I agree that it’s quite a way away, but the 1 crore SMA target is what Mr. Modi has been pitching in recent interviews. Reliance’s recent announcements reminded me of Spice Money, as they would be a direct beneficiary of any empowerment of kirana stores. If Reliance plans to stock kirana stores and use them as distributors, we should see some correlation with its uptake, and Spice Money’s GTV / SMA. Can write to the company regarding this.

What I also like is that they’re debt free at the moment, and since there isn’t a moat in the business, if they’re able to scale up and outlast the competition, perhaps that’ll be a key trigger. This is why I also had mixed feelings about the zero cost onboarding.

Please free to start a new thread and use any material you like; I’ve simply copied things from the investor presentation, and posted my thoughts on the Q3 earnings concall. The reason I haven’t started one myself is that I’ve watched every single interview with the management, and have read all available articles on Digispice, so there’s probably 3-4 hours of content available to understand more about the business. I even started looking through YouTube, as a lot of SMAs directly compare the various mobile ATM apps and seem to prefer Spice Money. In this forum I’ve only come across 3-4 people that are invested in the company, and there is agreement that the business has no moat or margins at the moment. I thought if they start showing earnings, or go through some really nice margin expansion, that would be a good time to create a thread, but please feel free to make one!

I’m probably going to create threads for Birlasoft and Tata Power too, atleast for the benefit of future investors that want context on the company at various points in time.

There’s been a world of difference in the process!

This forum taught me the shortfalls of a backward facing screener based approach like this:

And I learnt to instead read through annual reports, attend concalls where the Q&A sections reveal gems of information, aggregate every little piece of information from exchange filings, and focus on the management’s vision for the future. Various posts helped me understand the nuances of valuations, and why it’s a craft.

Over time my coverage universe has increased from twenty companies to over two/three hundred companies, and I realise that initially I had invested in some companies purely because they were the best ideas out of a very small sample. As I read more annual reports from companies I haven’t studied before, they show me new holes or sparks of genius in ones I do own, and help me understand the industry better.

