“What the wise man does in the beginning, the fool does in the end” - Howard Marks

So timing is of huge importance in stock market. I have seen most of the fund managers, who come on TV, always peddle their favorite stocks, after they have purchased these stocks cheap enough… I have tried mirroring stock selections of great investors for many years to my detriment… So now a days, I have stopped believing in my “good luck”

So rather than copying one individual/fund house (and spending energy to find out which is that great company in his/her portfolio), let’s focus on the various methods of coffee can method and debate pro’s and con’s of these methods.

Agree - Purchase prices matter unless one holds for long term. Buying a coffee can stock like HDFC Bank at 800 INR vs. 1150 INR makes a huge difference over short and medium term.

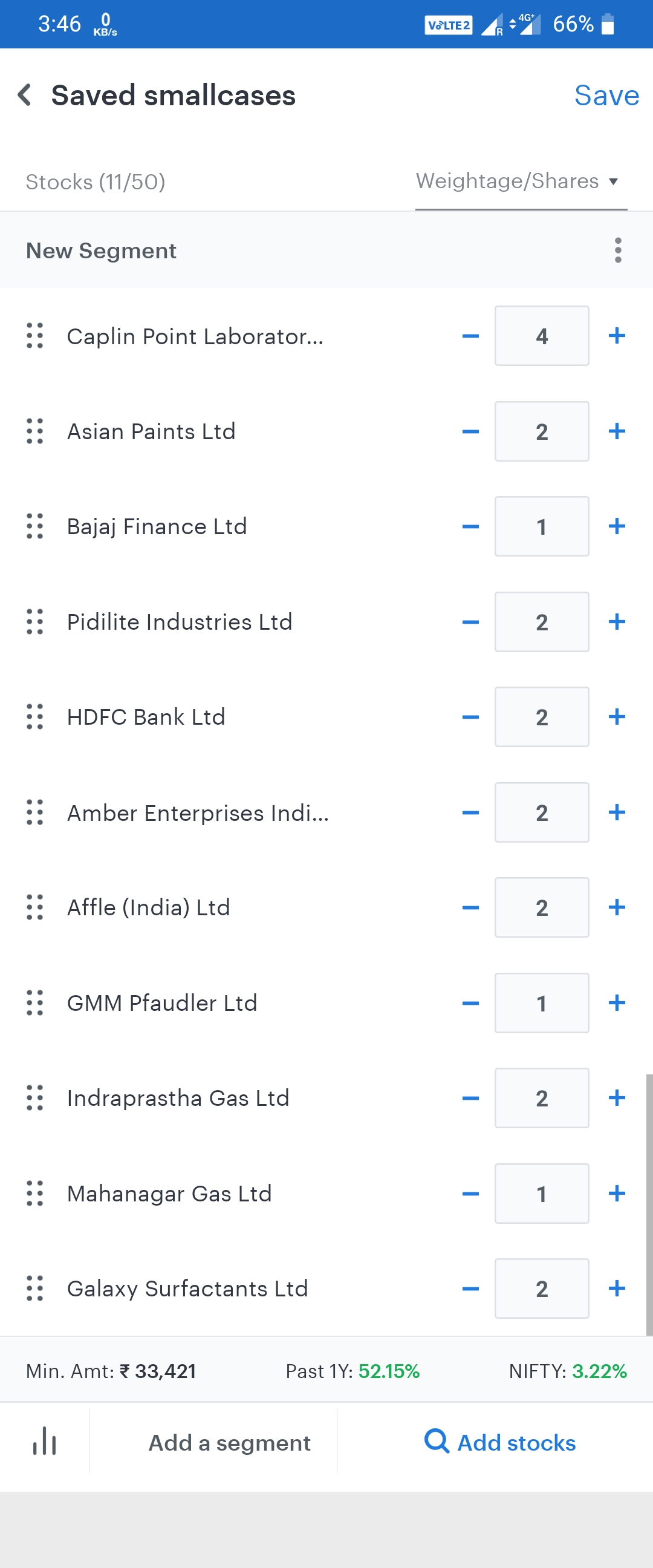

If one is mirroring, one must make a smallcase, weight it either equally or by market cap and place order through the small case. In case one tries to pick the ones that are low priced from the portfolio, one is not buying the full basket

Saurabh Mukherjee in one of his interview himself said that after selecting and buying stocks one should disclose the holdings so that more investors might come in to buy those stocks.

