This question for cement sector is well analysed here Cement Sector Preview | Bag of mixed fortunes; strong demand gets overshadowed by high operating costs

2 Likes

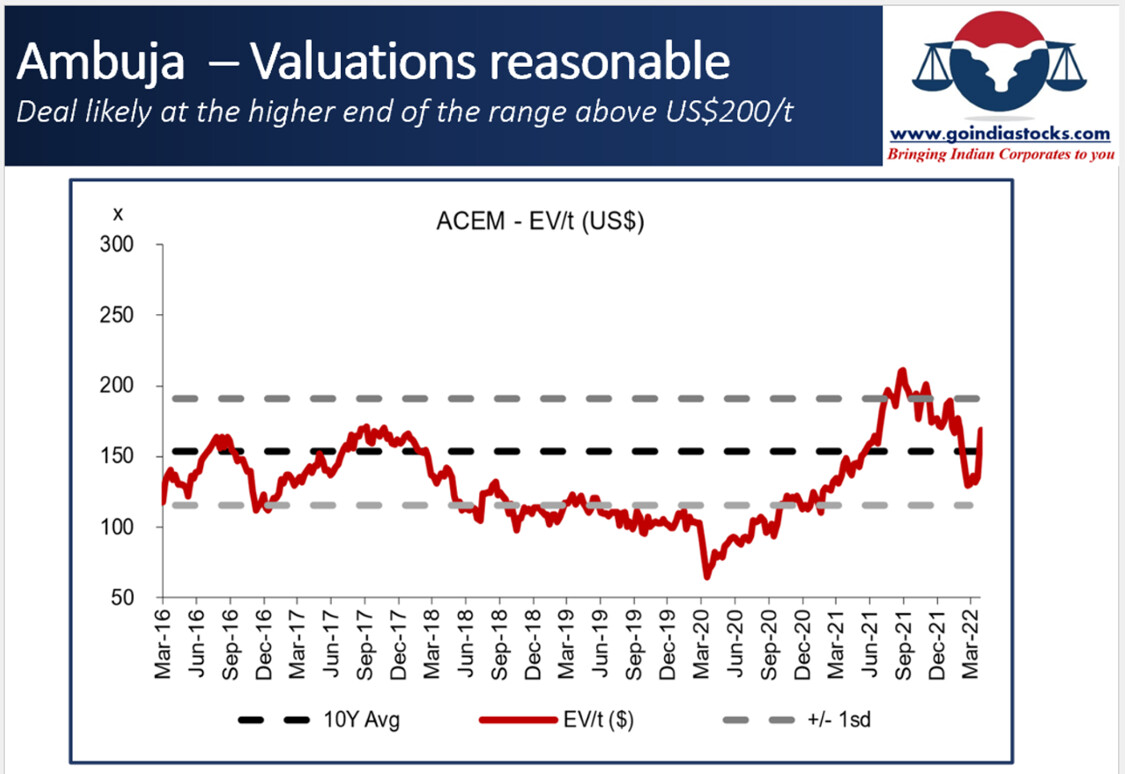

Lots of buzz around Holcim exiting India and selling it’s stake in Ambuja. Most acquisitions in India in near term have happened between US$100-130/t. However, all those were small units with no brand appeal. Ambuja is a once in life time opportunity. Currently stock is trading at US$169/t. Very unlikely deal will happen below US$200/t

Source: Speculating on Speculation...

7 Likes

Looks like Hindustan Zinc is available at a discount compared to the underlying commodity.

2 Likes

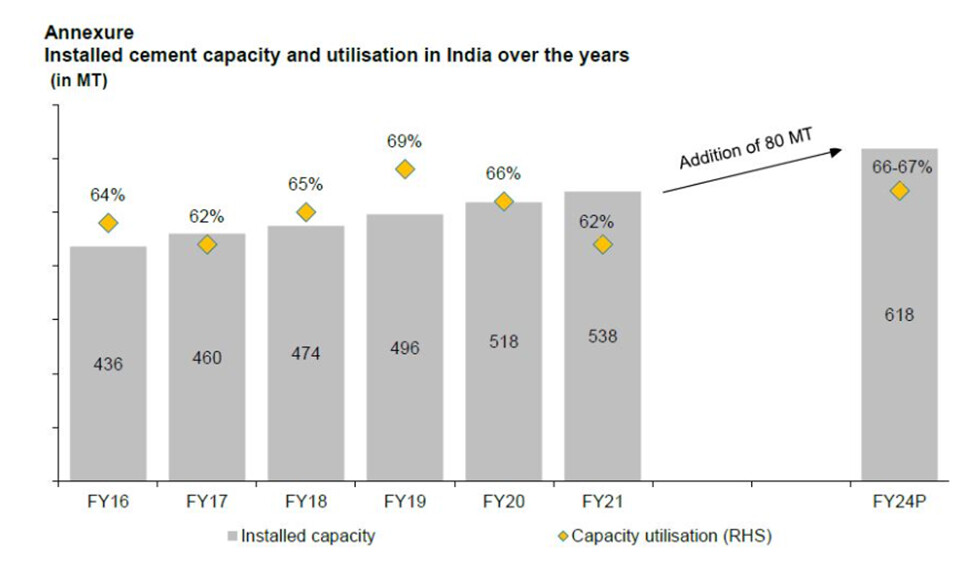

Cement industry is pressing the pedal on capacity additions with 80 Mil ton expected through FY24.