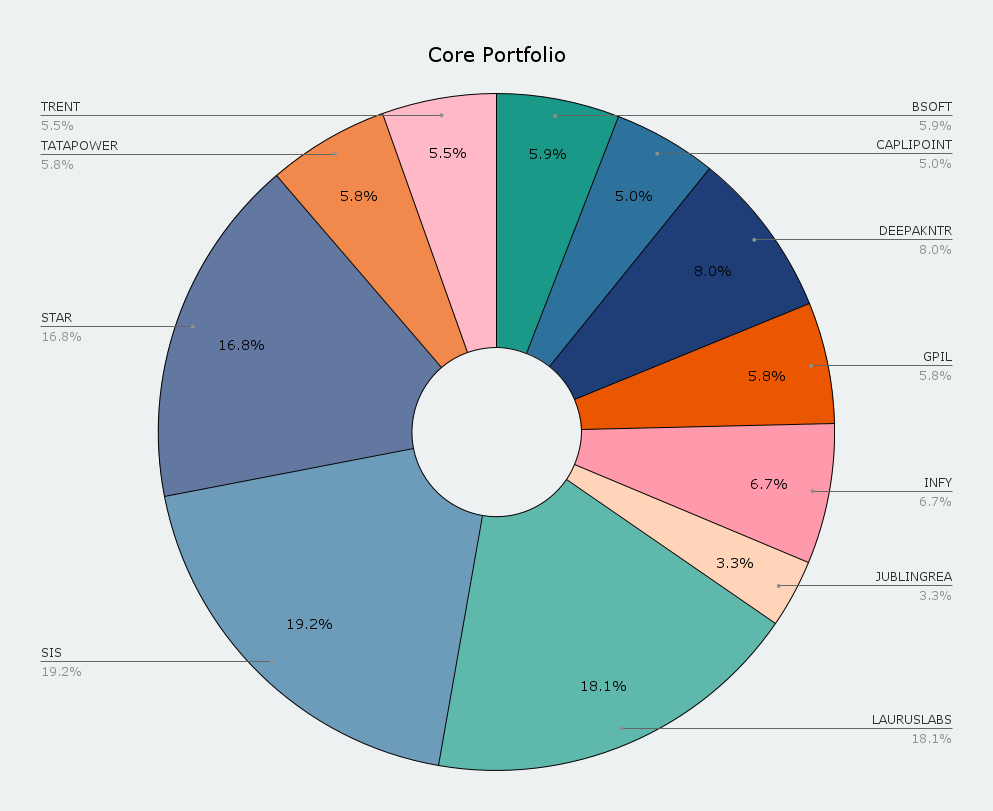

So the core portfolio has changed as my understanding has gotten better, showing me better ideas at the same valuations / prospects, and has changed as I think of the different risks I’m open to (geography, raw material, valuation). I’ve tried to make sure I’m not open to the same risk across multiple companies (Maybe one high valuation idea at most if at all, prefer to not be overly reliant on one state in India for revenue, etc). I’m certain my future portfolio will carry the same style, but with a lot of different names.

How long do I plan to SIP? I’m moving a lot of my net worth into equities over the next two years, and I’m not afraid of drawdowns. Hitesh sir pointed out that during such a time, almost all companies in the index are down commensurately, so there isn’t any opportunity cost in switching to a dream portfolio. After these two years, it’ll be a lifelong SIP after accounting for expenses, I’m planning my finances in a way that the portfolio won’t need to be touched for expenses unless there’s some unforseen emergency, and I’m reinvesting all profits.

As an update: I’ve exited Navin Fluorine and Hindustan Foods (with much sadness) and have bought a lot of Embassy REIT at 336, which currently forms around 23% of the portfolio.

Thanks @Chins - Agree, this selling framework is very important as we mature as investors. Also, just like buying & holding, this framework need to be unique to oneself as per our own mindset & psychology. The one which works best for us!

Do let us know if you work & find a suitable framework for yourself…I would also update my section as & when I get more clarity over this! Cheers

How are you evaluating the risks in Investing in Embassy REIT. The whole work from home threat and how you see this play out.

Asking since it forms a large part of your portfolio.

This has been discussed quite a lot. I don’t think people want to stay home; it was a joy and something new during the initial lockdown in March 2020, but by the second wave I think we all became pretty weary of the pandemic. We haven’t really had holidays, and with current vaccination rates, I wouldn’t be surprised if things sour again by the end of the year.

A few thoughts on office culture / virtual interactions:

While Zoom has changed the way we have interviews and meetings, the biggest shortfall is the lack of organic opportunities to have 1:1 meetings in a group Zoom call. Anything you say is always heard by the entire group. While working from home, I’ve also missed the little interactions that happen around the workplace, and scheduling Zoom meetings is always formal.

There is also a big difference between the living spaces in the west and in India. In the west, you’re usually alone at home or with your partner, and parents/relatives aren’t in the same house, making your home a viable candidate for an office space. In India we keep our relatives close to us, and don’t control the living spaces on our own terms: mealtimes, etc.

Coming back to REITs, office spaces will always be in need, even if companies move to a blended model. Two years from now, if there isn’t the danger element of the pandemic preventing us from going outside, I think employers in various sectors outside of tech will be pushing people to come in to work.

Personally, I want a component of the portfolio to be dividend based for the future. Since I think office culture will remain in the future, Embassy’s present headwind presents a buying opportunity. As these are new in India, maybe we’ll see REITs in industrial / residential sectors in a few years. I also really like Powergrid’s InVIT and want to buy some given an opportunity.

I still feel wary about the commercial real estate space. The points made above are sensible from a working experience perspective and at a time when people are very tired of remaining inside their homes. So there would possibly be some short term tailwinds when things open up.

But I think in the long term, COVID has really put a huge spanner in the works by making people try out and experience the work from home culture. My key areas of concern remain long term returns, and from that perspective I think it will be critical that:-

CEOs whenever they face any cost or bottom line pressure will explore options to enhance bottom line, and saving rental costs would be one of the easiest levers. Would a CEO look smart to his shareholders and board if expanding office space, I am not so sure

It will eventually come down to total aggregate demand in a scenario where some will move back, some will work on a mixed model and some might continue the current work from home. In that case, I feel uncertain that the demand will return to 2019 levels

Will the value of commercial real estate rise and eventually benefit REIT holders apart from the rental/dividend income? Commercial real estate was one aspect in the industry which had not suffered much. For it to appreciate from current levels if the demand does not pick up and inventory remains high remains in question

The key issue I faced when evaluating these REITs in India were that firstly they were all commercial and secondly a large section of their customer base was IT/tech companies - the most conducive to work from home. The internet has severely impacted several industries in the past, and I was worried this might be an evolving case of the same.

