial advisor , this is for educational purpose .

3 Likes