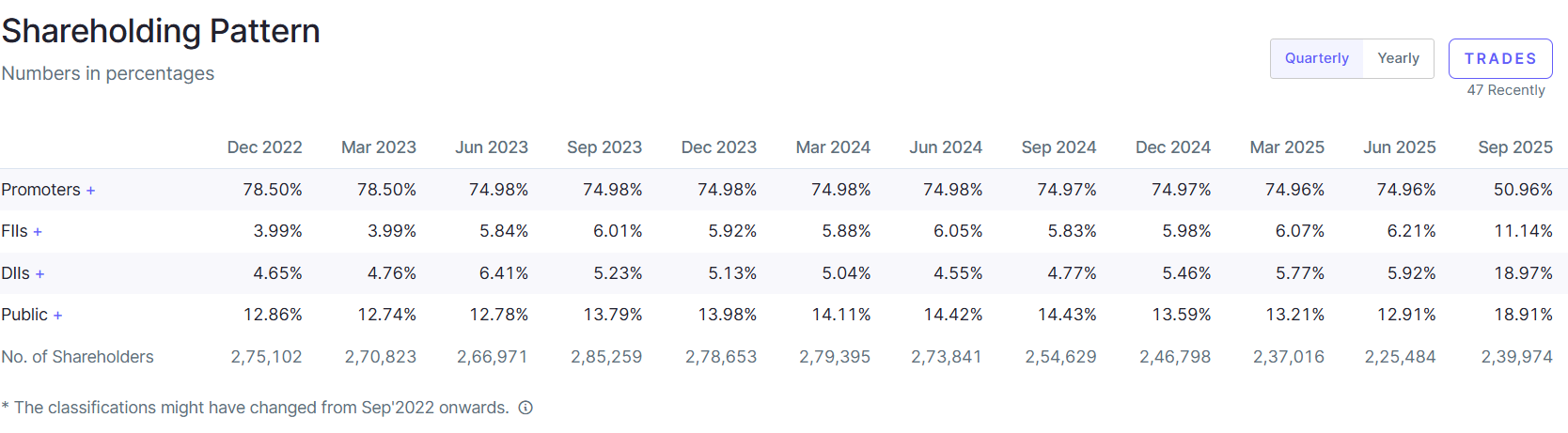

Company yesterday filled this information on exchange that they (Boob family) are going to sell stake for estate planning. Even during yesterday’s concall, same thing was discussed.

1 Like

I have been watching this stock since 2 years from sideline and been on and off here. recently 4 months back decided to exit based on performance against valuation. in all the time I was firm on conviction of promoters. now 24% stake sale from Boob family came as big shock to me. If its estate planning, it does not need to be as big as 24%. this is coming down from 74 to 51. I did not like it. On top of valuation concern and business growth, now we have promoter holding concern also. watching from sideline but damn I was going to load after Q1 result below 1300 but not sure now

1 Like

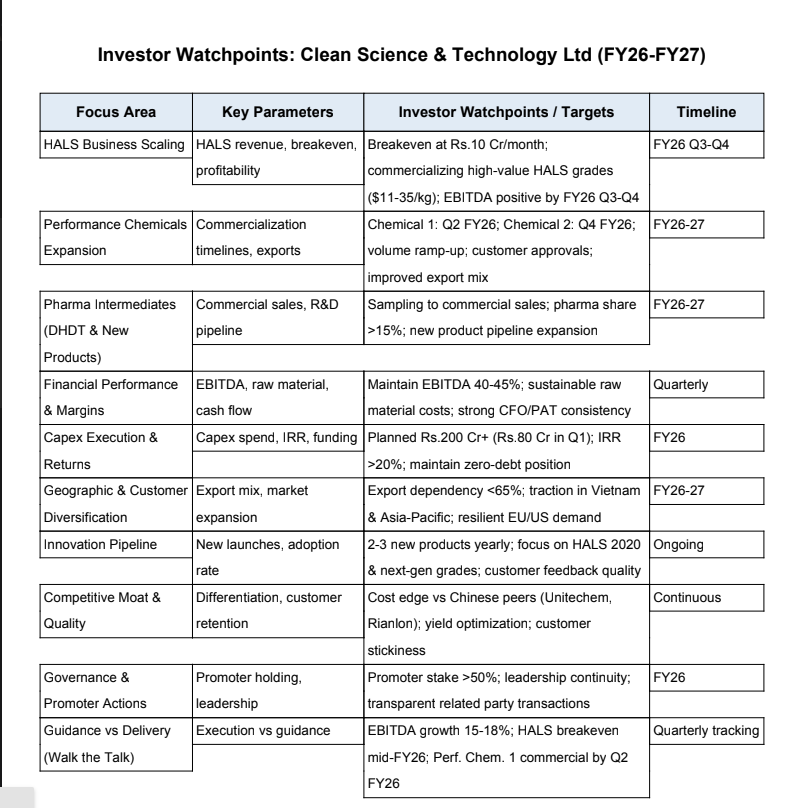

You may use the followiing Tracking template for quarterly performance and guidance monitoring:

| Metric / Factor | Management Guidance / Target | Timeline | Q3 FY25 Value / Status | Q1 FY26 Value / Status | Remarks |

|---|---|---|---|---|---|

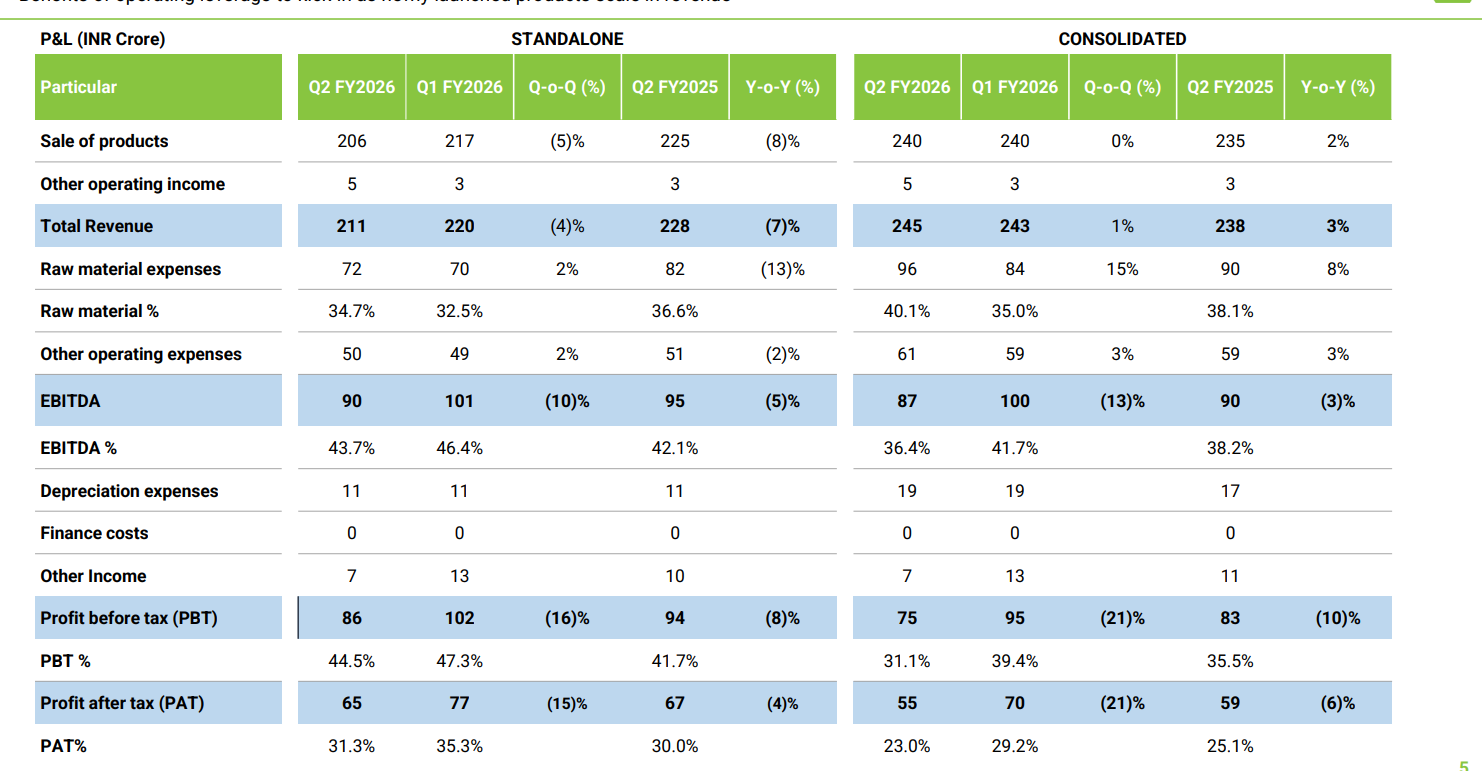

| Revenue Growth | Achieve double-digit revenue growth through volume scale-up and new product commercialization (e.g., HALS, pharma intermediates, new performance chemical product). | Target: FY26 | Standalone revenue: ₹231.6 Cr; Consolidated: ₹240.8 Cr (YoY growth 19% & 23%) | Standalone revenue: INR 220 Cr (YoY growth 1%); Consolidated: INR 243 Cr (YoY growth 8%) | Below guidance. due to a challenging operating environment with high volatility from global macroeconomics and geopolitical tensions, leading to a slowdown in demand. |

