CL educate among the largest organized listed player in education market which trading at deep discount. Though of initiating thread to jointly collaborate on this thread.

There is no moat in this business and hence it will rely on execution capability of management.

To me this opportunity looks very simple and it is available cheap to avoid deep analysis as the downside risks are very limited over 3 years period and upside is unlimited or at least 3 times . So i will present very basic framework and hypothesis. Here goes my simple checklist.

About the company: http://www.cleducate.com/about-us.html and analyst call transcripts to get hang of what they are trying to do.

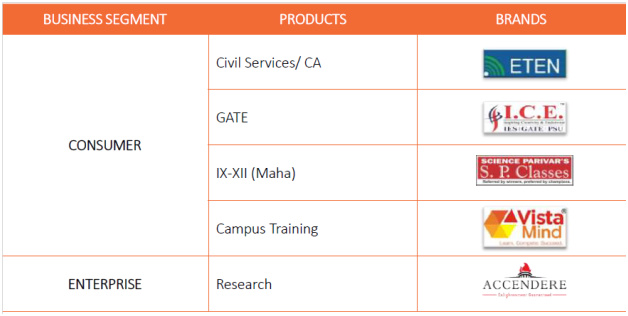

I am more interested in their consumer business and hopefully it is biggest contributor in years to come and hence no point wasting time on analyzing their enterprise business which eventually they will realize and hive off.

CHECKLIST:

-

Honest Management with Considerable experience: YES

IIM educated management who have built business in education due to passion. There is no sign of fraud or short-changing minority shareholders. They have built and scaled MBA CAT business in last 20 years.

Integrity: Good till now

Experience in scaling: 20 + years built CL to top 3 in MBA.

Power of incentive: less - Share in company 15 % by Sathya and 15 % Gautam - less than usual

Drive: Wants to build HDFC in Education. Focus on ROCE of 18 % or more

Capital allocation capabilities: Average -

CONSUMER MOAT BUSINESS WITH LONG RUN WAY- YES : Consumer business which can pass inflation to customers. The market is 37,000 crores growing more than 14 % annually.

Porter:

• Threat of substitute: Very less probability although technology disruption is another market segment where big Unicorns are already born like BYJU

• Threat of new entrant: No entry barriers

• Buyer Power: Consumers power low in dictating prices

• Supplier Power: Although suppliers (teachers ) have reputation power but this can be overcome by making them partners in business (Franchisee ) model. CL is doing this

• Competition rivalry: Competition is high but cost structures remain same for large players and everyone will have raise prices with inflation. Only very large players can distribute and spend on advertisements and expanding franchise centers. It takes lot of years to build reputation and hence acquisitions become very important to scaleMOAT:

• Pricing power: Present

• High Switching cost: Once Customer signs up usually fees are taken upfront and batch start dates are time bound and hence switching cost are high with customers as well as Franchisees.

• Network Effect: Opening more centers across cities with more products has effect of availability bias and develops a kind of network effect both students and franchisees reducing cost of advertisements and customer acquisition cost

• Low cost producer: Not yet known

• Negative working capital: Yes and requires almost no capital to expand

-

DOES Company stay in it Circle of competence (Specialist): YES

Yes, kind of although they did branch out in Schools business and Corporate side which are low ROCE business but it was done during recessions in CAT business. -

Target Market size must be huge with respect to company size- YES

37,000 Cr growing at 14 % per annum.

Fy18

CL Student Total Student appearing for test CL Market Share Addressable Market (50%) CL Market Share

GATE 25000 800000 3% 400000 6%

CAT 30000 300000 10% 150000 20%

civils 50000 1000000 5% 500000 10%

MBA 25000 200000 13% 100000 25%

CA 30000 300000 10% 150000 20%

Tutions & Engg 50000 2000000 3% 1000000 5%

- FINANCIALS and RATIOS representing good business with reinvestment opportunities -YES

LOW leverage: YES: Almost zero debt in fact cash positive

HIGH ROCE: Test Prep is 21 % while publishing and Enterprise

WORKING CAPITAL: Negative and float to expand. Virtually needs no money to expand

Consumer Business

2018 2017 2016 2015

Centres 200 162 161 146

Owned 91 60 54 49

Franchise 109 102 107 97

Students 86636 88462 77953

Digital 26857 24769 10134

Centres 59778.84 63692.64 67819.11

Students per centre 369 396 465

Rev per centre 0.93 0.83 0.84

Test Prep in cr 150 133 122

13% 9%

Publishing in cr 20 16 17

Rate 17,314 15,035 15,650

15%

ENTERPRISE in cr 97 71 60

University in CR 9 6 4

106 77 64

38% 20%

University 82 68 96

Per university 0.1097561 0.0882353 0.0416667

Total 276 226 203

Adjusted EBIDTA 53 52 39

EBIDTA % 19% 23% 19%

ROCE 14% 14% 11%

Guidance on ROCE - 17 to 18 %

-

CHEAP PRICE –- YES -FINALLY VALUATION MATTERS - can I get 15 % post tax returns over 10 years

Taking Seth Kalman method to find various scenarios of return expectations

Current Market CAP - 256 CRS - Price – Rs 180 Market cap < Sales -

Hitting of hammer on head valuation method - PE of 4 for business with ROCE 17 to 18 % and good potential growth without any requirement of capital

Cash on book s- 50 crs , Receivables and sale of school business is close to 100 Crs = 150 cr

EV = Market cap – 150 CR = 100 CR

Business avaible for less than 100 Cr and if we assume it does historical business with profit of 20 CR (Adjusted normalized profit ) so business is avaible at PE of 4 taking cash into consideration or even without cash PE is 12 So if business does ROCE of 18 % - we can easily expect return of 18 % for very long term -

VALUTAION BY MANAGEMENT GUIDANCE for 2020 - 60 Crs * 18 PE (Assuming 18 % ROCE ) = 1080 Crs - Basically 4 X from current price in 3 years

-

DCF Valuation without considering of cash and receivables - 20 % Return with growth of 10 % in Profits

25 cr

Initial FCF /OE 20 Assumed 5 cr for Maintnence capex

Years 1-5 6-10

FCF Growth Rate 10% 10%

Discount Rate 20%

Terminal Growth Rate 2%

Shares Outstanding (Crore) 1.42

Net Debt Level 52 crore of Cash

Year OE Growth Present Value

1 22 10% 18

2 24 10% 17

3 27 10% 15

4 29 10% 14

5 32 10% 13

6 35 10% 12

7 39 10% 11

8 43 10% 10

9 47 10% 9

10 52 10% 8

10 934 151

10 Year Valuation Multiple 18

Present Vaue of FCF Cr 128

Present Value of valuation Cr 151

Total present value minus debt Cr 279

Number of Shares 1

Present Value per Share 197

Finally, I think there is high probability that we will end up 15 % return over long term which is 5 times our money in 10 years and 25 times in 20 years unless management is totally fraud or they commit great mistakes.

Please let me know your views.

Disclosure : Invested 6 % of Portfolio and plan to make it 10 % .