the consistent fall in BPCL or HPCL while CPCL or MRPL climbed all time highs didn’t make any sense… the nuances of OMCs and Refineries very finely put. !!! thanks a ton…

A few queries in my mind…

i) is this a one quarter wonder due to inventory gains ? because going forward the gross margin may be suppressed or even turn negative if crude drops…

ii) are these elevated margins due to improvement in crude supply without improvement in crude products like diesel / petrol ?

iii) considering the steep run-up in refinery stocks, will stocks oil exploration stocks like OIL INDIA, ONGC or Hindustan Oil Exploration be better bets ?

Time has come that Power, Energy and Oil stocks should fall to new bottoms.This was the last sector standing, but now it has also surrendered. Whole fight of the Fed is against inflation and till the time these sectors don’t show weaknes, the fight would continue.

The structural deficit in Oil persists for OIL/ONGC and other E&P companies.

But as the report says "What happened this week in energy stocks is a classic blow-off technical pattern. Sudden and large reversals like this usually signal a trend shift

in the medium-term (3-4 months). As a result, while fundamentals might be trending bullish, we are likely headed lower/sideways for a while on energy stocks.

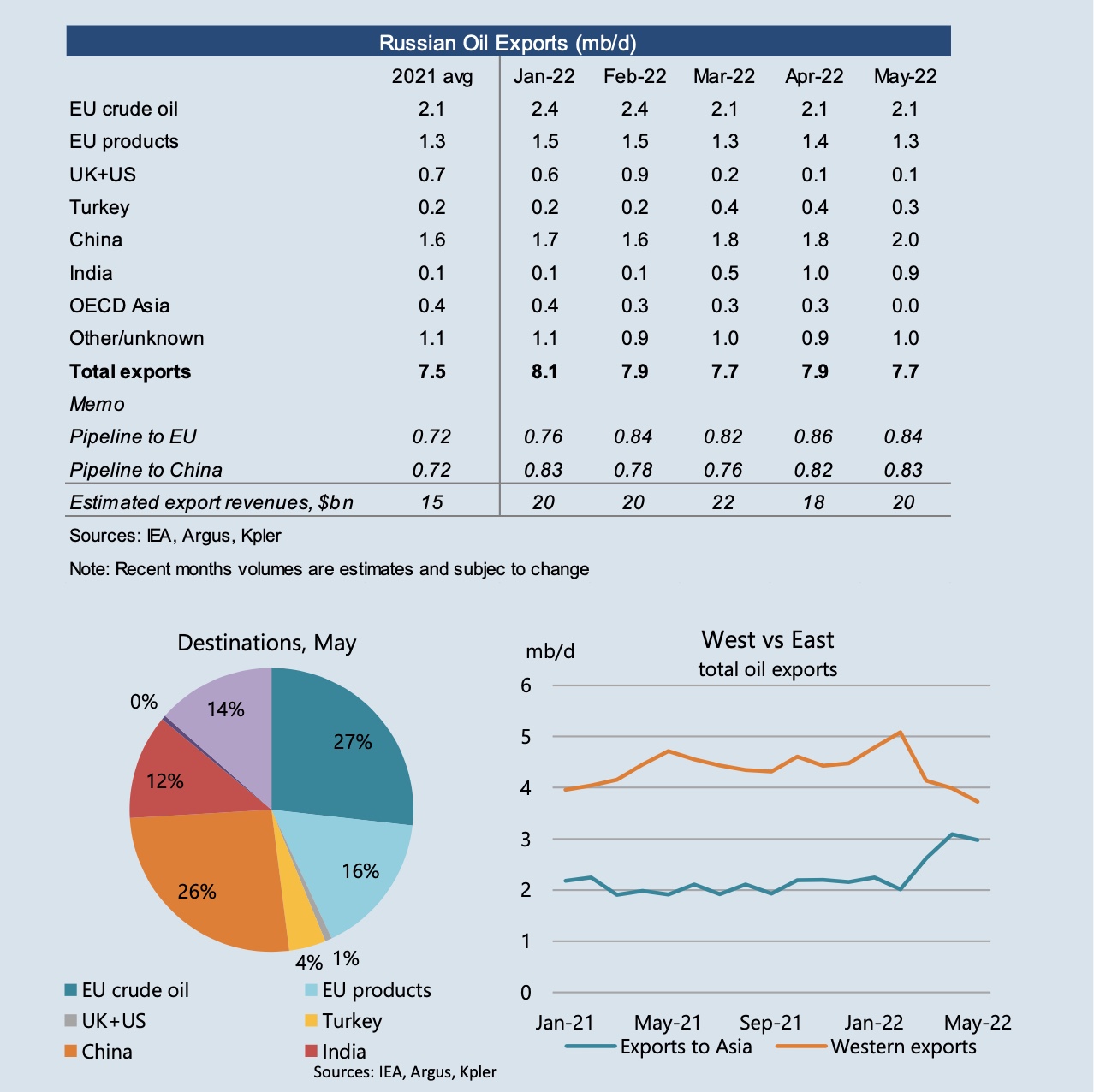

According to a Centre for Research on Energy and Clean Air (CRECA) report released on June 13, the largest Indian buyer is the Jamnagar refinery, which got 27% of its oil from Russia in May, up from less than 5% before April.

