did a detailed analysis on the business, hope this helps:

Business Overview

Rasesh Kanakia, who started as a real estate consultant in 1984 and later ventured into real estate development, founded the company in 2002. He

initially made a significant impact in the early 2000s with his venture into the movie exhibition industry, operating a successful chain of multiplexes

named “Cinemax.” Predominantly established in Mumbai and nearby regions, this chain was one of the early entrants in the multiplex market.

However, in 2012, Rasesh sold Cinemax to PVR and took a hiatus from the movie business, re-entering in 2022 with the launch of the “MovieMax”

chain of theatres on April 1st, 2022, after the conclusion of a non-compete agreement.

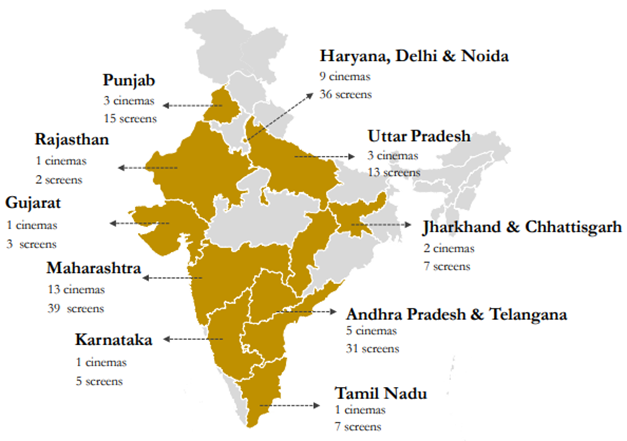

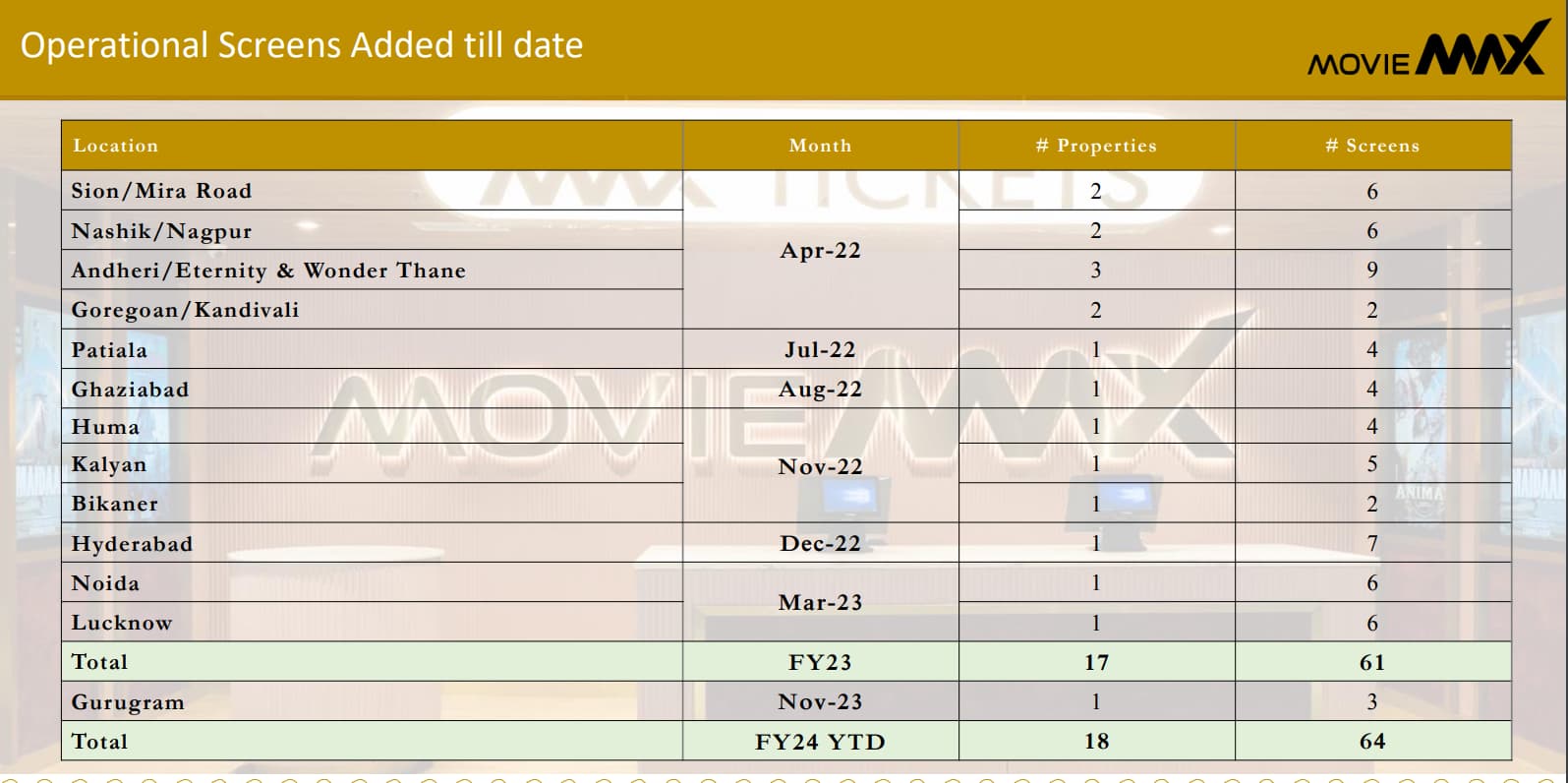

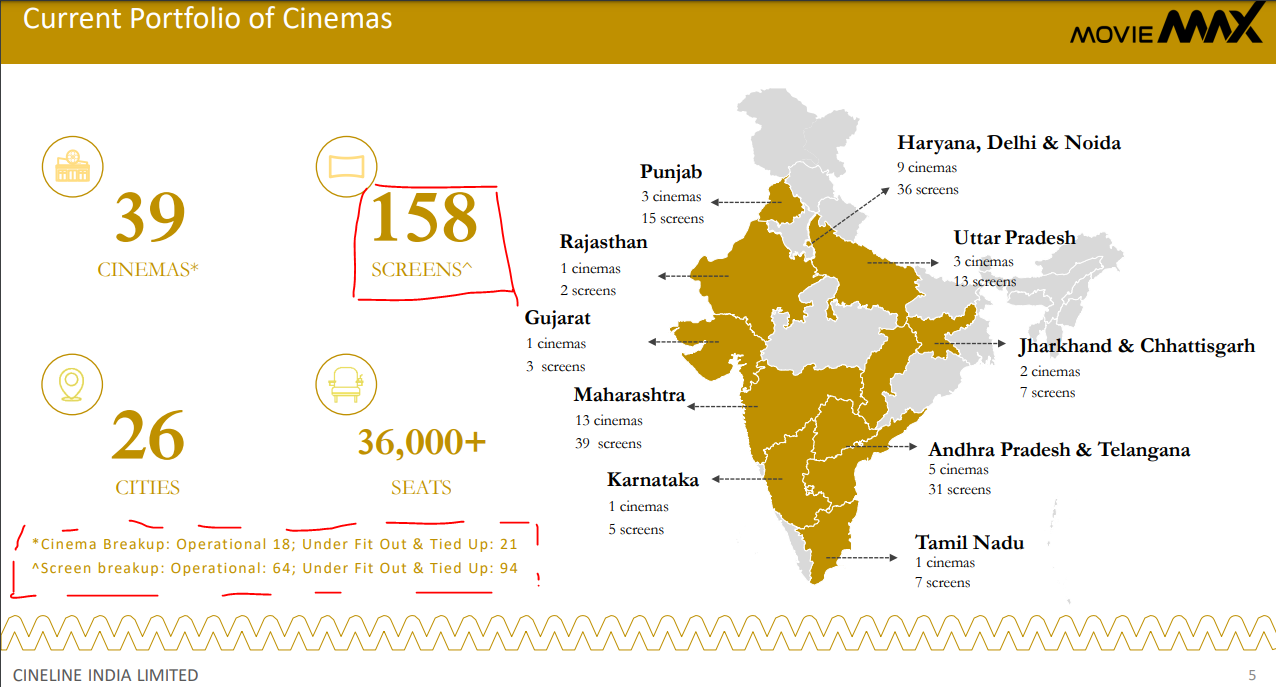

As of September 2023, MovieMax Cinemas has rapidly grown to become the fourth largest cinema chain in India, boasting 39 operating cinemas