That said, my views on residential real estate are completely the opposite. I wish I had some REITs of good players I could invest in for the dividend yield and appreciation mix that REITs provide as a diverse instrument. But like a typical capital cycle, there have not been any listings in the space - my confirmation bias makes me think that it might be that these residential developers realise that there is too much value in these properties at the moment and hence not the opportunate time to divest or go public. If I was looking for a house to buy, I think I would go buy one right now!

Discl : Not invested in the REITs, personal views only with no expertise in Real Estate

I agree, I too would look to cut rent, and have seen how rents have fallen in my area post covid. There are two things that I want to track:

On a micro level, I don’t know the discussions that are happening from workplace to workplace, and the experiences of my friends differed according to the relationship they had with their managers. Some were called in due to ease of having meetings, others were allowed to stay home. Will try to understand what senior management is thinking of.

The single biggest thing to track in my opinion is a company like KPMG or Google. In the west, they’ve moved to a 60% work from home model and have said that they’re looking for a more flexible rental agreement with their office spaces. Whether this plays out in their Indian counterpart offices is top of my list. (Luckily, we also have an active forum member working at Google whom we can poke for information )

I also want to say that confirmation bias makes us read the articles that echo exactly what we want to hear, so I’m very happy to hear a reality check on this thread or on the REIT thread where your opinion would also have more visibiliity.

So here’s the story on this in the short term. While the UK moved towards a blended model and left a majority of employees home, there was still a demand for office space. Why? Because while the number of people in the office dropped, they needed more space between those that were in, and had to make changes to facilitate safe distancing. Granted this won’t be necessary post pandemic, but we aren’t there yet.

But if offices become destinations to meet coworkers, get inspiration and exchange ideas, rather than just to sit at a desk, those in buzzy locations make more sense. If organizations don’t need as much space because people work remotely more often, they may choose not to cut their rent bill but to spend the same amount on a smaller, more characterful building in an amenity-rich central location – a much more attractive destination for employees than a featureless office park.

Gensler’s blog is also a wonderful read on where they see the future:

Overall, I like the detailed disclosure that Embassy provides, and will continue to track the story. I also don’t think we should treat them as stagnant, and countermeasures like leasing, subleting, and offering flexible tenancy terms could be a viable response to blended models.

With my own dividend plans, I’ve made provisions for Powergrid, and would happily lap up an industrial / residential REIT in the future.

Almost every firm is going for hybrid model of 50% working from home and 50% office. So if all MNC’s decides to go this way, unless there is strong set of new firms coming in to fill up the gap, I dont see huge upside for REIT’s who are only focussed on office rentals.

I agree, and I’m prepared for pain. My entry decision had to do with the NAV being around 387 per share, giving me a discount of 13%. I should have entered at 310 levels, but missed the bottom.

Specifically, I like the disclosures on leases that are expiring in the next five years, and their plans explained in the annual report and other disclosures. We’ll only know as the story plays out whether this is a value buy or a value trap.

Thanks for sharing the Housel article, was a really nice read.

As I keep learning, I realise just how many opportunities I’ve missed because I haven’t studied all companies in a particular sector. Thanks to the forum for pointing out the de-merger opportunity in Stelis. I’ve spent the last two weeks studying Strides’ standalone business and the potential Stelis has. While watching Sajal sir’s seminar on biotechnology this weekend, I was surprised to see both Stelis and Laurus Bio spoken about, and gave me a chance to gauge my understanding of both businesses. Added a position of Strides this week, using all profits from Hindustan Foods and Navin Fluorine.

Clean Science and Technology looks to be an excellent speciality chemicals company, and is vying with Vinati Organics for the top spot of my want list. It’s a global leader in its segments and has best in class EBITDA margins. However, the standout con is purely on the valuations it’ll sell for after the IPO. At an FY21 PE of roughly 50, it’s not cheap, but has headroom compared to peers trading at multiples of 60-70. The best time to have bought it was during the margin expansion from FY18 onwards.

