Growth in profits do not look qualitative as its working capital keeps on increasing more than its turnover so company is generating negative operating cash flow. can any one throw light on it and if anyone attending AGM please show this concern to management and post the reply.

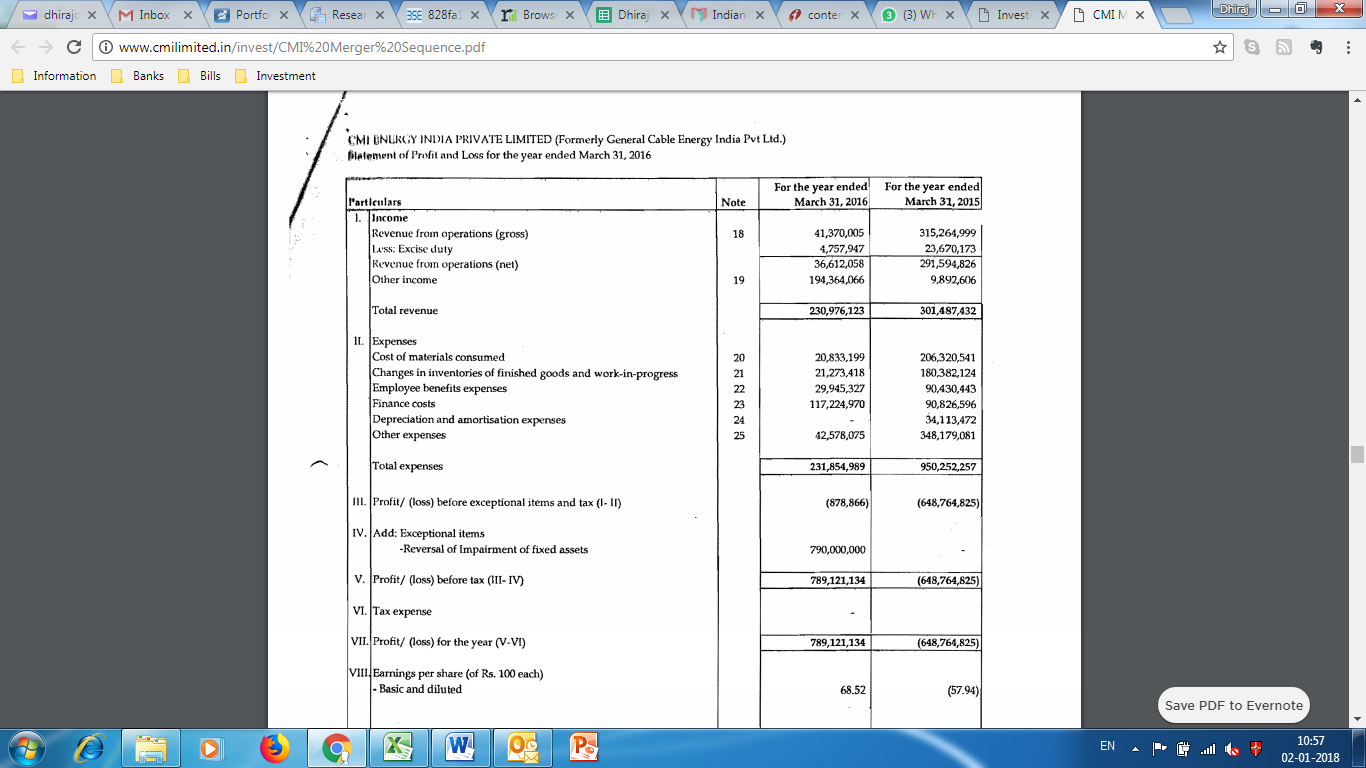

I was trying to check the balance sheet of the company to know how much profit can come due to this amalgamation.

