Ambika Cotton is a big exporter of high quality fabrics

1 Like

Faze three seems to have appreciated quite a bit and the valuations look expensive. Do you have more details on where the next phase of growth will kick in from ? Have they added any clients or any new offerings in their portfolio. Also is there any capex, merger/demerger or acquisition/takeover on the radar? They also have an auto seat maker co named Faze three Auto so are there any synergies between the two and are they negatively impacted by rise kn freight charges ? If you can throw some light on the company then that would be helpful in taking an investment.

Thanks in advance !

1 Like

caustic prices are still sustaining at around 60k. CS Flakes went for around 75k today. unheard of previously. CS lye 62-63k.

Soyabean prices corrected from Rs 2400 to Rs. 1400 in a matter of 2 days a month back, after having gone from Rs. 1200 to 2400 in 5 months. Playing with fire always not advisable in commodity stocks. MOS is most important.

Disc: not invested in any CS stock. just watching how cycles play out.

4 Likes

Soybean and bulk chemicals are not comparable at all. Soybean prices don’t have anything to do with China’s power issues

To each his own

1 Like

Still this event has nothing to do with commodity prices.

5 Likes

Sail post Q2 results

Disc: - invested at lower levels

3 Likes

Indian billet, pellet prices etc seem to be very stable even though Chinese iron ore prices are 50-60% down over last 2 months ago.

Indian billet prices are now at 45000 vs 41000, a couple of months ago.

Pellet prices are also stable around 12500/ton

2 Likes

@jitenp Jiten bhai, what’s your view on steel cycle, would it still continue ? Is it a structural change in the sector as per some views ? Many thanks

2 Likes

As mentioned in the last few interviews, I have been taking just quarterly views on steel. Very much depends on China. Iron ore has fallen 60%. So, one needs to be cautious. Had exited most positions sometime back. Just have a very small tracking allocation.

I have a slightly longer view on non-ferrous metals and continue to stay invested there.

10 Likes

Thanks so much Jiten bhai

2 Likes

Palm oil shortages are quite severe, I dont know offhand what companies have palm oil fields but it looks like there are 3,

Godrej agrovet

Gokul, both Gokul agro have some palm oil business and fields and both have been doing well lately. Probably some smart money is pouring into it

PS: Tracking position in all stock

Gokul are consolidating so I might add on breakout

3 Likes

I have been thinking & reading a lot on steel in the past few months. Upfront disclosure – my knowledge is extremely limited here, I literally picked up steel sector for the first time and tried to do some form of a basic analysis. Have not spent enough time by way of company transcripts or industry reports to offer any comprehensive view with conviction, but nonetheless at the end of my exercise, found myself with a positivity bias towards steel stocks. Have no exposure yet, but looking to buy on a ~15% correction from hereon for the frontline steel stocks.

-

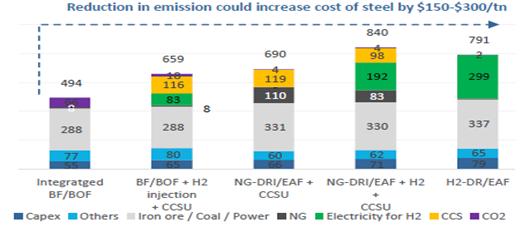

Structural drivers elevating cost of production - Now there’s a lot of eyeballs on the china housing crisis(evergrande), chinese attempts to crackdown on domestic past excesses, which has crept up the fear that chinese demand can significantly slow down, hence demand leveling off will weigh on steel prices. Although there certainly is a possibility of a hard landing (though I don’t really see chinese steel demand just dropping significantly, even if we see a few busts among large chinese developers, given underlying real housing demand is fairly strong), would steel prices drop significantly? I don’t think so, & the primary reason is because cost of production can structurally increase worldwide, due to environmental crackdowns & the need to use ‘green’ or less carbon intensive steel inevitably increases. Snapshot from a recent spark report, I think they have specifically nailed this point quite well in their reports - more focus on this point vs worldwide or china D/S next year.

