You’re very kind ![]() . I’ve been working on my position sizing, and the idea is to buy significant amounts when valuations are cheap. Something I’ve learnt from your post on Pidilite, as well as Hitesh sir’s posts on his portfolio thread.

. I’ve been working on my position sizing, and the idea is to buy significant amounts when valuations are cheap. Something I’ve learnt from your post on Pidilite, as well as Hitesh sir’s posts on his portfolio thread.

However, I’m sitting on cash that will bring down the allocations at cost over time.

When we think of them as essential service providers, it’s in the context of covid. They employ nearly 20,000 people who service 120,000 hospital beds, and the management is right when they say these people are needed as much as doctors or nurses. Covid safety measures have also brought this to light. Secondly, their frontline employees, both in India and abroad were classified as essential by the respective governments, and were allowed to come in to work during the lockdowns. They were even given a grant by the governments to not let any of their employees go. They stand to benefit from regulations as long as governments prioritise blue collar unemployment as a data point.

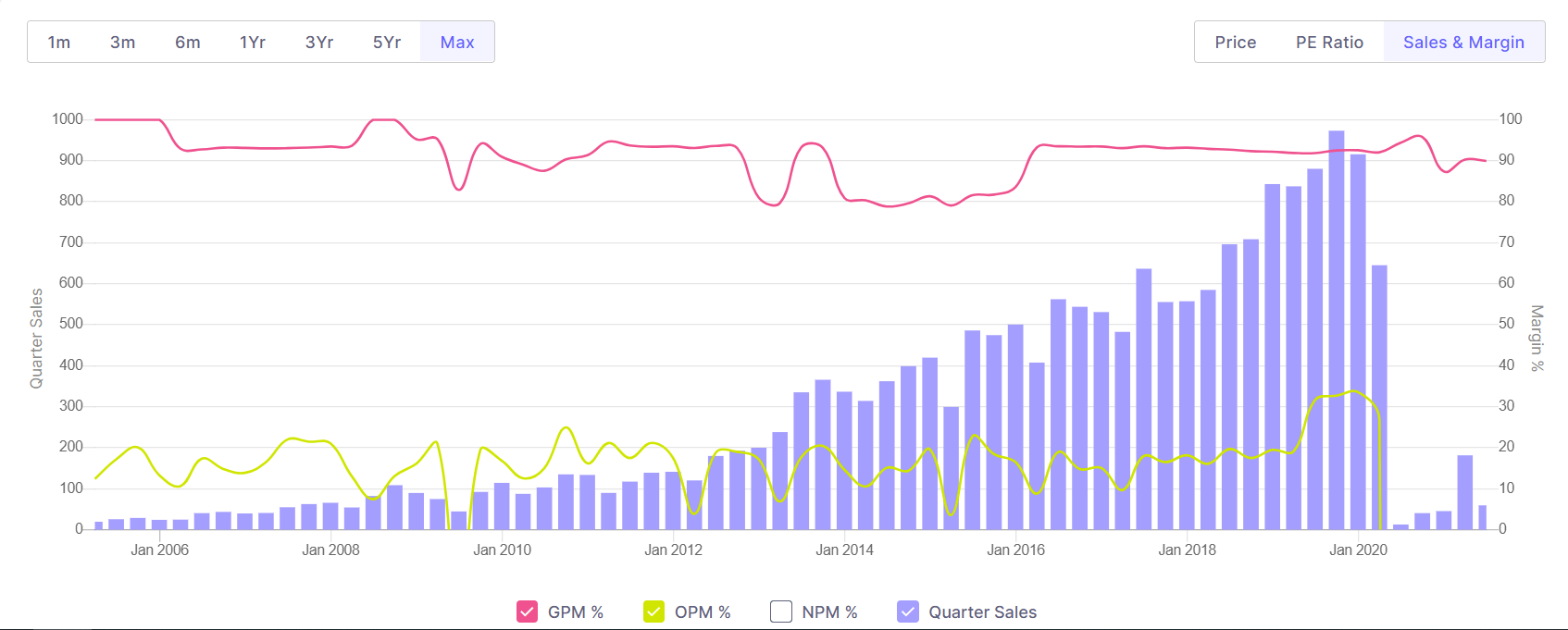

We see the truth of this in their revenues and margins. If we look at the sales and margins of a company they serve, say a cinema like PVR, it’s easy to immediately see the effect of the pandemic:

