I would like to start this with disclaimers first.

** Not SEBI registered, DYOR

**Invested, biased and dumb

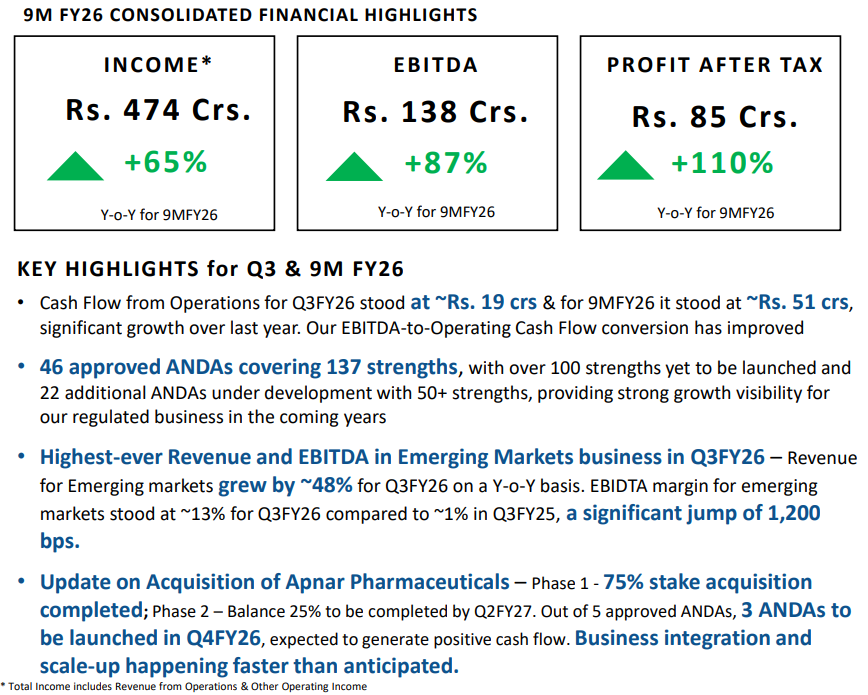

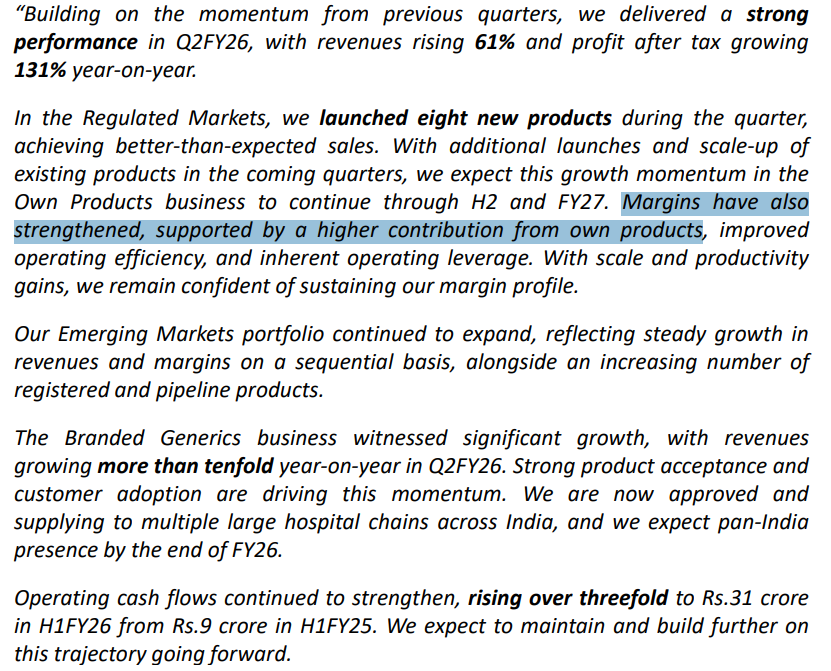

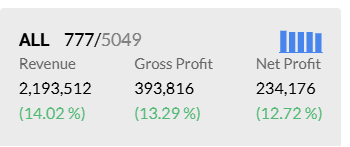

Senores came up with another steller quarter where most of the stocks are struggling, with 70% revenue growth and 84% profit growth.

EOD 29.01.202

- IPOed in Dec 2024, the business spooked interest in me after the Q1FY26 result season, when I was going thorough investor presentations and con-calls where they came out with 50% revenue and 100% profit growth guidance.

