I have a few weeks off, and due to the incessant rain, I’ve been indoors expanding my circle of competence. This week’s readings were on understanding NBFCs better, and dismantling every aspect of the EV future in India. Avendus has a brilliant deep dive on EVs which explains the interplay between policy, industry, and technology in every single part of an electric vehicle. I’ll write a longer post after I’ve studied every single company in the space; it’s still early days in this theme.

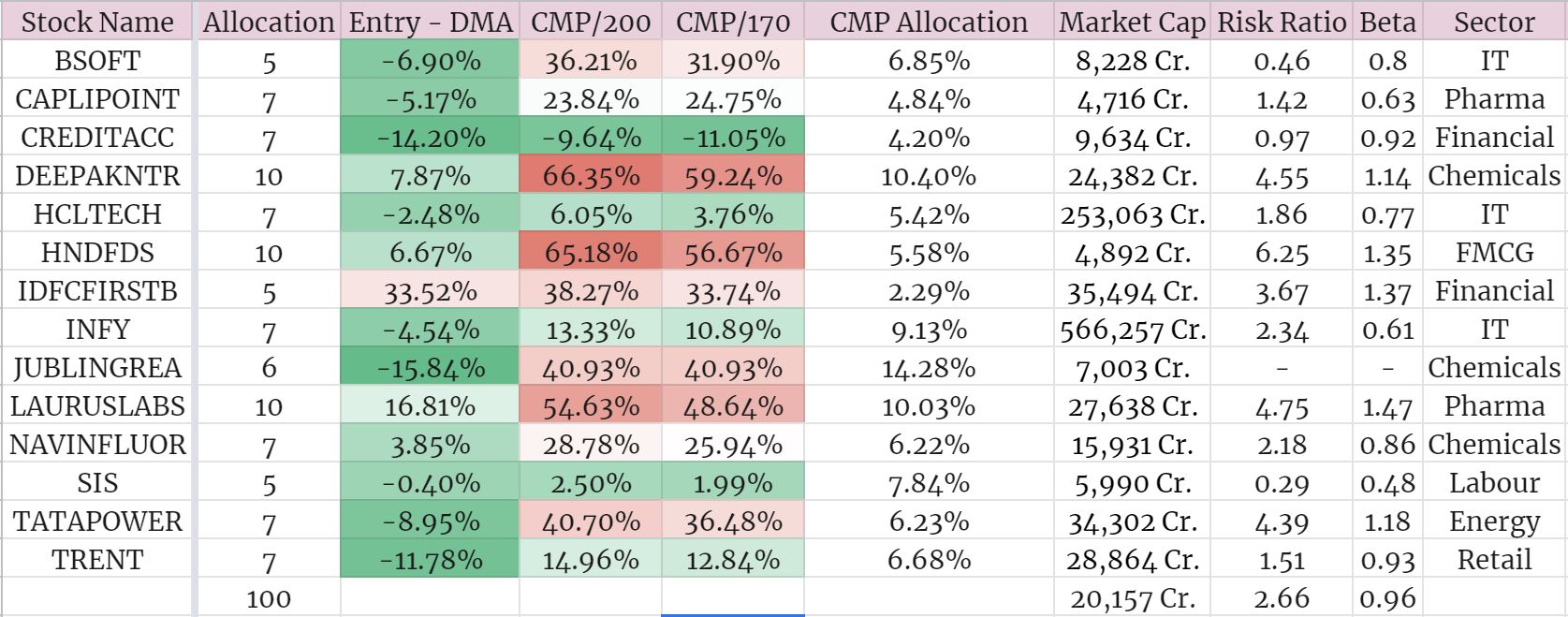

On the portfolio front, I’ve divided my cash position into 24 parts and my strategy is to SIP every month for the next two years. I pick up more of the stock that’s closest to the support line, but try to spread it out in a way that makes sense. Should there be an opportunity at really attractive valuations, I invest a much larger tranche, as seen in Jubilant Ingrevia. At the end of a year the allocations will align.

Some transactions from this quarter:

-

Picked up a tranche of CreditAccess Grameen at 600 levels, almost a 20% discount from my first entry. Sent AU Small Finance Bank to the family portfolio.

-

Started an SIP into IDFC First Bank.

-

Bought two tranches of SIS, trading at really attractive valuations and the chart looks like the formation of a cup/handle pattern from the first week of April (The rest of the chart is disgusting). Happy for this money to be locked in for a long time should things not work out.

-

Hindustan Foods being range bound for the last few months has been wonderful, allowing its 200DMA to catch up a little to current prices. Usually rallies just before results, I’m hoping to pick some more up.

