@Rohit_Kadam: Are you anticipating that future will just extrapolate the past performance for this business, concluding from the overall writeup and final valuation?

1Q on your note:

What’s the basis to conclude that Colgate is unlikely to bring its global parent’s other categories like soaps, home care, pet nutrition to India ?

1 Fwd. looking Q:

How management is able to rationalize (to various stakeholders - parent and shareholders) for such an anemic growth rate, considering growth potential for a businesses operating in Indian economy?

Any thoughts?

seems so, except that it seems the pain from Patanjali and naturals onslaught has receded to a large extent. So expect more resilient market shares versus the near 600-700bps share loss last 5-6 years. That means growth rates for Colgate may look a tad better versus the recent past but would be constrained by the category growth. That helps, from a stock perspective given their valuations versus peers (although val also reflect single category risk and slow category growth rates)

On bringing new categories to India, I am just going by what they have done over the last several years if not decades. In any case, it seems they have missed the bus in soaps and home care given we have several dominant incumbents there including HUL, P&G, and many Indian companies. Colgate India does have a small presence in body washes, albeit with a premiumish positioning.

They completely lost out in bringing other brands to India except for Gels which is imported and marketed here.

Oldies may remember that we use to have Palmolive shaving creams, Kapil advertising it.

Also, Axion dishwash detergent was there for some time.

I don’t see intent to launch new brands. They have tons of brands. Our Brands | Colgate-Palmolive (colgatepalmolive.com) But India is already getting crowded with local/global brands in these categories and may be bit too late.

There are multiple ways in which Colgate India can and could have grown, specially during the ongoing Pandemic but the execution has been in need of wanting more. It could be because of the way the Indian subsidiary or rather any subsidiary of the parent is run…

First of all…Colgate is not a toothpaste company…it is a predominantly Oral Care company…

Talking about penetration of toothpaste in India…How many follow the dentist recommended twice a day brushing?..the growth can be huge if just all the existing consumers start this basic oral hygiene step…and sooner or later most will…

Mouthwash - This could have been a huge growth driver and scope of innovation during this pandemic…adjacencies like mouth sprays etc. and educating & promoting a must use of this oral hygiene…however this innovation was lagging…one can argue that Colgate rather behaved responsibly and did not capitalize on the fear of Pandemic as it could be driven by global standards of new product launches in even adjacencies… whatever said and done…Mouthwash penetration is miniscule in India

Toothbrush - Huge scope of premiumization and many in US use battery operated brushes…right from kids to 70+ on their dentures…

Prescription Products - Colgate sells prescription based toothpastes and oral hygiene products in USA…these are very premium products…once people in India start brushing twice a day, floss regularly, use mouthwash then probably they would think of using such premium products…

So I have no doubt on the runway and growth of even this small Oral hygiene category but what is amiss is the zeal in Colgate India to behave like a category LEADER…to create new sub categories in India and accelerate their adoption…Pandemic could have been an excellent opportunity when entire world is inclined towards hygiene to accelerate the oral hygiene adoption but I did not see anything innovative or dramatic from the house of Colgate India…seems they are content with 5-10% growth rate…at least for now…

Disc: Tracking position. No buy/sell recommendation. Post only for academic purpose. I can be completely wrong in all my assessments

My overall opinion on this business:

- A well financed, domestic consumption story with strong brand recall.

- Considering the performance of the past 20 Yrs & assuming (worst case) that oral care remains the only focus area, revenue growth of high single digit and profit growth of low double digit are highly likely in the long run.

- I feel that Palmolive portfolio is finally becoming an area of focus for the management, seeing the evolution of the Palmolive portfolio (shower gels, oils, body wash, shampoos, liquid hand washes) in the last 2 years. Hence, both the revenue and profit might grow at rates better than historical trend (shown below):

| 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 20Yrs. | 15Yrs. | 10Yrs. | 5Yrs. | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sales | 1176 | 1161 | 1057 | 1042 | 1073 | 1218 | 1385 | 1553 | 1758 | 2025 | 2317 | 2805 | 3324 | 3579 | 3982 | 4389 | 4560 | 4328 | 4462 | 4525 | 4841 | 7.3% | 9.6% | 7.6% | 2.0% |

| PAT | 63 | 70 | 89 | 108 | 113 | 138 | 160 | 232 | 290 | 423 | 403 | 446 | 497 | 540 | 559 | 581 | 577 | 673 | 776 | 816 | 1035 | 15.0% | 14.4% | 9.9% | 12.2% |

- Ability (basis cash flow statement of the last 3 years) of the business to generate 800+ Cr. Free Cash flow, could easily support a dividend of 30+ per share on ongoing basis.