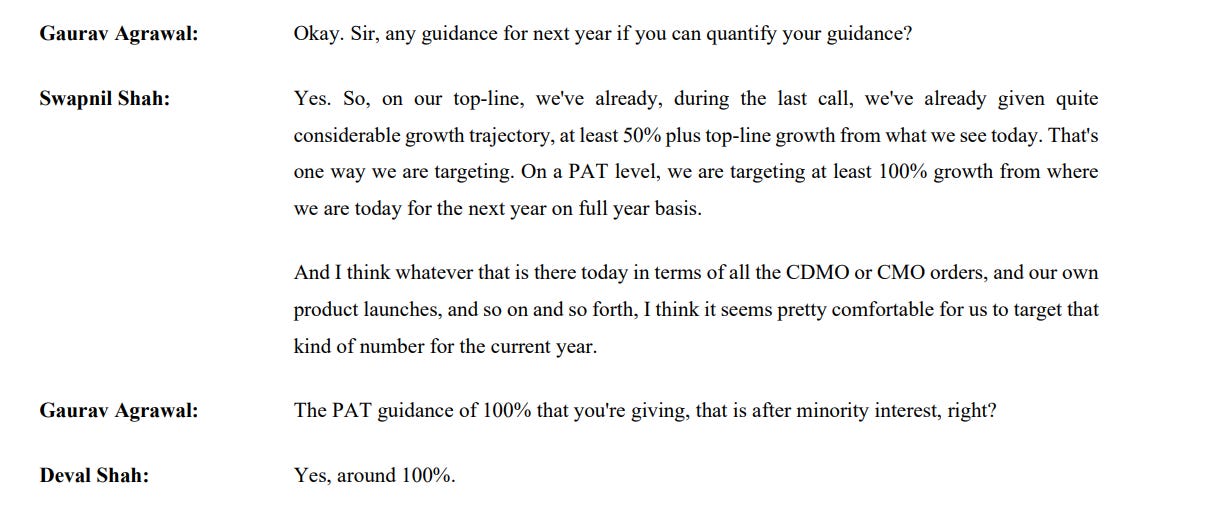

**Q1FY26 con-call

-

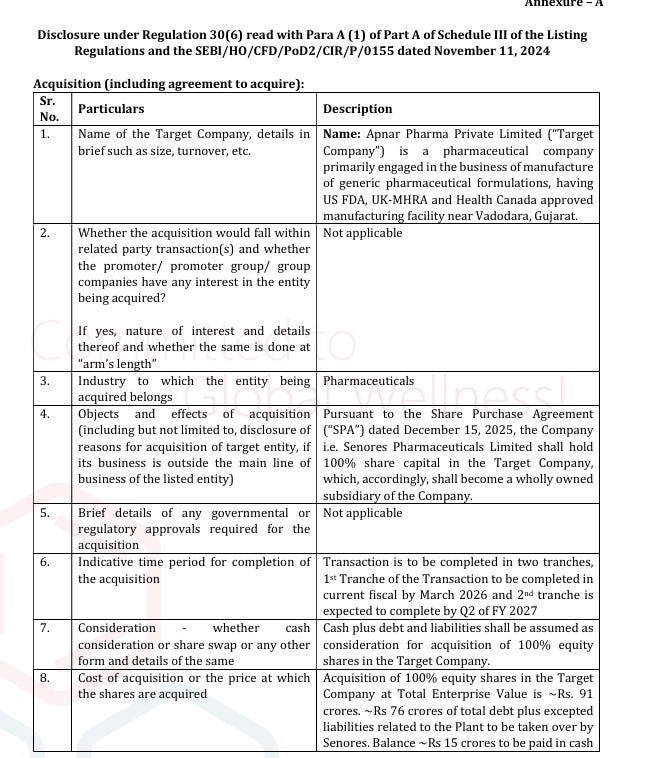

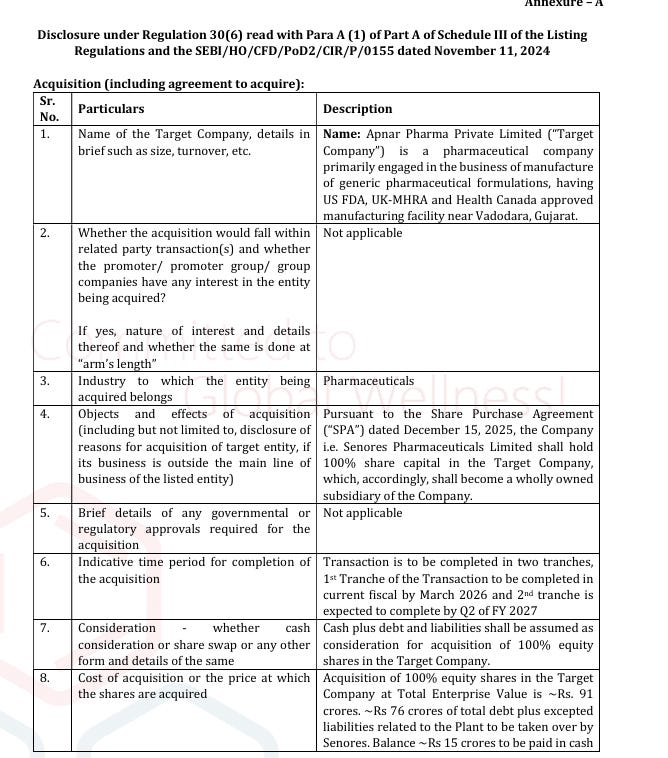

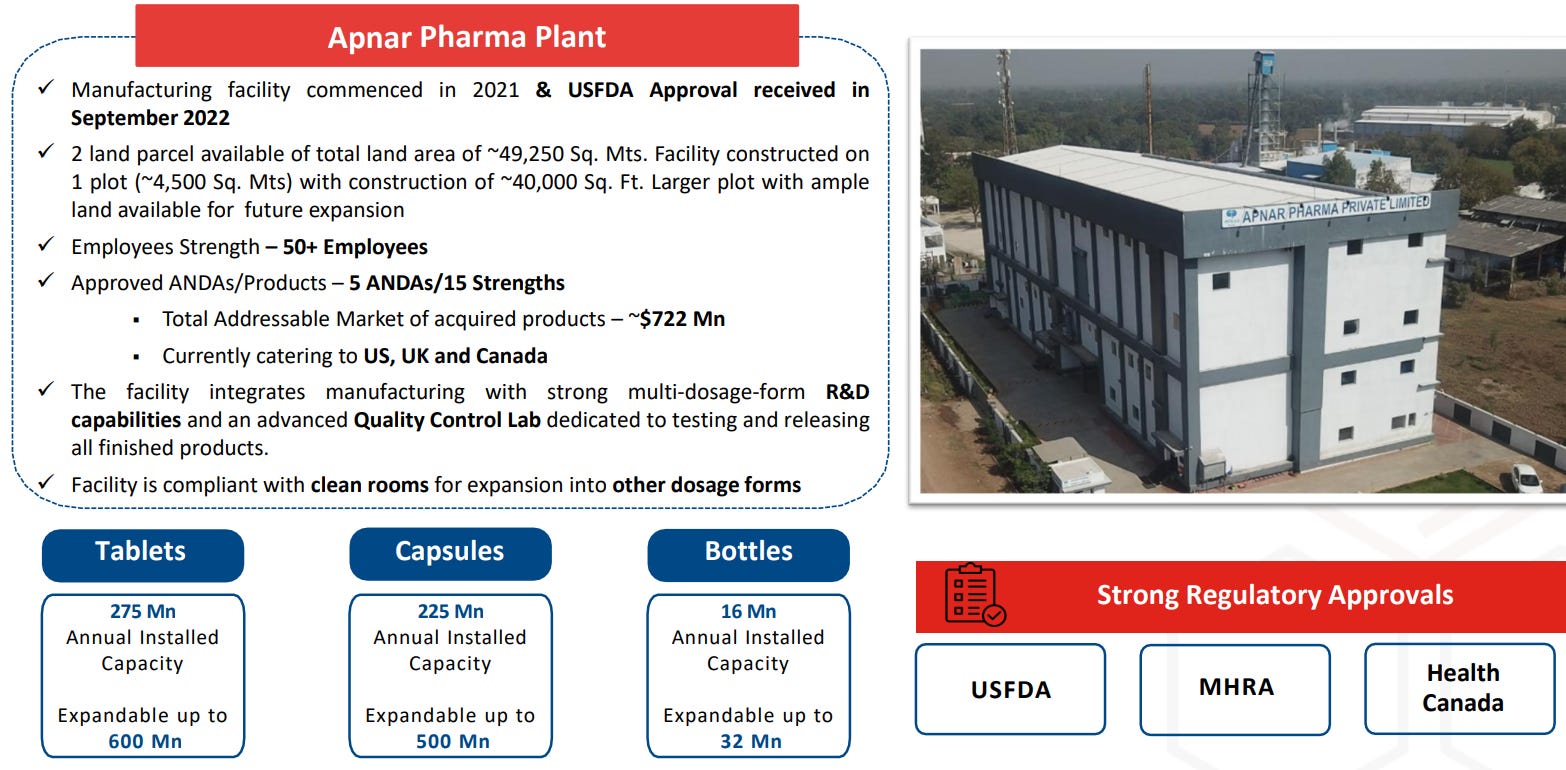

Another trigger came in on 15 Dec with the acquisition of “Apnar Pharma” at a enterprise value of Rs. 91 cr which came up with “an USFDA facility in Gujarat (commissioned in FY22), one plant in USA, has 5 ANDAs”- can get 100 cr revenue in FY27 with 30% EBITDA, 250 cr in FY28.