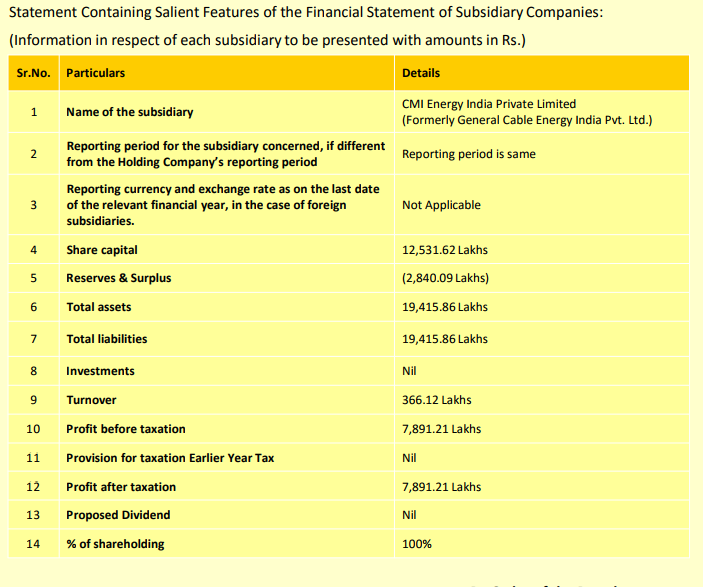

This CMI Energy India is same as General Cable Energy, CMI Ltd has acquired it. It is a subsidiary now.

So, here Profit after taxation is Rs 78 Cr. Am I right?

Please correct me, if I am wrong. After amalgamation, this much profit will come into CMI Energy!