across 26 cities and 158 screens. The company also owns two windmills in Viswada (Gujarat) and Revangaon (Maharashtra), with capacities of 0.60

MWA and 1.60 MWA, respectively, selling the generated power to the state government.

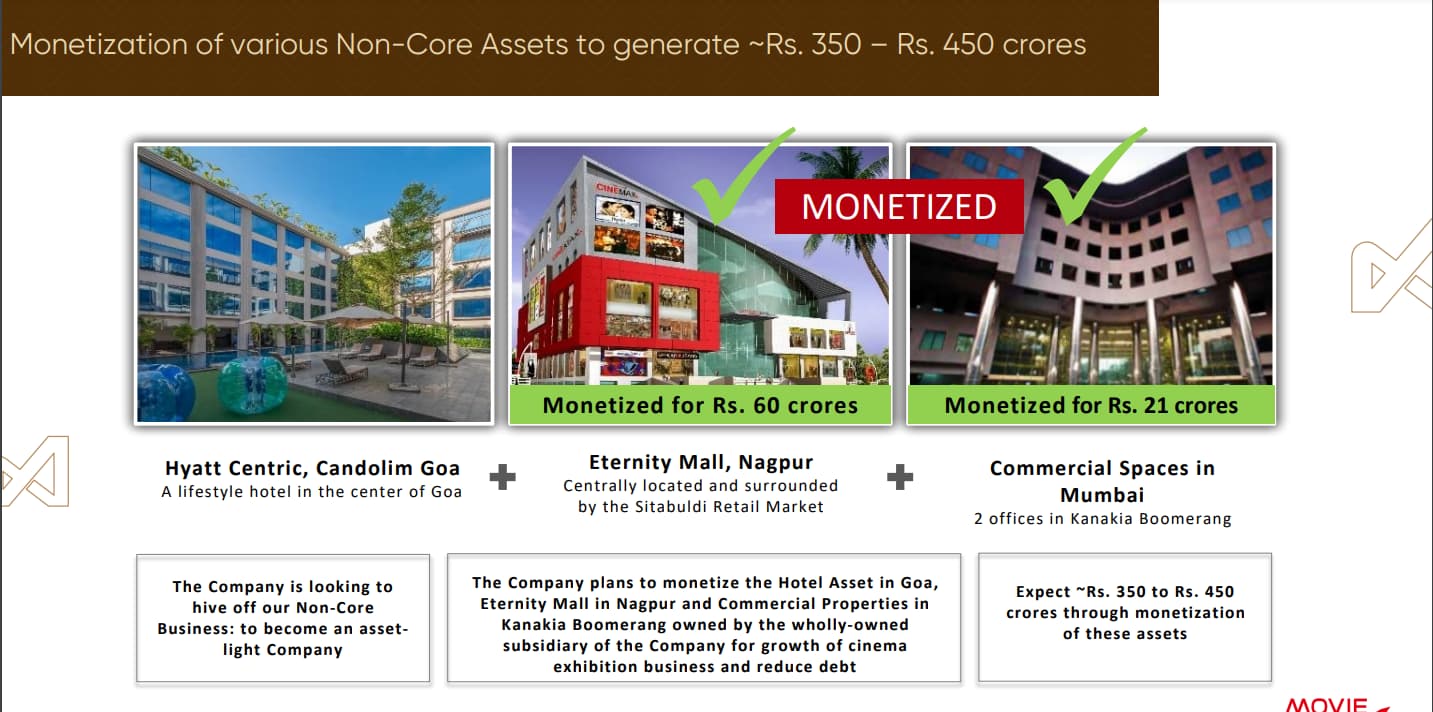

Previously, the company’s primary income was from rentals of commercial spaces in entertainment, commercial, and retail sectors. Now, it’s shifting

