Does this rationale hold true for all commodity plays or just a few .

Also - how should we estimate ebitda given prices fluctuate a lot . Am presuming prices for steel won’t come off much this year given the current circumstances but that’s a broad guess

Goldman Sachs has come up with the report on Copper. They have predicted the prices to steadily increase year on year until 2025 to reach $15,000/Ton(current about $9,000). They attribute it to EVs, Green Energy initiatives across the world.

Largely yes. Take last 5year average for sustainable EBITDA and make adjustment for any change in competitive positioning of the company like Indian iron ore prices have moved up sustainably by Rs1000-1500/t due to Auctions in Mar’20

Btw one can check current prices of iron ore/steel and read stories from SteelMint free here GIA Stocks

this is from my research which is available on my website www.goindiastocks.com. While you can look at both these parameters separately in chart on this website but not together. But you have given me good idea. Will introduce this capability to compare any parameters of the same company

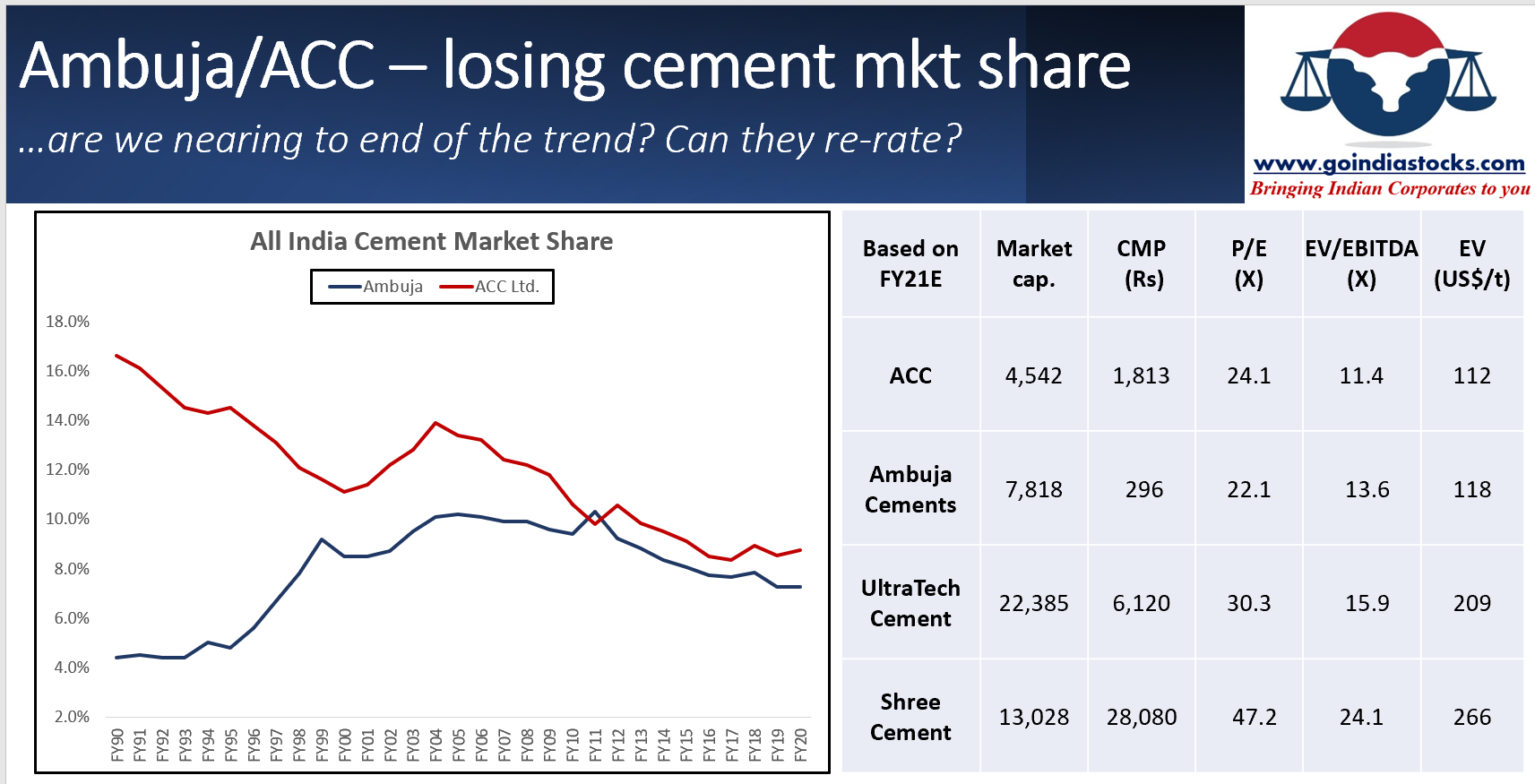

Ambuja Cement has announced increasing capacity from 29.65Mnt to 50Mnt. The first plant of 4.5mnt capacity is to be commissioned next quarter. This is coming on back of 10years of losses in market share. There is potential merger with ACC also in cards as one of the hurdles has been removed in the recently announced MMDR Act 2021. Can it re-rate now?

For a small investor NCL industries is also a good bet. There is a branded business of Bison Board also in the same company which is worth a lot, along with 2.7 MT cement capacity. Total EV is approx 1000 cr with WHRS capex already done and benefits of 25 cr plus annually which will add to the already strong bottomline. Some good investors have taken a sizeable position of late along with the promoter stake also increasing. If we value the Bison board business at 200 cr, we are getting a 2.7 MT well run cement company at 800 Cr which is approx 40 $ / MT

Will really appreciate to hear your view on this one

Good disclosures and dividend policy also - so better times ahead for next few years . Do check their last quarter business update to get more details

@Rakesh_Arora sir, what is your view on the impact of the new Covid restrictions on paper companies? especially with respect to the comopanies using recycled paper as a major source of raw material.

My theses: Seems like schools will be shut for another six months at least, so writing and printing paper demand should take a hit. Also supply of raw material should be limited thereby increasing input costs. Seems like this is largely factored in share rices too. Is this a correct understanding?

This article also mentions that aluminum and copper are also reaching all time high of last supercycle. Can this mean aluminum/copper companies are going to have good time just like steel companies ?

Dear all,

Another question,

On the Rain Industries thread it can be clearly seen that aluminum cycle has turned (as is clear from many articles on the web), but we have not seen a run up like steel for the aluminum companies, so any thoughts on this ?

It’s only aluminium

They have gone through an expansion

Last quarter revenue was subdued as plant had to be shutdown to start the newly expanded capacity

Varunji, most metal stocks and even commodities tend to move in a pack. There could be some lead or lag. You can read about my views on Vedanta and other steel companies in the source links to charts pasted above in this discussion. Our you can visit www.goindiastocks.com. thanks

Please build your own conviction, we are here to help each other with view points and analysis

. @Rakesh_Arora

. @Rakesh_Arora