Bank statments and cash deposit are already introduced . All i am saying is presently we are imagnjng Atms as only cash machines but with digitisation i doubt it will only b restricted to cash only. But as said its only thesis who knows what future unfolds DYOR!

Services to phones will also b charged but yes as u said they are easier than going personally to bank or ATMs. But my thesis revolve around semi urban and rural areas there is still scope there , lets c how it goes !.

1 Like

Can someone help me understand if CMS only offers cash management services or they fully maintain the ATMs on behalf of banks? Ie. who is responsible for electricity, cleanliness, security, cash availability etc.?

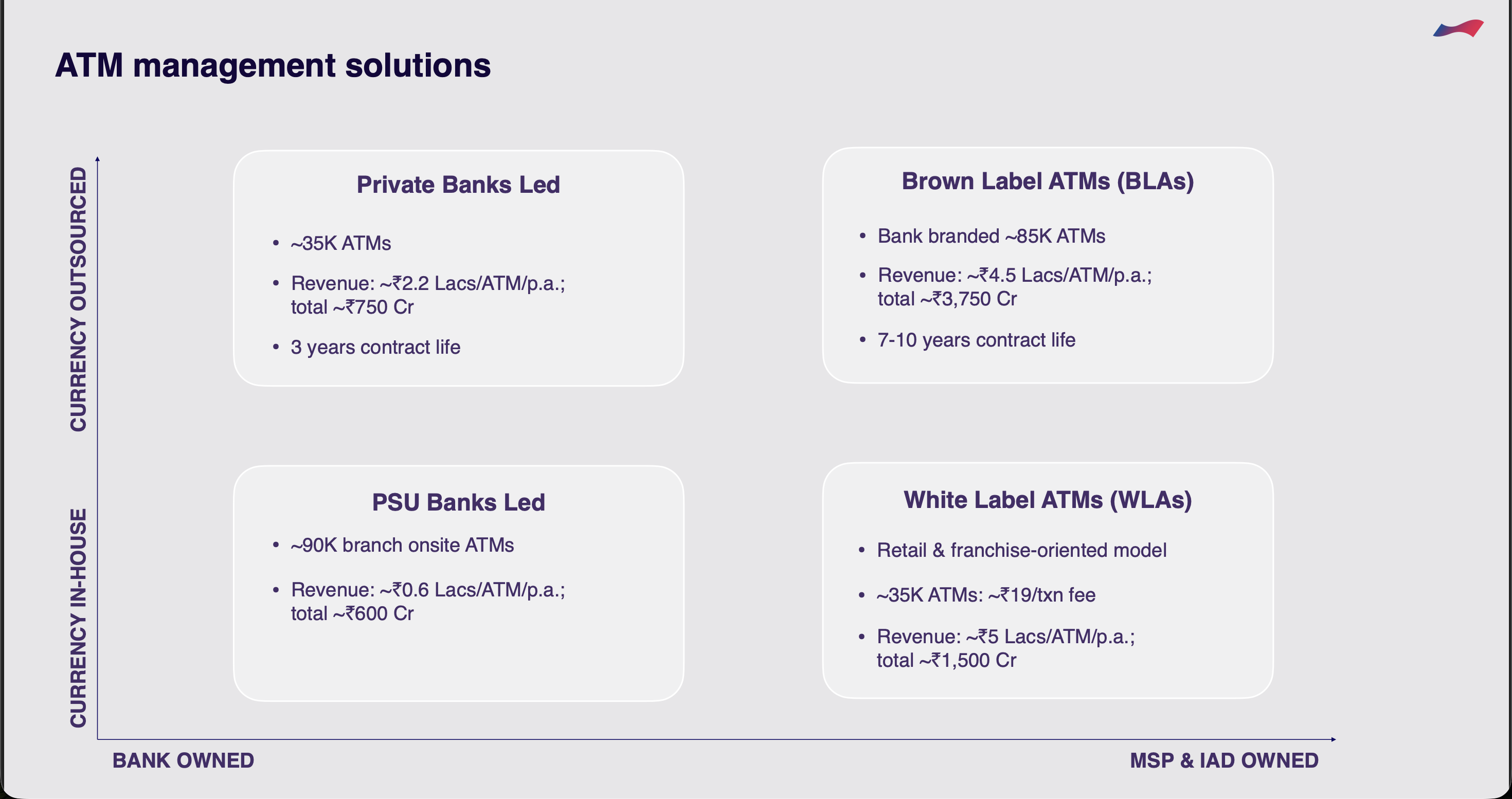

In ATM Management, there would generally be either insourcing i.e. everything done by Banks. Whereas when it is outsourced, this is generally called as Brown Label ATM’s. So service providers like CMS would be responsible for site Identification, installing the ATM machines, Man-guarding or AI - remote monitoring, Rent, cash replenishment, ATM software etc. And revenue for companies like CMS would either be a Transaction linked model or a Fixed- Fee model(Major for CMS).