Growth Levers:

- Premiumization trend

- Redefine oral health: New initiatives beyond toothpaste and manual toothbrushes such as sprays, & oil pulling

- Build the Palmolive portfolio

Concern:

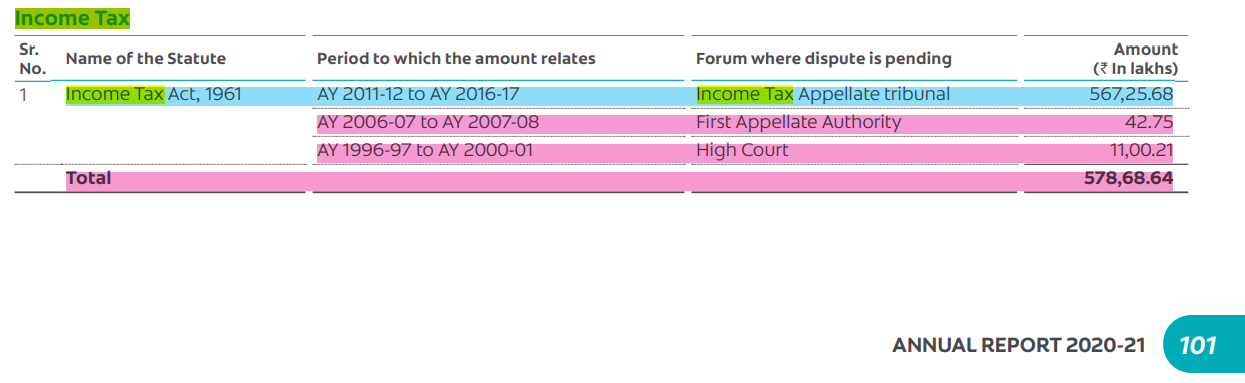

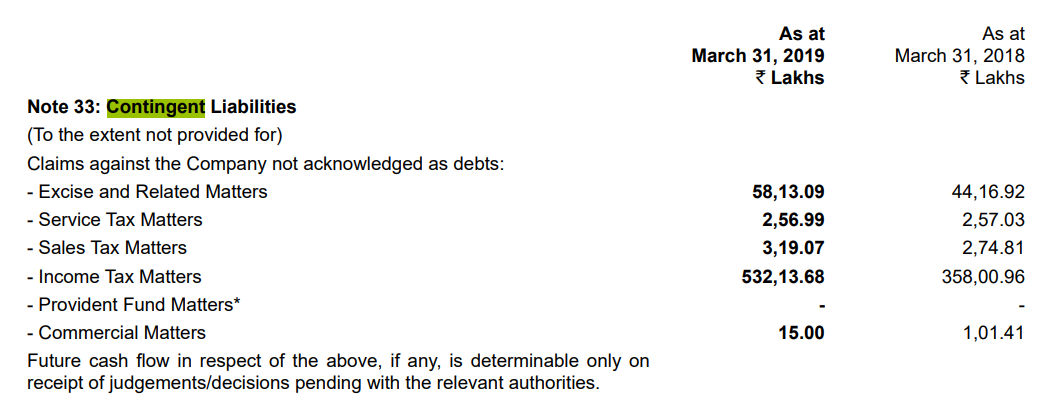

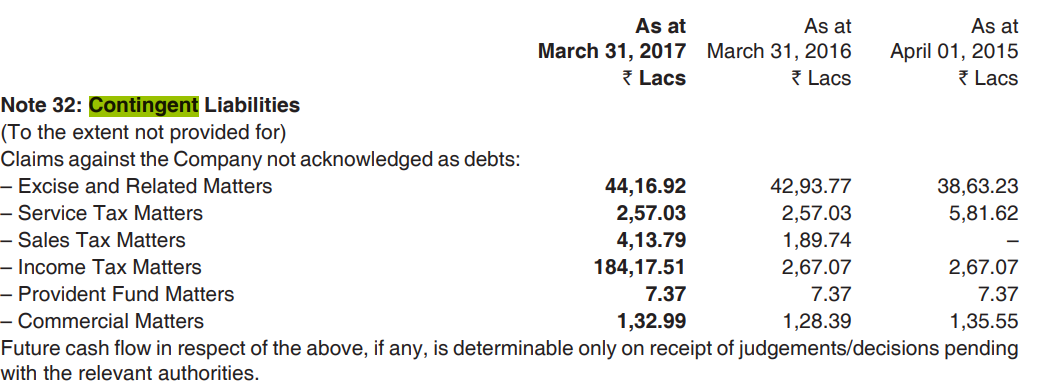

Contingent liability of ~900 Cr, which is not accounted on the Balance Sheet. Just wondering that how this will settle as it has largely accumulated in the last 5+ yrs.

Disclosure: Invested as it suits my risk and return objectives. Did transactions in the last 30 days. I am not a RA/IA. This is not an investment recommendation. The writeup is shared for collaborative learning.