Anyways the point of this thead is to find out and discuss possible Coffee Can stocks that we can hold for 10+ years and not just discuss what Saurabh Mukherjee is doing.

Some of the stock with strong brand name and management that I would like to hold for 10+ years are-

This is a good list. Cyclical stocks are not coffee can stocks as the timing of entry/exit becomes very important. So stocks like Bajaj Auto are not coffee can stocks

My thought is always to buy coffee can stocks. To buy them when there are earnings surprises or short term bumps. Example: Pidilite fell to 1315 yesterday, Relaxo to 580 earlier in the week. These will be very rare and short occurences. During these times, one must build big positions to ensure one is fully invested and then sell on the mean reversion to buy other coffee can stocks on similar surprises. My coffee can list

Pidilite

Astral Polyteknik

Cera Sanitaryware

APL Apollo

Kotak Mahindra Bank

HDFC Bank

Biocon (This has become 5-fold in last 5 years and looks good for more)

Relaxo Footwear

Page Industries

Saurabh makes a few very interesting points in his interview

Return is not proportional to Risk. Indian stock markets work differently. We will get on a stretcher if we take too much risk

Managing a fund is a responsible exercise and he is responsible for the 3000 odd families who have imposed their faith on him. He will not speculate

This point raised my respect for Saurabh.Look at the way many mutual funds have invested in all kinds of fancy stocks indulging in speculation

Once there is a high margin industry like APIs (due to movement out of China), lot of P/E players will jump in and fund these firms. The high margins will not sustain beyond a year or two.

One must also remember that P/E of Coffee Can stocks is high because they are in high demand, as the prior performance is extrapolated to continue in coming years. These companies have clean accounting, are non-cyclicals, have strong moats and potential to reinvest the earnings profitably to further their growth. So naturally they will be high P/E and every dip must be used to buy.

When the nature of the company fundamentally changes owing to capital allocation risks (ITC), growth story becoming a dud (Repco), initial assumptions no longer holding good (HCL Tech, Eclerx) and much more attractive opportunities available (ITC, Marico), do exits happen.

Lowest NNPA in 20 quarters, they have been continuously reducing their NPA’s. Much better than their peers ICICI and Axis which are trading at higher valuations

They are improving their market share gradually, strong growth in retail deposits

Good growth in gold loans and with RBI increasing limit to 90% is a positive for the bank

Improved provision coverage ratio at 58%

Attractive Valuations

Tata Chemicals-

The company under new management is trying to turn around its operations and is focusing on high growth areas. They have started production of rubber/ non-rubber grade silica, and have ventured into Lithium ion battery recycling and will setup battery manufacturing soon, they have also expanded their Nutra-Chemicals offerings. Thus they are reducing their dependence on soda and Bi-carbonate products and venturing into high growth verticals.

With a debt free status and its subsidiary Rallis already performing well the company should do well over the next 10 years.

Disclosure- holding Federal bank and Tata Chem is on my watchlist

Hi all - need help around how to calculate how much of the FCF is ploughed back into the business - something that should be considered a differentiator for CC investing with experts opining Colgate, HUL, etc. don’t fit the bill.

Thanks so much,

Mohit

According to Dave, an old Texan piece of stock market wisdom goes as follows: “Eat ’em, drink ’em, smoke ’em, go to the doctor, and look good when you get there.”

As simple as the advice may sound, it artfully focuses the investor’s attention on companies that tend to be non-cyclical in nature, as they provide products or services that consumers desire in times good and bad.