focus to become an asset-light entity, concentrating on growing its cinema exhibition business. This strategy includes monetizing non-core assets to

raise 350-400 Cr, which will be reinvested in the movie business. This includes the recent sale of commercial spaces in Mumbai and Eternity Mall in

Nagpur. (a) Commercial Spaces in Mumbai (2 offices in Kanakia Boomerang) has been sold for Rs. 21 Cr b) Eternity Mall, Nagpur surrounded by the

Sitabuldi Retail Market has been sold off for Rs. 60 Crores.)

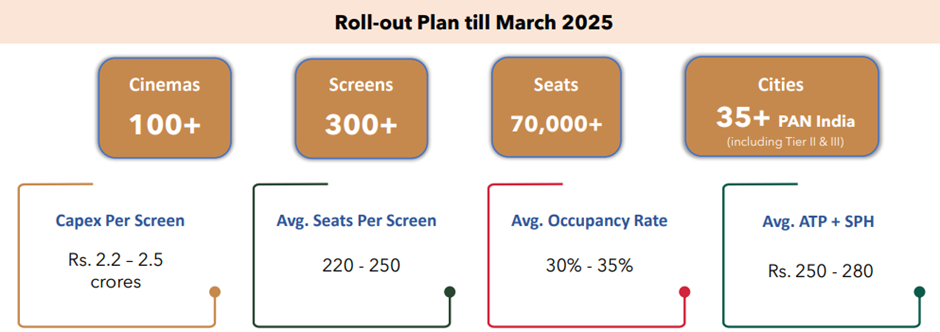

Moving forward, the company is focusing solely on its cinema business, aiming to enhance consumer experiences through the MovieMax chain. The

target is to reach over 70 cinemas, 300 screens, and 70,000 seats across more than 35 Indian cities by March 2025. The expected capital expenditure

per screen is estimated at 2.2 - 2.5 Cr, with a combined Average Ticket Price (ATP) and Spend Per Head (SPH) of Rs 250-280 per customer.

Business Metrics & Valuation

This financial and operational analysis of the cinema business reveals several key insights:

Revenue Growth: The company achieved a significant increase in turnover, reaching approximately Rs. 102 Crore in H1 FY24, up from Rs. 36 Crore in

H1 FY23. This growth is driven by both net box office collections (approximately Rs. 67 Crores) and food & beverage collections (around Rs. 28 Crores).

EBITDA Improvement: The EBITDA has improved markedly to about Rs. 28 Crore in H1 FY24 from Rs. 8.6 Crores in H1 FY23. This suggests an

enhancement in operational efficiency and profitability.

