Due to sale of Neelanchal ispat the balance sheet of mmtc will be improved and I thought it may be rerated.

Thanks

2 Likes

Yes @Rakesh_Arora it looks extremely cheap for the scale of the company. It has the 7th highest revenue among all Indian companies, behind only Reliance, Indian Oil, ONGC, SBI, BPCL and Tata Motors. And is available ata market cap of 15k crores only! This is what intrigued me.

They apparently own 40% of the world’s gold refining capacity, and so an increase in gold prices could give them windfall gains. And even though not many famous institutions are invested, the free float with public (outside of promotors, institutions and large indovidual shareholders (more than 2% holding) is just over 2%. Seems like extremely low risk and potentially extremely high reward.

1 Like

As I said, I haven’t worked on this company, so don’t know the nitty gritty. However, it doesn’t pass my 1st filter, which is generating free cashflows. Revenue is high but margins are miniscule. And working capital requirement seems huge. I am normally wary of turnaround stories having burnt my fingers. But this is my initial view, happy to learn from you and @ganesh_bastwadkar if you can dig more on it.

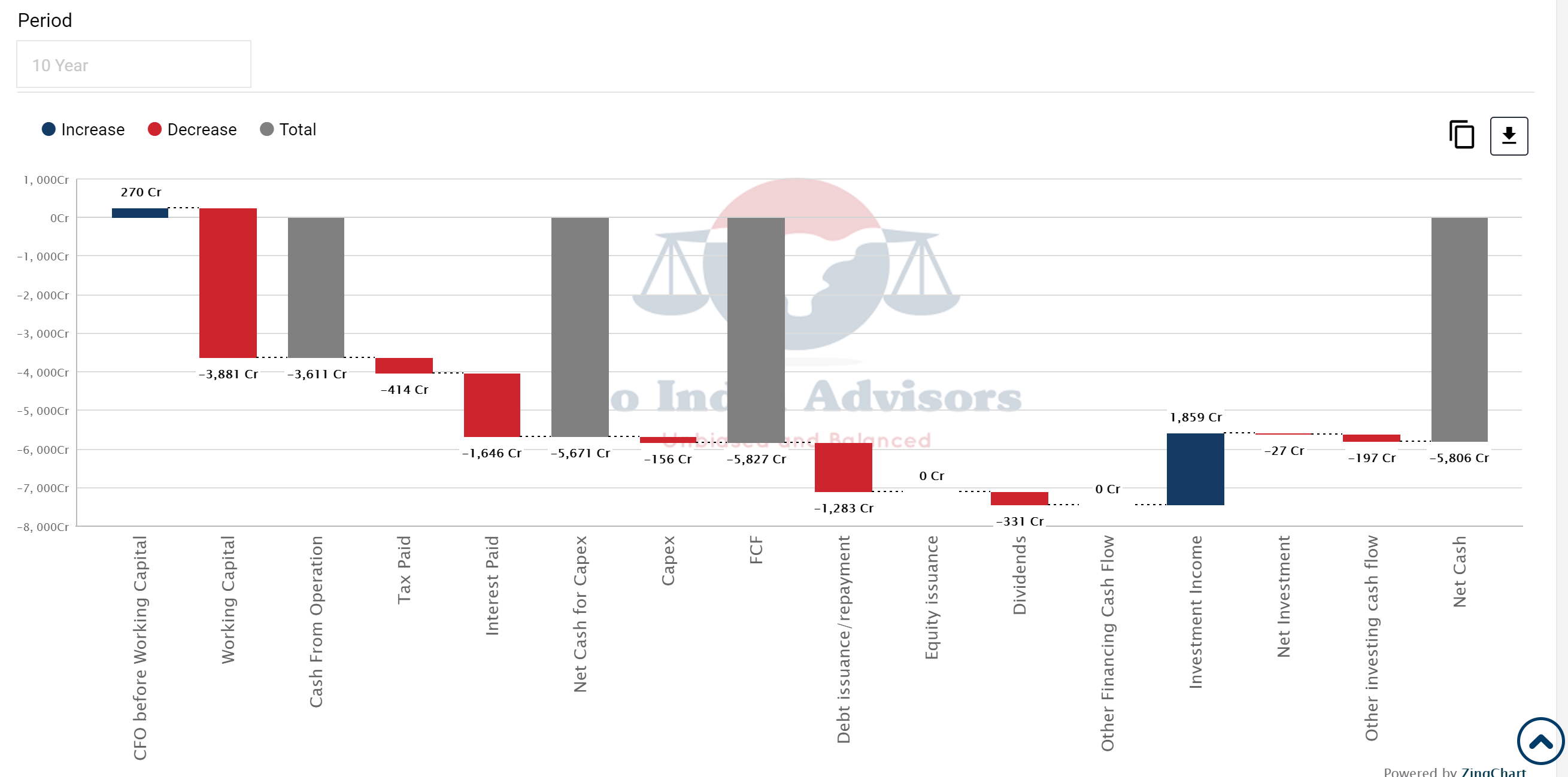

Source: GIA Stocks

3 Likes

@Rakesh_Arora Sir ur view on Ashapura minechem?

this company went through so much upheaval so have lost touch. Will have to read again. Maybe Ganesh can update us on the latest

Rakesh air thanks for the faith.