I also like it for a different reason; it’s the perfect partner to Deepak Nitrite in my portfolio. Here’s why. Its key starting material of anisole is produced from phenol. If the phenol value chain accounts for 58% of Deepak Nitrite’s topline, they’re adversely affected by a drop in phenol prices(Forgetting the management’s skill in negotiating long term contracts). Clean Science is the opposite, and benefits from a fall in phenol prices. I should be de-risked from phenol cycles if both companies are smart about their raw material supply chain. (I was also thinking of Valiant Organics along similar lines)

However, as the IPO is oversubscribed by over 200 times, I’m probably going to get a paltry allotment, and I’m praying that it falls sharply post listing against all odds.

Will post an update on the allocations once I’ve finished my buying for the month of July.

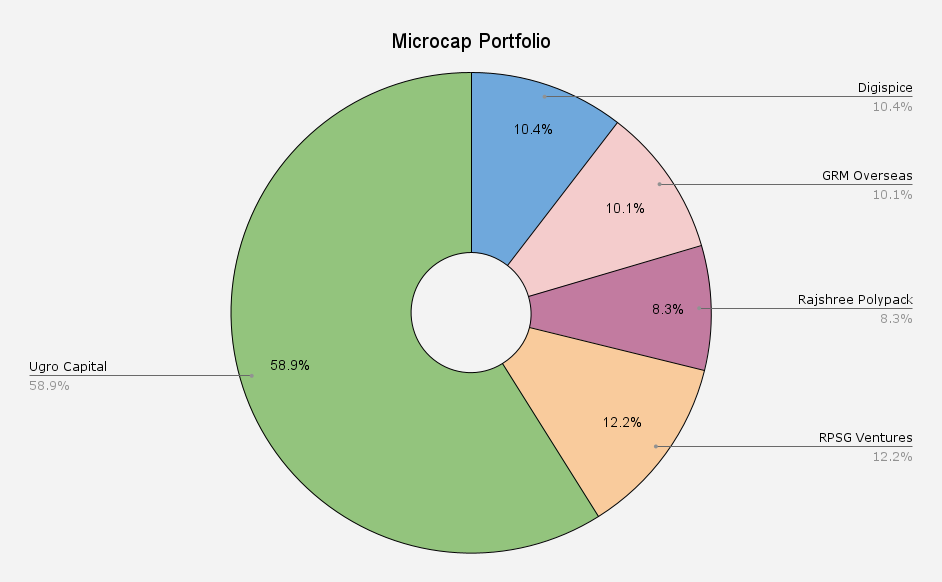

@Chins - Great find on DIGISPICE technologies at lower level. I am trying to find promotors and their profiles. I couldn’t find them either on Investor presentation or on the website https://www.digispice.com/

Hey, in the same website you linked, the information on the board of directors is given in the investor relations section.

If you’re interested in the management, Mr. Dilip Modi frequently gives interviews on Youtube and the earnings presentation / concalls are available there too.

Digispice and GRM Overseas are free, as I sold both after they rose 7-10x my entry. Kept some of the remainder to just monitor the business going forward.

As a fun fact, the Infosys in my portfolio was bought late in 2000 during the fall from its peak. The number of shares have gone up ~50x due to splits and bonuses. Had a long conversation with my family about investing during the IT bubble, and it’s a lot easier now for retail investors to gauge valuations. No profits were made until 2006, but the dividend yield is currently ~13% per share based on original cost.

So many winners were sold too early in the family. My parents bought HDFC Bank in 2001, Avanti Feeds at 34 rupees, but sold them after 200-300% returns.

Addressing the elephants in the room:

SIS India is currently my biggest holding. The investment thesis is based on three key models:

It’s a defensive play on essential services. Every time you build a shopping mall or a new office, they get business in 2-3 verticals, from security staffing to facility management. The moat is just economy of scale, and stability. If the world ended tomorrow, SIS would be the last one standing and still somehow churn out 5% EBITDA margins.

If their cash flows remain stable, one can see that there’s a legitimate case for them to deserve higher multiples. Their 5Yr CFO CAGR is currently 54%, while the share price hasn’t moved. One can’t compare to either Quess or Teamlease, but SIS is still available at less than 1x sales.

Finally, the labour market in India is extremely unorganised, with the market leaders only having < 5% of the market share, compared to 15-20% globally. SIS is focused on improving the market share over the next four years. There has been talk of how the recent changes to labour laws are meant to improve ease of doing business, and SIS has just taken on a director who has had 30 years of experience with labour laws.

