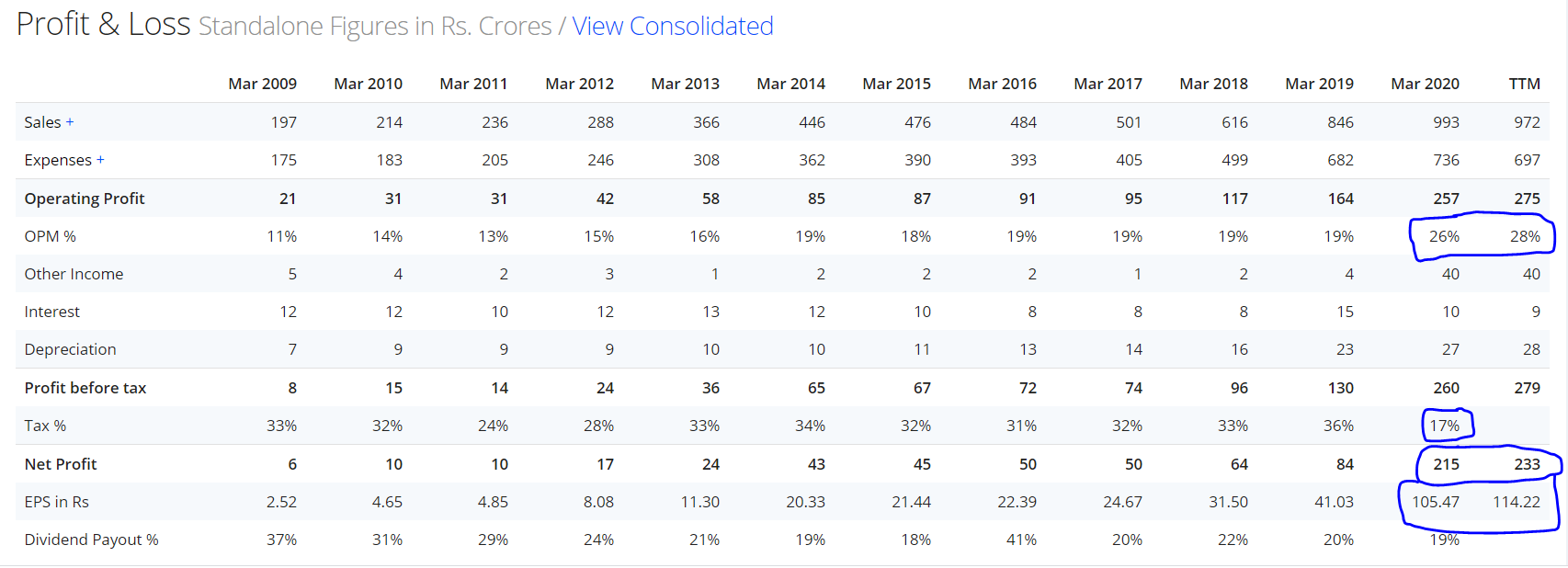

The CAGR numbers look fascinating because of the recent elevation in earning. If you consider till 2019, the growth numbers are not that good to qualify the stock as a Coffee Can Investing.

And the reasons behind the huge growth in earning are -

Moderate increase in sales

High increase in OPM

Lower Tax rate

Now the sales growth rate can be sustainable. But OPM and tax rates are not sustainable as the sector is exposed to changes in price of raw material.

For your information, Coffee Can investing does not follow CAGR, they emphasize on YOY growth rate. So I am still skeptical.

There is a confusion regarding coffee can investing in this thread. People are getting benefit of a strategy with minimum holding period of 10 years in 6months time.

Stock selection based on quality and growth filter is called quantitative investing (Quant). Check the Quant thread to gain insight.

Coffee can investing is a method where a bunch of companies are bought and left as such for a long duration of time. What happens is that the good companies grow and increase in size leading to a higher allocation and the bad companies reduce and form tail. Few companies with higher allocation will contribute to the bulk of returns after long time.

It was discovered by Robert Kirby who found that one of his client bought his recommendations and put the certificates in deposit box and never sold. His wife inherited his portfolio which contained few stocks which have grown to astronomical levels. He performed better by ignoring sell recommendations and being passive.

Any company can be kept in a coffee can portfolio. Only criteria is that one has conviction that it will survive and be bigger after 10years.

Which factor mainly contribute to the return of coffee can investing?

Excellently put and brought back to track on true coffee can investing what it stands for. A person who is a laid back coffee can investor doesn’t have time, energy and patience of over analyzing, screening formulaes, yearly/quarterly assessments to change his coffee can and so on and so forth. The only energy and patience he has is to hold on to his can.

When investing in equities, a person has to take two decisions.

Stock selection

Capital allocation

Stock selection

Buying quality stocks will improve the results as they have a higher probability of surviving long term. So it is better to invest in a bunch of quality stocks when making a coffee can portfolio.

Capital allocation

There is a thread on capital allocation. It is important as capital allocation determines the end result more than stock selection. The stock forming 30% of your portfolio will determine the portfolio returns more than the 2% stock.

Most recommend allocation according to conviction or equal allocation. Factor allocation can also be done.

At the start of forming your coffee can portfolio, you can select stocks according to your liking (quality, low volatility, value, momentum, conviction) and can allocate according to your choice.

From the next year, your capital allocation will be determined by the increase in the price of stocks. The companies with highest price increase will form the bulk of the portfolio after few years. They will decide the portfolio return.

So increase allocation to stocks with highest price movements ie momentum can explain the alpha of coffee can investing.

Any counter views are welcome.

Problem is that price momentum exists for short term, so at the end of that period the investor will be left with a large allocation of that investment. So, this strategy while capable of creating alpha will need regular monitoring to understand momentum and then to reallocate in opportune time, both of which are not exactly laid back type of investing.

