India’s most trusted brand from 2011 to 2018. Colgate-Palmolive (India) Limited is a subsidiary of Colgate-Palmolive, USA and a listed Company in India. The Company is engaged in manufacturing/ trading of toothpaste, tooth powder, toothbrush, mouth wash and personal care products.

Why Colgate?

Market leader in its category

Zero debt

Unwavering focus on personal care and hygiene

Recession free business and inelastic demand

Products/Brands

Oral Care - Colgate

Others - Palmolive

Toothpaste

Hand wash

Toothbrushes

Soap

Mouthwashes

Kids products

Specialty products

Marketshare

Toothpaste

Toothbrushes

50% (Leader)

45.2% (Leader)

Revenue Breakup

Oral Care

Others

90%

10%

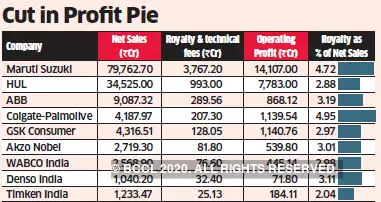

Royalty

Royalty is an additional cost that Indian MNC shareholders have to forego unlike Indian FMCG’s like Dabur. When compared to its competitor HUL, Colgate has paid almost twice in terms of royalty fees to its parent.

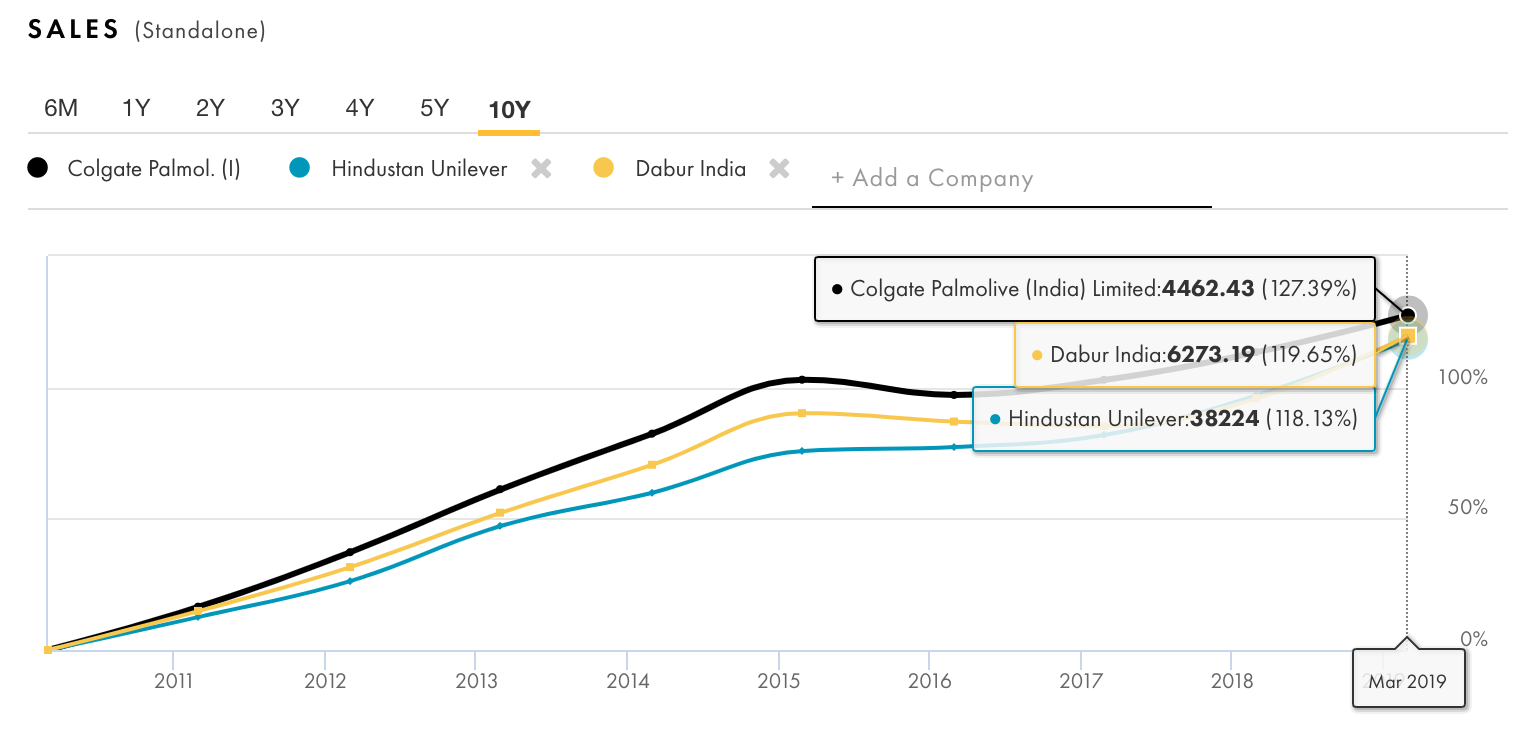

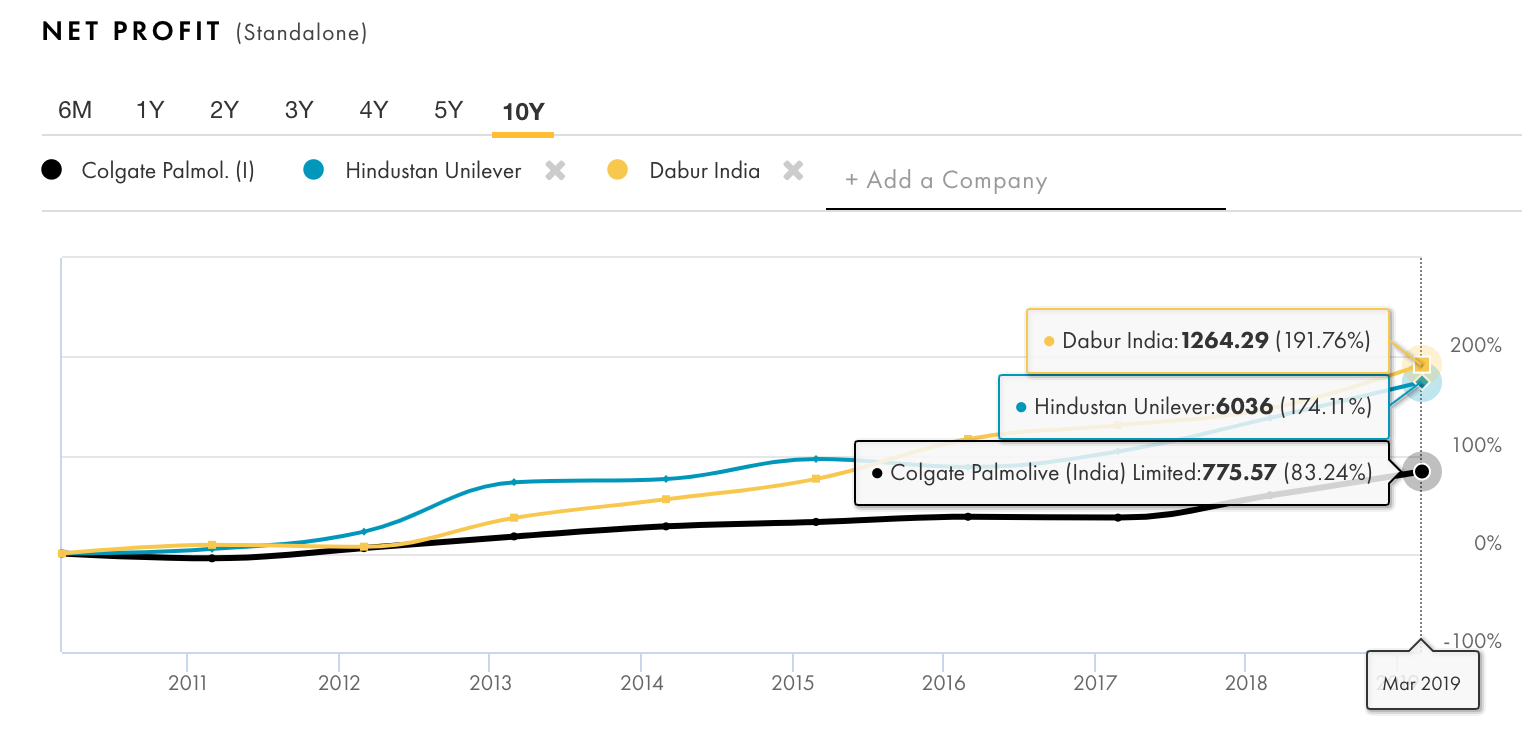

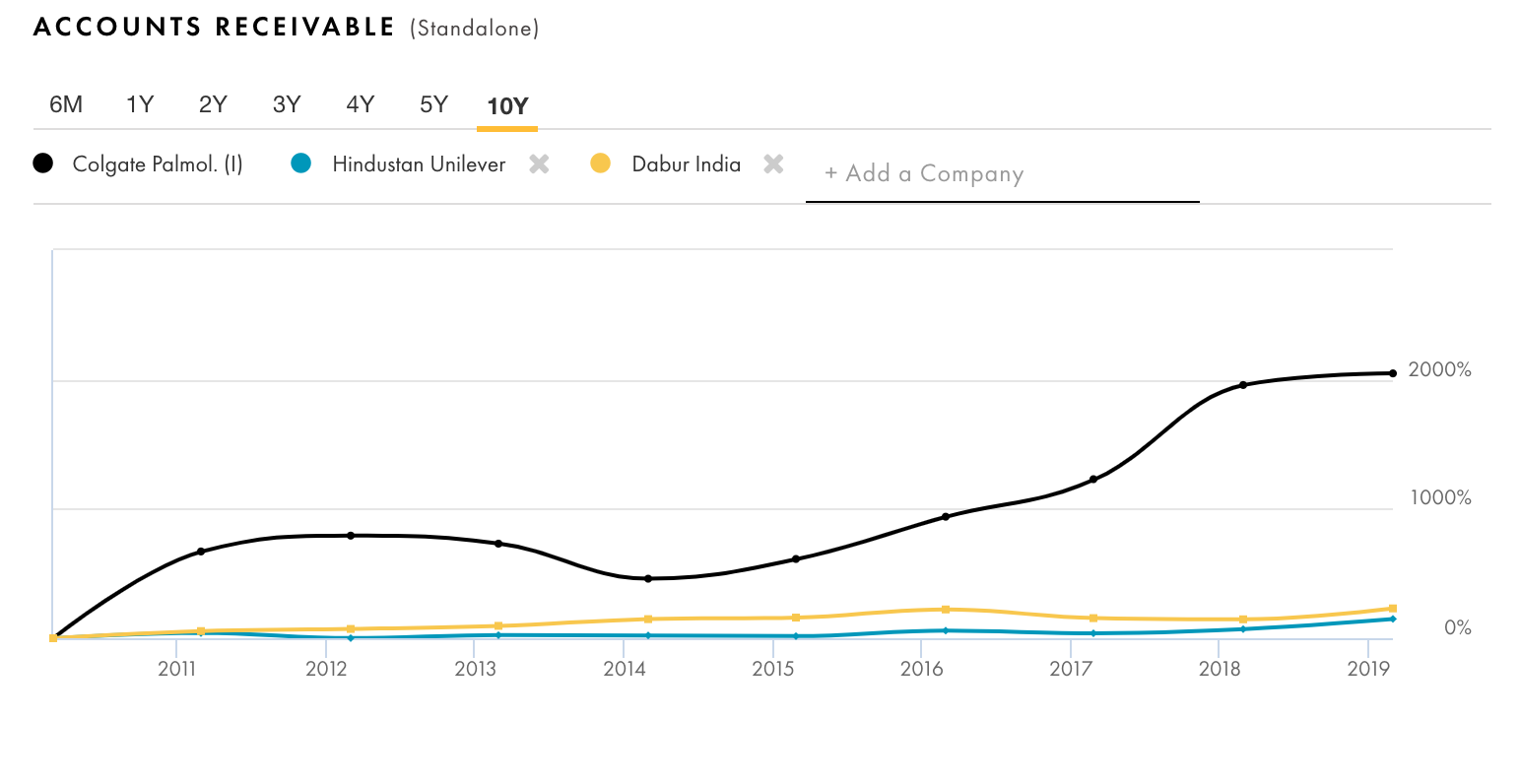

A majority of customers pay prior to shipment, thereby reducing exposure to trade receivables significantly. Due to a large customer base, the Company is not exposed to a material concentration of credit risk. However, in recent years, there is a notable spike in receivables as compared to its competitors. Do note that the competitors operate in multiple categories when compared to Colgate.

As per this report, 1/3rd of India doesn’t use toothpaste (questionable?) and only 1/5th use it twice every day.

Consumer Behavior

Unlike other consumer goods, toothpaste is perceived as a product that is subjected to changing customer loyalties in terms of switching to other brands. The cost of switching from Colgate to Close Up is not much and consumers like to experiment often.

For the price points that these products sell, any price discounts/offers can pull consumers from one brand to another.

Advertisements and availability (prominent shelf space) can also influence consumer behaviour.

Raising dental care costs and organized dental care is helping create awareness among consumers. More people are now using toothpaste twice in a day.

