Chennai Petroleum: An Analysis of Financials and Market Potential

CMP -510 Market cap - 7500 crores

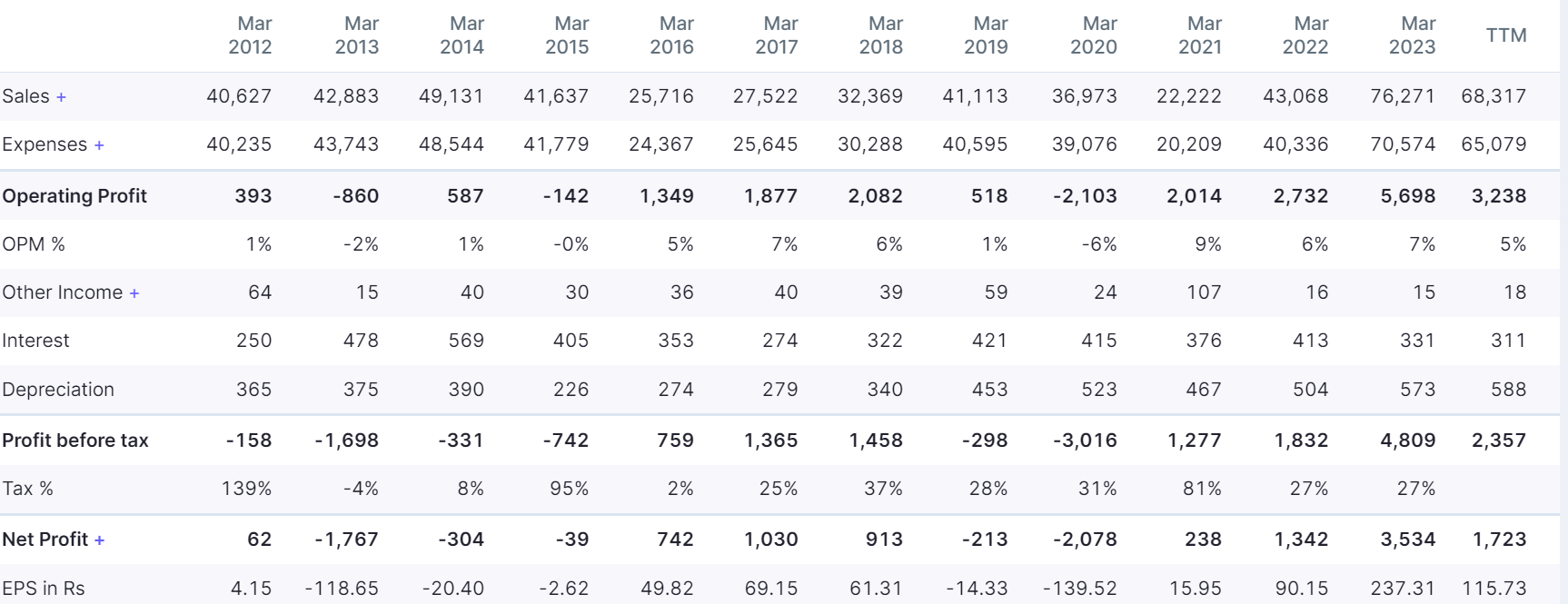

Financial Performance: Chennai Petroleum in Numbers

Chennai Petroleum has exhibited a strong financial performance in recent years. As of the latest financial year, the company’s price-to-earnings (PE) ratio stands at an attractive 4 times, indicating that the stock is undervalued in comparison to its earnings.

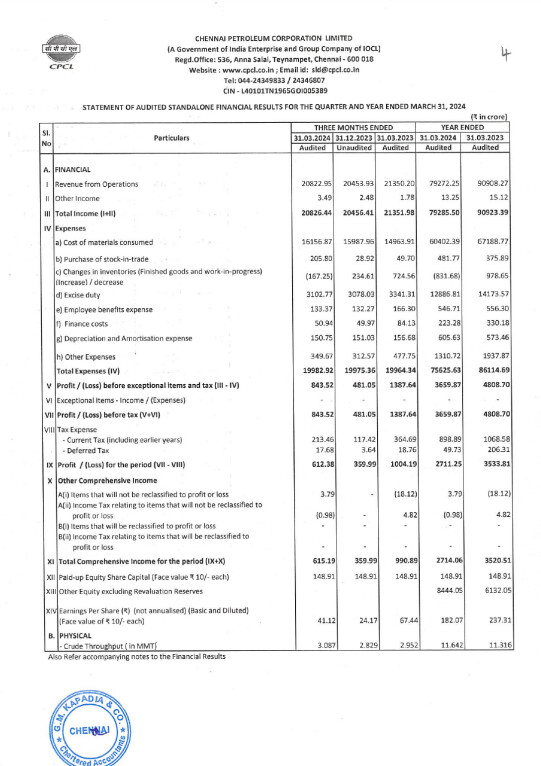

The market capitalization of Chennai Petroleum currently stands at 7,500 crores, reflecting the company’s size and market value. With sales amounting to an impressive 76,735 crores and a net profit of 3,534 crores(FY 22-23), Chennai Petroleum has proven its ability to generate substantial revenue and profitability.

The earnings per share (EPS) for the financial year 22-23 stands at 237, indicating that each share of Chennai Petroleum is generating substantial earnings.

Operational Efficiency and Debt Reduction

One of the key indicators of a company’s operational efficiency is its capacity utilization. Chennai Petroleum has achieved a remarkable capacity utilization rate of approximately 113% for the year, which signifies the effective utilization of its production capabilities.

