Why PI Industries? Isn’t it in cyclical business? How can we guarantee consistent sales growth? Hope you share your views. Thanks

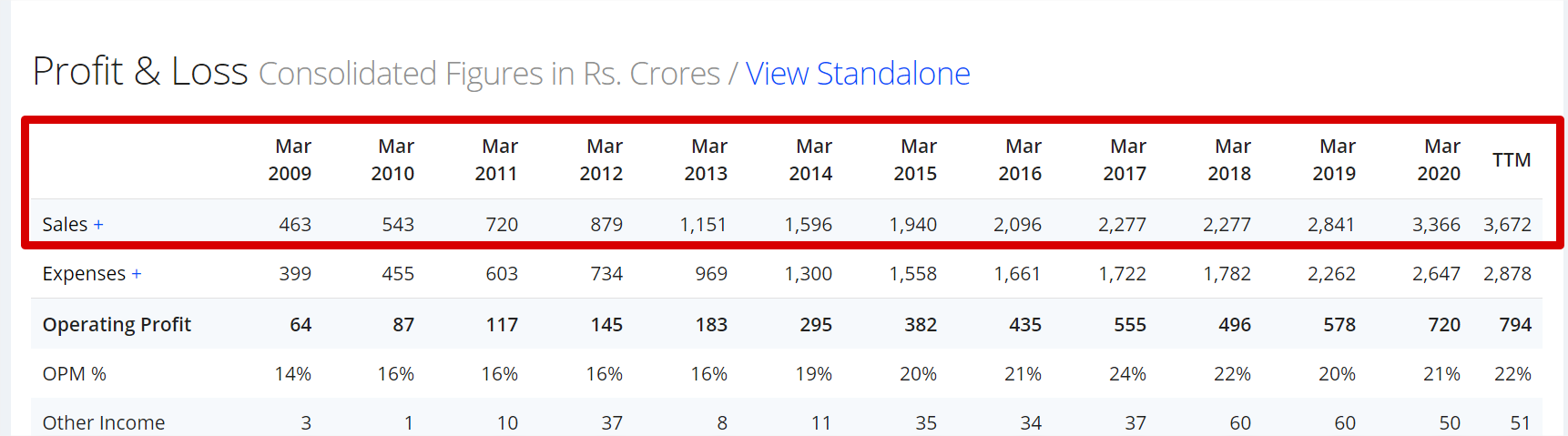

Hi, There are many industries where we can debate if they are cyclical or not. I put PI industries under same category. It might be just my opinion. I think demand for Agri Chemical will keep on growing due to world’s need to grow yield on the same amount of land. Hence we need to put more chemicals/fertilizers etc to improve yield. Also govt is spending lot of money for farmers. My thoughts are that farmers will spend it to increase the yield. About consistent sales growth, see below 10 years of sales of PI industry where sales keep on increasing. I hope it answer to your question.

3 Likes

Agrochemicals industry is semi-cyclical and the downcycle depends on poor monsoon. And so globally diversified Agri-inputs players are at an advantage as at all years some nations have good rainfall and some have poor. In the listed universe of Indian stocks UPL is a true globally diversified Agri-inputs player and so a Buy & Hold candidate if they can successfully repay the debt.

PI Industries is an indirect global player with much better business model than UPL as they do the custom manufacturing of agrochemicals for innovator companies who are globally diversified. PI has an agri inputs business too where they in-license and market innovators molecules. UPL on the other hand is a generics player like its Pharma counterparts Lupin, DRL etc.

7 Likes

Interesting, can you elaborate on this point with some examples and why would they do well for investors…for eg. In green fuel direct investing, I can think of something like NHPC or Tata Power to some extent but there are so many variables in this sector, I am not sure if the boom of green fuel will result in excellent performance of these stocks…same for most real estate picks…would be good to know your thoughts

1 Like

Although it was not addressed to me can’t resist the temptation to answer. I feel that NHPC or Tata Power are not good Green Fuel plays. One name that comes to my mind is Praj Industries, but not sure if one can have it as part of Coffee Can Portfolio.

Proxy plays should work well in this case and in that aspect we have secular stories like Pidilite, Astral, Paint majors, Kajaria, Cera, Consumer Durable Players etc.

1 Like

Thanks, curious why you feel NHPC and Tata Power are not good investment candidates?

Kotak Bank and Bajaj finance would need significant monitoring…at least every Q…Bajaj fin is after all a mere lending NBFC, Biocon would need every Q monitoring as it survives on whims and fancies of big brother West, PI and motherson I do not track and lastly L&T is cyclical…they themselves aware and hence want to grow their services business…I like and am invested in ITC and Britannia. Thanks

I said they are not good or true ‘Green Fuel’ Plays. They are mainly traditional fuel companies AFAIK with some exposure to green fuels. I haven’t studied them properly and so not much of an opinion about how good investment candidates they are. However, I strongly feel that such energy companies are not secular plays and so may not fall under buy and forget criterion.

2 Likes

I disagree that the growth is limited, India isn’t a CNG nation, maybe 30-40 years down the line!

IGL and MGL has been winning other GA’s /, the best thing that the government is finally opening to expansion in other areas!

Although it had allowed other companies to occupy the 20% of existing capacity, the long term lease does give more sense of stability of the business and also the existing pipeline is going to reap them benefits forever.

Talking especially of IGL, collaboration with regional player, like GAIL is going to give them an edge over the new players!

How I see this space is unlimited demand and almost no supply, also the MOAT around this business is allocated GA’s and existing pipelines!

I definitely see this in the 10 year long term portfolio!!!

1 Like

What if there comes a government regulations on prices or any rules on profit sharing or licences to operate? Like how happens in oil fields/petrol/telecom etc. If Gail opens up retailing and has the blessings of government, can private be as profitable as now? Lastly, what if 10 years down the line India is neither petrol nor cng but largely and completely an electric nation? Pls note I am not saying these companies are not good investments, it’s just that above questions arise when I think of energy companies in India…would be glad to know your thoughts as you are very positive on long term prospects of these companies and I would like to be corrected here as I miss a solid energy component in my portfolio since old ONGC days😀

2 Likes

Agree with your views that 10 years down the line it would be neither diesel / petrol nor CNG/ LNG.

Petrol or diesel is a mixture of Hydrocarbons. One molecule of Petrol contains on an average 8 carbon atoms, so if burnt , one molecule of petrol would give 8 molecules of CO2…

Similarly, one molecule of Diesel contains 16 Carbon atoms and so if burnt gives 16 molecules of CO2. That way, CNG may be better than diesel or petrol as one molecule of CNG contains one carbon atom so if burnt gives out 1 molecule of CO2 . Yes , CNG as automobile fuel has done it’s job in last 30 years since it was introduced in 1990.

However the future is Zero Carbon emissions… due to the threatening Global warming , climate change and so it is time to look for Solar , wind and energy from ocean waves… Look at Adani Greens with astronomical p/e… there is no stoppage…

For automobiles, it is only electric vehicle …look at Tesla… in fact our Govt has already declared its intention to incentivise electric buses in cities.

However at best CNG may still be a preferred option as PNG for kitchen…until solar cells become popular for cooking our food .

6 Likes

Check the cash flow statement under investment

THINKING ULTA HO KE : Invert

Cofffee Vs TEA

Coffee Can investment is WELL SUITED for the Institutional Managers . They are the zebra sitting in the inner most circle in the country of lions as they are accountable for other people money .,

The game for the retail investor should be finding the small cap well run companies with growing market share and the with product which is not easily get disrupted by the Giants. COFEE is always a costly than tea ( yet green tea is more of value )

one must find TEA companies rather COFFE because it CAN be or CAN not be a the VALUE enhancing as WIN WIN for all .

THIS is well run agenda of institutional or mutual fund houses to promote what they have . Koi HALWAI APNE DAHI ko KHTTA nai Bolta . These are good compounders

T: Target oriented customers probably with an industrial product / Packaging Solutions providers , Niche chemicals supplying to giants

E efficient Jockey with skin in the game

A : accountable management towards the value enhancement of all stockholders including suppliers , customers employees and shareholders .

On diversification : if there are 50 people in the room each has different convection for the stocks they hold say all have minimum 16 stock so together they have 750 stocks and say around 50 % of the stock are common in all the portfolios ( off course each one has different allocation based on the conviction ) so 8 + 50x8 = 408 stocks if one hold 408 stocks than can we say the person has diluted the effect of his / her capital … Being retail investor one must have concentrated portfolio … This is the thought Promoted by shrud market experts …

SHIT do happen in the market and that is True . Retail investor can’t influence the faceless mania of the fall or rise of the price ONLY and only thing he can control is the BUYING price … and the STOCK in which he want to enter . So only control what is controllable that is one’s exposure to ANY Stock . As Senior VP always said they are many ways to skin the CAT and so is true in case of Market and CRCKET both is game of UNCERTANITIES . One is Lucky if he buy the growing stock but at the same time one must Preserve the capital … That can be only Done by Studying HARd … Success is never accidental but a buy product of HARdWORK .

Happy Diwali and investing

Regards

6 Likes

sorry its bit late to reply, my opinion, ITC can be replaced with Tata Consumers, HDFC Life can be replaced with HDFC bank.

ITC: they have underperformed, management issues.

And HDFC Bank should definitely find a place in Coffee Can investing.

Nowadays most AMC’s have launched an ESG fund …but Mirae AMC has recently launched an ETF called ESG sector leaders fund with low expense ratio. That is where a lot of FII are interested in …

While going through the portfolio , I noticed one interesting aspect…it looks like a Coffee can portfolio…first 5 stocks are heavily concentrated… … First 10 stocks occupy 75% of the portfolio…though there are too many other stocks with just around 1% or less than that…

All these are supposed to be ESG compliant as per a score…or else the FII’ s would not buy.

Please scroll down & down to see the portfolio to view in terms of % each stock occupies.

6 Likes

Do read the following document to understand Aditya Birla Group’s grand aspiration to become the number 2 player in the paint section. Given the might and reach of the group it will be interesting to keep an eye on this space.

Also, given that the paint companies like Asian Paints, Berger Paints and even Kansai Nerolac had been long term compounders and so coffee can type stocks, it would be interesting as to how they counter this imminent threat.

7 Likes

Hello everyone. I have made a screen called Coffee Can Portfolio on screener.in

Sharing the link for the same. Would appreciate feedback.https://www.screener.in/screens/204312/Coffee-Can-Portfolio/?page=1

3 Likes

This is a really interesting discussion b/w proponents of coffee can and mean reversion. A few interesting points:

- Contrary to common perception that quality grows at 20%+, Pidilite and Asian paints have grown their PATs at 13.8% and 14.05% respectively over the last 10-year, and sales at ~11%. This is the exact same growth number reported by ITC.

- 10 years cumulative PAT (FY12-21) of Asian Paints are ~18’440 cr. and Tata steel made 10’341 cr. in last 2 quarters. Market cap of Asian Paints is 2.7 lakh cr. vs 1.3 lakh cr. for tata steel. About a year back, tata steel was valued at ~36’000 cr.

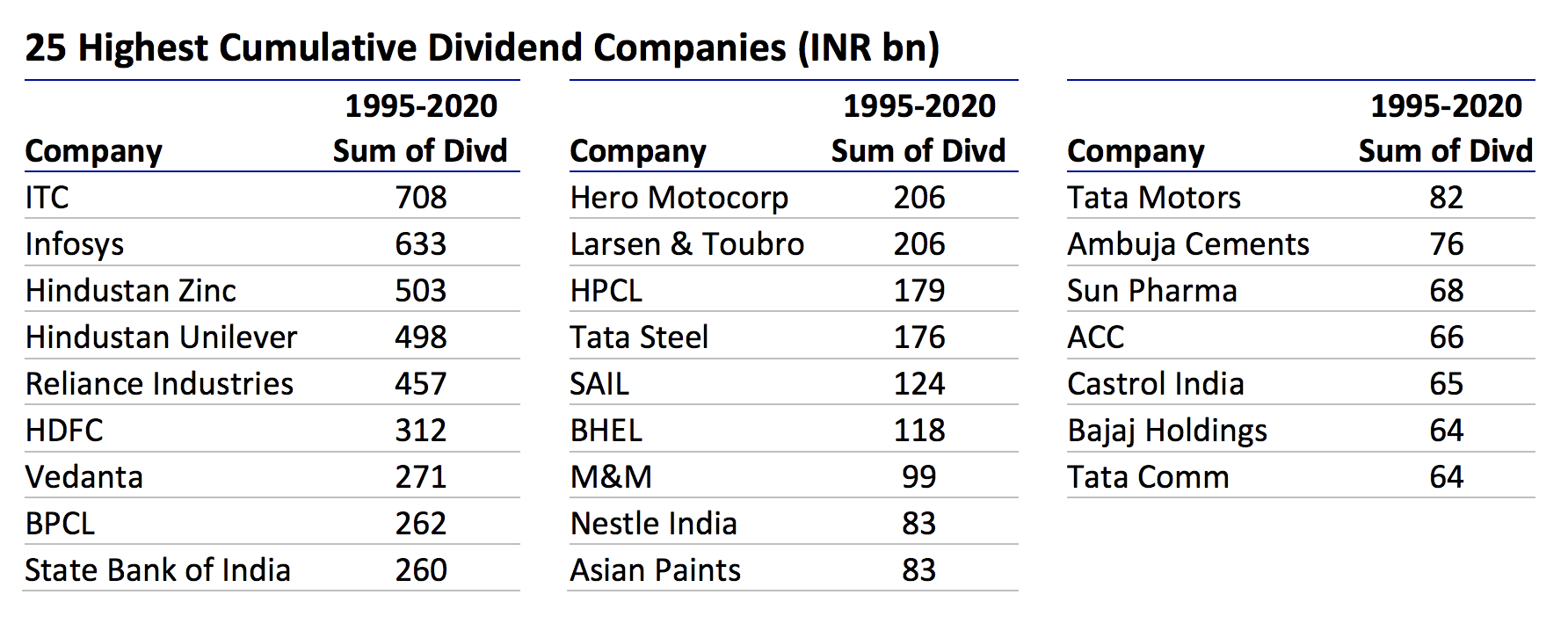

- Hindustan zinc (market cap: 139’203 cr.) has distributed more dividend than Hindustan unilever (market cap: 548’993 cr.) (Motilal 2020 wealth creation).