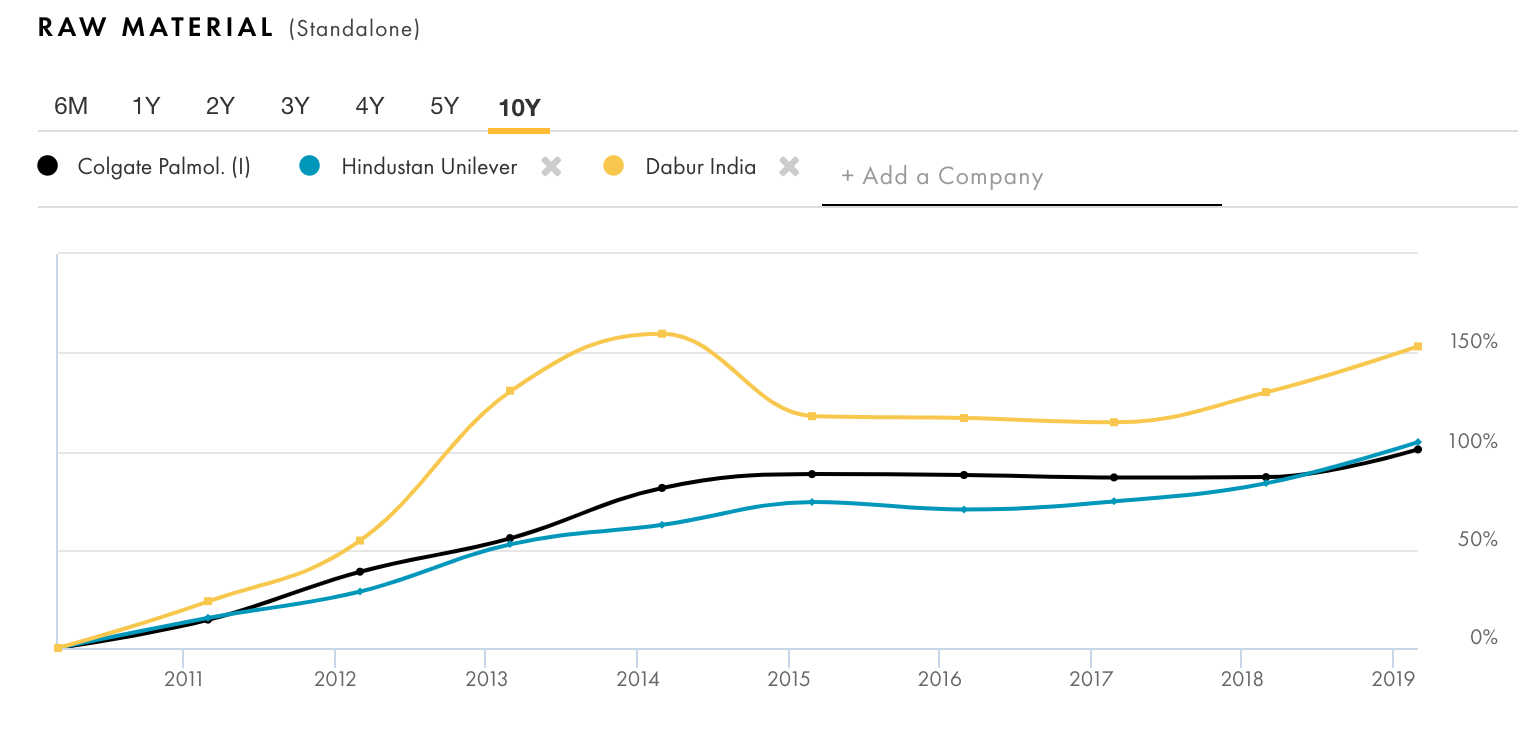

Raw Materials: Corn, Carton board, Resins and Palm oils.

A 1% increase in commodity prices would have led to approximately an additional Rs 6,19 Lakhs loss in the Statement of Profit and Loss (2017-18: Rs 6,52 Lakhs loss). A 1% weakening in commodity prices would have led to an equal but opposite effect.

Colgate seems to be doing well on this front as compared to competitors (not an apple to apple comparison though)

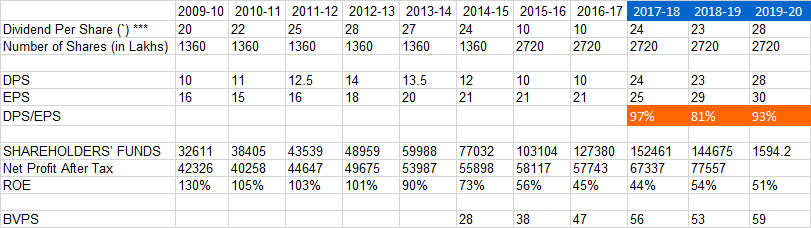

What’s their current dividend policy?

I checked the website and found the policy but the same does not mention a DPR number. From AR’s, I see that they are distributing almost all the earnings as a dividend in the last 3 years. Attaching below for reference-

How do you see this story from the valuation point of view?

In my understanding, HIGH ROE of 50%+ is deceptive in the case of this business because the buyer has to pay 23.5 times of the book value, resulting in an effective ROE of 2%+ on the initial investment. The past trend suggests that the business would not retain the incrementally generated earnings to multiply the same at HIGH ROE of 50% since the same is distributed almost as dividends. Good business: YES but Good investment at CMP: …? I do acknowledge that business has ‘REAL’ terminal value but doubt that it can generate ROEs of 35%+ in perpetuity.

Valuations for companies like Colgate is more of an art than science. Business wise, the bottom for this company might have come back when naturals were in vogue and companies like Patanjali were posing as a serious threat. At current price, I would not be rushing to buy. In hindsight, March was a good time to buy and I regret my position size is small, but I also admit it was not easy to invest lump sum at that point in time, because relative valuation was still expensive. Once you understand these businesses, wait for an opportunity and be ready to make the most of it.

There are a few changes that are happening in the overall Colgate global trajectory

They had a program called Global Growth and Efficiency program which was specifically for optimizing their supply chain and increasing gross margins. This program started from 2012 and ended recently on Dec 2019. The program was super successfull and Colgate India gross margins are at an all time high of 65.24%.

Natural and sustainable products is an important and high growth area across all their businesses across the world and people are willing to pay a premium for it. Some of the premium innovations in oral care are Colgate Natural Extracts , Charcoal toothpaste, bamboo manual toothbrush etc

Relaunches in cavity and teeth whitening products. Some Asia esp India focused products are Colgate Total maximum cavity were relaunched , there was a global relaunch in Colgate. There was a new launch of its hydrogen peroxide based toothpaste called Colgate optic white renewal in the US.

Globally, they are expanding their skin health portfolio. In 2018 and 2019 they acquired 3 skin care cos called PCA skin, EltaMD and Filorga. While they don’t have a skin portfolio in India - it’s good to know that they are enhancing their capabilities in this market- as we know India has a sizable skin care market.

