I don’t understand the comparison. Adani’s businesses have grown through tremendous amounts of debt, allegedly illicit transactions and favourable policy outcomes (although the last one holds for almost any industrialist in the country at some period in time).

Here are two articles which highlight this:

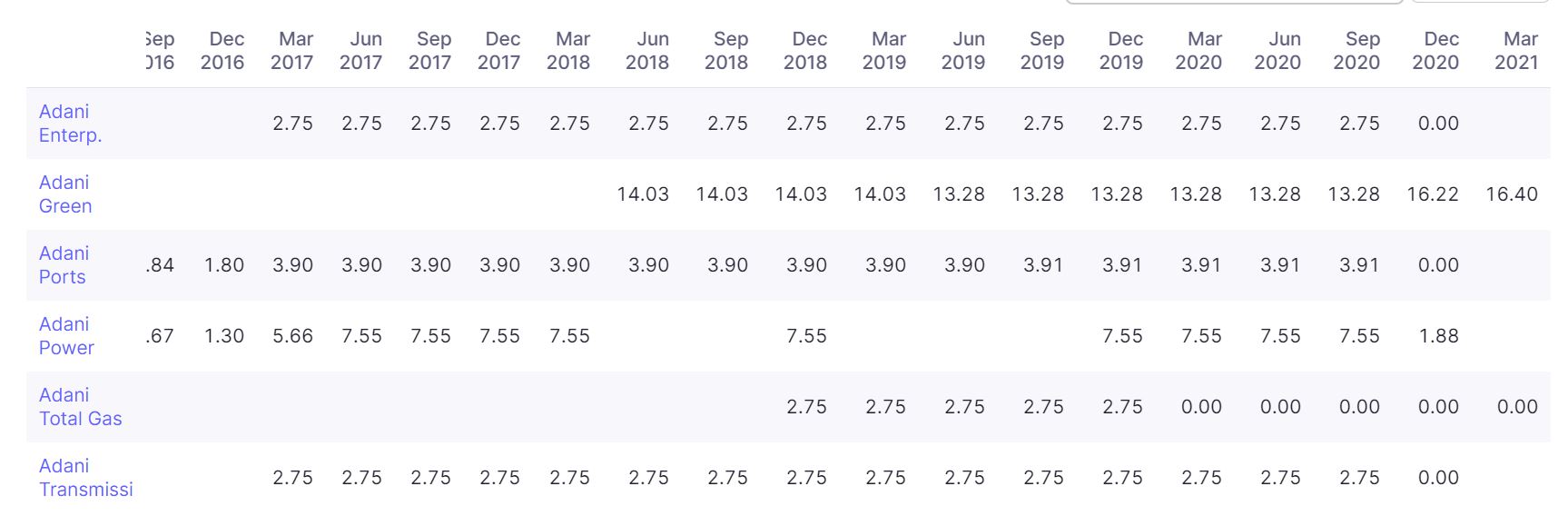

Both are great reads, and the second one highlights the trail of the alleged fraud which ends in companies owned by the Adani family, based in Mauritius. Mauritius is a recurring theme, with four foreign investors being registered to the same address. Here are the holdings for one of them, and it’s suspect that they don’t hold any other listed companies:

Their website http://www.untrin.com/ is equally shady and doesn’t look anything like a fund holding a stake worth 33,000 crores.

In terms of valuations, how many years of growth has the market priced in?

| Company | P/E | Price to Sales | P/B | Debt/Equity |

|---|---|---|---|---|

| Adani Enterprises | 158 | 4.31 | 9.91 | 0.89 |

| Adani Total Gas | 360 | 102 | 89 | 0.24 |

| Adani Green | 967 | 65 | 92.4 | 10.8 |

| Adani Transmission | 140 | 17.2 | 19.2 | 2.89 |

| Tata Power | 24.5 | 1.06 | 1.55 | 1.42 |

I’d also like to leave this wonderful comment made by Hitesh sir in 2013:

Tata Power is trading at reasonable valuations; they’ve gradually ramped up the various offerings classified as renewables, and walked the talk of moving away from coal power and dealing with transmission and distribution. The investment thesis is not just the renewables portfolio, but also the increased efficiency in the utilities business (seen by the 25 year contracts across the Odisha DISCOMs and reduction in AT&C losses post takeover).

A secondary long run thesis revolves around charging technology, and Tata Power could be a dark horse in this regard. I want to point out that this has many IFs and cannot be the main reason one invests in the company. There is already a case for upgrading existing distribution systems in India due to high losses of 16-22% compared to the global average of ~2-5%. A report on the charging infrastructure highlighted how varying levels of EV adoption via home charging would put a higher amount of stress on the local grid. Tata Power has already worked on this through chargers in Mumbai, and are uniquely placed to take advantage of the ecosystem given their exposure to Tata Motors and the grid.

I don’t want to push the last paragraph as the primary investment thesis but rather an afterthought, given how early/forward looking it is. The risks are whether they’re able to continuously bring down the debt/equity (already down significantly from last year), what the Odisha picture looks like after a year of operations, whether they’re able to succesfully divest the legacy business, whether Mundra will continue to bleed, and whether they lose key contracts to the Adani group.