| EBITDA Margin | Maintain robust EBITDA margins driven by favorable product mix and operational efficiencies. | Target: 40–45% maintained through FY26 | Standalone EBITDA margin: 44.8%; Consolidated: 41.5% | Standalone EBITDA margin: 45.9%; Consolidated: 41.2% | On track. Standalone margin slightly above the target range at 45.9%, while consolidated margin is within the range at 41.2%. |

| PAT Margin | Sustain overall profitability; guidance expects margins to remain in the 25–30% range. | Target: FY26 | Standalone PAT margin: 32.5%; Consolidated: 27.6% | Standalone PAT margin: 35.0%; Consolidated: 28.8% | On track. Standalone PAT margin exceeds the target at 35.0%, while consolidated is within the range at 28.8%. |

| HALS Volume & Utilization | Scale up HALS production: Increase monthly volume from current ~190–200 tons to achieve a cumulative annual target of 3000–4000 tons; improve facility utilization from 30–40% to 50%+. | Short-term: Increase utilization in next 2 quarters; Full ramp-up by FY26 | Current HALS volume: ~190–200 tons/month; Utilization ~30–40% | Current HALS utilization: ~22% (Volume: N/A) | Significant deviation. Utilization dropped to 25% from 30-40% in Q3 FY25 due to lower-than-expected demand for HALS products. Q1: sales :~580 tons i,e, 24 crore (quarterly), ~193 tons/month; Utilization 22% Management expects ramp-up through next 2 quartersManagement aims to reverse this trend with new product launches. |

| New Performance Chemical Product | Deploy a new performance chemical project with an allocated CAPEX of ₹150 crores, expected to deliver full–capacity revenue around ₹300 crores; to broaden the antioxidants/stabilizers portfolio. | Commercialization by H2 FY26; peak revenue potential in about 2 years | Project in early planning/construction stage (no production in Q3) | Construction on track; water trials in next 4 weeks; commercial production in September (Q2 FY26) | On track. Construction is progressing as planned, with commercial production expected in Q2 FY26. |

| DHDT (Pharma Intermediate) | Ramp up domestic production of DHDT (used in manufacture of Lamivudine) to capture import substitution; expected revenue potential of ₹80–₹90 crores at 70–80% capacity utilization. | Approvals expected in next 6 months, followed by trials; early FY26 | Currently in evaluation stage (samples sent); Q3 contribution: Nil | Plant commercialized; samples sent for validation; no revenue yet | On track. Plant is commercialized, and samples are under validation, aligning with the expected timeline for revenue generation in early FY26. |

| BHT (Antioxidant, Co-product with BHA) | Scale production to achieve an annual output of 2000–3000 tons, generating revenue of approximately ₹60–₹80 crores; later potential for further capacity expansion with a dedicated block. | Initial production this year; ramp-up next year; further scale-up considered later | Product recently launched using HALS facility; early production volumes | N/A | No update. No specific information provided for Q1 FY26; status remains unchanged. |

| Barbituric Acid | repurpose the existing facility of PBQ to convert it into barbituric acid, andestimated to commercialize by August end. |

By aug end | N/A | N/A | Commercialiation by Aug 26 |

| Overall CAPEX & Growth Investments | Incur substantial CAPEX to support growth: Rs. 160 crores spent (9M FY25) mainly on subsidiary expansion (CFCL) plus additional planned investments. | Ongoing in FY25; new projects to be commissioned by H1–H2 FY26 | 9M FY25 Capex recorded: ~Rs. 160 crores | Invested INR 80 crores in Q1 FY26 in subsidiary | On track. CAPEX investments are ongoing, with INR 80 crores invested in Q1 FY26, supporting growth initiatives. |

| Global Market Expansion & Distribution | Expand global distribution network to better serve small-volume international customers; aim to complete about 70% of network development. | Further ramp up over the next few quarters | Approx. 70% of distribution network in place (contracts signed) | Expanding into new markets (e.g., Vietnam); 61% of HALS sales from exports in Q1 FY26 | Progressing. Expansion efforts continue with new market entries (e.g., Vietnam), though the specific network completion percentage is not provided. Export sales indicate ongoing progress. |

8 Likes

Do we know when promoters plans to sell? anything shared?

