What a wild month of volatility! Portfolio saw a peak drawdown of ~20%, and is currently down 15% from all time high. I have used this as an opportunity to add fresh cash to the portfolio, and my strategy is to trim positions that I expect will see a weaker Q4 YoY, and raise weight in companies that should see a strong few quarters ahead. With this in mind, I’ve made the following changes:

-

Bought more Infosys for the first time in almost a year. Infy and TCS have seen strong high double digit earnings growth in FY22, and have been rated their highest multiples in over a decade by the market. It remains to be seen whether trailing multiples will drop back to the range of 24-27 once growth reverts to the mean. With RM inflation affecting margins in different sectors and the possibility of a few quarters of elevated crude, one also wonders if IT will be back in fancy during the next sector rotation.

-

Have been adding Deepak Nitrite slowly through an SIP. Valuations have cooled, but Q4FY21 was their best quarter in 3 years. I’d be surprised if they manage to beat the EBITDA margins from last March, and I think one will get a better opportunity to add after quarterly results. However, at an FY22E PE of 24.7, valuations are very reasonable, and I’m happy to add slowly on falls.

-

Have trimmed Sandhar at 245. I expect them to de-grow about 15% YoY, and the thesis here is contingent on scale up of the 5 new plants. One was commissioned in December, but the remaining are yet to be commissioned. Street expectations were for the semiconductor pressures to ease in June 2022, but we’re yet to see if this will be affected by sanctions on Russian neon.

-

Was stopped out of Filatex at cost. Re-entered at 110, with 2% of the portfolio. They benefit from a high crude environment, but since the thesis is dependent on a successful rPET model, I’ll scale slowly once the pilot runs are complete.

-

Krsnaa hit a stoploss at 629. Recovered losses by re-entering at 550. At this price, it’s now at 16x FY23E PE. I’ve raised allocations from 4% to 6.2%, and will add more on execution.

-

Raised weight in AB Capital. I didn’t think I’d see it at 100 again, and they’re on track to deliver their FY24 targets ahead of schedule. RoA and RoE have steadily been improving, and should be at ~15% by the end of FY23.

-

I was tempted by Ugro’s fall to add more, but they’re now moving to quarterly disclosures. I’m happy with my allocation.

-

Cash forms about 10% of the portfolio. A part of that has been kept aside for Sandhar and more Deepak Nitrite, but a number of companies outside the portfolio are looking attractive. I’m currently studying Piramal, revisiting Lux, and one spoken about below.

I’ve initiated a tracking position in a company that completely baffles me: SJS Enterprises. It’s largely an auto-anc, but not really an auto-anc, since it produces dials and logos that go onto vehicles and consumer durables.

Zygo23554’s wonderful post on Suprajit and auto-ancs got me interested.

Very few auto-ancs command high EBITDA margins, and RoCEs of above 15%. Sona Comstar looks to be the best in the bracket, with margins of 30% and peak RoCEs of 30%. RACL has also delivered margins of 20% and similar return ratios.

With this in mind, SJS immediately stands out as not belonging to the average auto anc basket:

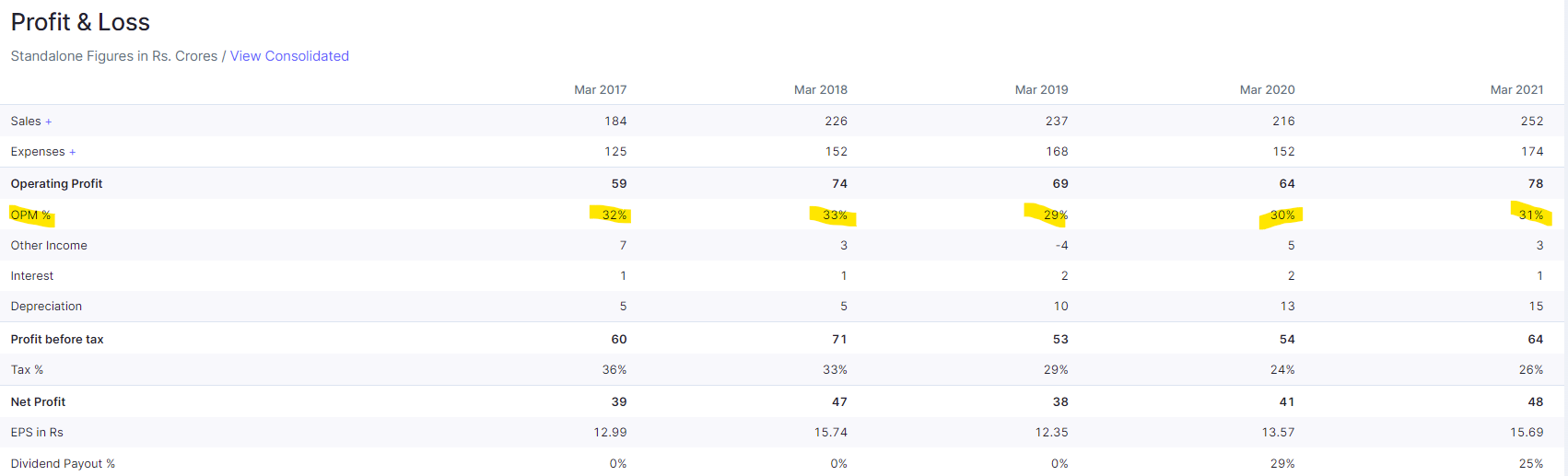

What’s more impressive is that they’ve managed to keep margins high through the downcycle starting in 2018. Their standalone business delivered 30% margins through FY22, through the RM inflation and tough environment others have reported. How have they managed to do this while producing parts that have no right to command 30% margins prima facie…

What’s even more impressive is their RoCE profile:

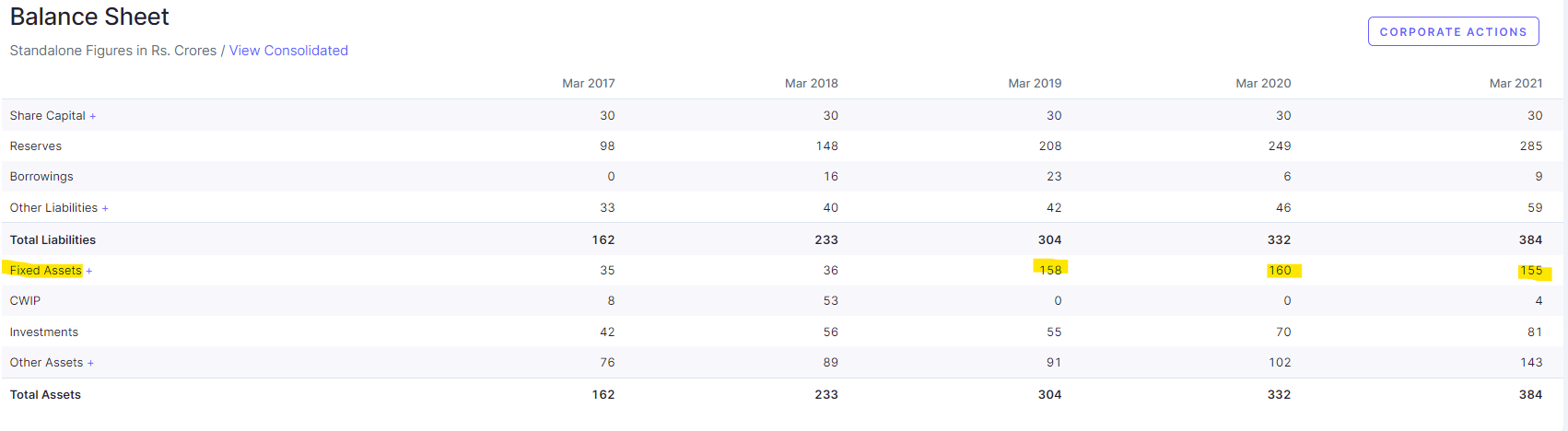

This looks to have taken a beating following 2018, but we’ve seen the margin profile remain robust in the same period. A quick glance at the balance sheet shows us why the RoCE has fallen:

The reason for the ratios falling in 2019 onwards is due to their fixed assets going from 36 Cr. → 158 Cr., where they moved to a new facility outside of Bangalore.

What am I missing? How are they able to command such high margins through various macro settings?

I’ll eventually write a post on the forum after I go through its red herring.