Other players like AGS got burst as they had more of transaction linked model in ATM management. Plus there was also lot of debt, which led to Liquidity crunch as economy slowed and ATM transactions dipped.

Generally, your CAPEX would be upfront but revenue would be deferred.

3 Likes

Cash business cannot be discarded completely. One BIG UPI fraud and cash will be king again or if charges on UPI starts then again cash will benefit. anyways there have been too much cyber fraud now a days so old people are again thinking about UPI and holding cash. although growth is difficult to predict in cash management business but downside can be estimated.

2 Likes

Coz of Gst 2.0

Many small businesses are now preferring online transactions as gst is low,

They dont need to maintain another book of account (that happens in cash)

As of now, we may see further decrease in usage of cash.

One needs to follow the market

Market is discounting cash, so cms also getting lower valuation

Contra bet is good, but who knows when it will work in favour.

2 Likes

absolutely correct but if company diversifies from cash management then they can pivot from this difficult phase.

1 Like

cash management only , for electricity, cleanliness, security bank deploy or outsource through other tenders.

market is discounting cash but it forgets CMS is the only monopolistic player in this sector and future of Co will not be restricted to cash only it has already started exploring diversification by acquiring security system related Co. Also top management of the Co has performed excellent and i have same expectations in the future. With a PE of 16 and ROCE of more than 20% it is a great contra bet. As they say be greedy when others are fearful!

Disc: invested DYOR!.

2 Likes

One key negative indicator in these kind of service is cash lost in transit due to theft. In FY 24 n 25 i think Co got dent of approx 150 to 200 cr in it. Out of which 30% insured 10-15% recovered other is still under process for recovery or write off.

Now even after the dent at present Co is able to maintain margin of above 20%.

This area is critical perhaps with increase security of incidents can be reduced that will be a big boost else one should provisin the same out of profit to arrive at futre forecasts.

Cash industry is consolidating - this is the best time to buy the leader. A while back a listed firm AGS transact tech, went bust. And CMS is also diversifying.

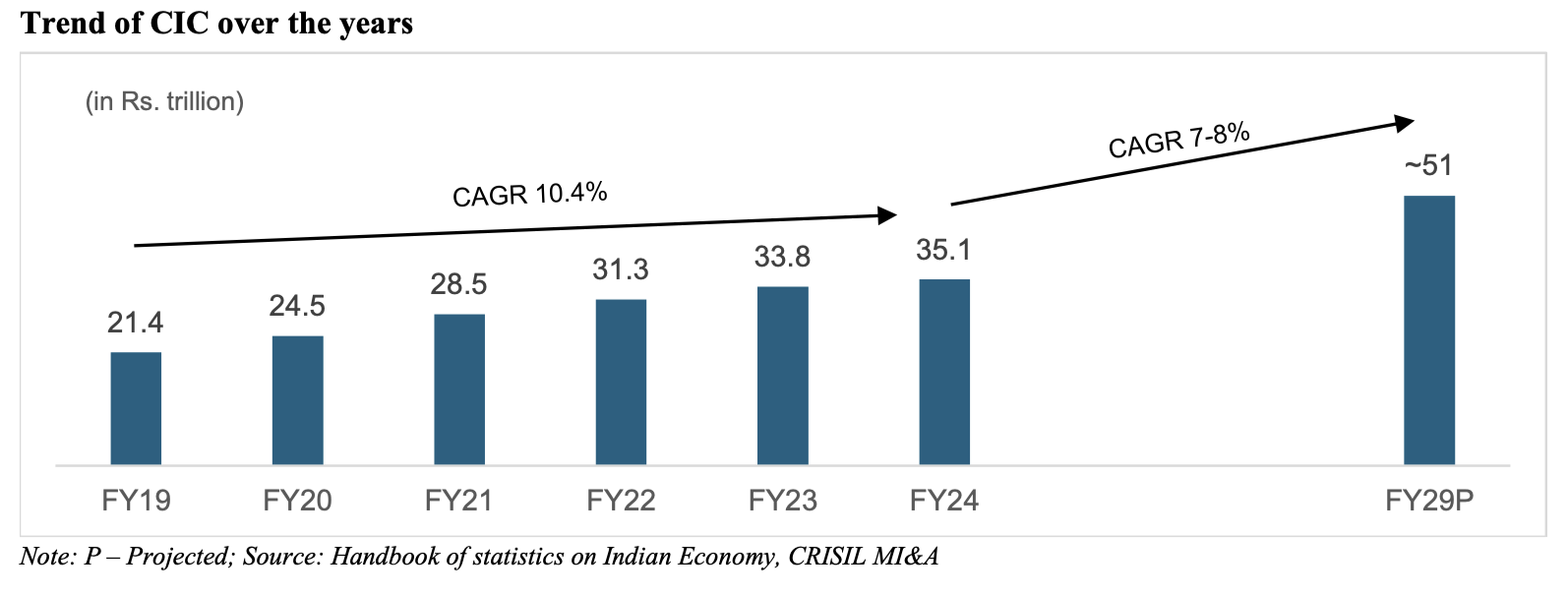

Plus even if Currency in Circulation has fallen after UPI advent - it will have single digit CAGR.

and knowing most Indian businesses black money is still very very prevalent!