Source: Crisil

Govt’s impetus on infra & housing projects, Bharatmala projects, housing for all, rapid urbanization and rising rural income, interest rates on housing loans at historical low are some of the key drivers of increased demand.

Ambuja cement has disappointed in volume growth in the past but now, new capacity additions and cost improvement programs (I CAN and master supply agreement with ACC) are yielding results.

- Greenfield plant with 3.1/1.8 mtpa for clinker/cement at Mundwa, 1.5 mtpa grinding capacity expansion in Ropar leads to 15% additional capacity

- Master supply agreement with ACC allows raw material swapping between the two. As per agreement both the companies offer 5% discount for cement supply to each other on their average net selling price. Agreement provides better logistics efficiency leading to lower freight cost. PBT improvement can be seen from FY20 onwards.

- Waste heat recovery system (WHRS), solar power plant, coal mining from Gare-Palma IV coal block lead to improved EBITDA/ton figure.

Current WHRS capacity is 6.5 MW and now ACEM plans to commission 54 MW capacity in HP, Chhattisgarh and Rajasthan. Current solar power capacity is 5.53 MW, now adding another 23.5 MW in Gujarat and Chhattisgarh. Other cost saving strategies include underground mining from Gare-Palma IV coal block, mining lease for long term limestone requirement.

A merger between the two companies would further lead to supply chain optimization and reduction in fixed costs. While other players have aggressively added capacities in the past, Ambuja has been lagging in this regard so a lot depends on the execution when it comes to 50 mtpa capacity guidance.

Earning power value: I calculated Ambuja’s value assuming-

- No future growth

- Company needs to sustain only current profits

i.e. adjusted earnings describe the sustainable level of cash flows that can be distributed to shareholders. it was trading near this price in March 2022.

Disc: Invested

4 Likes

Cap Goods - Quiet a few companies we track and own have all-time high order books. Significant order book is exports. I think exports will do very well. Domestic demand also coming.

Cement - Is a 2-3 year play. Cement demand will only improve from here. Valuations are favorable.

17 Likes

Just a view on the extent of the coal prices in international market. They are up by about 200% to the highest level of previous 10 years.

7 Likes

Can any one explain why the refinery stocks like Chennai petroleum, mangalore refinery Has given good appreciation in price?

From the news I could see increase in Singapore grm. Not sure about it.

3 Likes

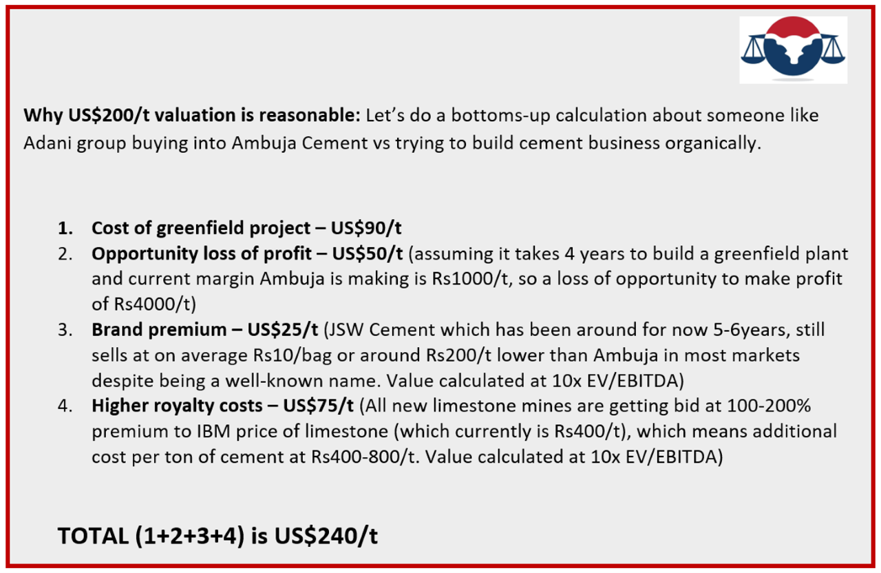

Was trying to compare whether building a cement plant organically at US$90/t is cheaper or buying Ambuja from Holcim at US$200/t? Surprising results

Source: when US$90 is greater than US$200..

20 Likes

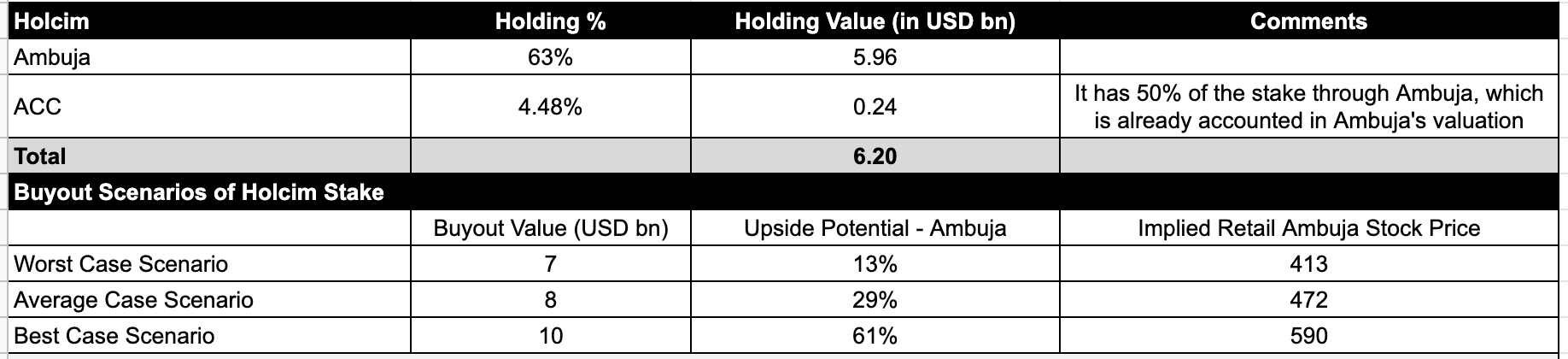

IMO, stock price of Ambuja has significant upside potential, which should unravel in the next 6-8 weeks.

Holcim stake sale is likely to happen between US$ 8-11 bn, and even a worst case deal size of US$ 7 bn should lead to decent upside, without factoring the following tailwinds:

- Merge possibility of ACC & Ambuja

- 1% of revenue was paid as royalty to Holcim which can now be discontinued

- A more active promoter

Would happy to understand if I am missing something here

Disc: Invested, and adding positions.

Reference link: Adani Leads The Race To Buy Ambuja And Acc With $13.5 Bn In Kitty | Mint. This is not a recommendation.

9 Likes

How is demand supply scenario in electric equipment,industrial equipment and compressor pumps

@jitenp , you’ve mentioned Capital Goods sectors having tail winds… cursory look and the sector seems so diverse… could you please detail on the sector… or any pointers would be helpful too… thanks ![]()

There are a few major reasons why only reffinery but not marketting company’s like Chennai Petro and MRPL shares risen/rising.

1- These are only refinery companies and not a marketting companies (OMCs), so they have no burden related with lower marketting prices, like IOC, BPCL, HPCL or Reliance.

2- Rising crude prices given positive inventory valuation gains.

3- Due to Russia- Ukraine war few global refineries stopedproduction and alongwith higher crude prices Singapore GRM rising heavily.

4- Last and most important. Excise duty cut in Nov.21 by govt. Rs.10 per litre on diesel and Rs 5 per litre on Petrol has improved their Ebidta heavily. You can check it from their March 22 and Dec.21 qtrly results seeing Excise duty cost to revenue percentage.

In Chennai Petro this gave over 1000 crs extra Ebidta.

I belive saturday the 21 May 22 further excise duty cut should further boost their EBIDTA and PAT remarkably and June qtr’s GRM is also around 10USD higher than March Qtr, so very likely June qtr results can be better than March qtr.

Disc: I am holding both shares in my portfolio.

8 Likes

Does anyone has concall transcript or Audio of Chennai Petro.

Pls share.

Does anyone have any idea why Chennai Petro and MRPL Shares falling (Everyday lower freeze) just after Excise duty reduction on 21`st May 22.

Some mkt rumours says Govt is considering to announce windfall tax like U.K did, taxed by 25% on profits, if Crude prices go above certain level.

Here i want to say such duty can be put only on oil (crude oil) producing companies like ONGC and OIL, Reliance, Vedanta etc but refineries should not come into that bracket.

Pls let us know the reason of fall in share prices of these two stocks.

2 Likes

Article in a daily on paper industry

PaperInd.pdf (72.9 KB)

@jitenp , Texmaco and Titagarh Wagons. They both have garnered orders worth 4-5x their annual revenues. Trading at near book values. Mcap less than annual turnover. Sounds too good to be true… please guide on wagon manufacturers… and on rail expansion play in general…

4 Likes

Any idea about why these oil stocks are up: Chennai Petro +15%, MRPL 20% up today. Oil India +13% since last 2 session. In news:

Because expectations are that oil prices will remain elevated for a while.

This is a long thread but explains it beautifully. Basically US and Europe are woefully short of refining capacity and existing refiners in various parts of the world are enjoying record refining margins. And refining capacity is not easy to set up fast. So the high margins may sustain for a while. Have a look at the chart of the refining margins in this tweet.

4 Likes

Thanks, beautifully puts it into context!