Business model:

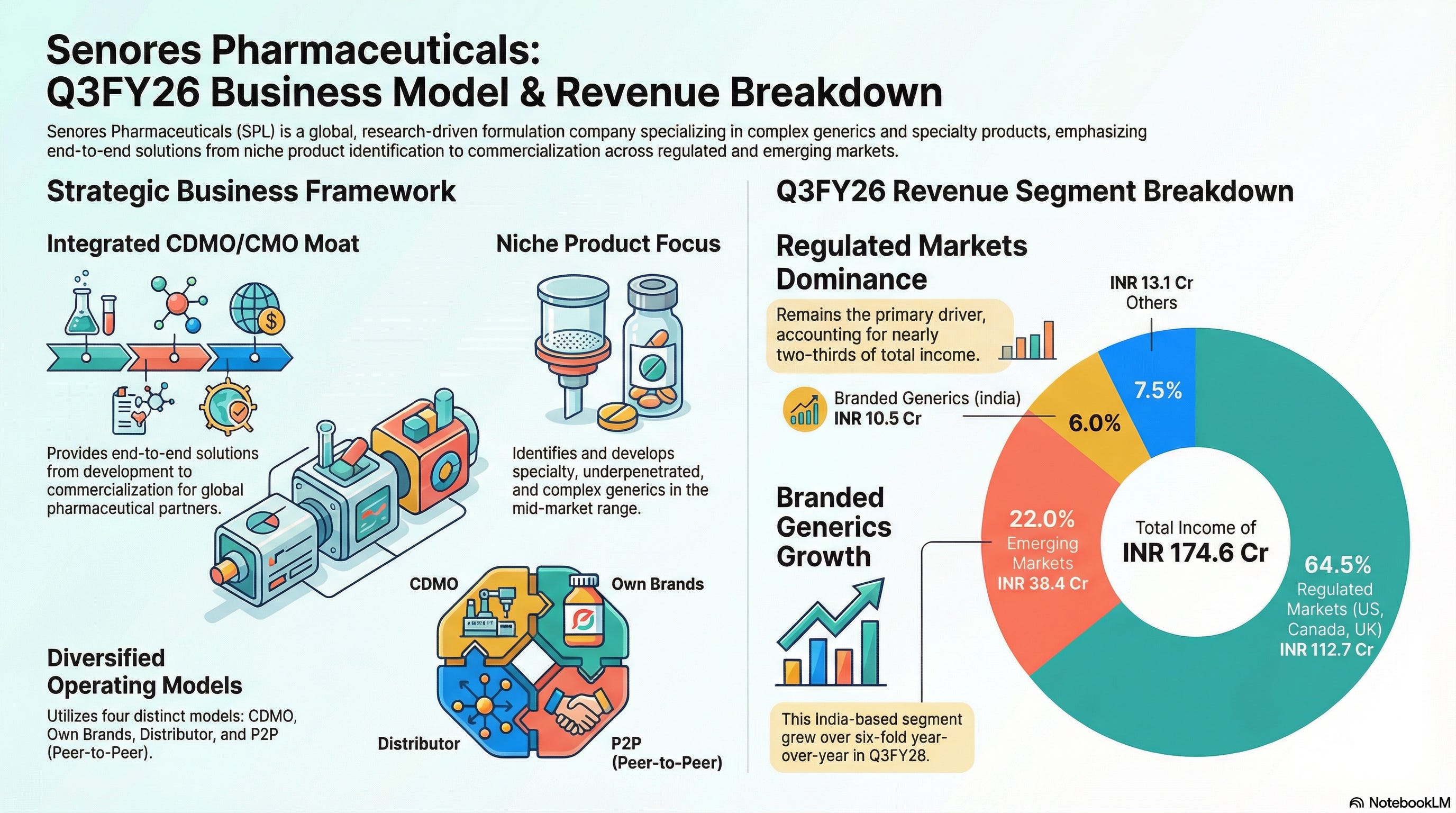

SPL is a global research-driven pharmaceutical company that develops and manufactures pharmaceutical products for the Regulated Markets of the US, Canada, and the United Kingdom across various therapeutic areas and dosage forms, with a presence in Emerging Markets. The company develops and manufactures specialty, underpenetrated, and complex pharmaceutical products. It also manufactures critical care injectables and APIs. -Screener.in

**Here is a visual to help you understand the business model a little better.

-

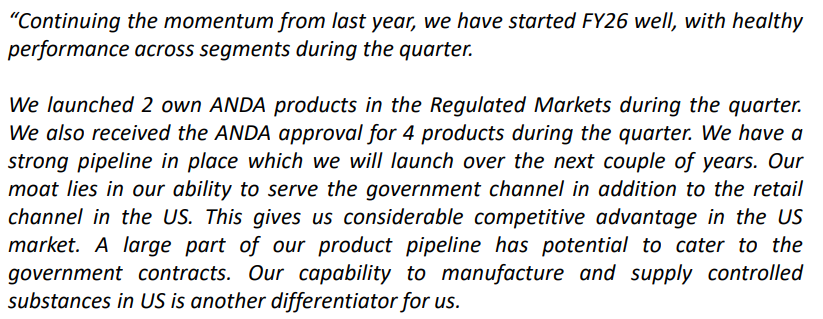

The management is on track with the guidance and will probably overshoot it if we take an estimate.