3 Likes

https://www.bseindia.com/xml-data/corpfiling/AttachLive/837dfdaa-a9f0-4767-95cb-3203c876afc5.pdf

Company has tried to address the concerns of the investor community in the above presentation, but the growth projection is still low at 12%. I don’t think the market will appreciate the low growth expectation.

2 Likes

But 12% revenue CAGR may not be too bad - Last 5 years (12%), last 3 years (15%); so its coming back to its long term average.

Market is probably too focused only on the ATM cash management part of the business which seems to have low future growth, however the CMS has meaning full 40% coming from other businesses like retail cash management, etc, which has much higher runway ahead. from 2L org cash points currently to 6L; and CMS has just dethroned the market leader in this space with 38% market share.. SIS is likely to be no 2.

1 Like

The way the company put a comparison of CAMS-Delivery-Bluedart etc makes me uncomfortable & feel like they want to protect their Stock price / Marketcap. Additionally, because they are unable to do it via performance…the focus is on saying LOOK! ATLEAST WE’RE CHEAPER THAN THESE OVERVALUED GUYS

2 Likes

Given that it was an analyst meet (as opposed to investor meet), I guess management was positioning CMS with the analysts. I was also surprised to see that, but I noticed it was one of the last slides.

Market has it’s own mind, but there is some perspective to be gained from that slide. TCI express for example, having no moat, in an industry with limited entry barriers carries a much higher valuation. Having said that, I think analysts assign zero terminal value to cash management/logistics business and hence lower valuation. Facts on the ground indicate a low but steady growth in cash usage.

What I like about CMS - it is in an industry where supply will be limited, management is focused on right business metrics, so far they have managed with little debt, good ROE. They have tried to create new optionalities recognizing the slower growth of cash going forward.

We have to take any growth projections with a pinch of salt. A few quarters back, 18-20% looked normal. Now even double digit seems challenging. Rajiv Kaul said in the previous concall that he would totally avoid giving guidance, if not for the questions from analysts. Reality is - no management can predict growth even reasonably accurately. We have to look at the company’s past, look at the current external situation and take a call whether the business will do well in medium to long term (if that is one’s time horizon).

disc - invested.

6 Likes

Everything that you mentioned, along with the fact that it’s really cheap at the moment, generates FCF consistently, - has high ROCE avenues to deploy that cash, and is a 100% domestic facing company (avoiding all the tariff turbulence). They also hold 15% of their market cap as cash at the moment.

Although the industry is pretty much considered to be a sunset industry - currently there are only four major plays (After AGS went bust) - CMS, Hitachi, Radiant, and SIS Prosegur.

Radiant has been struggling to uphold its margins over the last few years, - leading to further consolidation. There is a moat and CMS is displaying characteristics of a moated firm.

Disc: tracking position

6 Likes

You need to see the growth projections relative to valuations. The stock is trading very cheap compared to its historical averages since listing. So low growth expectation is already in price. And based on stock movement, i assume that the market is already factoring in low growth in FY26 followed by pick up in FY27. Dividend yield is also rising every year. If you are looking for a stable business with a proven management track record then CMS fits the bill at current valuations.

After seeing above posts its evident retailers do like this stock and accumulating , however looking at price moments it seems retailers shareholding is increasing and some DII FII is offloading which is a concern. until unless big player or institution comes into play stock price may revolve around this zone and test patience.

1 Like

You know the peer comparison slide also had caught me off guard. Especially their CAGR prediction for the next 5 years. But it is just 12% cagr growth, nothing absurd or beyond nominal GDP growth if you think about it. The projection also shows they’ll have 53% revenue share from non-atm business which is fair. So it isn’t an overly optimistic projection, but rather just in line.

Here is the video from analyst day: https://www.youtube.com/watch?v=KW_M4L6-3Oc

I wanted to hear how he spoke bout the peer comparison slide, and pls listen. 1:28:45

The reason for putting up the slide is to change the perspective. Analysts compare CMS to cash management firms globally which he believes is incorrect - because the company is actually a growth firm with value prices in India. So the comparison would be better with other logistics/tech outsource firms rather than global peers.

That’s the whole point. He doesn’t get into the stock market specifics and sticks to only the business model.

7 Likes