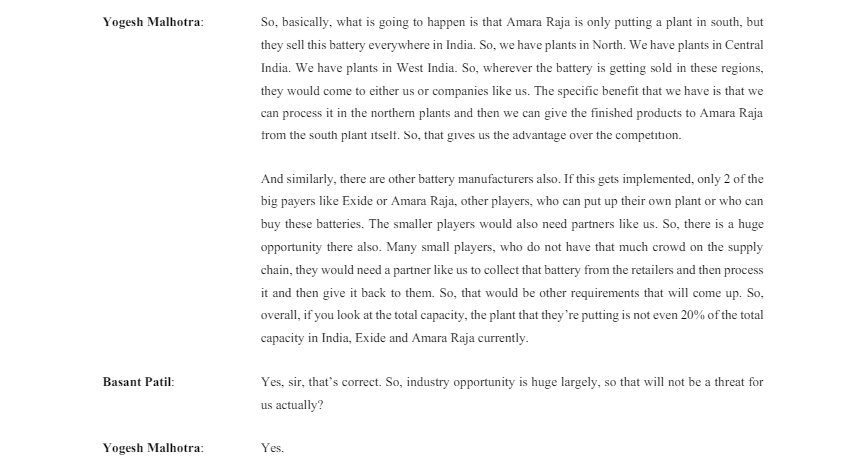

Posting a snapshot from the Mgmt concall in May 2024 on this question:-

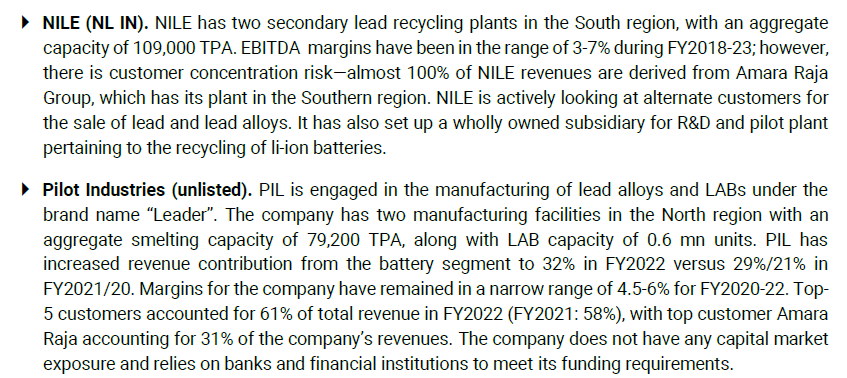

My personal view point is that companies like NILE and Pilot Industries should be impacted more which have a major dependency on Amara Raja Batteries for their sales. They are geographically also less diversified.

Credit: Kotak Securities.

Gravita should do much better considering the global network and diversification.

3 Likes

Hello,

Just adding my 2 cents to the community on what businesses I’m studying currently and interested in adding to my satellite portfolio with 20%+ growth anticipation. Will really appreciate the views of the community:

- Landmark cars

- Rolex rings

- SJS enterprises

- PVR INOX

- Dreamfolks

- City union bank

- Steel strips wheels

Will love opinions of the community members.

5 Likes

Those are some intresting finds.

I have doubts over landmark cars delivering growth in excess of 20%.

Unless growth comes majorly from expansion.

Rest of the themes seem fine to me in terms of anticipated growth numbers,

P.s: I could be wrong.

1 Like

Some companies targeting 20%+ growth (after Q4FY24 results):

Goodluck India

Maiden Forgings

BEW Engineering

EMS Ltd.

Shivalik Bimetals

Yatharth Hospitals

Kilburn

Pondy Oxide and Gravita India

Izmo

Ritco Logistics

Osia Hyper

Jyoti Resins

Galaxy Bearings

10 Likes

Found Osia Hypermart interesting (Dmart type business), but on digging deeper found many corporate governance issues.

Number of public shareholders increased by 500% in last one quarter from 6k to 38k. Looks like a pump and dump story in fact.

Negative operating cash flow, company never generated any cash flows from operations.

Lot of related party transactions. Rents and loans to directors.

Promoters stake is down almost by 20% in last 4 years. Announced another right issue recently.

8 Likes

My reasons:

Only major reason for including Landmark cars:

Also, I expect that since it is onboarding Mahindra too, that will be a good growth engine. Can’t say for sure though…

Rolex Rings: Overall bullishness in the sector plus this particular company seems a proxy to the sector.

SJS enterprises: The company have been able to achieve its guidance in the past. Hoping it to continue to do so. Plus it’s less cyclical than Auto industry and a kind of proxy to it too(I don’t know why am I more interested in proxy companies).

PVR INOX: variant perception. A contrarian bet since sector is ignored and in extreme pessimistic perception right now. I think the culture of OTT is different than cinemas and they both will have different place in the market (as against the view that OTT will kill cinemas).

Dreamfolks: Proxy to aviation and credit card industry.

City union bank: Conservative management. Reversion to mean framework. Hoping for the market to realise this company’s value.

Steel strips wheels: Alloy wheels market increasing rapidly. Company doing capex for Alloy wheels which is actually a high margin segment.

4 Likes

According to their guidance, Krsnaa Diagnostics and Sunteck Reality can easily achieve more than 20% sales growth in the coming two years.

Expecting the growth to be tepid for the next year. CV industry volumes are expected to remain flat or show minimal growth in FY25, which can impact overall volume growth for the company. However, expecting the margins to improve over the next few years due to higher mix of alloy wheels.

3 Likes

The thesis is playing out quite well. Gave a major break out yesterday. ![]()

1 Like

I had kept Jyoti resins in my portfolio for a long time. However, I dumped the stocks after realizing that the cashflows are subdued and not in line with the income this company is reporting.

Cashflow from Operations is a mere 25% whereas the benchmark is ~80%

2 Likes

I am a bit curious to understand why you have picked City Union Bank? What are it growth drivers?

The management has been very conservative in disbursing loans(which should actually be a good sign but that has led to slow growth) but now they want to go a bit aggressive. Plus the revenues, financing profits, and net profits have risen consistently but the share price has not inculcated the growth in last 5 years. NPAs are controlled and declining on both QoQ and YoY basis. I tried but couldn’t find any major red flags in the company.

So, the main reason is the valuations (one of the lowest price-to-book multiples in the industry currently). I really think that when banks and financials start to give a run-up, city union bank will benefit from 2 way- reversion to the mean industry valuations, and sector bullishness.

4 Likes

Suggest doing more deep dive on dreamfolks. While I was studying in the past, noticed mgmt did not live upto its guidance/sayings - I also recollect references to this on this forum (thread on dreamfolks)…check out

1 Like

Here is one great but older blog by Tar

I hope it helps.

1 Like

Hi everyone.

Great to see this trail. Adding few businesses that are projecting >20% growth in the next 2-3 years

-

Supriya Life sciences - INR 1,000 Cr revenue by FY27 (FY24 - 570 cr)

-

Muthoot Microfin - 25-30% growth for FY25

-

Sky Gold - INR 10,000 cr of revenue by FY27 (FY24 - 1745 cr)

-

Lincoln Pharma - 15-18% growth for next 2-3 years (P/E - 13x)

Would love to hear your thoughts on them.

13 Likes

3 Likes

Good compilation of 100+ ideas

https://x.com/EquityInsightss/status/1812341460773355980?t=QX65K7j6C4wA2Luys56FCQ&s=08

24 Likes