Is the elephant dancing?

We are also excited about our entry into the Face Cleansing category with our new Palmolive range of Face care products. The range features unique and innovative forms such as face foams, masques & scrubs that have been created with a unique blend of premium natural ingredients and essential oils.

Contingent liability of 900Crore is a concern indeed!

Thanks for bringing this to notice, What exactly is this contingent liability and is it in sync with other FMCG firms, specially Foreign MNCs like HUL, P&G Hygiene or even a Marico, Dabur?

It looks like matters pertaining to tax, excise, PF etc. but why have they been accumulating over 5+ years? Why are they not being catered to every quarter or year vise? Thanks

• Weak 3Q numbers from Colgate. The hope that sales growth will pick with 1) steadying market shares and ‘naturals’ launches 2) better mix led realization growth from premium products – has not quite played out this year so far and certainly not played out in 3QFY22.

• Sales grew 4% YoY (5% two-year CAGR). This is much weaker than peers like HUL which reported 10% sales growth. The weak sales growth implies flattish or weak ~1-1.5% volume growth, as Colgate would have taken steep hikes to cover rising input costs. This suggests Colgate may not have fared well on market shares – possibly lost some shares or held at best but unlikely they have gained. Colgate mgmt. has made no mention of their market shares in the press release (something they consistently did in the past, until recently). This does not give comfort as to whether they have stopped leaking shares (although it’s known that pace of loss has reduced).

• Gross margins fell 320bps YoY and 20bps QoQ, likely due to a higher packaging cost, sorbitol prices and higher trade incentives (to drive sales given the pressure on sales). Colgate delivered flat YoY EBITDA margins of 30% thanks to sharp ad spend cuts of 24% YoY. This is a time to take up spends (to start gaining back shares) not cut them to deliver quarterly margin. At the least they could have grown ad spends in line with sales at 4-5%.

Colgate stands out !!! Interesting to note that Nestle diligently provisioned on the balance sheet for similar matters. However, AR of Colgate highlights management’s chutzpah to defend their stand in the court of law.

| Nestle | Dabur | Godrej | Britannia | Marico | Colgate | |

|---|---|---|---|---|---|---|

| FY 20 | FY 21 | FY 21 | FY 21 | FY 21 | FY 21 | |

| Contingent liabilities | 1 | 242 | 161 | 94 | 188 | 900 |

I think it’s already elevated w.r.t other businesses (Data shown below):

| Nestle | Dabur | Godrej | Britannia | Marico | Colgate | |

|---|---|---|---|---|---|---|

| FY 20 | FY 21 | FY 21 | FY 21 | FY 21 | FY 21 | |

| Advertisement | 764 | 784 | 986 | 451 | 698 | 625 |

| Operating Revenue | 13290 | 9507 | 10936 | 12880 | 8048 | 4840 |

| Advertisement as % of Oper. Revenue | 5.7% | 8.2% | 9.0% | 3.5% | 8.7% | 12.9% |

Thanks, not the point I was making. I meant YoY growth in ad spends should be at least in line with sales growth - don’t need to cut corners there when your market shares are in any case bleeding.

And basis your data, one wonders why despite doing higher as spends (% sales), Colgate is the slowest in terms of sales growth among all the above-listed companies (basis last five years).

I think this could be taken as implicit admission by the company that they can’t grow much in oral care and are finding it hard to even regain lost market share in toothpastes.