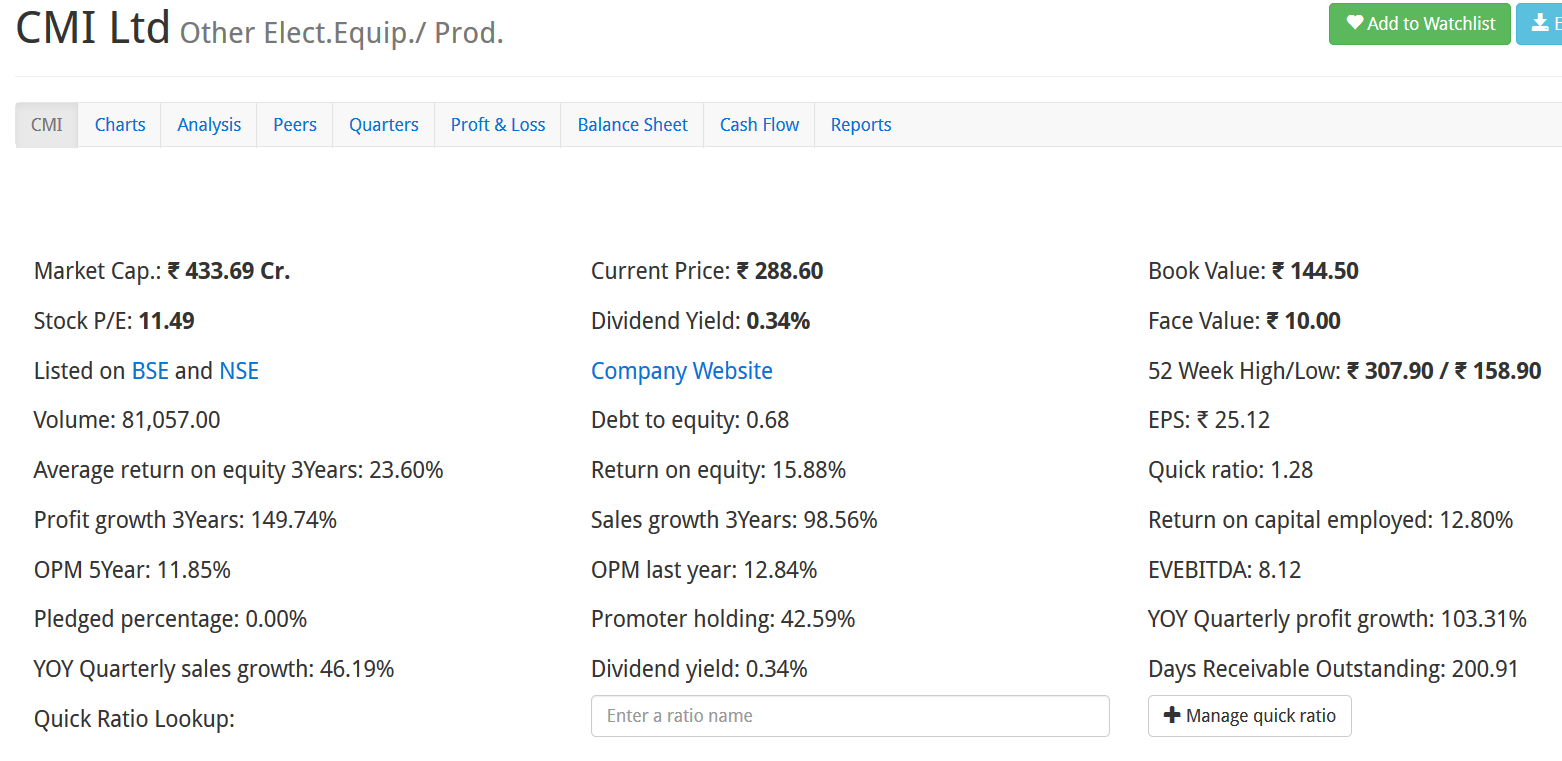

Where to check financials of Pvt Ltd? Is there any website for free. I got two websites during search but both were for a fee.

Few times I need to know financials of Pvt ltd but nowhere to find info.

It can happen that CMI Energy has other income from sources. Rental etc.

But reserve and surplus in negative!

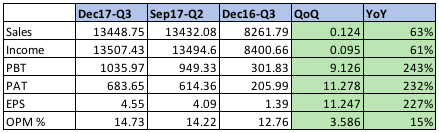

Today CMI has released its AR2017 and after going into the balance sheet I found a huge increase in Trade receivables. Their sales increased 55% YOY but trade receivables increased 179% can anybody explain why is that, M really concerned now, trade receivables/sales ratio stands at 33%+

Is company giving lots of loose credit? Any insights from anyone will be much appreciated.

The increase is WC is likely due to the high rise in Receivables. The receivable days currently stands at 201 days. We need to find out why this is happening.

Screener.in gives wrong values sometimes times, I think this is the case.

Days receivables can be calculated as under-

(Accounts Receivable / Year Revenue) x Number of Days In Year ie.360(considering 90days a quarter) .

From the image I posted earlier from the company AR , their receivables days is 141Cr and Revenue for the year(FY2017) on consolidate basis is 420Cr .

So doing the math according to above formula we get 120.8Days and not 200days as said by screener.in (Sorry for my previous post that I told It was 83days)

If there is something wrong in my calc do let me know.

There has been a good amount of sales in their march qtr Fy-17 and due to account closure at the end of year they could not liquidate their debtors due to which their receivables increased and hence their working capital increased. This is the reason why cashflow is negative

From the Union budget, there’s a big push on the Railway infra. Indian Railways being the major customer for CMI, hope it will continue to have strong order book and nos.

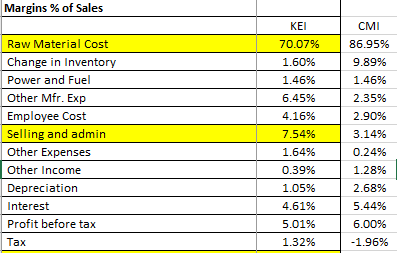

Does anyone have a comment on the difference between CMI and competition KEI industries? While KEI has other business segments, its cables business is about 75-80% of overall revenues. Raw material cost is clearly much higher for CMI than for KEI.

Yet CMI manages to have double the NPM of KEI. I would be interested to hear if anyone has a perspective on the difference in margins between the two companies. Needless to say, its important to understand such a significant difference in the two companies biggest raw material cost viz copper - whether the sourcing is different, or whether the product mix of the two companies is different needing different grades of copper.

Company deals with distribution companies and railways, both of which are bad at paying in time. They had significant orders from UP and TN, both are really bad in paying. Thats why the rise in receivables, however, this should stabilize going forward as the company diversifies its client base

In FY16 annual report on page no. 115 in Auditor’s report under “other matter” it says revenue earned by Baddi plant is Rs 90 cr. but that revenue was earned in FY17. How is it possible that this figure appeared in Annual report before it was even realised. Is it Coincidence?

Also do anyone has any idea why PAT and other margins are huge in Q4 as compared to last 9M of a FY. Like for 9MFY17 PBT margin is 4.11% but for Q4FY17 PBT margin is 9.26%.