This is a lovely interaction with Kenneth Andrade where he explains the capital cycle theory with Indian examples. The cleanest presentation I have seen on this topic, a must watch.

This is a lovely interaction with Kenneth Andrade where he explains the capital cycle theory with Indian examples. The cleanest presentation I have seen on this topic, a must watch.

Hi everyone, wanted to discuss a query on Jindal stainless. Nickel prices have shot up massively in the past few days. According to the latest filings, Jindal stainless maintained an inventory of 3767 crs. against sales of 5027 crs. for the quarter ended September 2021. This comes out to be nearly 75% of quarterly inventory. And in this time period JSL hasn’t moved much. Is this a good way of benefitting from a significant inventory gain due to Nickle? or is my assumption wrong?

Usually there will be some pre-booked orders also against this inventory. So the inventory gains may be limited. And in medium term it doesn’t matter as those gains will be lost when nickel prices comes down. In fact with sharp increases in Nickel prices, demand might crash.

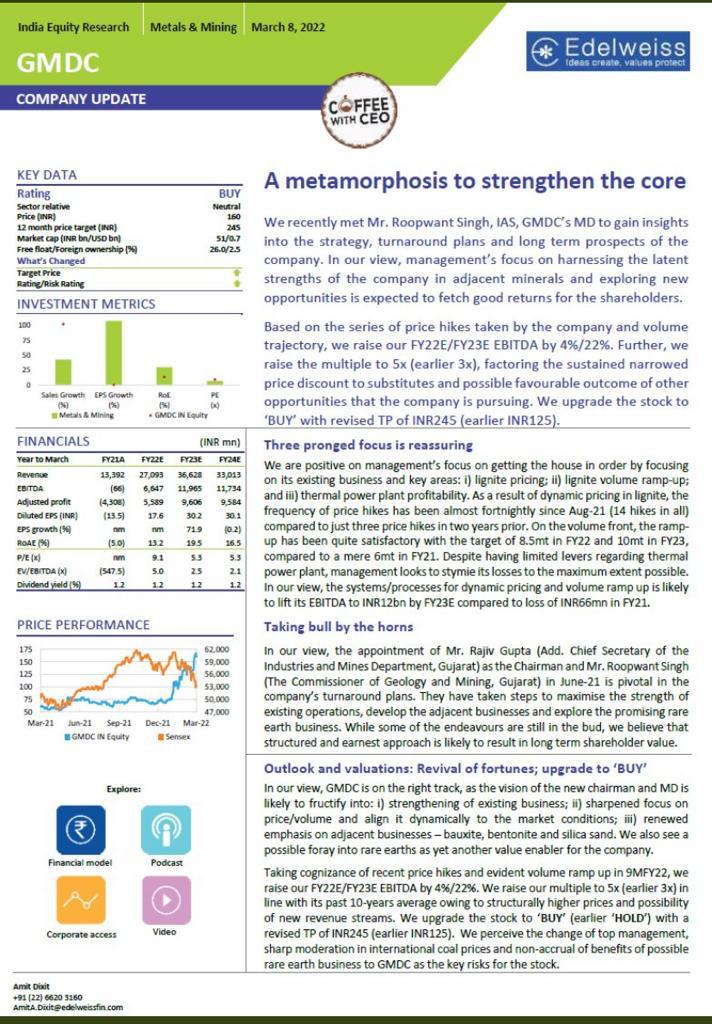

GMDC management talk

Interesting points

Cash deposit with NBFC earning better ROI and this cash will be used as and when required for capex.

Already 5 operational blocks and new 6 blocks will be operational in next 1 year

EV study and R&D underway and shortly it will be known.

Lignite is substitute for coal and due to higher coal prices the lignite prices are expected to go up.

Margin will be maintained at 28% +

Other projects are in implementation stage along with companies like Navin Florine etc ( details on website available)

Hope all things turning out to be positive.

Disc. Invested

@jitenp Sir is the papers stocks are on fire ?