-

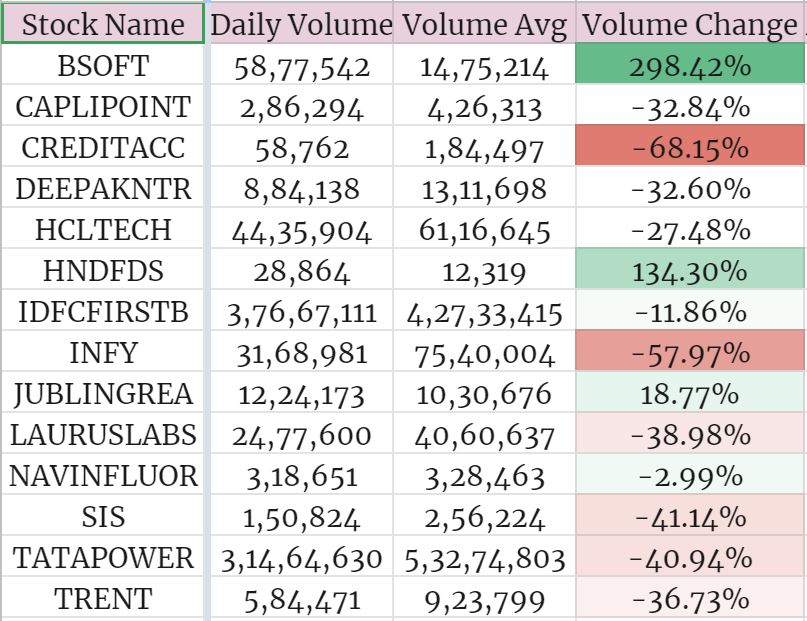

Birlasoft broke out of its 52W high with huge volumes. There’s no reason to exit in a hurry, I’ll only replace if there’s a better company in the space. I’m yet to fully study the IT sector.

-

With Trent, the goal is to evaluate the business again once we have details about Nykaa’s reported IPO. That’s a company in the space that I’ve been eyeing for a long time, but can’t say anything without concrete details regarding valuations, etc.

With the smallcaps, I was wrong in my post from early May. After playing it defensive, I watched KMC Speciality and BCL Industries double. No regrets though

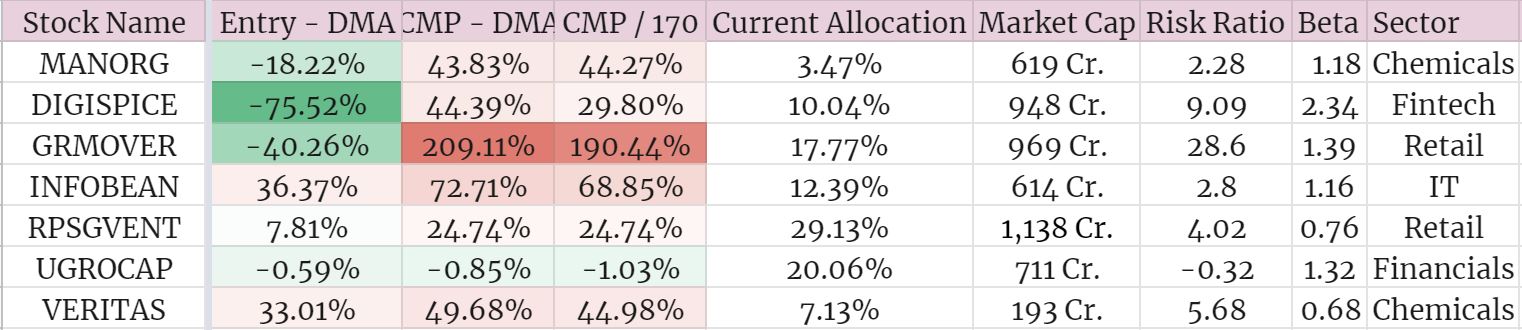

I’ve cheated a little. RPSG Ventures should technically be in my main portfolio, but I’ve decided to follow my rule of tracking the smallcaps over an extended period of time before bringing them into the core portfolio. With Ugro, I was discussing the idea with a friend who works in a VC, and this coincided with the discussion here at Valuepickr.

-

Instead of allocating 10% to each company, I’ve decided to raise the allocations in both Ugro and RPSG to reflect conviction.

-

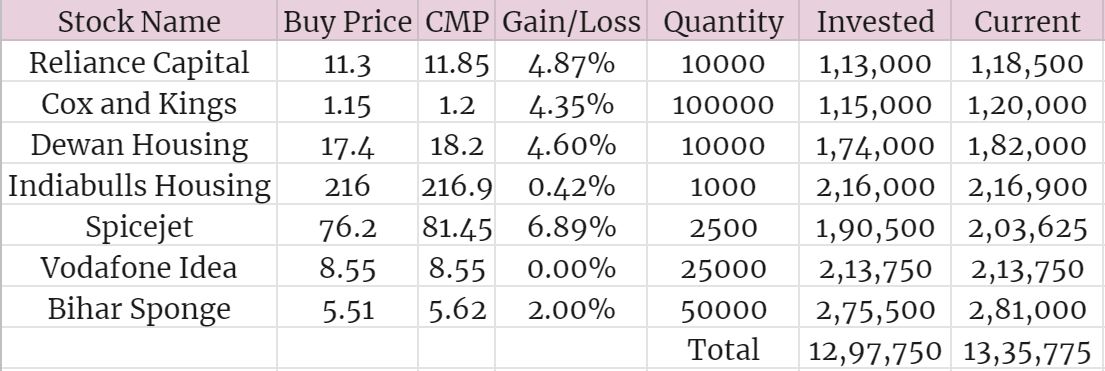

I’ve withdrawn my initial capital from Mangalam Organic, Digispice and GRM Overseas. It’s astounding that GRM still hasn’t crossed the 1000Cr. mark despite running up 24 times since March 2020 lows.