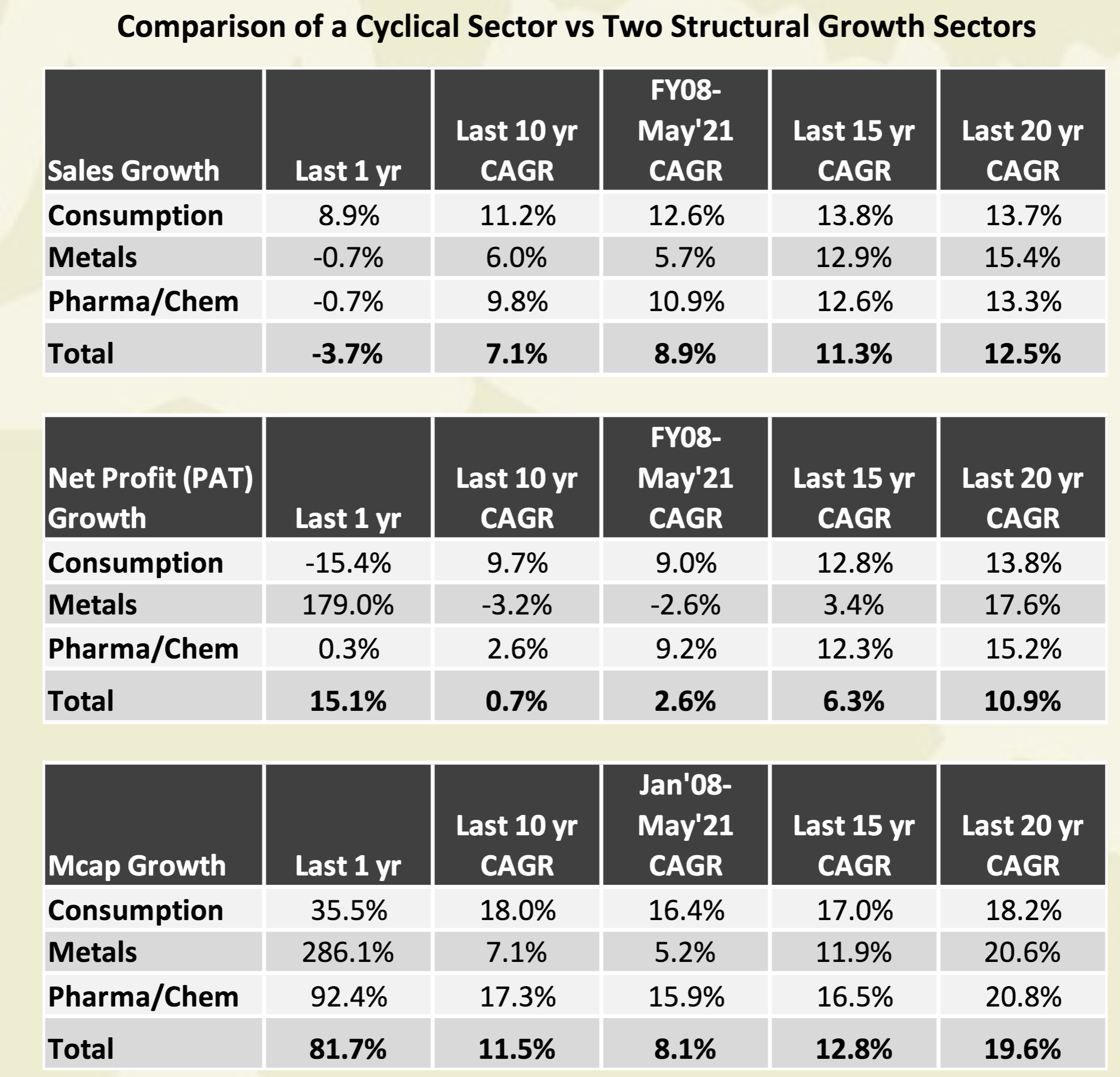

- Over the last 2 decades, metals have grown faster than consumption and pharma stocks (in terms of sales and profits) (Samit Vartak latest memo)

One thing that is definitely true (and something that I find very counter intuitive) is if we buy a basket of good stocks and forget them, only a couple of them drive overall portfolio returns. Here is an example from our own VP public portfolio.

18 Likes

Thanks for sharing this comparison, it makes me feel Asian paints is undervalued even at 2.7L cr. when comparing it to Tata Steel…

2 Likes

Hi where can we find this comparison data ?