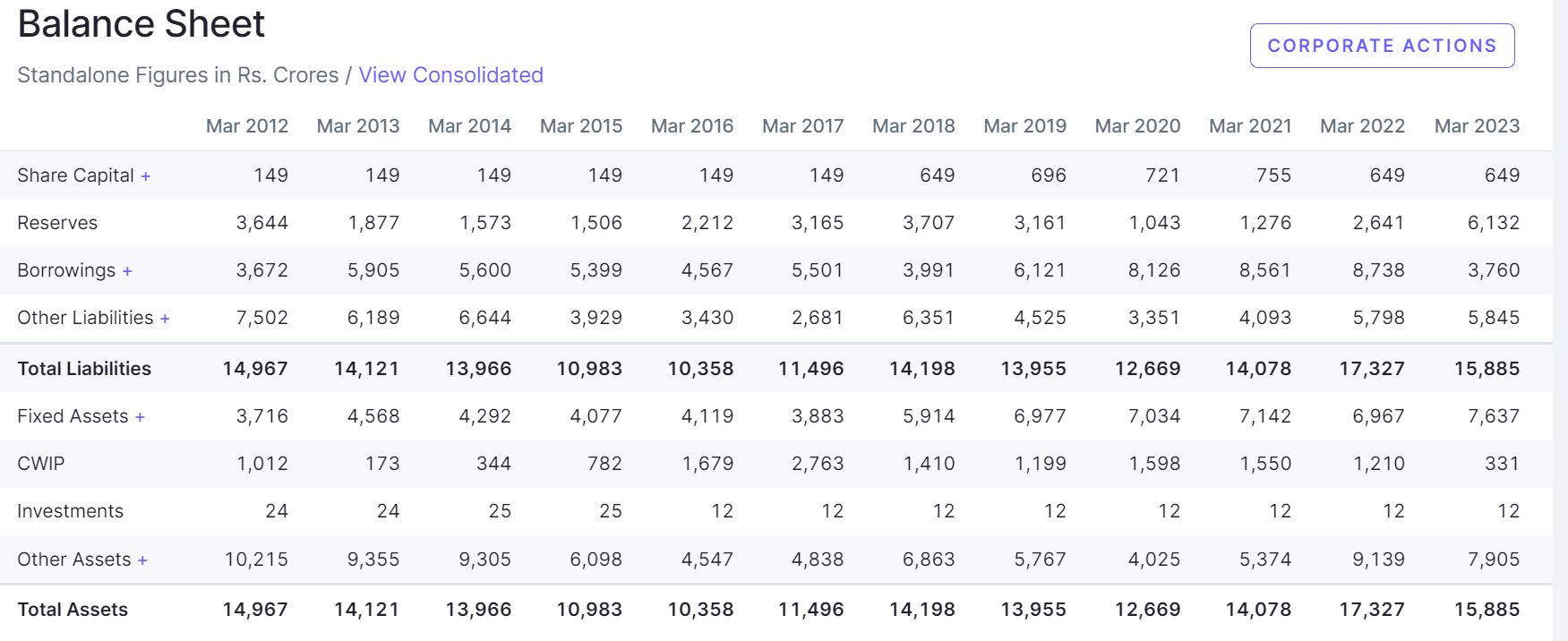

In addition to operational efficiency, Chennai Petroleum has also demonstrated its commitment to reducing debt. During the year, the company successfully reduced its debt from 8,500 crores to 4,200 crores.

Based on the Oil and Gas Journal published in 2022, NCI of CPCL is 10.03, making it the fifth most complex refinery in India and second most among IOCL Group Refineries.

Gross Refinery Margins and Market Potential

Gross Refinery Margins (GRM) play a crucial role in determining the profitability of petroleum companies. Chennai Petroleum has consistently achieved GRM in the range of $10 to $13 for the year, indicating its ability to generate profit from refining operations.

Revenue Breakup and Competitive Advantage

Chennai Petroleum enjoys a competitive advantage in the market, primarily due to its diverse revenue breakup. The company offers a wide range of products such as high-speed diesel, motor spirit, naphtha, and other products like Paraffin Wax, Hexane, Micro Crystalline Wax (MCW), Sulphur, Petcoke, SN-150 Base oil, JP-5 & JP-7.

Chennai Petroleum Corporation Ltd. (CPCL), Manali, has recently commenced the supply of aviation fuel of Jet Propellant-5 (JP-5) grade for the Indian defence forces through the Chennai–Bengaluru oil pipeline (CBPL).

JP-5 is a high flash point fuel and the CPCL refinery is the only one to manufacture this grade in the country. Till now, the fuel was being sent via coastal tankers.

The CPCL, along with Indian Oil, has developed a standard operating procedure for moving the product through the pipeline. It is being sent to the IOCL terminal at Devanagonthi near Bangalore.

Reserves and Free Cash Flow

Chennai Petroleum boasts a healthy reserve of 6,132 crores, which translates to approximately Rs.411 per equity. This reserve not only provides the company with financial stability but also serves as a buffer during challenging market conditions.

The free cash flow (FCF) for the financial year 22-23 stands at an impressive 5,749 crores.

Other points

CPCL is investing in JV with IOCL in which CPCL will hold around 25% stake in the upcoming 9.5MMTA refinery in Nagnipattam which shall mostly be operational in 2 to 3 years.

MOAT

Revenue Mix from around 14 products as shown in their recent 2023 annual report. This will act as the strongest MOAT for the company which help it increase its operating margins.

Compared to peers the valuation of the company is only at PE of 4 & 7000 crores in market cap for a refinery with 10.5 MMTA capacity, 70,000 crores plus in revenue, profitable & debt to equity ratio at 0.54 which servers us an opportunity to look into the company.