On weekends, I usually spend my time reading about new companies. However, I think a fair journal should also include the numerous companies that don’t make it to the portfolio.

Here’s one such name that made it to the discard pile:

- Vivo Biotech:

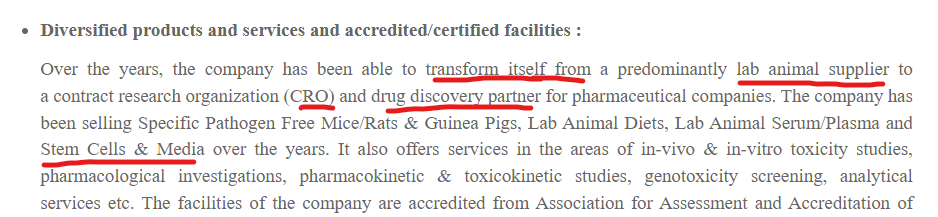

Here’s a 100 Cr. company that’s made margins of >20% for the last few years, and has steadily grown its bottom line. A quick glance at the annual report would capture the attention of anyone who’s invested in pharma:

Exciting right? A micro-micro-microcap that’s present all the right themes, making margins of over 40%! Here’s where it starts to unwind:

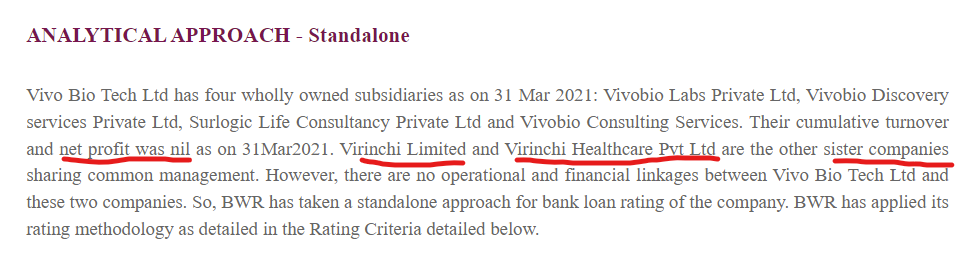

- Is a sister company to Virinchi Limited:

To those readers that are out of the loop, fellow members at Valuepickr have urged caution regarding this group:

Some former Virinchi Hospital management now work for Vivo Biotech.

Inviting comments from those that have studied this further ![]()