CMI Ltd is engaged in manufacturing of various types of specialized cables catering to various sectors.

FY 15 Sectoral Rev split – Railways (56%), Power (17%), Petro-chem (13%), Rest (14%).

79% of its revenue comes from PSU & rest through private sector.

Major customers include – Indian Railways, GAIL, Indian Oil, Alstom, TATA, Siemens, ISRO, SAIL, Global Toyo, The Linde Group, NTPC, Bharat Electronics, HP, EIL, etc.

23 of their clients have empanelled them as their preferred vendor

Current manufacturing facility is located in Faridabad, Haryana. Operating at 65% utilization, the plant reported 9 month revenues ending Dec 2015 of Rs 170 Crs.

During FY 2015, the production capacity increased by almost 25% over last year due to commissioning of one additional cable laying machine, improving capacity of other important machines & by better production planning & control system.

In Sep 2015, CMI acquired Haryana facility of Danish company FL Smidth for Rs 20 Crs. Link

In March 2016, CMI completed acquisition of another manufacturing facility at baddi from General Cables, USA for Rs 150 Crs. Link

-

Baddi acquisition positions CMI as a leading manufacturer in India for specialized cables. Also, CMI has inherited international processes & systems for manufacturing specialized cables.

-

Baddi plant has the potential to generate almost four times the revenue generation capacity of Faridabad plant

-

The acquisition strengthens their current product portfolio with addition of new products & new clients. Also, the potential for cross-selling to their existing clients.

Promoters are increasing stake in the company by way of warrants / pref allotments.

GMO acquired almost 10% stake in the company in Jan - Mar 2016 qtr.

Q3 FY 16 Investor presentation

Financials –

https://www.screener.in/company/517330/

At Current Mkt Cap of Rs 250 Crs, CMI trades at an LTM PE of ~13x.

Risks / Concerns –

-

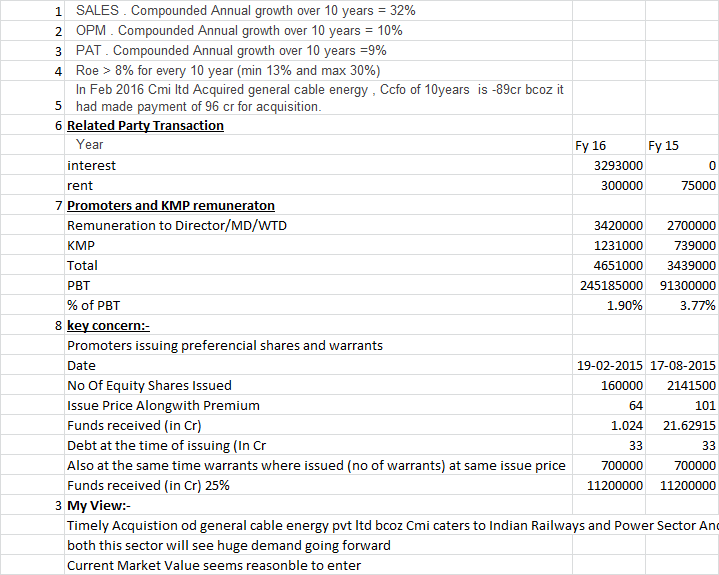

Recently completed acquisition would result in leveraging of capital structure. Though June 2016 consol B/S is not available but finance costs have gone up by 140% in June 2016 qtr yoy.

-

For a company of its size (FY 16 turnover @ 240 Crs.), Rs 150 Crs acquisition is pretty large & a slight slowdown in revenues – could deteriorate the outlook considerably.

-

The company is reporting high growth rates in revenues for the past 3-4 yrs but it does not disclose its order book position. Hence, difficult to get a sense of revenue growth going forward. However, Mgt. has given a guidance of 100% rev growth for FY 17 Link

Disclosure: Holding tracking qty