West Coast Papers :

FA 4 QTRS increased Sale ;Margins improvement; Cyclic movement of sector

TA : Dbl bottom , Weekly candle break out from 50 SMA upwards ,MF are in buying positions ;Relative strength to nifty 50

Seshapaper

FA : 4 QTRS increased Sale ;Margins improvement; Cyclic movement of sector

TA : Dbl bottom , Weekly candle break out from 50 SMA upwards ,MF are in buying positions ;Relative strength to nifty 33

dis : invested may be biased

Can anyone shed light on the capacity utilization by the steel industry?

A few like Arcelor-Mittal and Tata Steel have issued orders for new equipment, so one presumes the bigger companies foresee a shortage of capacity.

But what about the rest? And if we are on the verge of a capex boom from the steel sector, who could be the beneficiaries?

Very well explained: Paper sector recent performance is driven by

a) Demand normalisation (due to schools reopening),

b) Distribution channel restocking (due to inflationary concerns and strong demand),

c) Price hikes driven by raw material shortage of waste paper used to manufacture recycled paper - In Oct 2021, EU has banned exports of waste paper due to the shortage arising during the last 2 years due to pandemic and increasing use of digitisation. Price hikes are by both Grade A paper mills (integrated pulp and paper producers - JK Paper, Andhra Paper etc) / AND Grade B&C paper mills (60-65% of production output and depend on expensive waste paper and agro residue as raw materials)

Further paper price hikes expected in near term ie next few months

Check out the blog on paper -

https://www.multipie.co/blog/multipie-weekly/paper-gains-are-real-not-just-on-paper-this-time-📰💰/

Just adding some views on this + scuttlebutt on this from a paper buyer:-

Paper prices have seen a significant price hike in the last month, and there is still a supply shortfall. This includes Grade A mills.

Production for writing paper and printing paper (notebooks and office stationary) is seeing strong demand despite the increase in RM prices. This already started with strong production demand in Q4 21-22 and could continue higher in Q1 2022 in case things remain on track with reopening of schools, colleges and offices in full stead

Base year is very low giving scope for significant growth with upcoming demand + price hikes.

Just taking an example of Seshayee Paper:-

Currently trading at 1 Price to Book. Net profit in the last ‘normal year’ (with lower prices than current) was 190 Cr in FY 2019. At a market cap of 1190 Cr, this means it is quoting at a PE of ~6.2 on normalised earnings, vs median 10 year PE of 10 and 5 year PE of > 8. This is despite almost being debt free with growth visibility + a company which has very high exposure to writing and printing paper.

There is also insider buying happening in the stock, latest in March’22 (buying by promoter N Gopalaratnam and Promoter entity Time Square Investments Private Limited)

Disclosure : I am invested in Seshayee Paper and biased. I am not a SEBI advisor and this is not investment advice