I’ve mentioned in a post earlier that Tar’s writings on Stelis lead me to study the company. In the past, Strides has chosen to not go via the IPO route for demergers, and I’m hoping this time won’t be an exception. The standalone business has a lot of exposure to US generics. We’ll know during the results whether there has been price erosion in their molecules, but given a part of their portfolio was a wash last year, it may be offset.

My plan is to purely be in Stelis post demerger.

I’ve been accumulating Ugro in the last two months, and expect pain in Q1 as they have been hit by Covid. Management is being cautious, and I don’t expect growth for a year or two. Until then, I’m happy to accumulate below book value. Price has recently fallen as Abakkus Fund sold their holdings. I don’t see it as a red flag as this was a tail holding for them, but if other PE investors pull out, that would be a concern. I sold my holdings in CreditAccess and moved the funds into Ugro, as they’re both in the MSME sector, and I see a higher upside in Ugro for the same risks due to covid. We’ll know more about asset quality as the story progresses.

Keeping my REIT separate from the portfolio as I see it as a really defensive FD that compounds over time.

Currently studying Natco, Nykaa and Valiant Organics.

Admire your uniqueness in thinking as that is what makes a difference over long term. We would find very few, infact no one in this forum who would have SIS as their largest holding or even more than 10%…this clearly reflects your independent thinking approach…congratulations!

Having said that, you are well aware as you mentioned SIS cannot be compared to Quess/Teamlease as probably because the later are more inclined toward white collar jobs while SIS is more blue collar…I have not researched this area much but remember I was interested once, if I am not wrong, during SIS IPO when I felt I have read/seen this name somewhere and was positively surprised to see it in every security person’s shirt in my office…Next, I was also intrigued when I read once that Patanjali was interested in the space of security guards…this news came for a short time and maybe their interest faded away later…but all this rightly points to the fact that you present and perceive SIS not as a blue collar job provider but rather “essentials” provider…

However, this essential set of workers maybe prone to government regulation and god forbid, adverse events? Would that not be a big risk to take for largest holding in portfolio? (apart from the fact that margins may not be high nor scope to increase much in the already low paid blue collar jobs in India…would be interesting to see how the margins compare to global counterparts where blue collar jobs are decently paid and respected as well)…

Not intend to question you but rather discuss on this interesting industry. Would learn something from you

You’re very kind . I’ve been working on my position sizing, and the idea is to buy significant amounts when valuations are cheap. Something I’ve learnt from your post on Pidilite, as well as Hitesh sir’s posts on his portfolio thread.

However, I’m sitting on cash that will bring down the allocations at cost over time.

When we think of them as essential service providers, it’s in the context of covid. They employ nearly 20,000 people who service 120,000 hospital beds, and the management is right when they say these people are needed as much as doctors or nurses. Covid safety measures have also brought this to light. Secondly, their frontline employees, both in India and abroad were classified as essential by the respective governments, and were allowed to come in to work during the lockdowns. They were even given a grant by the governments to not let any of their employees go. They stand to benefit from regulations as long as governments prioritise blue collar unemployment as a data point.

