Ideally, they should not sell Goa hotel. It gives them a stable income source of roughly 16cr each quarter. It also acts as a hedge in real estate which is increasing. A good EID will help this stock

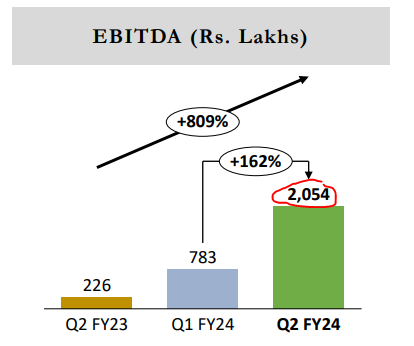

Cineline did 20 cr ebitda in q2-24 from cinema business with 64 screen operating, extrapolating it as an avg for 4qrts makes it rs 80cr ebitda(its naïve and too much of an optimism to assume this considering seasonality, hit releases etc, but just for sake of some estimation)

if they sold hotel for rs500cr(as they claim its the valuation) and added 230 screens (its from the company published info about cost of installing a screen) they should generate around rs300cr additional ebitda.

Currently hotel does an ebitda of rs 10 cr per year, so growing screen count looks like better capital allocation.

Its still however a riskier investment considering the past history, but it can playout well if they execute as per the published plan and maintain operating metrics.

2 Likes

However, it won’t pan out like that as per me. I am doubtful on 500 Cr valuation for hotel. It is a stretched valuation. IHCL is presently a 84000 Cr Mcap company with 23000 operating rooms and 10k+ inventory.

Hence, conservatively we should consider 2-2.5 Cr per room valuation for Goa hotel. My assessment is 350-400 Cr.

Further, they will use this money to get debt to a comfortable level (From ~350 Cr to ~<100 Cr for <1 debt to equity). The remaining 100 Cr will be used for reinvestment. I agree it will still be better.

But, I don’t hear any progress on hotel sale also.

Management has confirmed that sale is in advanced stages, it is likely to be done within next 2 quarters.

Also they are getting slightly less than 300cr as mentioned earlier by management

2 Likes

can you share a source of the info please?

Company participated in investor conference by Arihant capital, it will be live on Youtube in some time. They shared the over the call

Thank you , appreciate that, will look up.

Results are out

- Just ok Result

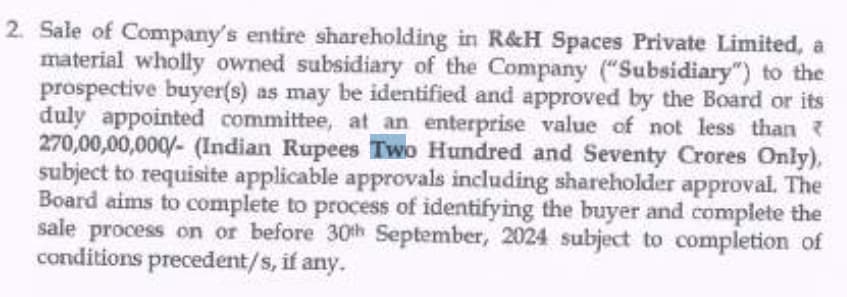

- Looks like hotel is being sold for 270 CR

- Release calendar seems like dull

1 Like

Where was this notified ? Could not find it in the press release.

Moviemax offering election results.

Looks like there is a drought for good movies for last 3-4 months.

Disc : Invested.

As per promoters this draught would continue, as there is no good content on horizon as well.

1 Like

Now there is a pledge by two promoters. Do we know the real reason? Document says for personal reasons

1 Like

Not much movement on the counter. Is there any positive news coming for this stock? Has there been any update on hotel sale/ quicker opening of screens?

There is bad news… More shares pledged…

Corp Governance issues highlighted here with the hotel property being acquired from a related entity at highly inflated price and now being sold by the public entity at a loss!

Caveat emptor!!!

5 Likes

The Promoters integrity is large overhang in this counter. I have spoken to a guy who has earlier worked for Cinemax , the feedback wasnt very good. Though he wasnt explicit about it.

1 Like

270cr is the value on books right? also its mentioned there that “not less than 270cr”

generally book value depreciates every year and after four years of cumulative depreciation 334cr might have become 270cr “on books”

1 Like

Back and forth between hotels, same with exhibition screens, heavey pledging, related party transactions, several things make it feel discomfort. The only brightspot is Exhibition screens opening at fast pace and their operating metric looking good (if you trust the reported nos).

This is an appalling article. This is an integrity issue from the promoter then.

They have gone back on their projections on screen growth. This could have been a decent business if operated well. But, nothing survives having bad management.

Also, thank you so much for sharing this.

1 Like