Q3 Investor presentation & concall snippet-

-

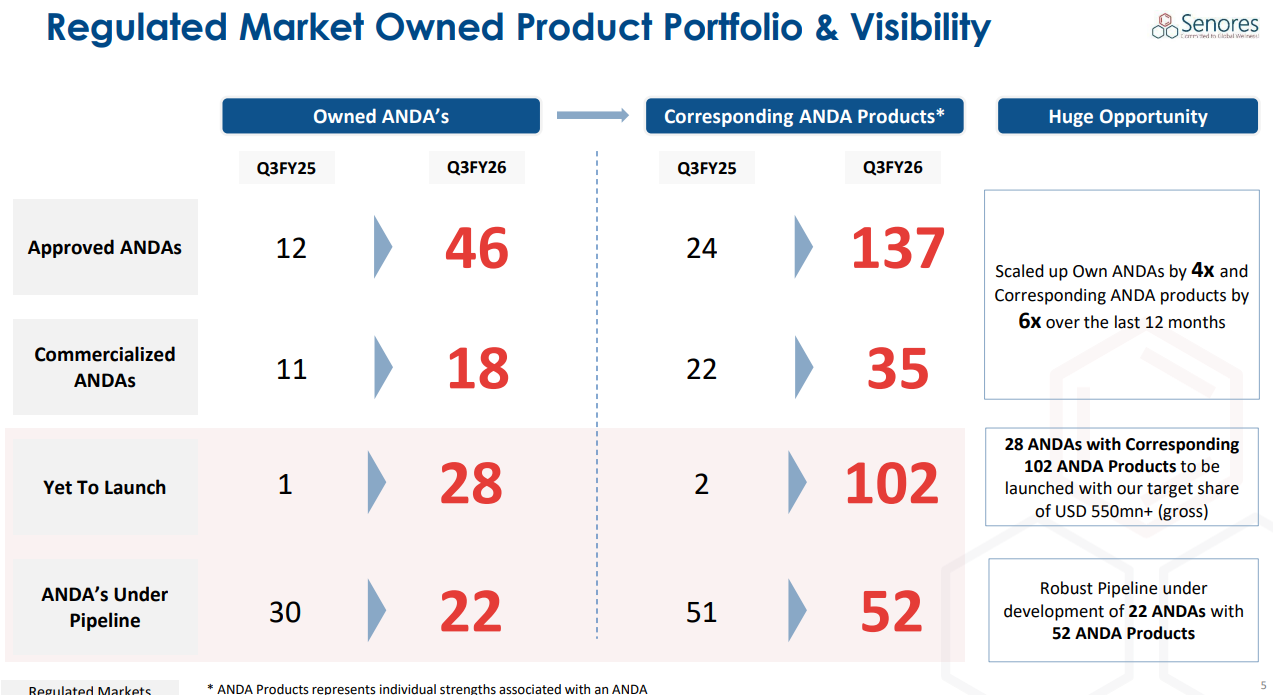

The company has 46 approved ANDAs covering 137 strengths, with over 100 strengths yet to be launched and 22 additional ANDAs under development with 50+ strengths