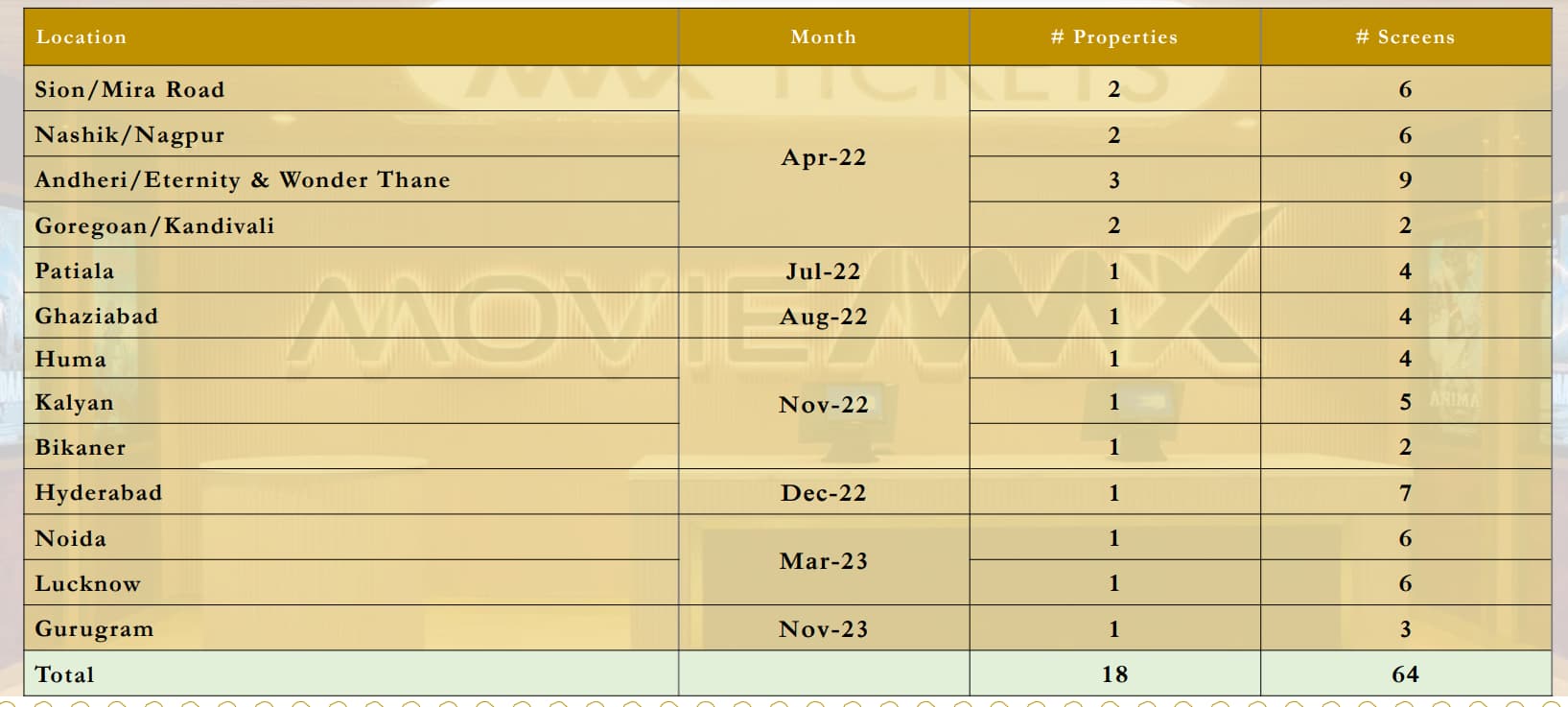

Expansion in Screen Count: The increase in the number of screens from 118 to 158 and cinemas from 30 to 39 within a year indicates aggressive

expansion, which is a positive sign for growth potential.

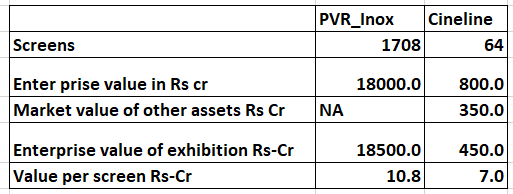

Valuation and Sales Projection: The business is currently valued at approximately 1X Sales for 2024-25. With plans to add another 150 screens in the

next 1-2 years, there’s an anticipation of a significant sales increase, potentially doubling the current Annual Recurring Revenue (ARR).

Impact of Expansion on Current Financials: The current negative EPS (Earnings Per Share) and cash flow can be attributed to ongoing investments in

expansion and new locations. This is a common scenario for businesses in a growth phase.