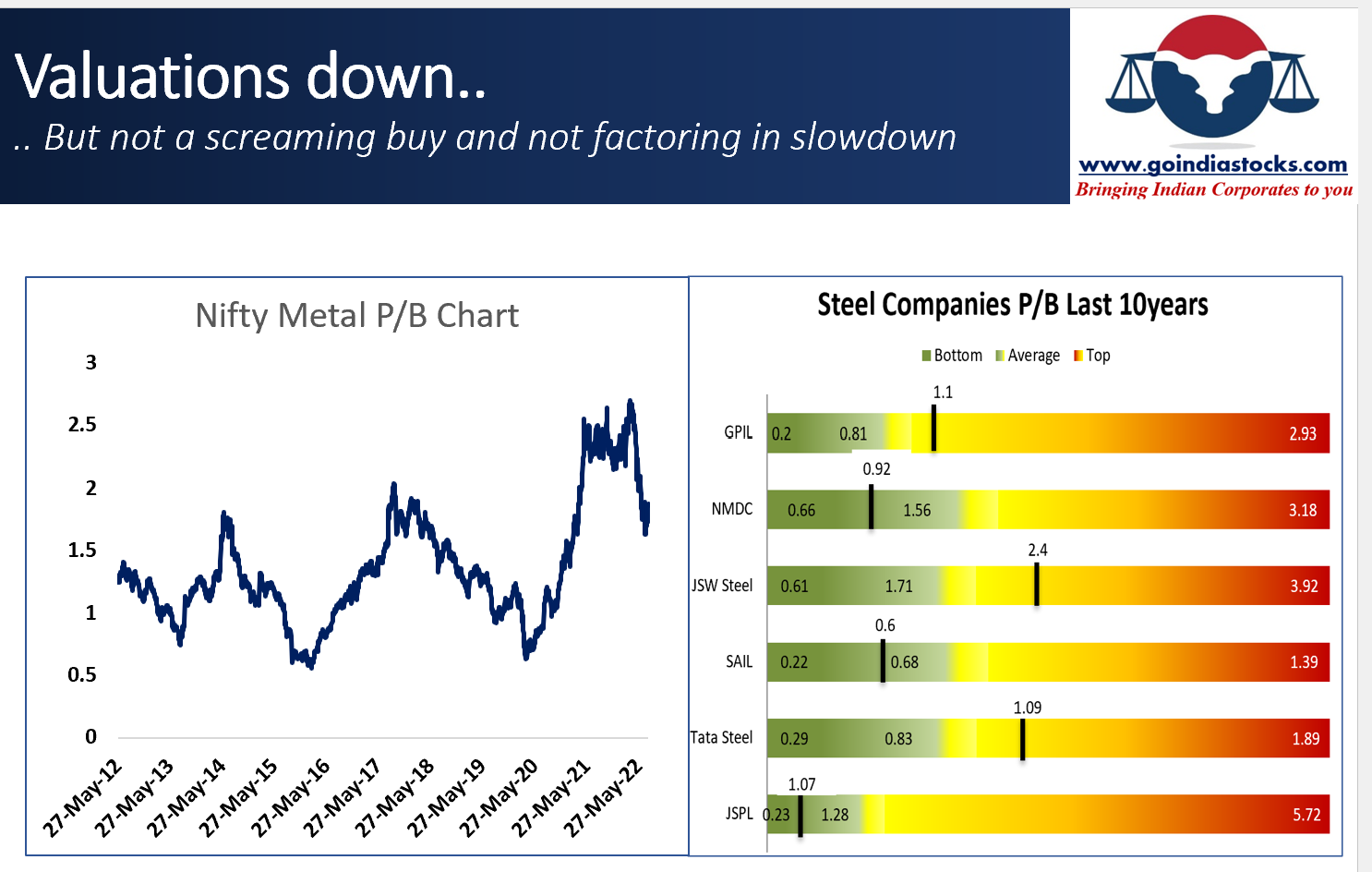

Last time when commodity prices fell post GFC in 2008, this is how the profits of Tata Steel moved. Commodity price movements can be drastic, bottom fishing is not advised.

For both texmaco and twl railways orders come with price variation clauses

But private orders are fixed price contracts

These pvt orders should be @25 pc of their turnover and are short delivery orders

These short term orders should fetch them improved margins.

While all stocks fell, the earnings damage was not of same magnitude as commodities. Secondly no doubt one has to buy stocks when they are cheap, and if one has very long term view, maybe it is a right strategy. This is to say that in our opinion, bottom hasn’t been made as yet. Needless to say, this is a viewpoint, buy and sell decision everyone has to take on their own.

Rather than just cheapness, one should also see growth and management quality even in commodities.

JSW steel and SAIL both are steel companies.

Today, JSW Steel is 5x of 2007 price.

SAIL is down 70% or so from 2007 price.

That’s a 15x or 1500% difference in returns!

So, it depends on the management quality in both short term and long term returns even in same sector and same business irrespective of market timing.

SAIL is a PSU (similar to Air India, MTNL etc) and most PSUs eventually go bankrupt, and are a no-go investing zones for me personally, irrespective of valuations.

Purely from a business metrics POV, that’s right. However I invest in PSU where they’re a monopoly. Take IOC, petro OMC, largest jet aviation fuel supplier, gives fantastic dividends but price yo-yos a lot. I just buy it a bottom, getting a dividend yield of 9% in the worst of times or 12% in the best of times.

I’d amend yours to go after PSUs where another entry is cost prohibitive in terms of CAPEX by a private player and they’re a monopoly supplier.

Any views on to what extent will this impact the earnings of oil producers and refiners sector?

An inherent risk in commodities sector (Tax & more tax)

last 10 years were bear market in metals… in the bull market from 2001 to 2007 tata steel used to trade at 3-4 times book now its trading at 1.2 times book… so the bigger question to ask is “are we in a metals bull market or not ?..” or simple put can america stop printing money…? today they launched huge green stimulus bill … what will all that money be spent on? metals…

Tata steel bought corus after the profits made in 2007 which was one of their worst financial decisions and the standalone Indian entity paid for the losses it incurred for more than a decade.

Coal Stocks in Power plants remain tight, though have eased up from low levels in July. Decent monsoons should support Hydropower generation to offset the increase in power demand.