Another interesting area is their fastest growing business i.e pet foods driven by Hills. Hills recently achieved the maximum sales growth in the last 11 years. While pet foods is a developed business in countries like US/Europe etc - it’s picking up speed in countries like India. While globally oral care contributes 46% to it’s overall sales it contributes 86% to its Asia business - so again chances of having a pet food business in India are next to zero. Pet foods is a small industry in India sized about 2200 Cr which is controlled by Mars (pedigree, whiskas, royal cannon)

Enlisting new channels e.g travel retail and pharmacies. These are channels which serve specialized products. We have a landscape dotted with pharmacies in every nook and corner so the possibility of using this channel to push specialized products is interesting.

I think Colgate is doing very well in having a plan in place to increase margins. One cannot expect high volume growth going forward however taking price through these initiatives will certainly see the ROCE increase going forward.

Find enclosed link for my working on Colgate for investor who hold shares since listing. The data is compiled from BSE and past annual reports. Amazing performance over 4 decades !!! Highest even return generation over 40 years. However, past is never indicator of future and hence it might be good to know it, one can not just blindly replicate same. One has to look at future prospect and valuation of company. I have bought Colgate in August 1994 for my uncle and have pretty mediocare return (comparable to fixed income) for almost two decades, despite good management and excellent market position, due to wrong entry price.

Decent performance with YoYsales up by7%+, net profit up by 30%+ , margin expansion, optimistic commentary, basic innovation continues, good interim dividend.

Was able to add some during Q1 correction, a decent slow but safe compunder for mid term(12-15%) including dividend on conservative side , if one is happy with such returns.

The writer seems to be thinking too much on a fairly simple business. Patanjali and other competition are valid threats and colgate fared pretty well. I feel the way it protected it’s margins in such tough times is commendable. You throw one thing at such companies and they come up with another ways to deal with any things which any of us can think or even not think of. This company globally has more years of existence than hours of economic lessons many of us, including the article writer and myself, must have attended…not to undermine the fact that maintaining margins would be tough…but that would be least of the worry for real long term investors.

Disc. Small position, not a buy/sell recommendation.

key highlights of the analyst conference

Recent launches are gaining strong tractions: Colpal did two to three new launches/relaunches in last two to three months. It launched Colgate Vedshakti mouth protect spray, which kills germs and provideslong lasting freshness. The launch got good traction in the domestic market (especially in urban markets) with strong consumer repeat of ~30%. It is already available in one lakh stores in India and is also gaining good traction on the online platform. Colgate Diabetics, which was the first-of-its kind oral care product for diabetes patients. The brand got strong traction and repeat sales of 20%. It is available in 25% of urban pharmacies and direct dentist reach (#1 SKU on e-pharma). Colgate Visible White, which was relaunched recently gained an over 80 bps market share in modern trade channel and more than a 120 bps share on the e-Commerce platform.

E-commerce and modern trade continues to perform well: E-Commerce and modern trade channels continues to perform well for the company. The e-Commerce business grew by 23x over CY2016-21 while market share on the channel improved by 1,400 bps between FY2021 and FY2021. Premium products are gaining strong traction on e-Commerce channel along with the core products. On the other hand, the company has market share of 170 bps on modern trade channel on back of proper SKU segmentation. Both these channels and general trade are playing a key role in delivering good revenue growth for the company. Chemist channel remains under index and provides lot opportunity to scale up through this channel in the medium term.

Focusing on strengthening in the rural market: Improving awareness of dental care in the rural markets is one of the key growth drivers. A strong network of wholesale partners is aiding regular supply of the products in these markets. The company is focusing on increasing awareness of better dental habits, which might result good demand for oral care products in the rural markets in the coming years.