1 Like

1 Like

Can anyone please enlighten me on why the promoters sold their stake?

Promoters are deliberately trimming a minority stake to free up capital for family estate planning, NOT because of business trouble. They retain control, and the fundamentals remain solid. The drop in stock price is more about emotion than structural weakness.

1 Like

they sold 24% stake which brings holding to 50-51%. so one need 2600 cr for estate planning? all of a sudden reducing stake this much is not good event. we need to find out who brought the block deal and than decide.

2 Likes

My take:

-

Boob family Ashok boob already 70+ age & Krishna Boob might be in 50+ might not be much interested in business now. Even in every concall, only Siddharth Sikchi is present. But Siddharth & his family holds only 19.79% stake.

-

This FY results will be almost flat or minor 5-10% uptick. Real growth should start in FY 27 where pharma intermediate & PC 1 should start contributing. H2 of FY 27 & FY 28 would see great growth, if things pan out as per plan.

-

But then why promoters are in a hurry to sell that too 24% stake without much gain (Ipo price was around 900 in 2021). So it is not like other promoters where they are milking the bull run & infated price of stock.

-

Lots of ifs & buts & that is reflected in price & PE also. If they execute well, there is possibility that they would have CAGR of 20% from FY25 to FY28/29. I am averaging my position.

For me, biggest threat is Vinati Organics. If they start competing with clean science in flagship products it would be disaster for Clean science as there will be no pricing power with them & margin can suppressed heavily.

8 Likes

Seems that there are couple of strong headwinds to Clean Science business in near term (leaving aside large block sale by promoter group).

-

Reasonable to believe that Vinati Organics was one of the biggest customer that Clean Science had for flag bearer products (MEHQ(Monomethyl Ether of Hydroquinone) and Guaiacol. Vinati itself has completed the backward integration by producing these products in-house. This is a fairly large capacity (2000 MT for MEQH and 1000 MT for Guaiacol) - for context, CSTL’s combined capacity is expected to be ~5000 MT for this family of products.

CSTL’s edge has been the novel green route (Anisole as feed) of production as compared to traditional hydroquinone route used by Camline fine etc. Vinati/Veeral’s new capacity is also based on the same green chemistry (Anisole based). Further, Vinati has indicated that part of the capacity will be feedstock for existing products like BHA etc. and rest will utilized as merchant sale in the market.

Overall, MEHQ market is not too huge (believed to be ~12,500 MT/year). Clean science will loose its biggest customer revenue for MEQH/Guaiacol from Vinati. Additionally, will compete with Vinati for the merchant sale pie.

-

Another high revenue product for CSTL is BHA (Butylated Hydroxy Anisole) which has a uses of anti oxidant in food industry. Recently FDA has added BHA to the list of products under post market assessment category (potential Carcinogenic effects).

FDA Update on Post-market Assessment of Chemicals in the Food Supply | FDA.This new list in itself is part of the broader overhaul that FDA is undertaking by way of seven parameter prioritization tool:

FDA Proposes New Tool for Post-Market Scientific Assessment of Food Ingredients – Well DoneMost likely, inclusion of BHA to the list is based on National library of medicine report which has listed Butylated Hydroxyanisole under the category of ‘Reasonably anticipated to be a human carcinogen’

Butylated Hydroxyanisole - 15th Report on Carcinogens - NCBI BookshelfFurther, there are multiple other sources to indicate regulatory investigation on adverse effect of BHA.

- State of California: The Proposition 65 List - OEHHA

- International agency for research on cancer: IARC Publications Website - Some Naturally Occurring and Synthetic Food Components, Furocoumarins and Ultraviolet Radiation

-

New capacity of HALS family of product, though will partly offset the revenue loss, if any from MEQH and Guaiacol. However, they are comparatively lower margin products.

Looking few quarters out, at company level margin profile will have dual impact - lower margin HALS will be larger part of the revenue (maintaining 4000 MT projection for FY’26, gradual ramp-up to 10,000 MT) and high margin MEQH going down gradually.

CSTL had the kind of growth and margin profile (40%+ EBIDTA) which will make any investor drool. Just that table has turned (seemingly) and competition/customer wants to keep that important slice of the pie.

