Source? Did not see in their concall transcript - https://www.bseindia.com/xml-data/corpfiling/AttachHis/2e63d207-a628-43f3-b3ad-49088a4242ca.pdf

Marksans Pharma promoters are confidently saying a revenue of 3000 cr in 2 years, which is 50% growth. But they are conservative in their claims and has over delivered. And Teva itself can deliver 1000 cr revenue in 2 years and Capex is still in progress. And they are claiming that it is already break even.

So these are projections as the case of all other companies in the list.

5 Likes

Hello. Is there a link you can share of the source? Thanks

1 Like

Go through the concalls , you will get all the details.

Here is a simple rule that helps identify companies that will deliver 20%+ profit growth on a PORTFOLIO level in 3-5 year horizon. Rule: “Select all companies that have delivered more than 14% ROE and 20% revenue growth in at least 7 of the last 9 years”. This rule has generated 20%+ annual return when tested on rolling basis from 2000 to 2023.

Below is the list of the companies that appeared in FY23:

Hindustan Foods

SBI Cards

Avenue Super.

Lancer Containe.

Husys Consulting

Aditya Vision

Share India Sec.

Beta Drugs Ltd

Route Mobile

Affle India

Aaron Industries

Sigma Solve

Clean Science

This list contains both small and large companies.

For more detailed rules and examples, check out this thread on investment rules where we discuss best investment-rules in India tested across market cycles over the last 25 years.

12 Likes

Hi Prabhat, iam holding marksans since few years, and I can surely say company will cross 3500CR revenue by FY26 and even more because management has always been conservative in giving targets.

Wise Travel India Ltd

Transport company that offers car rentals and transportation services

ROE and ROCE 3 year more than 30

Client

Nokia, IndiGrid, Amazon, Microsoft, Tesco, Vedanta, Indigo, RBS, CocaCola American Express, Renault, LinkediN, Hitachi, Cheli, Sapient, Panasonic, etc.

Future Plans:

=> Company is Targeting sustainable growth of 30-35%

=> Planning to expand EV fleet

=> Debuted internationally in Dubai in 2023, focusing on innovation, customer service, and eco-friendly mobility.

6 Likes

This is an excellent thread for capturing growth companies but we should take management guidance with a pinch of salt in this current bull market. I would request people to also post company management’s past guidances and how much they have delivered on their promise. Are they really walking the walk or just talking?

16 Likes

Growth has been good and company is mainting healthy balance sheet. but they have not given future giudance or there long term targets. can put small amount and track story and gradually increase investment.

P.s. just googled and saw reviews. mostly given 1 star by most users. overpriced and not up to the mark service.

What diffrent work they are doing from smaller travel agency and like ola uber service ,is there any diffrent buisness model they have?

Caplin point has also guided for 20%+ growth for next few years. However, people have a bit of concerns regarding its cash balance on books.

Shankara builpro also has guided by 20% growth for next 2-3 years, however for Q1 though EBITDA did grow by 20% but they have high finance cost & hence flattish PAT growth. The same is expected for next few quarters.

5 Likes

Sundeck’s reality guided for 30% sales growth and stated it is a conservative estimation.

Their Dubai reality project has good potential for two to three years.

They operate in luxury residential areas, which is a hot cake nowadays.

Please read the q1 25 concall transcripts for more clarity.

Have invested and biased views.

2 Likes

Can’t open it.

is this the post you were talking about @Sid_Mathew? Found it somewhere else…

Also @Jimmy_Kagathara what’s your view on the veracity of this?

5 Likes

Yes that was the post. Had found it while researching the company. Had also found this.

1 Like

So this is not an issue right?

Can you share the proof that management has cleared these allegations? Don’t just write for the sake of reply. Please provide details.

3 Likes

Can you kindly highlight what CG issues Caplin Point has ?

I looked at operating cash conversion for the past 5 years it looks fine, net cash company , no family on BoD.

Not sure if I’m missing anything

5 Likes

I do not have any evidence of CG issue. However, generally I do not prefer companies with multiple subsidiaries in its structure.

Disclosure; My views are only for academic discussion and not recommendation to buy or not to buy or sell or hold.

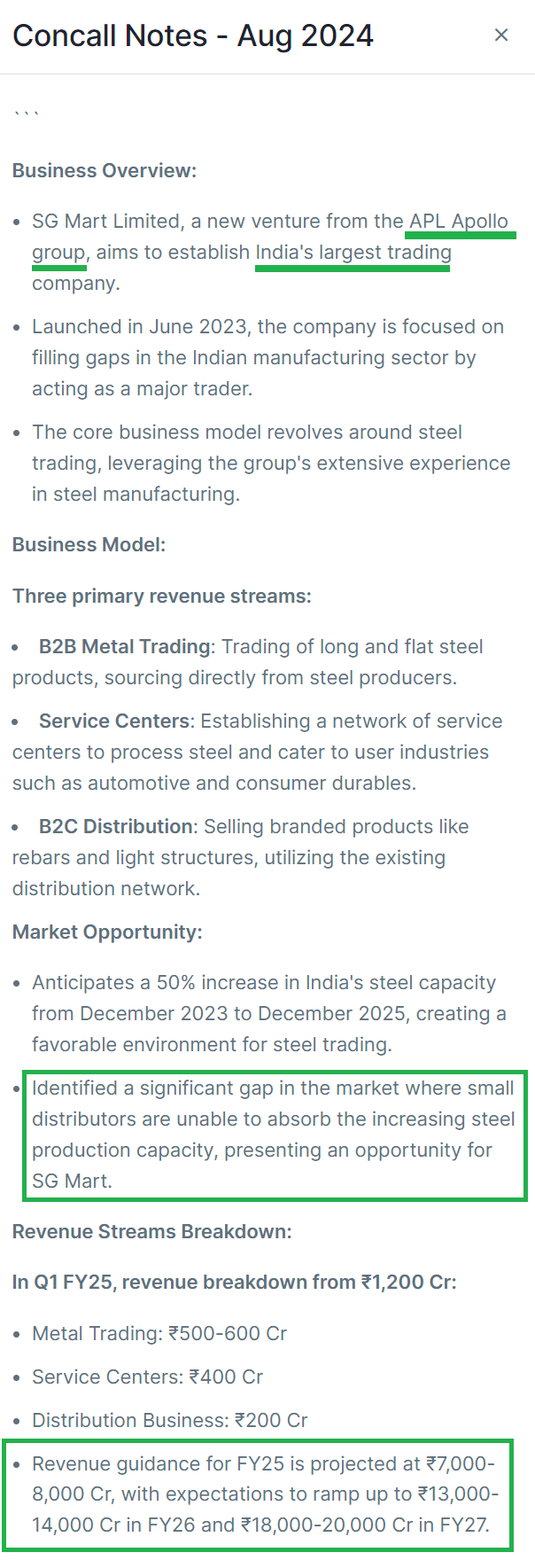

SGMART

FY27 revenue guidance is around ₹18,000 crore, with an estimated net profit margin of 2%, leading to a projected PAT of ₹360 crore. Given the current TTM PAT of ₹87 crore, this represents a potential 4.5x increase in PAT over approximately 4 years. If the company successfully establishes itself as an organized player in this unorganized sector, it may potentially become a long-term multibagger.

Disclaimer: recently added and biased.

9 Likes

Has anyone here used SOVERENN who claim to find multibagger stocks early on.