I am tracking MMTC since past couple of years

I feel that the the momentum in gold and silver fuels the growth of this company.

This acts as custodian for digital gold and silver and I expect the digital sales/ investment will increase and benefit MMTC.

Rakesh sir please correct if anything is wrong.

1 Like

@Rakesh_Arora Hello sir. Many thanks for sharing your wisdom with all of us. Always a learner under your guidance. Needed your views on Rushil Decor.

As my understanding goes -

- Increase in lumbar prices might shift the buyers towards MDF products.

- Sajjan Bhajanka Ji (of Century Ply) recently bought a stake in the company as part of Bulk Deal.

- Debt repayment + Capacity Expansion creating Alpha in the earnings.

Cons - - Recent Force Majeure due to the Covid crisis. (But it might be short-lived)

Thanks a lot in advance for your insights.

3 Likes

@priyaanshu I have biased view being a holder. The MDF thesis is looking great and with anti-dumping duty coming in, most players are talking about 30% EBITDA margin. However big question as you have right put it is when their new plant reaches full capacity utilisation. They need their technology suppliers from Germany to visit India and given the Covid situation not sure when this happens

4 Likes

Already started?

2 Likes

If only one stock can be selected in small cap cement companies, which one is the best preferred choice as per valuation and future prospects…

@Rakesh_Arora sir your opinion pls…thanks

This article talks about two things- 1. China is taking stricter actions to curb unreasonable price hike and that is having spillover effects in India metal stock prices.

2. The other side of the coin - Indian steel companies were already selling at cheap prices as compared to global market (TV Narendran of TATA steel also spoke of it). So, there won’t be any import led competition. Profitability looks sustainable.

China curbs are to try ‘cool’ of price speculation but they don’t do anything to demand which looks robust globally and supply of iron ore which is under slight pressure due to weather impact. So story still intact. Also, mill margins are at a very high level and production will continue even if margins/prices correct a bit.

To me the best way to play this is via Graphite Electrode stocks. Heads I win a lot and tails I win a bit.

3 Likes

Already 15% correction has happened in past week in steel prices due to Chinese Govt intervention. But the prices still are high and beyond Rs 65000/ton. Even if it drops to 55000/ton, the margins will remain high as in most big steel companies cost of making per tonne steel is around Rs 30000. These margins will only help companies to deleverage quickly which we saw in Q3 and Q4 of last year.

1 Like

@PraveenKG difficult for me to recommend individual stocks given Compliance. However I can tell you that I own Dalmia Cement, but bot 18months back below 700, so already run up quite a lot. Same is the case with most cement stocks. Normally cement stocks correct during monsoon season and bottom out around Sep-Oct. Also this time around, due to 2nd wave of pandemic, infra projects have been stalled. The labour supply is impacted as rural India has taken the brunt of Covid 19 this time. So my suggestion will be to wait for weak numbers to show up and enter when stocks have corrected 15-20% from here

8 Likes

sir your views on deccan cement ? one of the cheapest cement stocks in the market.

Came across this on Twitter

3 Likes

Dear Rakesh ji

Please advise, can early signs of movement of international steel prices be done using the link below : Commodities Prices - Spot - Futures

This might even help to track international sugar prices if a direct relation is really there.

Looking forward to your valuable advice.

1 Like

yes, trading economics is a great website, I do use it regularly. For steel sector, I have made free access available to stories and prices from steel mint here on my website GIA Stocks.

9 Likes

After steel (ferrous/non ferrous), sugar, cement cycles, now realty sector is in talks. Undoubtedly the realty sector is bearing the brunt of the second COVID wave, if we listen to the concalls of companies like Macrotech, MD says that once covid situation is lightened & vaccination is accelerated, we are sitting on a multiyear upcycle in realty sector and big players are definitely going to earn more because of the poor/highly leveraged players going bankrupt or liquidity crisis. There’s consolidation going in this industry, you can find this in chairman notes of Oberoi realty, Sunteck realty.

Also, I read that the players who have ready to move/ near to ready to move in inventories will be the first to benefit once second wave subsides.

Discl: companies mentioned above are just for reference, I may have position in any of them, views may be biased.

3 Likes

@Rakesh_Arora Sir as per Steelmint (read on GIA), HRC china price reduced by 10% on May 21…what implications it has for India steel prices.