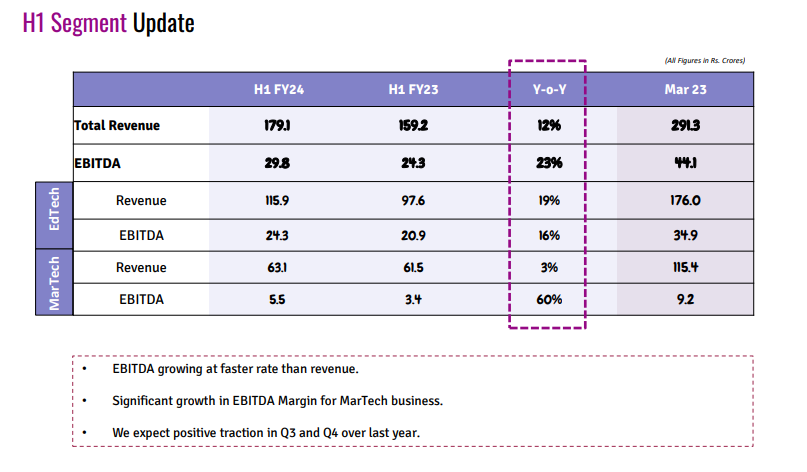

Please go through their latest Earning call . Edtech is generating EBITDA of ~16%.

They are organizing Investor day within next month.

@Saiyam_Jain : Please share pointers to back your statement. I might be missing something.

Please go through their latest Earning call . Edtech is generating EBITDA of ~16%.

They are organizing Investor day within next month.

@Saiyam_Jain : Please share pointers to back your statement. I might be missing something.

Hello anyone following Global Education? The company seems to have very high growth and high margin. I can understand they are different from CL Educate but can’t find a peer company like apple to apple comparison.

Thanks.

There were Chinese companies U.S. listed firms Gaotu Techedu, New Oriental and TAL Education which had Combined market cap of 120 Billion. TAL fr example was doing revenue of USD 5 Billion a year.

You can look at so many startups as an example you would not get any idea from just comparing financials. The competitive examinations business is all about teachers and outcomes (How many students got admitted). Reputation is the key here so you cannot build by purely selling ads. They have to buy these small companies and increase scale yet get good outcomes. That is a tough task.

Unfortunately, management was tied up with so many businesses and still, they should sell the corporate marketing business and focus only on Education but the drive is completely missing as the founders are now old. Immense potential to grow but let’s see. for me it was a style investment i did not need to think about business as such and it is multi-bagger. But now i need to evaluate if they can get growth back.

Disc: Holding stock since 2018 averaged down.

My guess earlier people thought Biyjus of the world would rule this space and now looking at what is happening to these companies gives hope to these companies. There is also a lot of money chasing small companies and a lot of traders in the market who play momentum. A combination of these plus recent actions by management can be the reason. Wait till domestic funds capture the fancy if management gets growth and consistency.

Do you see not relying on star teachers as a moat? I feel this can be a risk… Star teachers are one of the key factors when it comes to a student selecting any institution.

What are the views here?

It difficult to call dependency on one person a moat. If something happens to that person company is dead. Brands should survive with a process that increases the probability of securing a seat in IIMs. I generally buy company cheap so I don’t have to predict moats and how moats will evolve. This is a very difficult industry

True though I won’t speak about just one or two teachers it’s about a group of good teachers who make the institution. Hook for a student would be a star teacher or campus placements etc.

Truly agree when you say you buy cheap there can be errors when you buy something at an earnings multiple of 60 or 70 but when you enter at a lower multiple the room for error is less.

However, it has become tough and challenging nowadays to find stocks at low multiples and decent growth with a sustainable margin.

Yes of course the group of star teachers will help them get more. I think they are this by searching for these people who are entrepreneurs (like to start their center under CL ) vs other internet start-ups who are giving them 1 CR to 3 CR salaries.

Yes now searching for what I call sitting ducks is not easy but if you look around there are options available. We are not mutual funds we need one or two ideas in the year or two years.

CL Educate buys NSE Digital exam division. This is a very good move to utilize cash on balance sheet. This one can scale for all online examinations in India.

Revenue 200 CR and EBIDTA 17 %. 34 Cr. Paid 230 Cr plus 75 performance which is not bad. Hope they can scale for other CBT exams.

After many years i think this is good bet by CL Educate management.

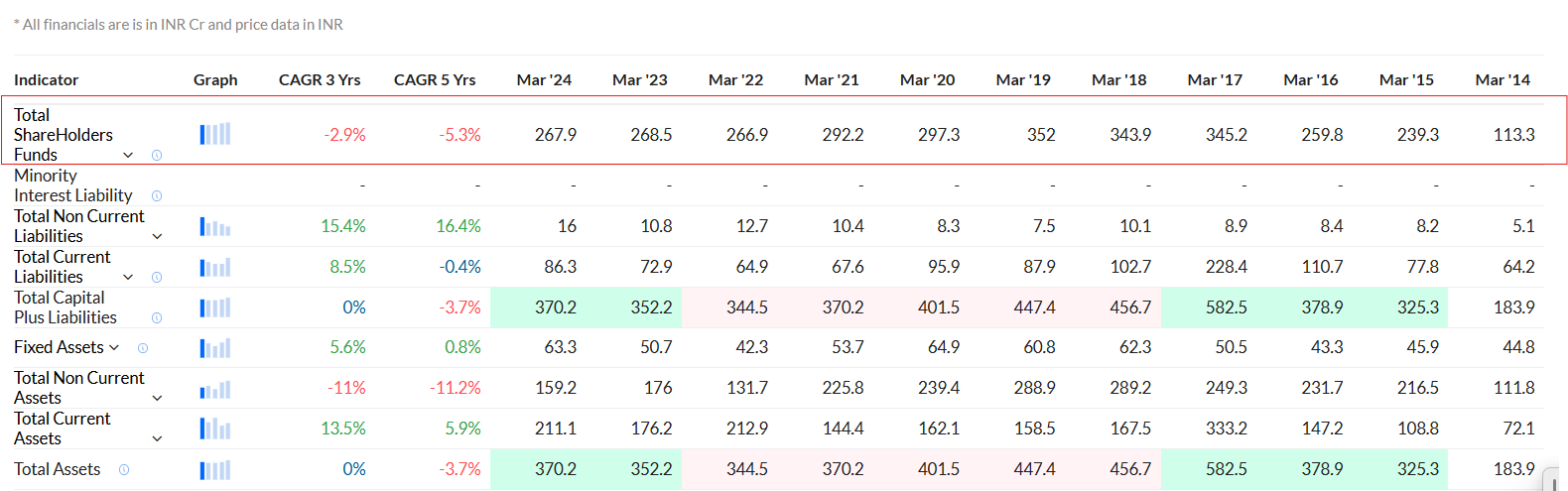

Quick question - why is their balance sheet (shareholder’s equity) not improving over the past 5+ years? Apologies as I didn’t have time to dig into. But would love to hear views if any of you have already analyzed it.

They have series of mistakes investing in schools and also had receivables from Govt stuck. Looking at equity growth does not help. They did lot of writeoff on invesments .They also had lot of cash on balance sheet.You should first look at Tangible capital deployed and incremental capital returns. Incremental ROIC * investment rate = EPS growth.

Edtech business throws lot of cash and is good business while Enterprise business is low ROCE which now growing internationally and they have decided to focus on better margin business.