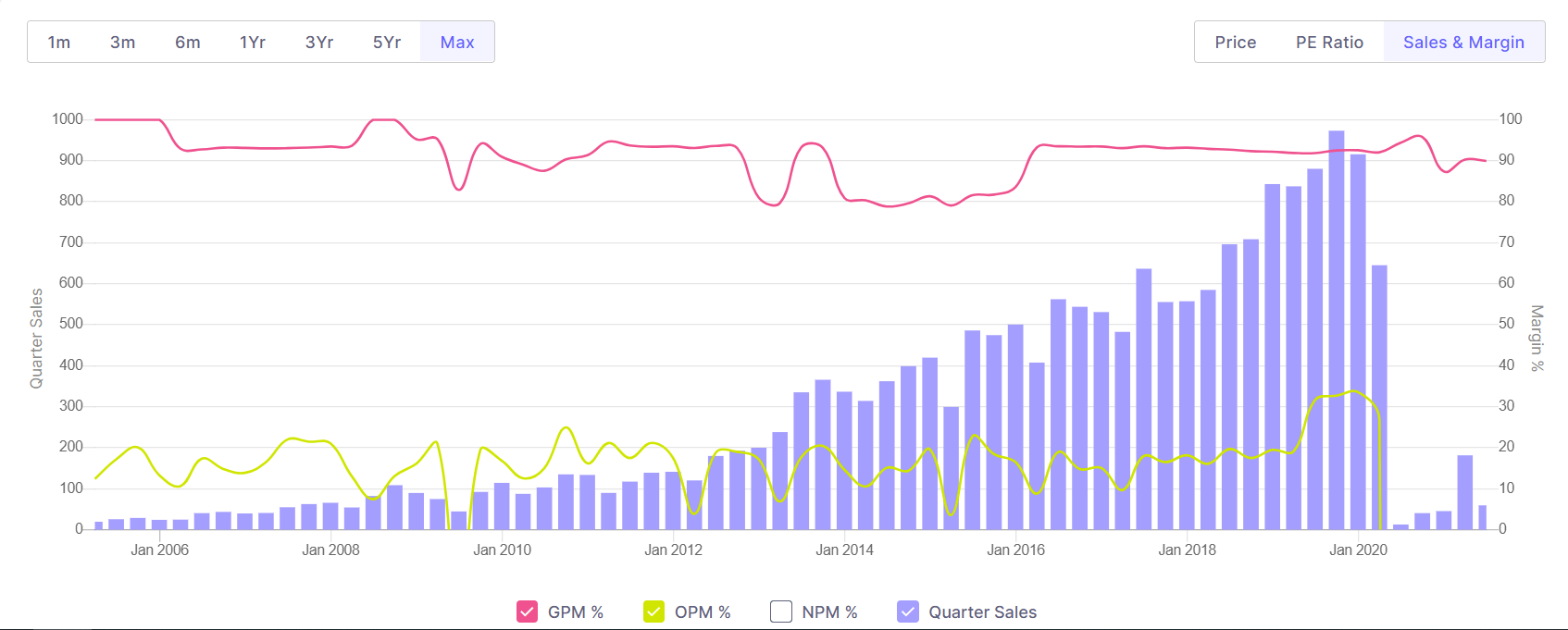

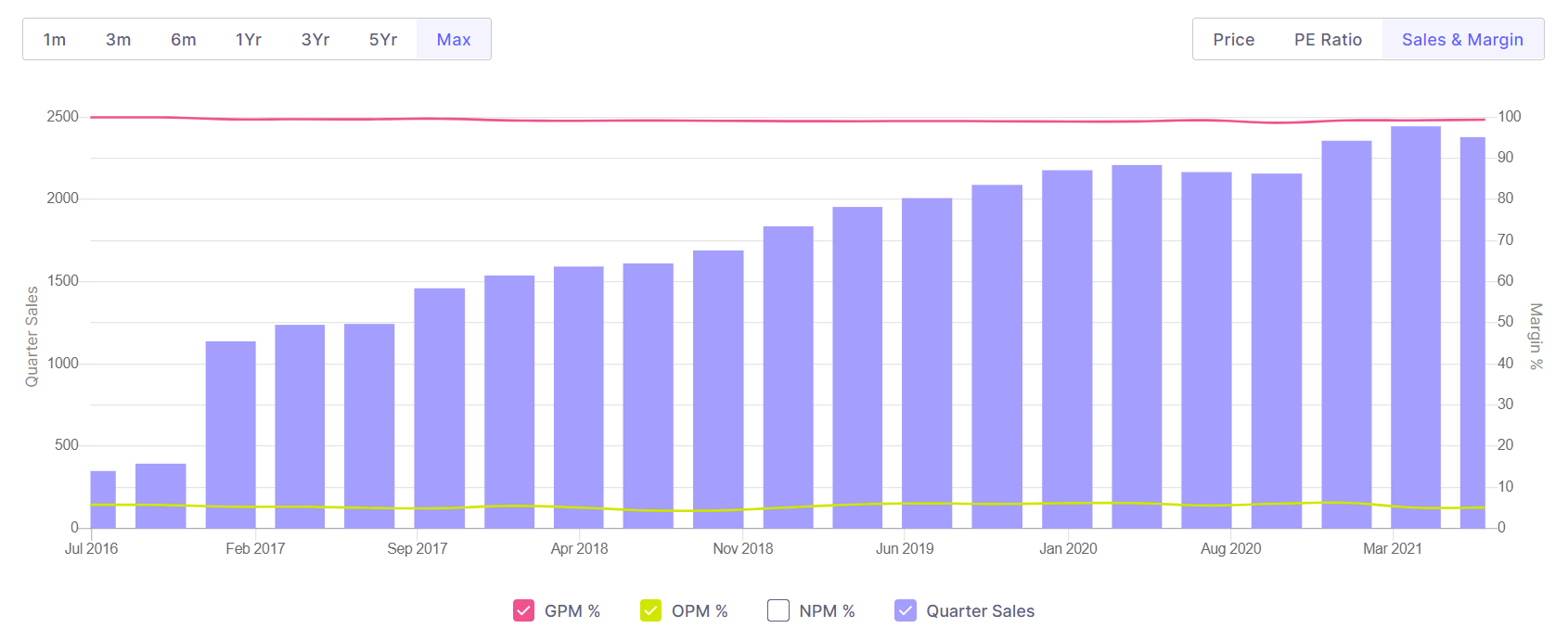

We see the truth of this in their revenues and margins. If we look at the sales and margins of a company they serve, say a cinema like PVR, it’s easy to immediately see the effect of the pandemic:

Covid would have been a nightmare for them, dealing with so many employees, and yet they’ve come out of the two waves so far without a blip. In terms of government regulation, I’ve been reading about how the labour laws in the country are archaic, and there are new codes which are in the process of being implemented that allows more freedom for the formalisation of this sector.

Here’s one read out of many:

The global EBITDA margins are around 4-5%, and you’re right that staffing faces a lot of competition and there isn’t scope for margin expansion. SIS guides margins of around 5-6% going forward, and the transformation they’re working on is to incorporate surveillance products into their portfolio. I’ve attached a single page from the annual report that explains what they’re working on. They aim to get 20% of their EBITDA from products/solutions rather than services, by FY25.

As they’re present across the country, and as you’ve experienced in your office, the management spoke about how they’ve got sticky customers who tried local providers and yet came back to them. After covid one also wonders how many local security staffers / facility management providers have survived. SIS’ plan is to grow organically over the next five years and push their market share from 5% to 15%.

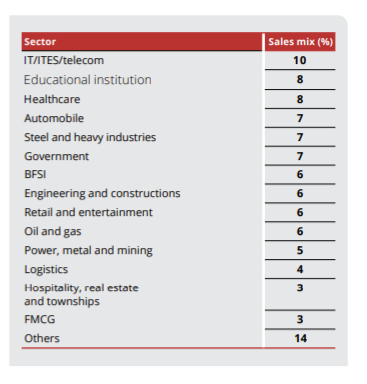

Please feel free to post your thoughts, you’re always welcome. This is a really interesting business, and we would need multiple posts to have a conversation on all of its verticals. They’ve become bigger than just being security staffers. Some other points of interest:

Only 38% of their revenue comes from security solutions in India.

Their facility management is flexible, and they cater not just to malls, but events like sports and concerts. The latter have been depressed by covid and would bounce back after the world opens up again.