Disc: No Investment

Tarun

18 Likes

Today I exited completely from clean science in loss & invested same in other company. Reasons:

-

They export 20% to USA. After terrif this can be impacted.

-

Recent news of cough syrup will impact it’s sale of Guaiacol. Previously when such incident happened, it took dent in guaiacol sales quiet a bit.

-

BHA sales might also get impacted in future due to above mentioned suspected carcinogen list.

-

Vinati’s product portfolio will enter in market sooner, which will impact their margin in core products.

-

New capex of 150 cr. product - They told to start production in next 4 weeks in last concall. Still no update about the product & its commencement.

-

If I would be promoter & If i need money for whatever reason - If I am bullish about my products & pipeline - I would rather prefer to delay estate planning & would take some other route for investment - To wait for next 1 year to get better exit pricing from the stock. Here it doesn’t seems to be the case with Promoter.

-

Stock again approaching & breaking price of block deal price. Which is not good sign.

I have high hope with company & promoter’s capability. But with heavy heart I had to sell it bcoz of too many uncertainties.

8 Likes

Issue is with Glycol not with Guaiacol(Sometime noise will create)

Clean Science Guaiacol is Pharma Grade!

Business Perspective Next 2 Years will be challenging

Limited TAM

HALS Ramp up(margin dilution)

Vinati Scaleup(Competition)

Trump Tariffs(Bonus Pain)

What if’s & but’s

for Vinati not an easy task Even Clean Science Failed in PTZ & PBQ

Vinati Making MEHQ, Guaiacol and etc doesn’t Matter it’s all about Yield

recent promotor dilution is may be red flag(Someone think it might be Smart Exit)

Company is decent till Now

Company did Huge Capex nothing is materialized atleast in EBITDA level

Hoping Sidharth will Handle well

Time will decide & Time will Settle “Everything”

I’m not a Pro just simple & Common retail investor multiple entry & exits in past not booked any loss till now in CSTL Peak Holing 74Qty right now holding 27qty at 1100

1 Like

It happens, part of investing. there were yellow flags all over. they may do well and prove us wrong but you decide based on what data you have. cant predict the future. stock has not given any returns in 3 years now but always maintained 1100-1200 as baseline but now its clearly broken and I see more pain as valuation will come under the scanner. I had very high hopes from promoters as well. Sidhharth is very solid promoter to follow but somehow I felt he was not comfortable rest selling 24% stake… going down to 51 from 75 while you are literally seens as growth company is not good. anyways not sounding negative and dont want anyone to panic sell. Disclaimer - bought and sold multiple times with no margina gain and loss. just could not see story breaking out as I thought. now just watching as invested lot of time in studying it.

4 Likes

I am invested in the company with their walk-the-talk future goals.

If anything is missing in the quarterly results that is non-negotiable, my straight view is to exit from the company.

Disc: I am creating the above image using ChatGPT for better understanding.

Thanks for clarifying about Glycol & guaiacol.

But the fact is guaiacol is used in cough syrup, not the culprit for the recent cases. My logic is, due to this issue, there will be stricter rules for cough syrup for few months. Both - people will be reluctant to take syrup & doctor will be reluctant to prescribe it for some time unless complete necessity.

Similar kind of problem happened in around 2023 (I guess) & u can read concall summary where Siddharth clearly mentioned about low guaiacol uptake for few quarters due to similar incident happened that time. Of course, after 1 year it again came normal, which might be the case this time too.

1 Like

(post deleted by author)

1 Like

Clean science gave again disappointing results.Many anaylst and investors are confused about this company.Some are bullish and other have exited the stock.

But at same time DII and FII have increased their holding in sep quater a big jump.There was block deal.My capital is stuck in this stock since 2 years.Pls help need clarity.

Their, Hindered Amine Light Stablizers is also facing lot of competition, other local.products also facing competition,lot of headwinds going forward. Though the company is good, I doubt it can generate meaningful shareholder returns going forward.

3 Likes

Cant suggest what you need to do but I dont think anything dramatically wrong in company. went through concall and most of the Q are answered clearly. that is why I like Siddharth Sikchi. Q3 is going to be flat and improvements from Q4 onwards. I am still on sidelines and mostly will have 5% allocation at or after Q3 result. this is just very unfortunate investment story!! what a strong company but could not generate returns for investors due to mad bull run in 2022, some unlucky timings and macros that It cant control!!

3 Likes

when Uncertainty around Stocks earning, they get hammered . Siddharth Sikchi mentioned , he will get clarity on next quarter earning. Market can bear Losses and discount, but uncertainty can’t take It’s always overreacts ..