Natural’s toothpaste continues to perform well: The naturals category constitutes 38-39% of the toothpaste market in India. Colgate Vedshakti has hold its market share for last three quarters. The category’s growth is ahead of industry growth. The company has gained market share by 60 bps y-o-y basis in FY2021. Sustained increase in loyalty to ~50%. Along with Vedshakti, brands such as Colgate Active Salt and neem variant toothpaste is performing well and adding value to Colgate’s naturals portfolio

New launches in toothbrush category gaining share: The toothbrush category (contributes ~15% of the company’s revenues) was badly affected in the pandemic environment as consumers deferred purchases, considering the product discretionary in nature. The company launch new products such as Gentle Enamel and Gentle Ultrafoam under the gentle cleaning feature, which gained market share of ~1% each within a launch of three months. The company has extended the Slimsoft brand with naturals variant of Himalayan salt and Turmeric. It also done innovation in kids portfolio with the launch of Colgate Magik. The management expects toothbrush to perform well in the coming years. In the current environment, the replacement cycle of toothbrushes is likely to reduce and Colgate expects good growth for the category in the coming years.

Strong cash flows and improved dividend payout: Operating cash flows improved to Rs. 1328 crore in FY2021 from Rs. 890 crore in FY2020 led by stable working capital management and strong improvement in the profitability. The company paid a dividend of Rs. 38 per share for FY2021 (dividend payout of ~100%) better than dividend payment of Rs. 28 per share in FY2020.

No of headwinds - Apparently lack of disclosure and investor connect, add that with market share losses( given others are gaining e.g. Dabur etc), higher push on mktg not yielding much outcome yet. Add this with RM inflation issues.

Curious case of good quality sector leader not delivering on expectations, though valuations are below longer term median level but no interest from market participants, weak on charts as well.

Was invested in FY21 as defensive bet, not invested anymore, on watchlist.

All FMCG companies are under pressure. There is sone talk of price war in FMCG companies. The dividend yield will increase as price falls down more, more strong investors will buy but that will help stock price or not is another question.

Valid points on headwinds. But purely from a long term perspective they have not done badly:-

Revenue has grown from ~3900 Cr to ~4800 Cr from 2017 to 2021

They have progressively increased OPMs during the same time period from 24% to 31%

Accordingly profit is up from 944 Cr to 1500 Cr in the same time period

Would expect toothpaste, toothbrushes and personal care (in case the focus increases) to continue to have a moderate growth runway ahead

Colgate with its brand strength always would have significant profit levers in its kitty, from price increases to subtle volume reductions to manage cost in the long term

It is a business which would be impacted by traditional mom and pop stores and traditional trade being impacted during COVID. Even if

Consumers still needed toothpaste would they have used as much of it or be buying bigger more profitable pack sizes during this period? Toothbrushes is definitely more discretionary and trade opening dependant

Increasing dividend payouts and strong cash flows

Current PE of 37 for an MNC FMCG sector leader with solid ROCEs and long growth runway looks attractive versus historical valuations. Short term headwinds might exist but in my thought process, in a hot market, this seemed a reasonable investment opportunity at current levels. Taken up positions basis the same.

Discl : Invested, transactions in last 30 days. This is just a personal view, not investment advice

Colgate faces the same issues as ITC: a high ROCE business with low growth. The company is a classic “quality trap”. It won’t be surprising if the stock continues underperforming for some time, or even falls till valuations take growth realities into consideration.

I think bigger issue with colgate here is that they have all levers and opportunities of growth…like Palmolive was a great opportunity in personal hygiene during pandemic, so was oral care, mouthwash, antivirus mouth sprays etc. Could have been some exciting new product launches from segment leader…but they chose to stick to basics here…even their global portfolio of oral care is not utilized to fullest in India…

Two type of companies can afford to do this- one is an incompetent one which failed to grab the opportunity and second is someone which looks much much beyond and sticks to its core and larger set of targets…colgate bring century young corporate would fall into the category of second i.e. most mature, confident and with its own set of rules…

Important here would be to understand colgate india’s long term vision here…as only that will give right answers here and I am sure they will achieve what they intend to…

Apart from fundamentally picking stocks I also do option trades. This time have sold 1500 puts to accumulate some of colgate. Based on the fundamentals the price is at a good point, where dividend yield and high ROCE would contain downside. And its a major brand, any good news would immediately attract buyers.