Sorry Vineet. Took so long to reply as we were working on the sector. I think while sugar stocks are currently overbought but there is a structural change happening driven by ethanol which can improve return ratios and make earnings more stable.

Source: Sugar fix for your portfolio...

6 Likes

Sir on a comparison the PE ratio and PB ratio of Dwarikesh Sugar appear attractive.

In fact the FII holding has also increased in Dwarikesh Sugar.

Rakesh sir Your views pls

2 Likes

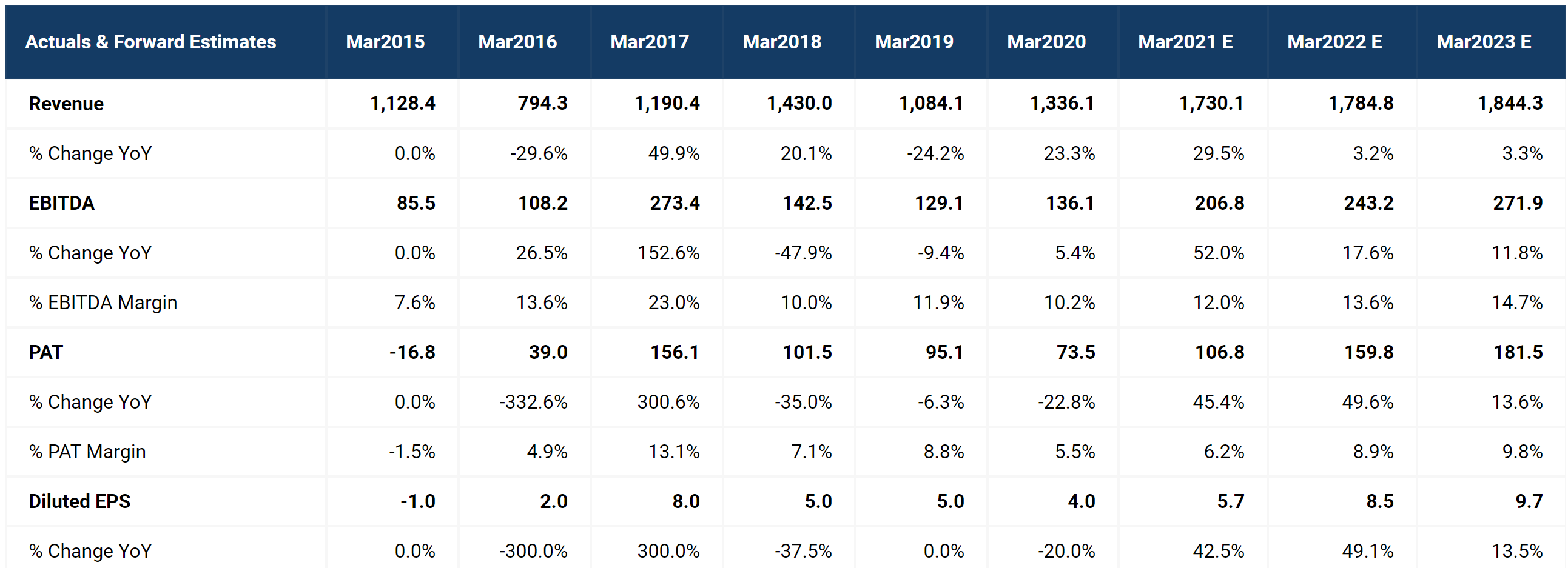

Based on analysts estimates for Dwarikesh, it is trading at 5x FY23. So more upside possible. But do your research, am no expert here

Source: GIA Stocks

4 Likes

Thank you for your response @Rakesh_Arora

The Sugar fix your portfolio blog is very well written!

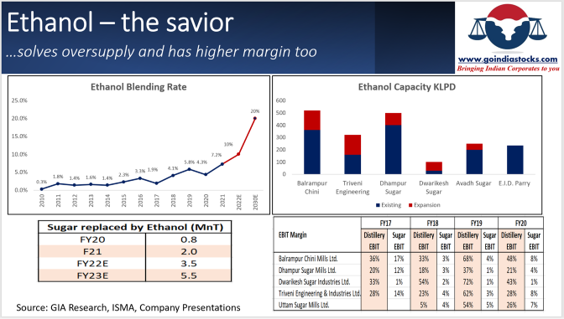

So based on the blog, my inference is that companies with high ethanol capacity stand to benefit on two counts: 1) The demand for ethanol will be higher than supply from sugar till 2030, so it’s a structural demand story, 2) The margins from ethanol may be higher than sugar owing to higher margins from distilleries.

Dhampur seems to be cheap on a P/B vs ROE basis, as well as it has high ethanol capacities. So in all Dhampur seems like the best risk-reward from this point over the medium to long term. Does this make sense, or am I missing something?

On a side note, do you have any views on ethanol specific players like Praj? Leave aside their bio-tech expansions, how does just the ethanol play look to you?

3 Likes

Sugar sector explained very well. I got some knowledge hence posting here.

8 Likes

Can someone please post the crux of this article ? Someone who has subscribed to business standard.

After sugar, now steel players saying it structural change and that is coming from the Tata’s.

Is it really different this time ?

You can listen to the Tata Steel concall where he has explained this:

1 Like

China -Australia tension will keep Iron ore prices at elevated level.

61 per cent of China’s iron ore was imported from Australia in 2020, UBS found.

CRU Group principal analyst for steel, Erik Hedborg said reduced production in Tangshan, China had driven up prices.

This was due to China’s emissions crackdown in Tangshan.

“Recent production cuts in Tangshan have boosted demand for higher-quality ore and prompted mills to build iron ore inventories as their margins are on the rise,” Hedborg said.

Godawari Power valuation is proxy to Iron ore prices.

3 Likes

Some big deal are being carried out in Ashapura minechem. This share will be most undervalued if the management guidance of 2MT of iron ore export holds true for FY20-21 and doubling the same in current FY. I am no expert of technical charts but if boarders can help us out with technical chart then it would be very helpful . Thanks

https://www.moneycontrol.com//stocks/marketstats/blockdeals/view_deals.php?sc_did=AM07

1 Like

@Rakesh_Arora

Sir what is your view on Ashapura Mine

It appears to be undervalued compared to peers

I read that some of its legal issues/ litigations are resolved.

Is it a better short term investment

2 Likes

on the basis of merger news valuation will drop initially of BSL i guess , we may see a correction in stock price

hi All, Is anyone following the cement cycles, any insights, inputs and where is it in the cycle would be helpful.

1 Like

I wrote about it Cyclical, but for all seasons...

2 Likes

@Rakesh_Arora Sir how do we know the lifetime of a mine ? Do we have any publicly available data on this. If yes where we can find the data ?

one has to check with individual company for exact details. However on Ministry of Environment and Forest (MOEF) website one can find environmental clearance pdfs, they hold lots of information.

@Rakesh_Arora

Sir whether the increase in gold and silver prices will benefit Mmtc.

Pls share your views taking the following tweet

@ganesh_bastwadkar MMTC hasn’t made money ever. Not worth spending time on it. Better plays on gold are Gold NBFCs, MCX and some banks like CSB etc

2 Likes

@Rakesh_Arora on gold, what about Rajesh Exports? Largest gold refining company in the world, and is into jewelery retailing too. Had consolidated for long and has a nice rounding pattern on charts.

@Vineetjain111 sorry haven’t done much work on it. Looks cheap but why no institutional investors of repute there. Can see only LIC.