-

The goal with all of these companies (except for RPSG and Ugro) is to continue to take initial capital off the table, giving me a long tail of essentially free smallcaps. If I hadn’t sold KMC and BCL, there would be two more in this list, but lesson learnt.

Some company highlights this quarter:

Tata Power

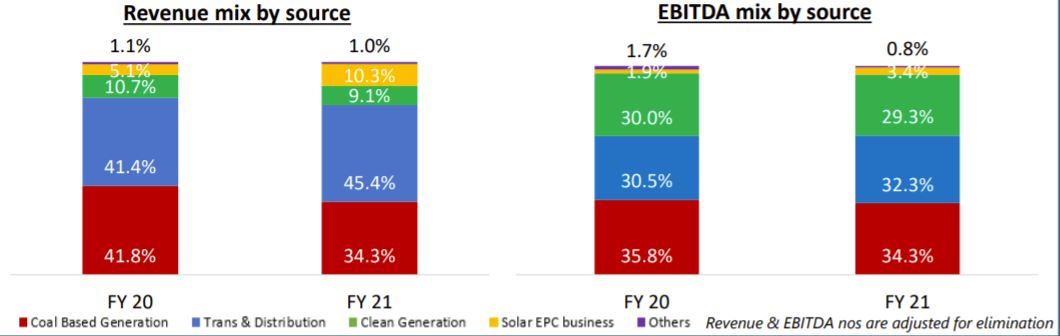

I’m surprised that there isn’t a Tata Power thread on this forum, but I haven’t seen any mentions of people following the earnings calls, so I’ll post my own notes from this quarter. The simplest investment thesis to Tata Power is seen by looking at their revenue breakup. A few years ago, they decided to move away from coal power generation, and focus their strategy towards scaling up their renewables, transmission and distribution businesses and making them more effective. At the same time, they’re trying to bring down debt and turn the company around.

Concall Notes

-

Through acquisitions in Odissa, they’ve gone from 2.6million customers in FY20 to 12million customers in FY21 and have a target to triple the current revenues in Odissa by FY25.

-

Renewables grew from 88Cr. to 175Cr. this year. Focus on solar EPC, rooftops and pumps. Tata Power Solar revenues grew from 2144Cr. to 5119Cr. this year.

-

Solar EPC orderbook of 2294 Cr. in Q421, total orderbook of 8742 Cr.

-

Rooftop revenue grew to 300Cr, orderbook of 600Cr.

-

Solar roof digital campaign → 5Cr. impressions and 41,000 leads → 43 Cr. order value.

-

Solar pumps: 6500 pumps this quarter, 13000 pumps in FY21.

-

Capacity doubled for solar cell/module manufacturing in Bangalore.

-

Reduced debt by 7500Cr by divestment / fund raise. Still planning to get rid of coal mines in Indonesia, other countries.

-

Interest cost down to 7.4% from 8.3% last year.

-

Debt/Equity down to 1.4 from 2.0 last year.

-

EV charging points at all important railways in Mumbai. 175 charging stations this quarter. Total 456 chargers for 4W, 80 ultra high capacity bus chargers in Mumbai / Ahmedabad.

The utilities/distribution framework will become a pillar of the EV adoption in the country. Most transformers can’t handle the additional load that EV chargers (and home chargers) bring, and will need to be upgraded/separate transformers will have to be installed.

A discussion on transmission/utilities would be remiss without mentioning the Adani group, but the following articles convinced me of giving them a miss regardless of the returns.

Jubilant Ingrevia

I’ve written about my concerns regarding the Jubilant group’s approach to regulations in its thread. I have no doubts about the company’s ability to scale up over the years, but I’m going to have trouble sleeping at night knowing there’s a regulatory sword hanging over its head.

The option that makes the most sense to me is to slowly book profits in a way to take my initial capital off the table. This way the regulatory risks will only affect the profits, and I can then happily sit on the company for years. I’m still waiting for the earnings meeting and the annual report.

) . Cheers

) . Cheers . That mindset has got me through this volatile year(and volatile past decade too lol) and I’d suggest applying it too since there will be periods of huge panic over the next few quarters. I’m not a fan of entertainment/travel/auto etc too…however, if they do get beaten down to crazy low levels they could give a no loss opportunity somewhere down the road when the other sectors get fully priced in. Also, I’ve realised I’m only not a fan of a sector until I study it thoroughly and then I end up becoming one (happened recently with commercial real estate… something I always avoided)

. That mindset has got me through this volatile year(and volatile past decade too lol) and I’d suggest applying it too since there will be periods of huge panic over the next few quarters. I’m not a fan of entertainment/travel/auto etc too…however, if they do get beaten down to crazy low levels they could give a no loss opportunity somewhere down the road when the other sectors get fully priced in. Also, I’ve realised I’m only not a fan of a sector until I study it thoroughly and then I end up becoming one (happened recently with commercial real estate… something I always avoided)