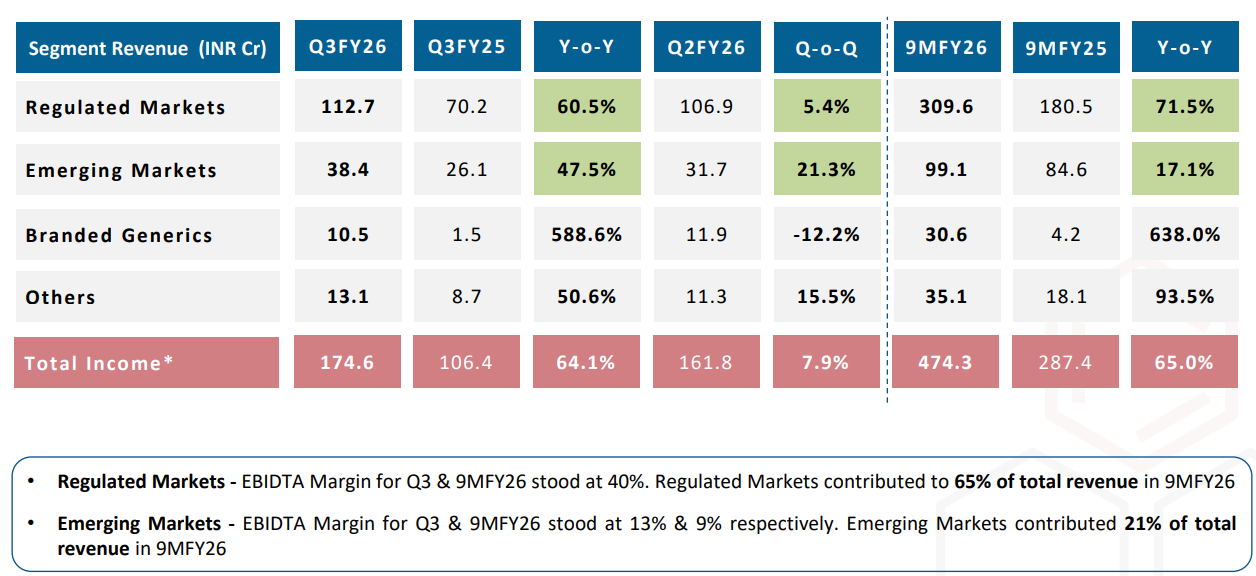

- Revenue breakdown as of Q3

- Facilities before Apnar

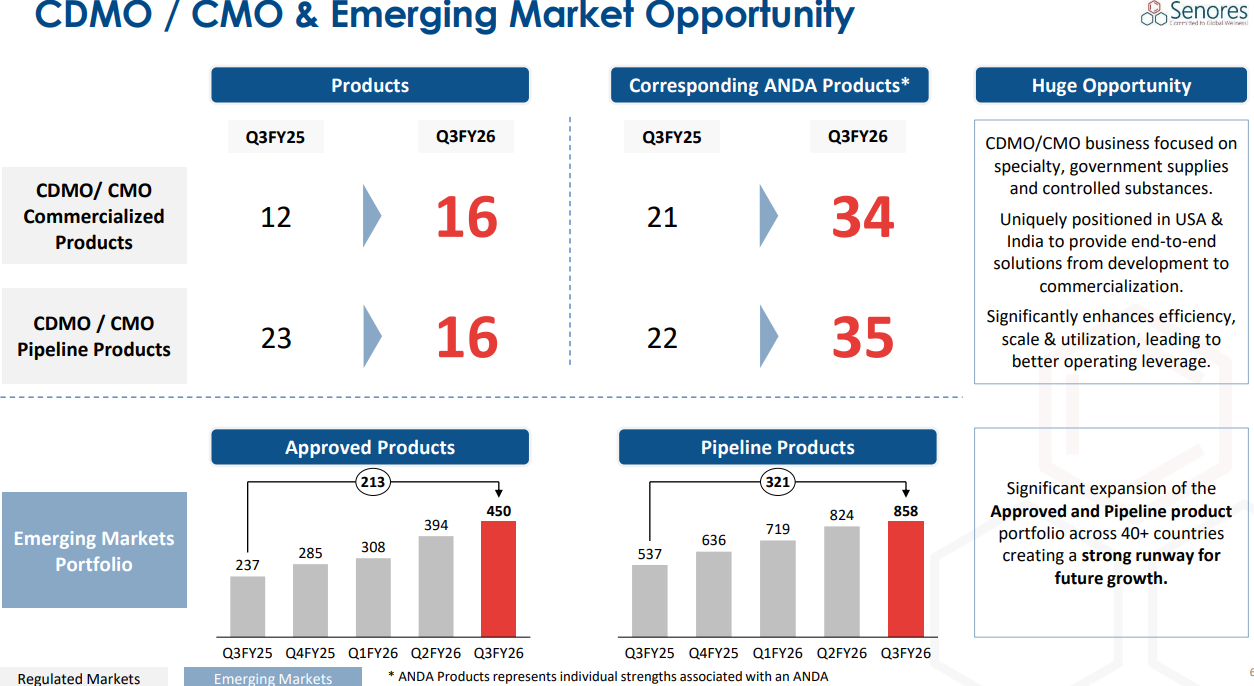

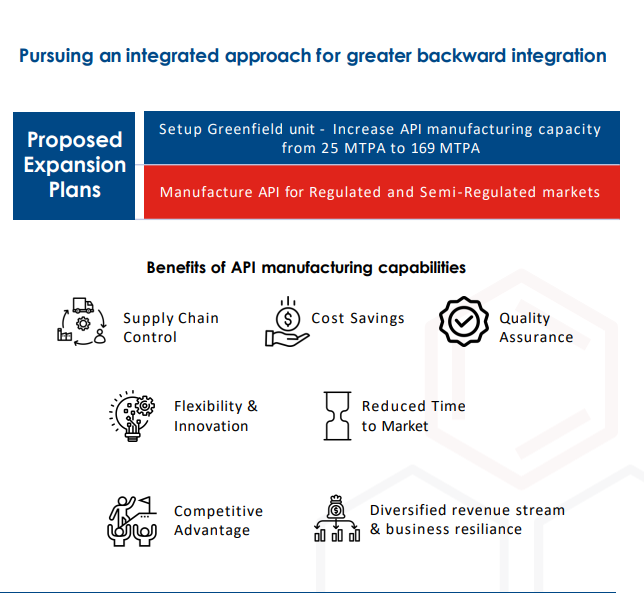

- Planning to backward integrate in API

-

The company finally became cash flow positive with operating cash flow of Rs. 51 cr.

-

120-150 cr revenue possible from Apnar in FY27.

-