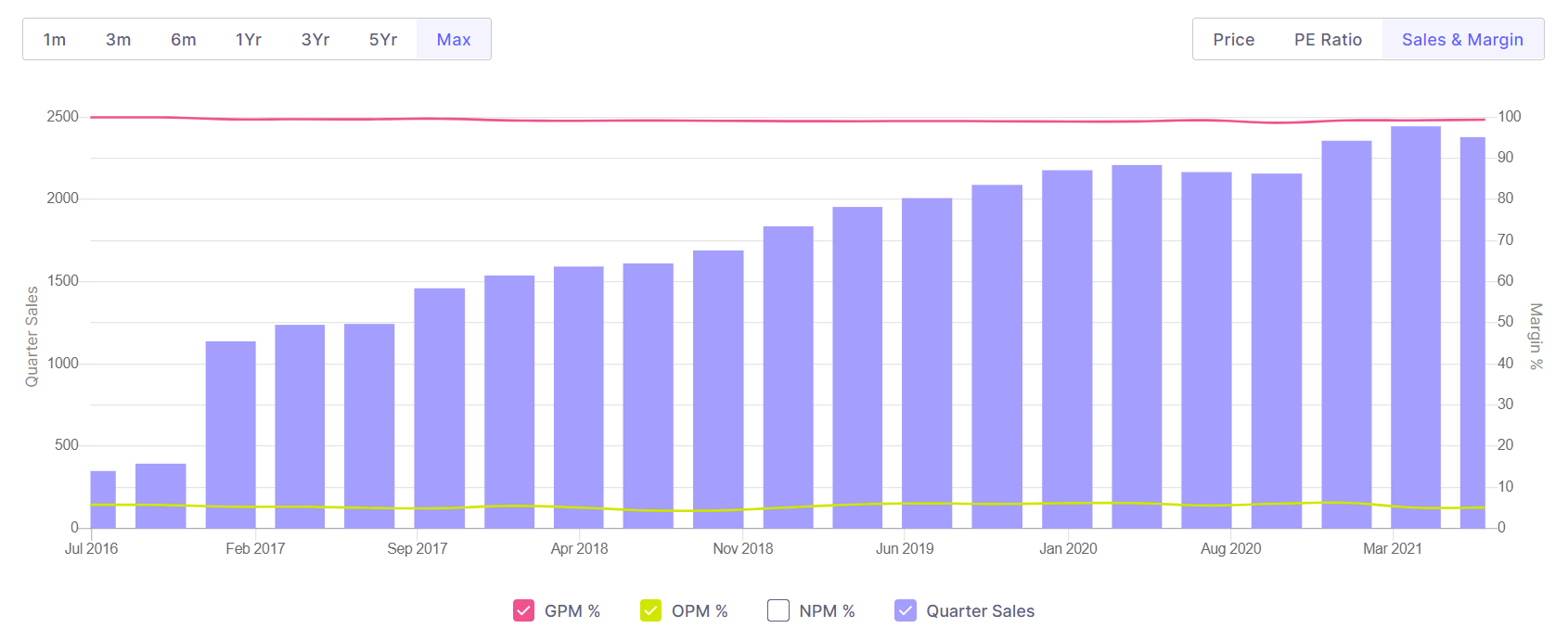

Whereas for SIS, try pinpointing the impact covid has had on revenue and EBITDA margins:

Covid would have been a nightmare for them, dealing with so many employees, and yet they’ve come out of the two waves so far without a blip. In terms of government regulation, I’ve been reading about how the labour laws in the country are archaic, and there are new codes which are in the process of being implemented that allows more freedom for the formalisation of this sector.

Here’s one read out of many:

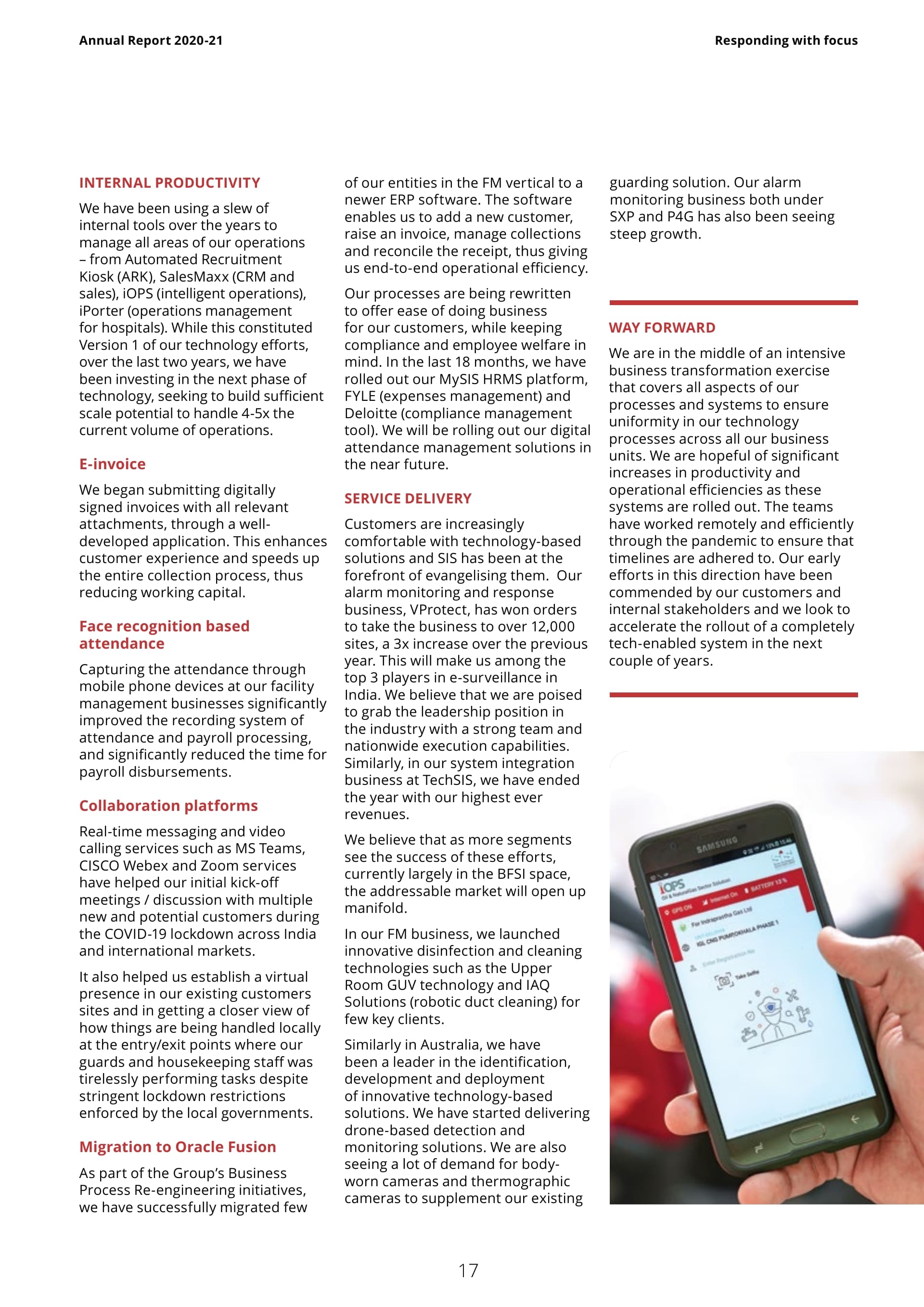

The global EBITDA margins are around 4-5%, and you’re right that staffing faces a lot of competition and there isn’t scope for margin expansion. SIS guides margins of around 5-6% going forward, and the transformation they’re working on is to incorporate surveillance products into their portfolio. I’ve attached a single page from the annual report that explains what they’re working on. They aim to get 20% of their EBITDA from products/solutions rather than services, by FY25.

As they’re present across the country, and as you’ve experienced in your office, the management spoke about how they’ve got sticky customers who tried local providers and yet came back to them. After covid one also wonders how many local security staffers / facility management providers have survived. SIS’ plan is to grow organically over the next five years and push their market share from 5% to 15%.

Please feel free to post your thoughts, you’re always welcome. This is a really interesting business, and we would need multiple posts to have a conversation on all of its verticals. They’ve become bigger than just being security staffers. Some other points of interest:

-

Only 38% of their revenue comes from security solutions in India.

-

Their facility management is flexible, and they cater not just to malls, but events like sports and concerts. The latter have been depressed by covid and would bounce back after the world opens up again.

-

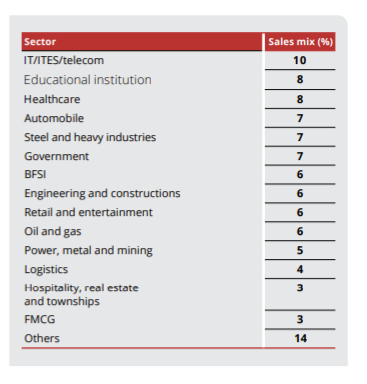

They’re diversified even within each vertical. Here’s the breakup amongst the security solutions:

Would definitely recommend reading the annual report, simply because it’s so unique ![]()