“Hydrogen & Carbon Capture are currently known pathways to greening steel. Any tech involving the mix of the two would increase the cost of Steel making by 25%- 60%. With R&D/Capex costs being steep, the ongoing projects (mostly European) are likely to add only 1% of Steel capacity by 2030 (~20MT) – these are largely directed towards DRI (Direct reduced Iron) not a preferred model vs the cost-efficient BF/BOF model (Blast Furnace/ Basic Oxygen Furnace) adopted in Asia. Current Hydrogen costs are 3-5x of Coal and needs substantial investments at scale to cut the costs by half (A journey similar to Solar PV which could unfold in 5-8 years), which is possible a possibility only with policy support - most likely in the form of Carbon tax (already prevalent in EU). China will commence ETS (emission trading system) in 2H’21 starting with Power sector, with Steel being added soon. Though it may not change the cost of conventional steel immediately, we see a gradual tightening & cost of emission leading the change in the medium-term. Green steel investments / compliance costs are high & expect profitability to be a step higher compared to past trends to enable these investments / transition.”

"Cost of Green Steel higher by $150-$300/tn (+25-60%) depending on tech/process vs conventional BF/BOF. Cost of Hydrogen generation + Carbon Capture remains key”

“Carbon Emissions in steel making can be reduced by > 50% only through a mix of Hydrogen (replacing Coal) and Carbon Capture storage and utilization (CCSU). 100% emissions is achievable only through Green Hydrogen (Electrolysis through Renewable power)”

“Cost of Steel with lower Co2 impact is atleast $100/tn vs conventional steel making based on FY20 RM cost levels. Achieving 100% reduction in CO emissions require H2 from renewable powered electrolysis plant – which is $200+/tn today”

Unless there is a scenario in which steel companies are allowed to enjoy higher profitability, the investments needed to manufacture less carbon intensive steel don’t make sense to them at lower steel prices. New technological innovations to make more climate friendly steel should require relatively higher prices for the time being. And the time being could be a few years, not a few months. These are mammoth technological improvements over 200 years of time tested cost effective ways to manufacture steel and they will require money (higher profitability). -

Multiples rerating heading into FY23 on current or even lower profitability due to large debt reductions - Open the recent pnl, see that the margins have already moved up, the mind = risk reward is not favourable, we are already in midcycle or near the end, risky now. It’s fair to say that since margins have already moved up, the risk reward is less favourable. But what about multiples? Strong deleveraging playing out should not be ignored.

Take a historical analysis of valuations back in 06-08 or 10-11 on EV/B, not P/B. Even if steel prices see a correction, a reasonable one, not a very significant one taking prices back to pre covid levels, stocks look reasonably cheap on EV on next year’s earnings/multiples. Where is the euphoria? One can argue that steel prices can fall significantly taking it back to pre covid levels, in which case the bull/base case here completely fails. But even in a base case of a moderate correction in steel prices(still elevated vs pre covid after seeing a sharp drop from tops), there is decent profitability. So far, it’s been an earnings led move, not a multiples one, since for CY2022e or FY23e, nearly all forecasts incorporate a significant drop in steel prices. If that assumption of a significant drop in steel prices does not play out in the time stated, odds are higher then that multiples rerating come into play, pushing up stock prices heading into CY22/FY23.

5 Likes

8 Likes

Steel sector report and charts:

Steel industry can steer India towards $5 tn economy by 2025: EY-CII report (msn.com)

1 Like

I think this is a great news where a lot of value unlocking might happen.

@jitenp - Your thoughts on this news item would be quite valuable.

2 Likes

this would be great for the whole disinvestment program. Govt has made a decent start with the difficult disinvestment of Air India. A couple more and whole PSU pack maybe rerated.

Am invested sufficiently in the PSU pack. Many are at excellent valuations and at sustainable 5%+ dividend yields. An excellent proxy for cash and defensive bets, and if things go well, may offer decent capital appreciation too.

Had increased allocation to PSU stock basket in the last few months.

13 Likes

Hello Jiten, there is good correction in small and midcap ement stocks. What are your views on it? Largecap cenent is holding well and does not look like cyclical. What are your views on cement cycle?

Thank you

Disc: Not invested in any cement stock currently.

Update: Caustic prices now down to 45k-50k per ton in domestic markets.

http://www.sunsirs.com/uk/prodetail-368.html

One can check the chart for CS prices in China also.

1 Like