They’re diversified even within each vertical. Here’s the breakup amongst the security solutions:

Would definitely recommend reading the annual report, simply because it’s so unique

Interesting to note that their margins is similar to global counterparts despite the fact that blue collar jobs in India are lowly paid. Some points I would think on -

Is SIS a win-win for their main stakeholder - the labourers/essential providers or do they feel they are exploited?

Do more and more type of blue collar workers want to be a part of SIS and see them as enabler (like plumbers/electricians etc. etc.) or do they want to remain independent and see them better that ways - this can be suggest stronger runway of growth and expansion to adjacencies in future

Big facilities need workers in lump and hence the need for SIS…but like in most business, the longevity, stability and profitability of businesses depend on their direct customer reach…a B2C model compared to a more B2B model of SIS right now…do they have that vision or even scope …is that a market today or tomorrow or in western markets how has B2C played out? For example Urban clap provides such B2C platform for various blue collar jobs…

Would be good to know your reason for choosing SIS over Teamlease/Quess corp. How do their revenue/margins have fared priori to covid and during covid as compared to SIS.

Regarding products & solutions - It will be interesting approach by SIS to track and can present a decent B2C opportunity as well here with some product lines. However, the competetion from technologically much better placed companies can be intense…from the likes of Hitachi, ABB, Siemens, Johnson controls and even Indian consumer durables players would foray to this segment once the market opens up. I read once even RIL intend to have home automation and security products in future. So this space would not be easy and is not their strength area…just a thought

As always, thank you for the wonderful break down of your portfolio. I am add a few shares of SIS, BSoft and Caplinpoint based the information here and will continue to add.