Kalki is continuing it good run

Kill will slowly pick up pace, It is a movie which will become a sleeper hit

Sarfira promos look good

Auron mein kahan dum that again looks interesting

Hindustani 2 seems bad but perhaps marketing will help

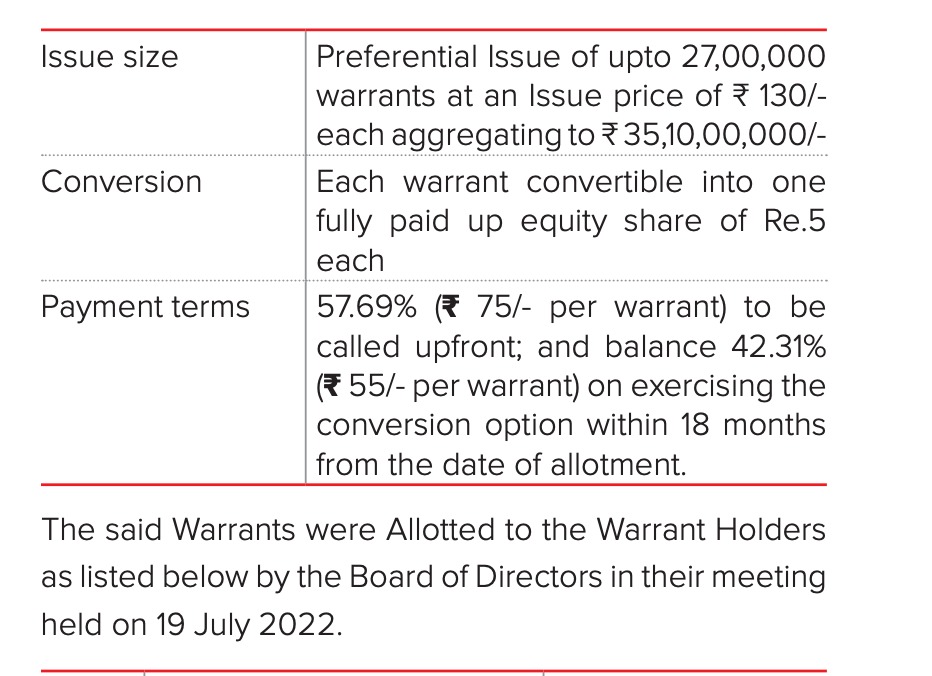

I came across this company while I was researching PVRINOX and the overall multiplex business. I observed some interesting things here. The promoter received about 27 lakh preferential warrants at a price of 130 (75 upfront + 55 once they convert the warrant to equity) with a time period of 18 months from July 19, 2022, i.e., January 19, 2024.

Mysteriously, the stock started hitting the upper circuit from late November 2023 (might be due to good results or something else) until January 19, 2024 (???), and from there it made a top around February 5, 2024. The stock was down 40% in about 25 days. Interesting!!! (Check screenshot)

