I wanted to highlight two pieces here on VP that really resonated with me this month.

These are wonderful posts on valuations, wealth creation through re-ratings, and conviction during periods of underperformance. It made me think of past exits due to headwinds, and understand the pitfalls in my portfolio better.

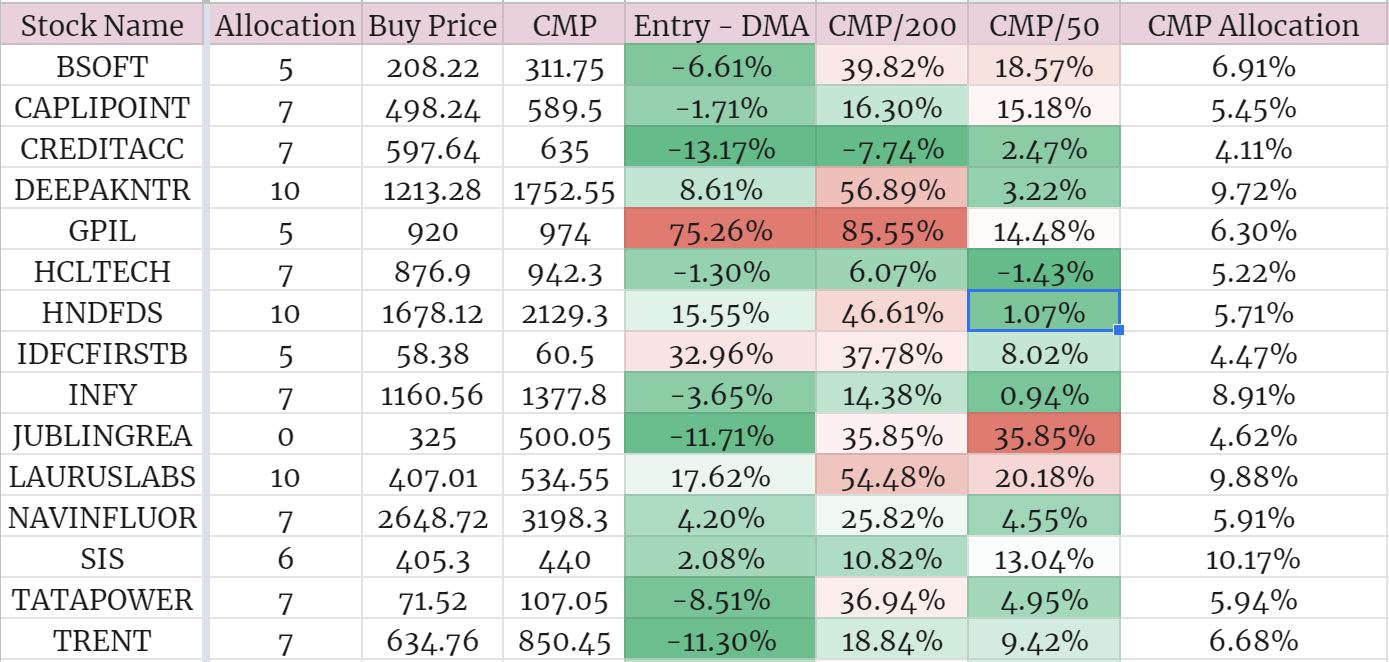

I hope the SIP method is clear from this. Even if the current price is far higher than the daily moving averages, the overall buy average will be very close to the support lines. The next tranches will be of Tata Power, Trent and CreditAccess Grameen towards the middle of the month.

Jubilant Ingrevia has been a really difficult stock to part with, but I used the run up today to withdraw my initial capital. I’m sure there will be a lot more value unlocking as the results, annual report and AGM shed light on the business, but now I’m happy to watch on without fear. Once I have clarity on the environmental clearances in 2022 and the effect of the NGT orders, perhaps I’ll add more then. Good ESG metrics are important to me, and a company that’s high on the wishlist at the moment is Vinati Organics.

I’ve put the Ingrevia allocation into GPIL which was down almost 5% yesterday. The wonderful thread here covers the investment thesis.

The most expensive holding in my portfolio is Hindustan Foods, but my initial tranches were bought when it was inline with its historic multiples, and reasonable compared to Varun Beverages. Navin Fluorine is expensive due to a tax rebate they got in March 2020, which got discarded from the TTM calculations after this quarter’s results. I regret not buying IDFC First closer to book value at the start of the year. This said, I like valuing a company by comparing the market cap by the opportunity size, and that offers me some comfort in Hindustan Foods but everyday I wish it were cheaper.

What I haven’t mentioned in this thread is how I’ve been splitting strategies with my family on sectors we like. My mom has been accumulating ITC, IOLCP, Galaxy Surfactants, Borosil Renewables and Vaibhav Global among others. Perhaps I’ll ask her to share her experience in the markets here on VP as some of her holdings are from the 1990s, and include some tragedies such as Opto Circuits and Photoquip. I’ve also subscribed to the Quantamental smallcase, and will invest after opening up an account with a new broker.

It’s annoying me that the wealth destruction portfolio is creating wealth. This looks like a smallcap market that will generate returns in the short term even if you invest blindly, and that’s making me uneasy.

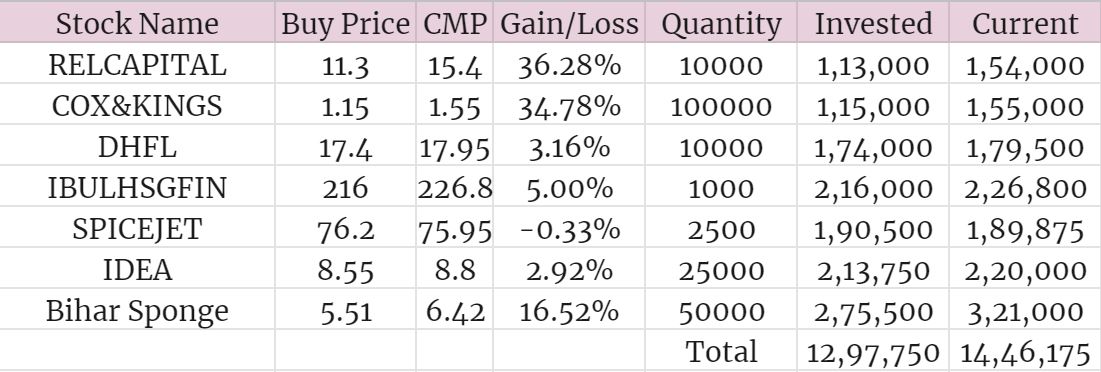

To end May on a positive note, we’ve sold most of our GRM Overseas holdings. The investment thesis was purely an undervaluation play, and in six months it has gone up almost ten times from the first tranche. A share of the profits have gone towards much needed renovations at my mom’s house, and a part of it to covid relief and charity. The small remaining holdings will be kept for the bonus. ![]()

At the same time, I’m baffled and see it as nothing but luck. I’d never have imagined six months ago that across all the holdings, this would be the company the market chose to reward.