Management’s Strategic Approach: The management’s focus on growth, backed by a thorough analysis of future profitability for each new location,

suggests a strategic approach to expansion. This indicates a balance between aggressive growth and calculated risk-taking.

Small Base Effect and Future Growth: The concept of the ‘small base effect’ implies that the business is starting from a relatively low base, which can

result in disproportionately high growth percentages as it expands.

Competitive Analysis

The company is quickly rising as a prominent player in the movie cinema chain sector, ranking fourth in India behind PVR Inox (~1600 screens),

Cinepolis (~600 screens), and Carnival Cinemas (~450 screens). Chairman Mr. Rasesh is actively pursuing an aggressive growth strategy with the aim

to elevate the company to the second-largest position in the national market. As the company continues its expansion, it is expected to benefit from

operating leverage, which will contribute to cost savings and a reduction in operational expenses.

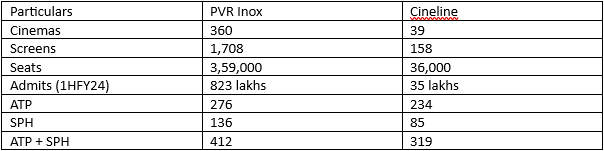

Metrics (H1 FY 24) PVR INOX /MovieMax

No. of Screens 1,569 /158

No. of Cinemas 340 /39

No. of Seats 3,40,000 /36,000

No. of Cities 115 (India and Sri Lanka) /26 (India)

Occupancy % 26.1% /~30%

Admits (No. of people) 8.2 Crores /35 Lakhs

Total IncomeH1 2023-24 Rs. 3344 Crores /Rs. 103 Crores

EBITDA Margin 33% /27.4%

PAT Margin ~2.5% /~0.1%

ATP (Average Ticket Price) Rs. 264 /Rs. 222

SPH (Spending Per Head) Rs. 134 /Rs. 83

Investment Narrative/Thesis

India’s screen count dwindled in the pandemic and currently there are 8,000 screens in the country compared to China’s nearly 80,000. The Indian

film exhibition space remains largely underserved with >6,000 screens being single screens waiting to be converted into multiplexes and can

accommodate more multiplex screens especially in Tier 2 and Tier 3 cities. As far as screen density goes, India lags miles behind countries like the US,

Canada, and China with six screens per million of population. In comparison, China has 30 screens per million of population while US has 125 screens.

Adding to it, the language barriers in India’s film industry have started to blur and dubbed south Indian movies are making inroads into the Hindispeaking markets and vice-versa.

In India, cinema is not just entertainment; it’s a vital part of the culture, a source of escapism or a family coming together event. Movies in various

languages cater to a diverse and large population, creating a constant demand for film content. With India recently achieving $4 Trillion of GDP on

the back of the growing consumption story and a growing youth population, who are generally more inclined towards entertainment and leisure

activities, including movie-going. As urbanization increases, the lifestyle of people changes, leading to more leisure time and a tendency to seek out

entertainment options like movies. The ease of online ticketing and the effectiveness of digital marketing campaigns have made it easier for audiences

to access and choose cinema offerings. The introduction of advanced screening technologies like IMAX, 4DX, and 3D has enhanced the movie-watching

experience, attracting a larger audience to cinemas.

Scuttlebutt

Regional Focus and Market Dynamics: The company is notably emphasizing expansion in South India, where approximately 70% of India’s moviegoers

are located. This region, especially Tamil Nadu, followed by Telangana, Andhra Pradesh, Kerala, and Karnataka, is identified for its higher occupancy

rates.

Seat Count and Market Share Goals: With cinemas averaging over 600 seats, the aim is to establish more than 200 screens in South India. The longterm goal is to capture a 50% market share of cinemas in this region, which is expected to contribute to reduced operating expenses and improved

screen occupancy rates.

Strategic Location Selection: Leveraging their background in real estate and multiplex operation, the promoters conduct in-depth analyses to identify

profitable locations. An occupancy clause is included in the lease agreements, a strategy not adopted by PVR, providing downside protection. The

average lease term is noted to be 19 years.