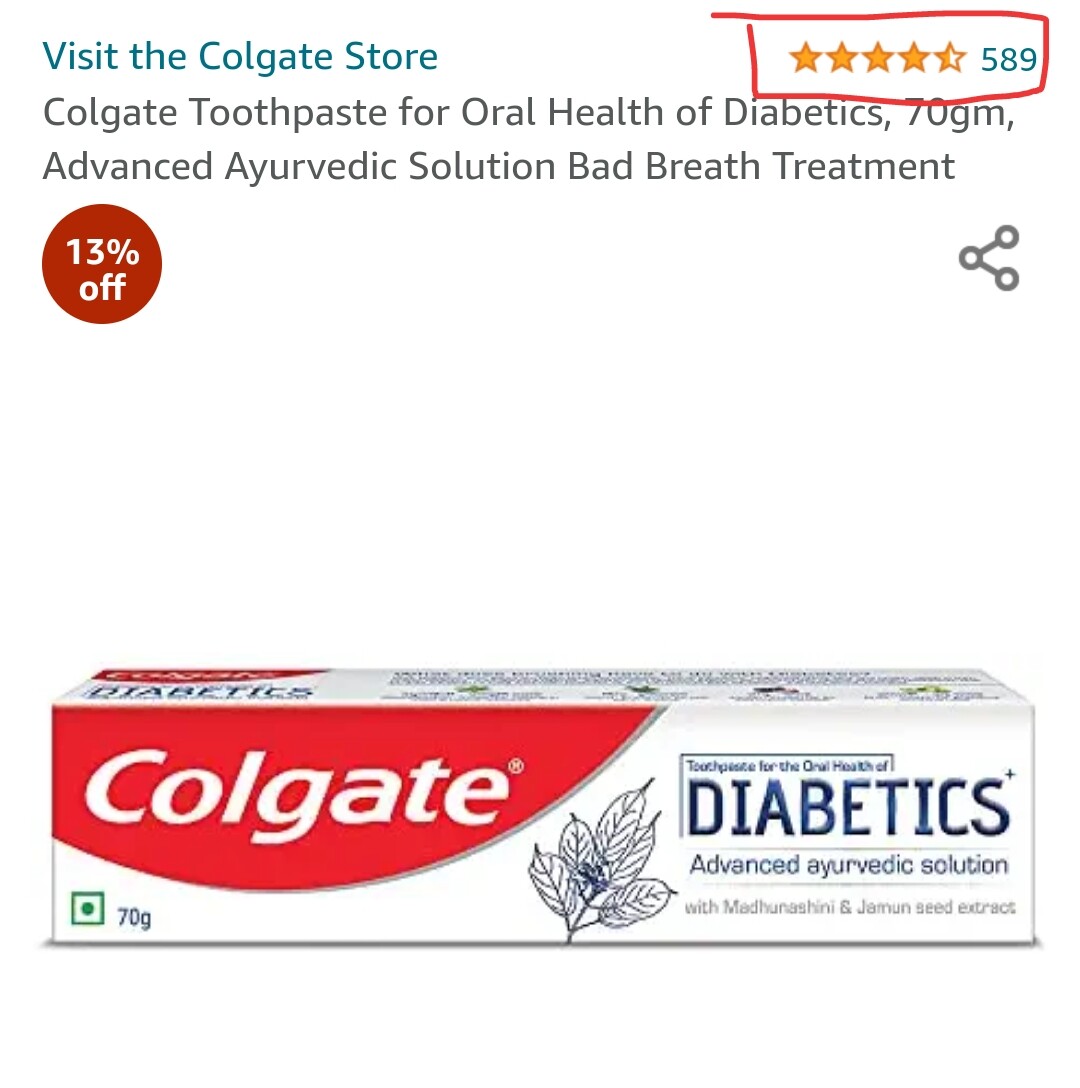

Does anybody has an idea How is Colgate Toothpaste - For Oral Health Of Diabetics, Advanced Ayurvedic Solution performing in the market?

Amazon rating is good 4.6 with 500+ reviews so a successful product

Note: Supprisigly Colgate visible white sales is 15 times of Colgate dibaties. Both are fancy with respect to normal Colgate. Which indicates no one is concern about dibaties while brushing (sugar present in it).As we eventually spit it.

What they care about is white tooth. So no point of analysis about success of Colgate dibaties as impact on revenue is less than 1%.

But if you suddenly here pepsodent, patanjali, dabur, etc dibaties toothpaste. Then they are successful for sure. Lol

Prabha Narasimhan from HUL named new CEO, Ram Raghavan elevated to global role.

Discl : Invested

Your insights were really interesting. I don’t know why Colgate launched their diabetic paste if it’s just less than 1% of their total sale. Though you talked about Patanjali & Dabur, so I did quick research to understand what’s happening there.

What was astonishing to me was that Patanjali is really giving run for money to Colgate in dental care. I think maybe the case because sales is subdued for the last 5 years. Here is a Youtube Video on a comparison between Colgate & Patanjali.

Also, Google gives a lot of news article on this. here are few links, which I found were insightful.

Do share your thoughts!!

Disc : Was invested earlier. Still tracking !!!

In my opinion, focus is now evident on the Palmolive brand:

- Selling online @ https://palmolive.co.in/ | 25 Products (08-Jun-22)

- Palmolive brand enters face cleansing category (13x Opportunity of body cleansing)

- May 21 Investor Presentation | No mention of Palmolive. However, conference call had one remark - “we will also figure out how to make sure we build the second leg of the business intelligence, which is the Palmolive portfolio.” In the May 22 Investor Presentation (https://www.colgateinvestors.co.in/media/2878/cp-india-analystmeet-26may2022.pdf), few slides are inked with the Palmolive brand: Slide 25 to 28 and Slide 59(Equal Half to Palmolive and Colgate brand)

Other Observations:

- May 22 conference call | Oral Care Products - 90% levels of penetration at the country level. Drivers for top-line growth in medium to longer-term | LUP (Low Unit Packs) focus, the premiumization focus and the innovation

- May 22 Investor Presentation | Slide 54 | New Products listed as another focus area