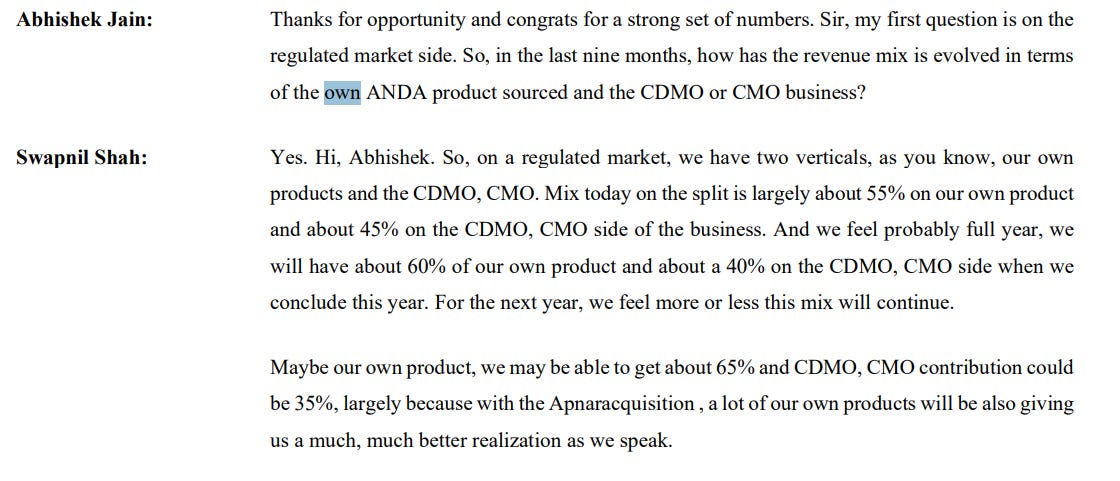

In regulated market, own ANDA products contributes to 55% of the revenue which has 4-6% more margin than CDMO/CMO, which will set to go to 60% in FY27.

-

The 40% EBITDA margin is sustainable and even can improve by 1%.

-

The managemet will provide FY27 guidance after Q4.

Key management quotes:

“it’s always better as a management to remain a bit conservative”