Quality and Service Differentiation: The insider highlighted the superior food quality offered, including live counters, a feature not supported by PVR

in South India.

Competitive Landscape Awareness: The largest player, PVR INOX, has a widespread presence across Indian cities. In contrast, Cinepolis is focusing on

expansion in metro cities only. The third-largest chain is currently facing financial struggles, being declared an NPA by its biggest lender

Business Strategy

Expansion Strategy and Market Analysis: The company’s expansion is strategically focused on locations that promise profitability rather than just

expanding for the sake of increasing numbers. This approach is underpinned by an understanding of the South Indian demographic and the lack of

quality cinema experiences in Tier 2 and Tier 3 cities.

Financial Model and Investment Strategy: The business operates on a revenue share model with mall or property owners. For instance, initial

investments of 3-3.5 crores are proportionally shared between the company and the property/mall owner. This model is particularly favored in

locations with a higher probability of lower occupancy rates.

Cost Management and Investment Efficiency: The use of a revenue share model significantly reduces the initial cost per screen, with a reduction of

at least one-third expected. The strategy also includes a refurbishing timeline of 6-7 years for each project.

Leadership Approach: The Chairman’s leadership style is described as pragmatic and grounded, focusing on sustainable expansion that prioritizes

profitability and efficient location targeting.

Revenue Share Model and Property Acquisition: The company has predominantly tied up its properties under a revenue share model. This approach

is not only cost-effective but also mitigates financial risks associated with fluctuating occupancy rates.

Acquisition of Standalone Multiplexes: A key part of the strategy involves acquiring standalone multiplexes that have struggled to resume operations

post-pandemic. This move is indicative of opportunistic growth, capitalizing on the market changes brought about by the COVID-19 pandemic. By

taking over these multiplexes, the company can expand its footprint and market share, particularly in locations that may already have established

infrastructure but lack the operational bandwidth to restart independently.

Key Risks

Shift to OTT: OTT platforms offer a wide variety of content, including movies, TV series, documentaries, and more, all accessible from the comfort of

one’s home. This shift might lead to less and less people visiting and spending money watching movies in the cinemas

Revenue Share Model Vulnerabilities: While the revenue share model reduces initial investment, it also ties the company’s fortunes closely with

those of property owners. Changes in the terms of these agreements, or financial difficulties faced by property owners, could impact the company’s

revenues and operational stability.

Operational Risks in Acquiring Standalone Multiplexes: Taking over standalone multiplexes that failed to restart post-pandemic involves inheriting

any existing operational challenges.

Lease Agreements with Occupancy Clauses: While the occupancy clause in lease agreements provides downside protection, it could also limit

flexibility. The company may be obligated to maintain operations in less profitable locations due to long-term lease commitments.

Promoter Background

Mr. Rasesh, serving as the Chairman, collaborates closely with his brother, Himanshu Kanakia, who holds the position of Managing Director. Himanshu

brings a unique blend of engineering talent and innovative skills in project development and the film exhibition industry, contributing his expertise to

the expansion and construction of new venues. Additionally, Mr. Rasesh’s son, Ashish, has joined the business as the CEO of the movie exhibition

sector. Despite being relatively new to the industry, Ashish is dedicated to realizing the vision set forth by Mr. Rasesh. The management’s previous

experience in both the cinema business and real estate development indicates that they possess the appropriate skills for re-entering the industry.

This background instills confidence in their ability to meet the outlined expansion targets. Their approach, characterized by cost efficiency and strategic

planning, further supports the likelihood of successful expansion.

Conclusion

The company appears to be in a strong growth phase, reflected in its rapidly increasing turnover and EBITDA, along with aggressive screen and cinema

expansion. The valuation at 1X Sales for 2024-25, suggests that the stock may be undervalued, offering potential for significant growth as the business

scales and stabilizes. The management’s focused and analytical approach to expansion supports a positive outlook for the company’s future