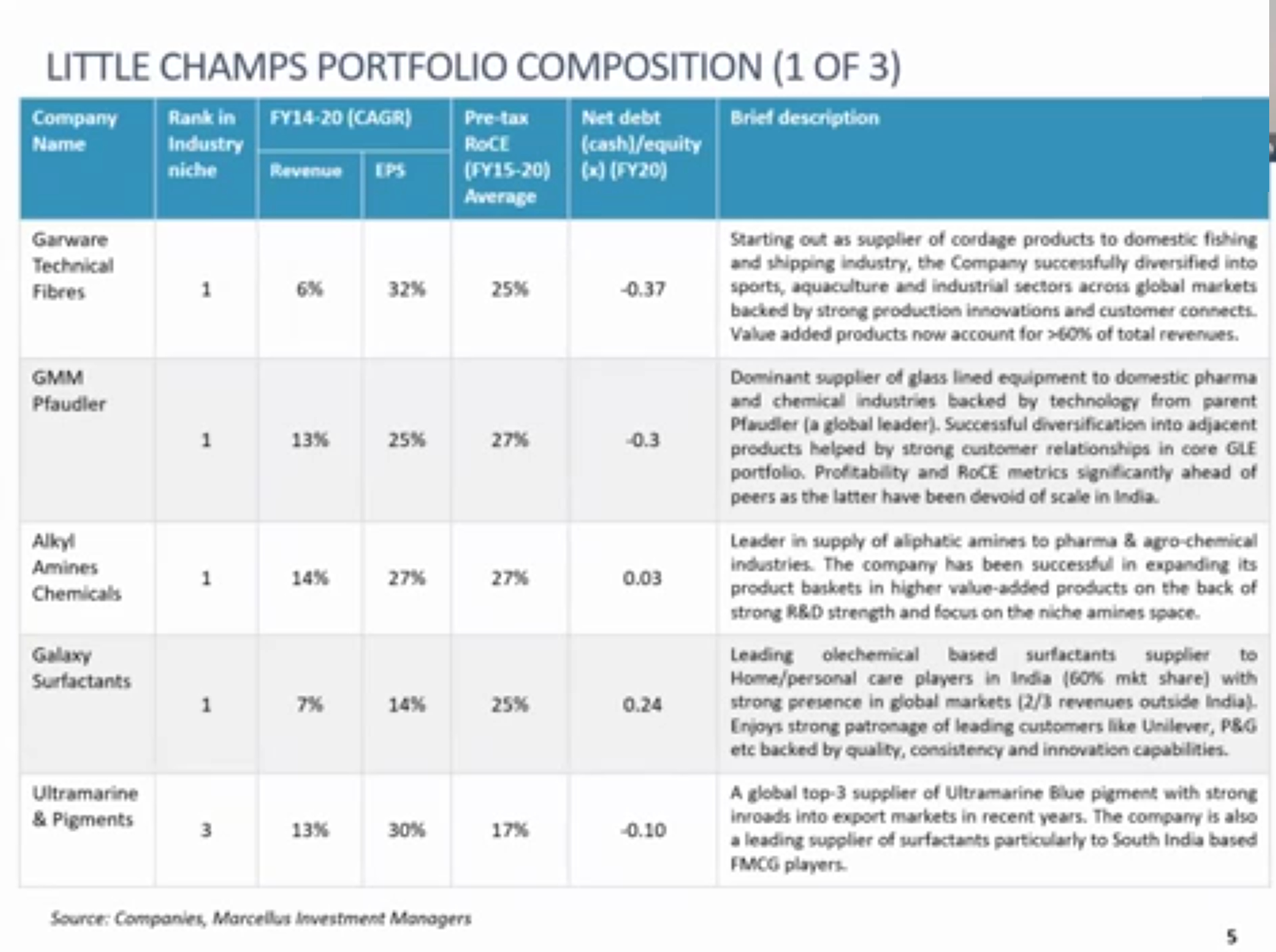

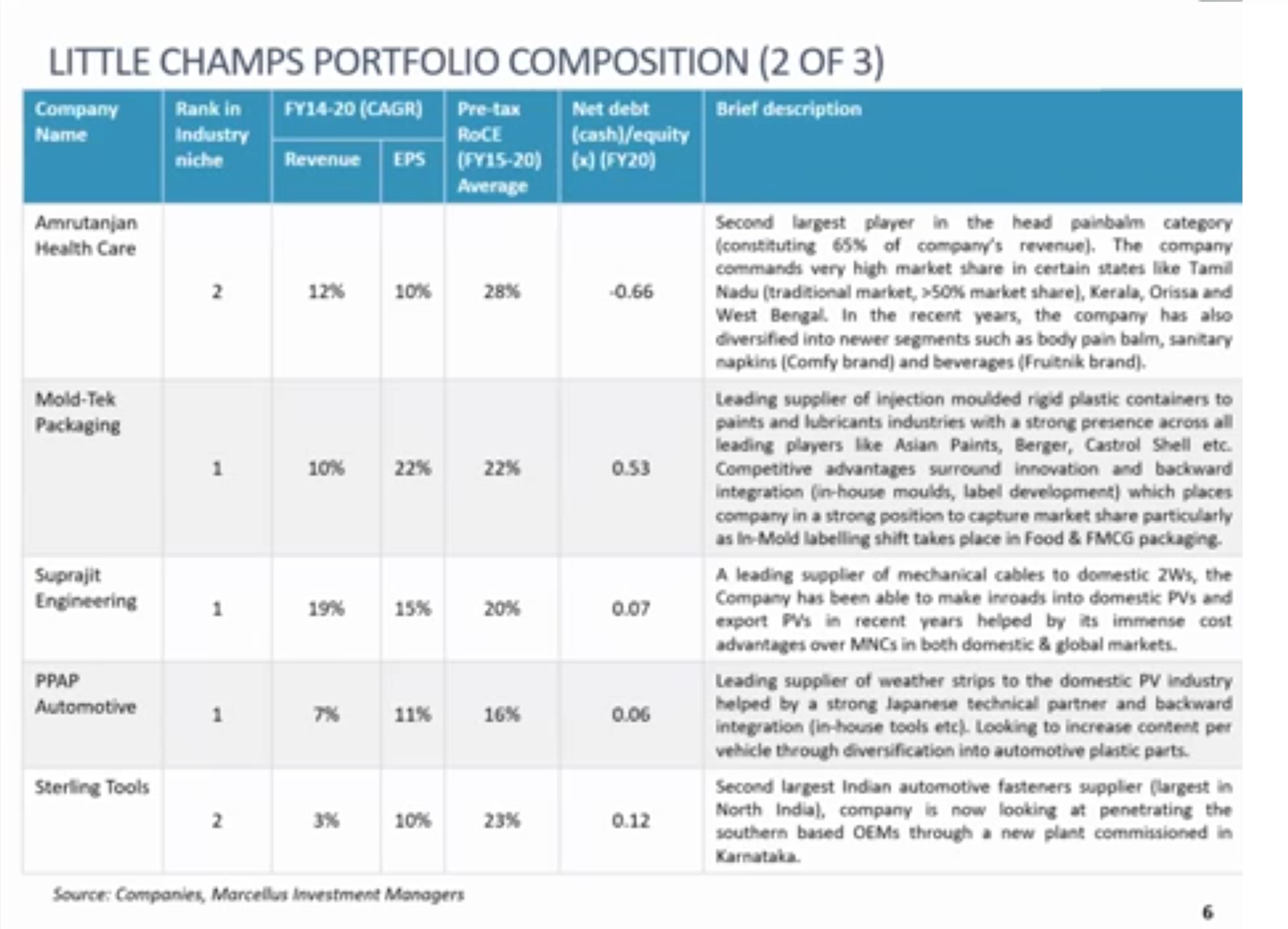

Before I share the details, it would’ve been great if you did some homework on the company and Marcellus Little Champs portfolio as you’d have got all the answers yourself.