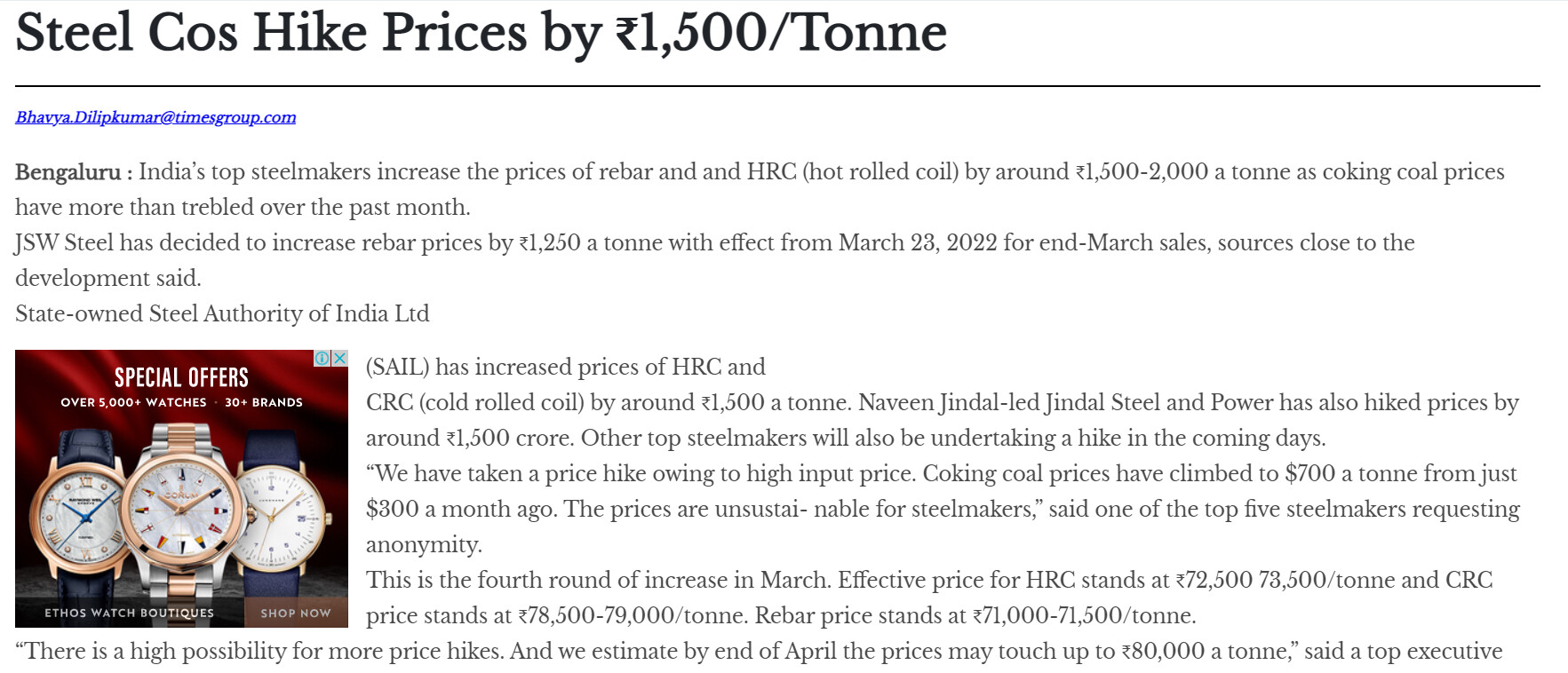

Steel prices increased. Who is the gainer of this - Iron Ore producer, Coal Producer or Steel companies themselves @Rakesh_Arora - will appreciate your insights please

Coking coal is eating away the margins and is forcing steel companies to take price hikes. The key beneficiaries are

Thanks Rakesh!

How much percent of iron ores fulfilled captively for Tata Steel, JSPL and JSW ?

Tata Steel 100%, JSPL 20% and JSW Steel NIL. This is based on where they pay old royalty rates. JSPL and JSW have taken iron ore mines at higher royalty rates which doesn’t save them any money over market rate

As per this article, if cotton prices are trending higher then the textile mills which are able to pass on cost pressure will benefit. Isn’t it ?

Whenever global commodity prices rise, the Indian firms automatically becomes competitive as they also get pricing power (like this happened recently in paper companies). Please correct me if I am wrong.

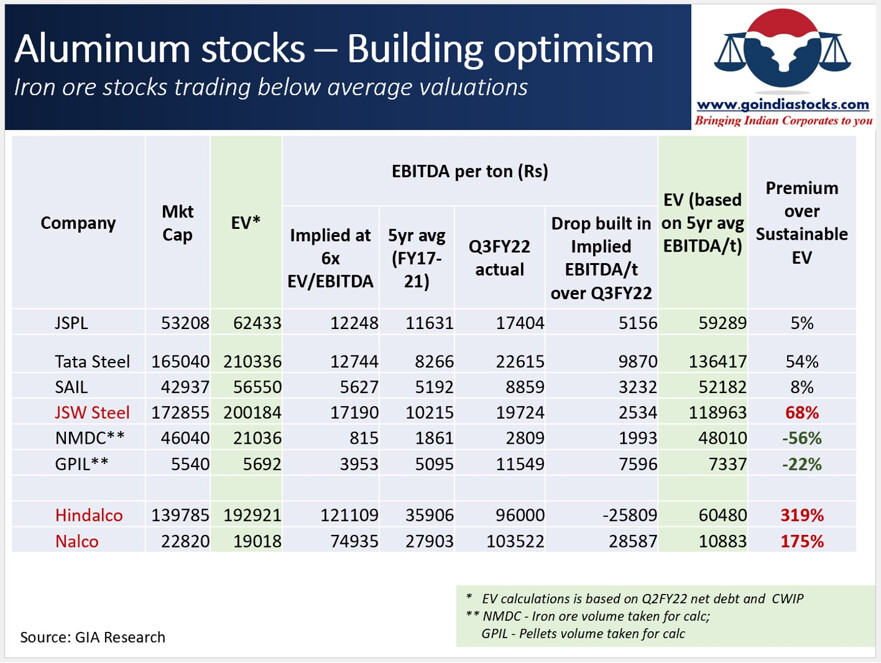

Tried to calculate the implied EBITDA per ton for metal companies based on current EV. And compared it with what companies achieved in last 5yrs average and in Q3FY22. Interesting results.