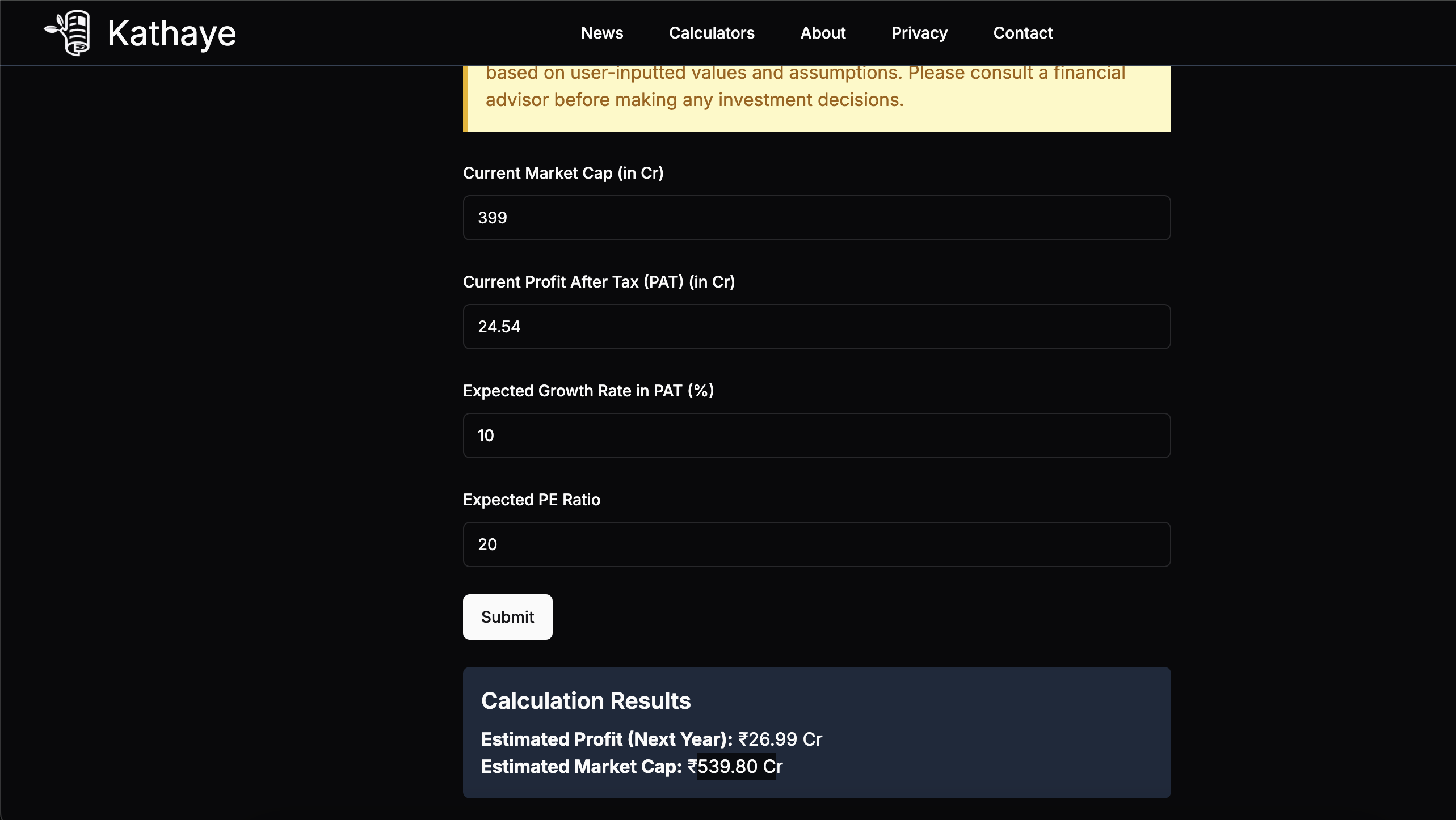

Overall, if the company is able to grow its PAT by 10 (high chances if revenue grows by 15%, based on past quarters and cost-cutting initiatives), expecting a PE ratio of 20, the market cap will grow around 35% (from 399 cr to 539 cr).

Disclaimer: Not invested. The above are just observations and for educational purposes.

The assets and liabilities of the Hotel Business have been shown as assets and liabilities held for sale since the company is in the process of selling the hotel business.

This is an accounting entry and the assets and liabilities continue to be on the balance sheet

People who are tracking cineline closely, need your views. Here is my thought process -

I have been tracking this company for long time. Hotel business sale was key trigger which happened on 29th March. Huge positive, will make them debt free. However, since they have signed SPA, we need to track when actually the money hits bank account and gives them funds to expand and repay debt.

A few days back, promoter has released a lot of pledge on the shares which again is positive. Though I dont know in real time what is pledged % ( I think screener has a lag or end of quarter data) . If anyone knows how to check this real time or close weekly interval, pls guide.

Utpal Sheth and promoter took warrants at around 90 price 1-2 weeks before hotel sale. These folks knew what was coming and hence this also gives confidence.

Now, the tall task still remains - they need to execute, add new screens, scale up PAN India, increase ticket size and obviously this depends on their abilities + good blockbuster release. For this execution needs to be tracked closely.

What other things should be monitored going ahead ? Is there anything here which is still tricky? To me, it seems like 1-2 quarter of good execution and bottomline positive (since interest payments will vanish now) and maybe over time screen expansion will lead to growth. Seems like a good story going ahead to keep adding to as and when execution happens.

Disclosure - recently invested after hotel sale news.

The movie business is facing tough competition from new, regional, and small-capacity theatres. I recently went to watch The Diplomat, and there were hardly any people in the hall. What’s your opinion on business.

We all know movie business is struggling due to OTT, regional players, lack of quality releases etc. etc.

Yes, growth may be a bit subdued due to above factors, but then other avenues are there - food business, SPH increase , ATP increase, New screen addition etc.

Overall, Cineline looks to be going in right direction with hotel sale, net debt free, getting quality investors, lean balance sheet, planning pan india expansion etc.

Q4FY25 result discussion - need supporting and counter views.

To me, more important than result was the conclusion of hotel sale. This has led them to be net debt free overall. This will free up interest cost as told by mgmt of around 22cr annually which can be deployed for expansion.

Doing quick ball park calculation - even if they maintain their FY25 performance- Operating profit can be 40cr and then no interest cost and depreciation assuming same as 20cr last year, we get 20cr and post tax @30% we can get 14cr PAT. This is having lots of assumptions - no growth in ATP, SPH, no other surprises, additional expenses for setting up new screens, normal business environment etc.

So this seems like a good win - hotel assets gone, more funds for expansion, at 10 cr PAT, the deal is at 30 PE (at current cmp of 91), ROE in FY256 can jump to (10/143) ~7% from NA right now.

{kind=link}