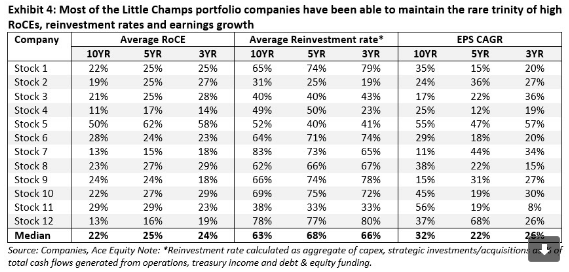

Do these numbers from Alkyl Amines look Coffee Can enough?

Compounded Sales Growth - 10 Years: 16.56%

Compounded Profit Growth - 10 Years: 34.09%

Avg Return on Capital Employed - 10 Years: 25.1%

Avg Return on Equity - 10 Years: 28.92%

I don’t know the exact date they bought Alkyl Amines but they were definitely holding it well before March 2020. They published this newsletter on 8th March 2020 where they discussed the portfolio holdings without revealing the names. I ran these numbers through screener and was able to decode stock 1 as Alkyl Amines which in hindsight proved to be right and also something I benefitted from as I bought the stock during March lows around 1150 - thanks to Marcellus team, screener and the pandemic!

I have been a beneficiary of just keeping up to speed with their different portfolios and it’s up to each one of us to either take advantage or keep questioning them / their motives endlessly.

I do agree on one point with you that he seems to be talking about Divis, GMM Pfaudler, Alkyl Amines a lot recently - maybe because they’ve been flying and Marcellus owns most of them. However, let’s not blindly question every single thing they’ve done without making any effort ourself to find the answers.

I may be wrong, but usually when someone makes too much publicity of the stocks in portfolio to facilitate the exit. They must be owning large number of shares and would need buying interest to absorb the supply and hence extra publicity.

Just a thought came across my mind. This post can be deleted if felt inappropriate to the forum/this topic.

We can only know whether Marcellus are selling if anyone is invested with them in little champs.

Disc. Not invested in any of the 3 stocks mentioned above

Was listening to a very recent talk by Marcellus with regards to portfolio balancing…

It was interesting!

When the portfolio value of a stock goes up due to phenomenal increase in stock price ( P/e increase) , they would like to prune the quantity of that stock and move the money to other undervalued stocks in the portfolio or some other new discovery stocks where they find value and growth …

Anyway, the basic objective of the fund manager is to multiply wealth .

But while selling or pruning a stock from the portfolio , there need to be plenty of buyers in that stock so that the stock price does not fall too much…

Can we please stop dedicating this thread to analyze the merits/demerits of Marcellus Portfolio!!

Else, lets just rename this thread to “Marcellus Coffee can Portfolio” and start a new thread to discuss the concept!

The problem is that this thread contains an equal number of useful non-Marcellus discussions also.

As has been told before, Coffee Can is a thematic concept and Marcellus (previously Ambit) are just some of the well known Indian propounders. There are such propounders in the Global scene also. The screens and qualitative aspects vary somewhat though.

Regarding the ‘open’ nature of the portfolio one should know that in the age of Internet things hardly stay hidden. One can easily know the top holdings of Malabar, Amansa, Nalanda, Valuequest in so many sites (e.g. Trendlyne). Marcellus PMS has smaller AUM and doesn’t own more than 1% of any public companies and so their portfolio isn’t available in those sites. Also they mostly seem to be an advisor. Likewise some smaller PMS / Advisors also share names of their portfolio in cryptic language which doesn’t make it difficult to decipher the holdings.

Lastly many such advisories have 15 days no-question-asked refund policy which makes it easy to clone their portfolio.

But does cloning help?

Well-known microcap investment manager Ian Cassel recently told “You can borrow someone else’s stock ideas but you can’t borrow their conviction. True conviction can only be obtained by trusting your own research over that of others. Do the work so you know when to sell. Do the work so you can hold. Do the work so you can stand alone.”

Request you to read the following article from Value Research Advisory which has similar refund policy.

So now a days, I have stopped believing in my “good luck”

So now a days, I have stopped believing in my “good luck”

")