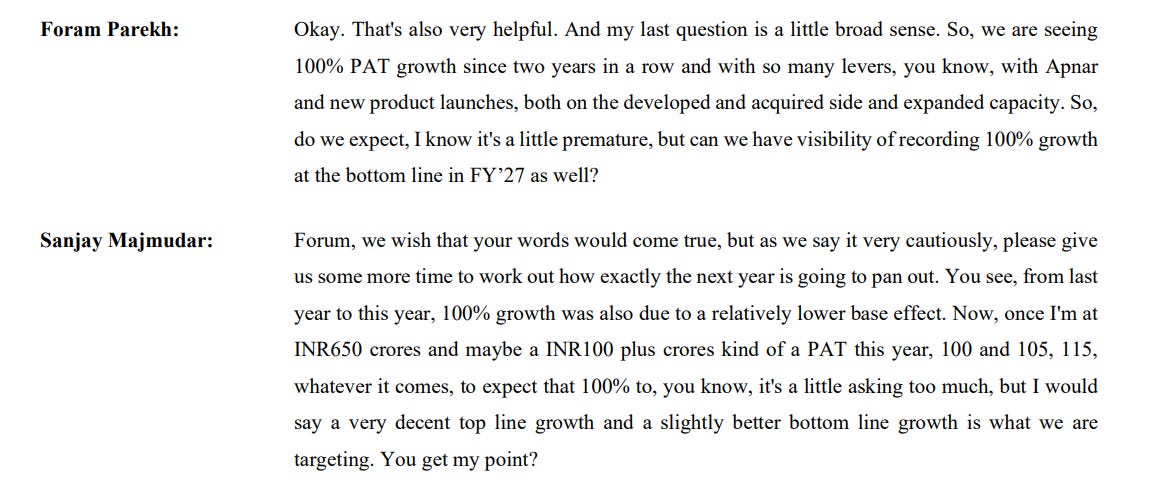

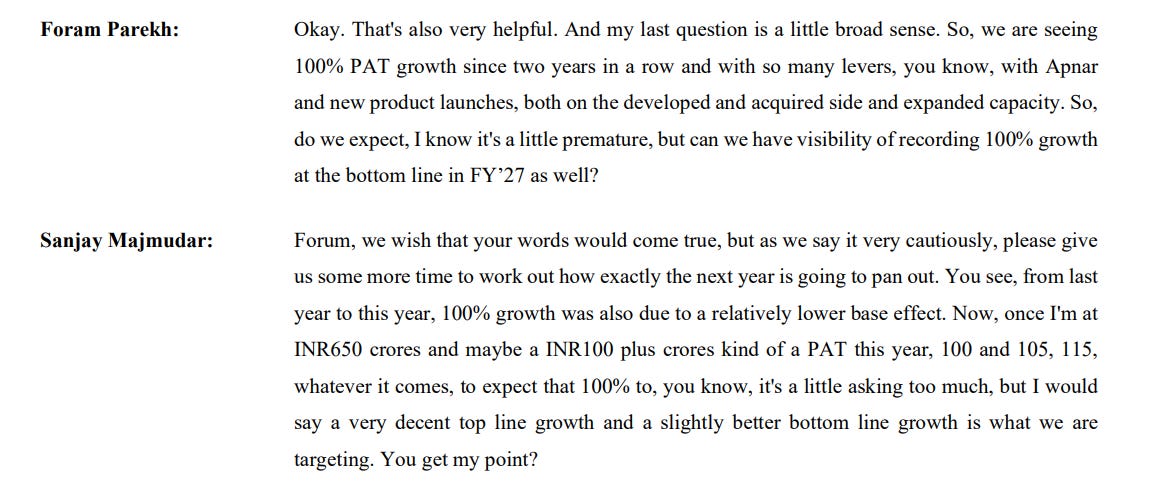

“to expect that 100% to, you know, it’s a little asking too much, but I would say a very decent top line growth and a slightly better bottom line growth is what we are targeting”

Beyond Q3 & closing thoughts:

-

The management is walking the talk staring from the IPO although it’s only been a year since the IPO.

-

Acquisition of Apnar pharma and Zoraya platform seems really strategic and well planned and can be a great revenue booster.

-

The management has already warned about the pace of growth coming down due to base effect which shall be confirmed after Q4 results and conference call.

.

-

-

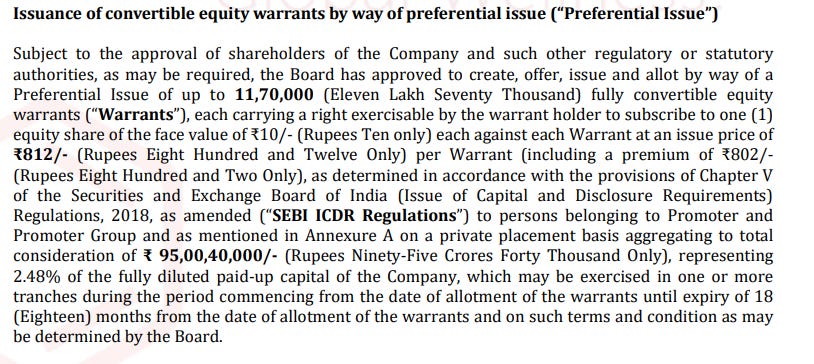

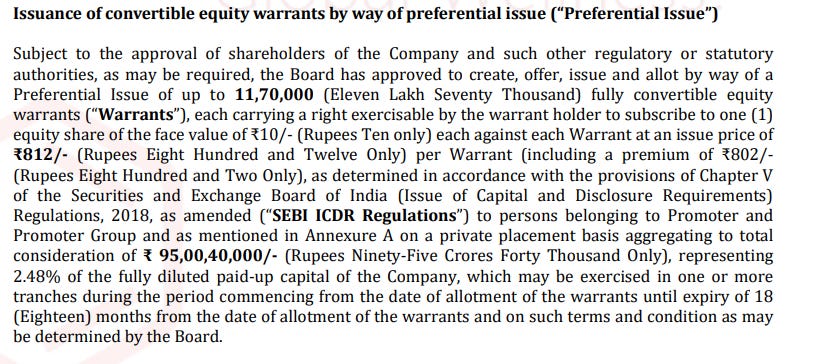

The management has issued warrents worth Rs. 92 crores by preferential issue at a price of Rs. 812 to for product acquistion and working capital requirement

** Thank you. And feedbacks are welcome