Exactly. In coffee can investing we won’t rebalance at all and let the winners be the largest proportion of our portfolio.

Momentum investing has a saying ‘cut your losses short, let your winners run’. In coffee can investing it can be modified to ‘let your losers rot, let your winners run’.

IMO, Valuation always matters when buying a stock. How the growth trap would be avoided? It is a question which need serious deliberation.

Growth does produce more output, more income and more buying power. They tend to support the stock prices. But the prospect of growth often creates too much excitement and results in overpricing, especially in emerging economy like India. The allocation based on conviction with a singular factor of momentum can many times become counterproductive and returns become sub optimal. The reason being that the expectation already got build up in company stock beyond fundamentals sometimes.

I think blind sleeping over many stocks in expectations for many years may be counter productive.

Yes, value can be used to form a coffee can portfolio but it will be momentum which will determine which stocks increase in size and form a larger part of your portfolio after few years.

I don’t recommend buying stocks in momentum for the portfolio. There is always a risk that all your picks turn useless. That is why I would prefer quality with value.

I’m thinking of constructing a coffee can portfolio of large companies as a way to ensure that i can deploy capital in a less risky way than my core portfolio (which consists of mid and small and microcap companies). Towards this end, looking for feedback on the following portfolio I had in mind:

Kotak Mahindra Bank

Bajaj Finance

ITC

Britannia

Biocon

PI Industries

Motherson Sumi

Larsen and Toubro Infotech

My primary criteria for picking has been to think about the next 10 years and think about companies which are bound to do well in next 10 years (since this is a shut it and forget it kind of a PF). Would be open to adding/modifying companies to this list and any other feedback.

Your serial no 4 & 8 are same !

ITC may be good from vauation and future business profitability point of view …but nowadays ESG investors/ FII and even a lot of HNI investors may avoid this stock because of cigarette business. Therefore , the stock may not give you desired returns , though the company performance may excel… You may think of replacing ITC with something like Tata consumer or Nestle …

Also , I would like to avoid motherson sumi since Auto business is cyclical… Rather I would go with a Tractor business or a 2 wheeler business or simply skip Auto…and think of adding Asian paint or pidilite… you may also consider adding Divi.

I think it is very difficult to predict what sector will be market darling in 10 years. Auto is cyclical, but motherson has managed to grow despite that. Their latest 5 year plan has a large target of growing revenue 4x in 5 years. I know they will fail, but in doing so, they would grow is 2-3x which is great for an investor.

Btw just because FMCG has been market darlings in the past, it says nothing about what would happen in the future. Their valuations can easily revert back to mean quite easily in the future. Have a look at how HUL valuation has only gone up in last 15 years. This is certainly not sustainable. Even with Britannia and Biocon, I would stagger by buying as much as possible to reduce this effect as much as possible.

Thanks for the advice, I definitely appreciate it.

The portfolio overall looks neat & here are my 2 cents :

Shut it and forget it for 10 yrs is a uncomfortable going in statement with the level of change in society , you just cant take that approach , i hope you meant you wont churn and allow these investments to compound but at the same time keep track of their quarterly / Yearly performance in parallel .

Next 10 yrs could have the Green fuels & real estate up-cycle , should look at fair representation to that aspect or some proxy sectors ( if interested ).

There was some recent digital Media article on how Motherson sumi is obfuscating their financials…i dont seem to recall the digital media co. which wrote that recent article … …need to be aware of it & I personally don’t prefer a co which has too many Acquisitions @ a regular pace …leads to lot of integration issues & mgmt bandwidth gets dissipated in those areas ( even though the mgmt is always positively coloring the acquisitions ) but its better to be circumspect especially its your no-churn for 10 yrs portfolio.

All the best !

Thanks for the clarification, yes i intend to track them infrequently and at lower priority than core PF companies. Definitely once a year. Once a quarter if possible.

All real estate players seem to have large geographical concentration risks. NCC (the second largest construction co) is already part of my Core PF. Will evaluate L&T in case it makes sense to add.

Any suggestion on Green fuel companies to evaluate?

I think Motherson is definitely quite complex. But i have followed management commentary and meta-commentary as well they are actually simplifying the structure. Also their acquisitions have a rhyme and reason behind it - it is their clients who are asking them to make the acquisitions. These are made at a very favorable price.

Also wanted to add 1 thing: i intend to maintain equal allocation (by cost) at most times because of a difficulty to judge size of opportunity for these large/complex companies.

Thanks for adding your thoughts, it has definitely given me something to think about.

On Green fuel, next 10 years will see more of CNG , LNG , Ethanol, methanol, Bio gas and increased Electric vehicles…Disel , petrol vehicles would be minimised

Solar, Wind , will replace thermal power plants using coal.

No recommendations but i personally prefer the following :

Green Fuel : IGL , MGL ( personally not invested due to valuations at this current time ) but it has lot of govt. controlled dynamics , need to be aware of it …but the mkt universe is humongous for any co. which plays its cards well in this sector…Best of luck !

Both IGL & MGL are great companies !

But, their 80% business is from Automobiles in Delhi & Mumbai respectively…so growth is limited… Where are the roads— Already congested with traffic…also Metro rail being expanded will take away some vehicle traffic load … Moreover, Both these cities will have more and more electric buses.

Also , to break monopoly of IGL & MGL, Govt has already permitted dozens of companies to operate gas Distribution in many other cities…

In my humble opinion, if you are asking for other’s opinions on your portfolio you might want to double check your need for validation from a behavioural finance point of view. The views will most likely hinder than help you anyway

That sounds wrong on many levels. But just to take one up, the views are not for validation. The views are for actively seeking disconfirming evidence. You might want to check this out: