By divestment the beneficiary is MMTC.

As on date approx 94% stake in Neelanchal Ispat is held by MMTC.

Neelanchal is a loss making unit.

Once it is divested the Balance Sheet of MMTC would be strong and expect it to be a cash cow.

Hopefully the surplus from stake sale may also add some reserves to MMTC.

Disclosure: started to add MMTC

Caustic price going up. Yesterday’s ex factory GACL price was 25500.

Sir, from where are u tracking prices of caustic sode. it will be helpful if u can share the link

My friend deals in caustic and few other chemical so I get update from him

yes, prices have been on the rise with the reopening of paper and textile industries. 28k is accepted rate in northern markets. This is not ex-factory rate. this includes freight.

for the previous quarter they were around 22-23k.

Disc: invested

Today price is 29000 by GACL EX PLANT

Disc tracking caustic soda price as invested in TGV RAYALSEEMA

From 25500 to 29000?? What I’m missing??

Sudden closure of one plant it seems. Same in northern side. Rate increased today itself for caustic soda flakes. Caustic lye soon there will be rate hike.

Outlook from Morgan Stanley on Indian Steel Industry

I think their estimates are extremely conservative. SAIL could easily do 40-50% higher EBITDA than their estimate in FY22

I think the big risk in SAIL is from future investment plans, M&A plans for divestment and government production “targets” pursued in the medium term. Otherwise it looks undervalued from EV/EBITDA point of view. Hence I think one has to invest with caution here.

Disc: Invested but small position

@Rakesh_Arora Sir, Your views on above two report in which one says steel rally will be short lived and another saying that it will continue till FY 23

It’s very difficult to predict so long term in commodities space. I think there is visibility atleast for next 12 months as economies will see a big jump with vaccination and unlocking. The demand support will only get better than worse. So, too early to think of stocks having peaked out. Best way to value these companies is to look at 5-6x EV/EBITDA on sustainable medium term margins while adding the windfall gains being made currently for the period we have visibility. In some cases, the windfall profits are substantial. For example Godawari Power is currently doing EBITDA run-rate of Rs450-500cr per quarter, which is almost 20% of current market cap. So if current prices last for 1year, you are looking at windfall gains in one year almost equal to market cap!

Another really interesting interview (link) with Kenneth. His understanding of business cycles is impeccable!

- Aggregate profitability has shifted from consumer makers to commodity makers and this should persist until the point new capacity comes up. Most of the current players are viable because they have survived the last downcycle

- Excess supply came b/w 2008-2011 which made it an oversupplied market

- Banking and NBFCs are late cycle plays, at the beginning of a cycle there is an upfront capital investment at lower cost of capital from efficient players with strong balance sheets (eg: only few steel players exist now compared to 2008). In the later part of the cycle, more participants come in and lending business gets pricing power

He is implying we are in traditional commodity bull run , but lets look at facts

In Steel

if there is overcapacity , why steel prices are rising … It is because of COVID near 30% of capacity moved out - resulting in huge inventory drawdowns … These will be corrected soon as soon as shut capacity resumes …

The Demand recovery is no where pre COVID as auto production still has not reached 2018 levels . Housing sector still is over supplied vis a vis 2014 /15 levels …

In China policy is getting tigher and housing starts are supposed to slow down in second half … All this are not bullish for traditional commodities

We are bull run for non traditional commodities

-

Decarbonised commodities -

-

Data

These commodities needs to explored more in this thread

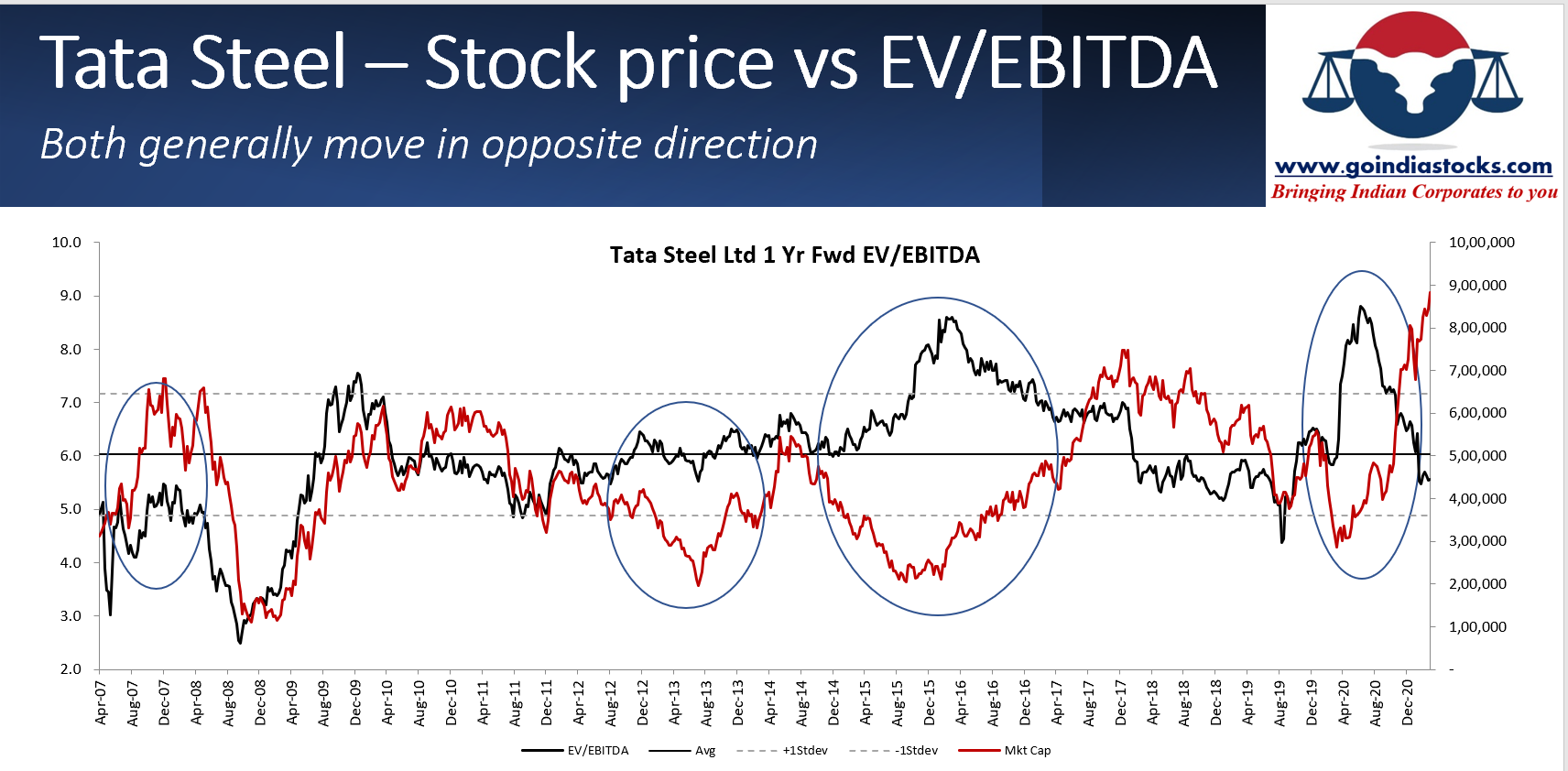

Commodity stocks bottom out at higher EV/EBITDA multiple and peak out at lower EV/EBITDA multiple. Check this chart of Tata Steel

Source:Valuing commodity stocks with blow out earnings...

what are the triggers to keep a track on to see if the cycle is turning negative … and hence gauge how much steam is still left .

Hi Varun, not sure if you are asking me, but view is as follows. Either one can do detailed demand supply models to forecast when the dynamics turn unfavourable and would require access to lots of paid data. Or go the simple way which most retail can do, which is follow the P/B chart and exit when it is nearing old peaks. If one wants to be even more scientific, one can give 6x EV/EBITDA on normalised earnings. Now use the net debt number you think is most likely 1year forward to calculate mkt cap. If market cap u get is lower than current market cap SELL.