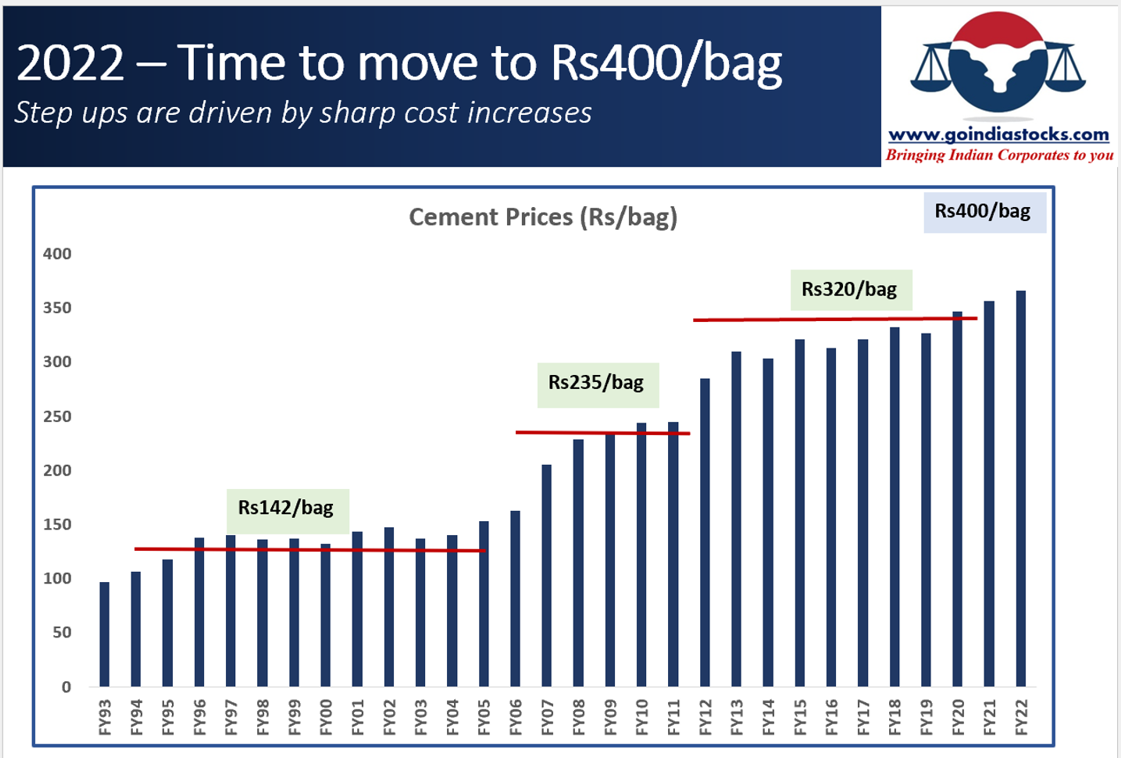

Cement prices tend to move up in step ups. We have seen 3jumps in last 20years. And given the current sharp cost push of almost Rs60-65/bag, cement prices should see increase of Rs40-50/bag pre monsoon. Cement prices stick while current cost increases are temporary with war premium built in them. Strong margin expansion possible ahead.

An extremely insightful talk by Abhay Baijal of Chambal Fertilizers on the ongoing Russia – Ukraine conflict and the emerging global scenario in commodities and its impact on fertilizers and food prices, inflation, government policy and so on. Click on the link below, his talk starts from 39:35 minutes onwards.

(Note: The slide heading erroneously mentions electric vehicle ecosystem etc. Please ignore)

@jitenp how is demand and supply senario for capital goods and cement sector?Thanks in advance.