First I will try to address the issue that’s concerning most investors is that Chemplast Sanmar Ltd (CSL) has been delisted at 15 rs in 2012 and coming up with an IPO in a bull market at (530-541) rs.

In 2012 Company took a voluntary decision to delist itself from exchanges as the global outlook following the 2008-09 financial crisis has deteriorated. CSL was listed in 1995 on exchanges and delisted in 2012. I could find only 2 Annual reports of the delisted entity(2011 & 2010) from the NSE website and few disclosures from the past.

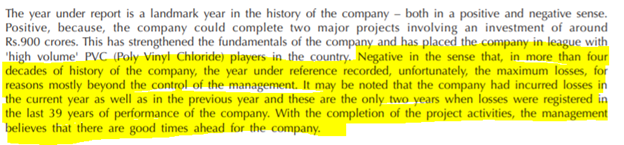

Snippet from 2010 AR:

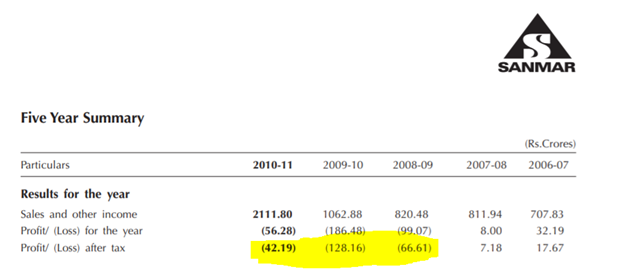

CSL went on to make losses for FY 2011 and 2012.

Financial Summary from 2011 Annual report:

Including 2012 CSL made losses for 4 straight years before delisting itself from exchanges.

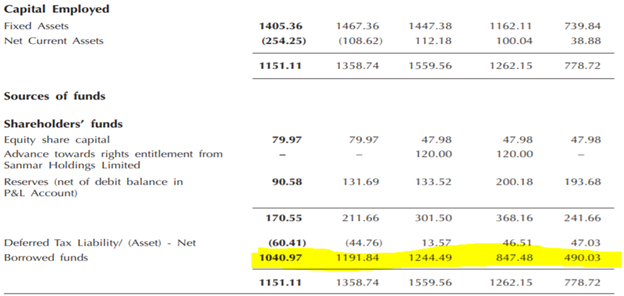

CSL’s Debt/Equity ratio climbed to 6:1 and majority of assets are funded through debt.

Continued losses, mounting debt, and a negative outlook forced the management to take a decision to delist itself and restructure its entire operations.

The product portfolios of the delisted entity in 2012 and CSL in 2021 are significantly different.

The company’s Business segments in 2012 were

PVC where the company manufactured various PVC resins, Company also has Trubore piping systems (which now seem to be acquired by Prince Pipes & Fittings).

Chlorochemicals- Caustic Soda, Chloromethane Products, Silicon Wafers and Refrigerant Gas (HCFC)

Also had other products like industrial alcohol, industrial salts, Company had 7 manufacturing plants. 5 in TN, 1 in Puducherry, 1 in MH. (CSL’s current product portfolio will be discussed later).

Moving ahead with the overview of CSL’s current business and highlights from Red Herring Prospectus:

Overview of the Company:

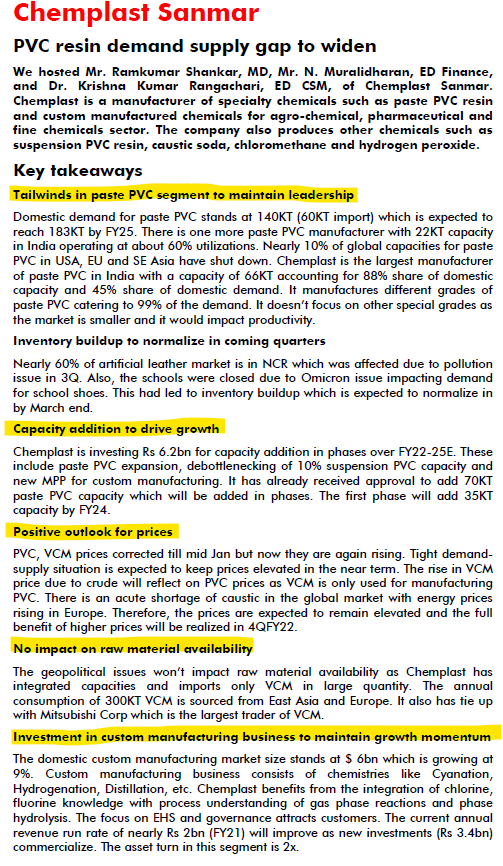

CSL is a specialty chemicals manufacturer in India with a focus on specialty paste PVC resin and custom manufacturing of starting materials and intermediates for the pharmaceutical, agrichemicals, etc

CSL is one of India’s leading manufacturers of specialty paste PVC resin

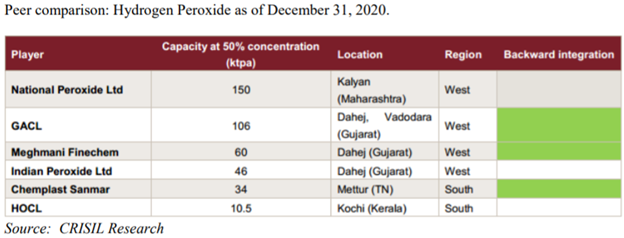

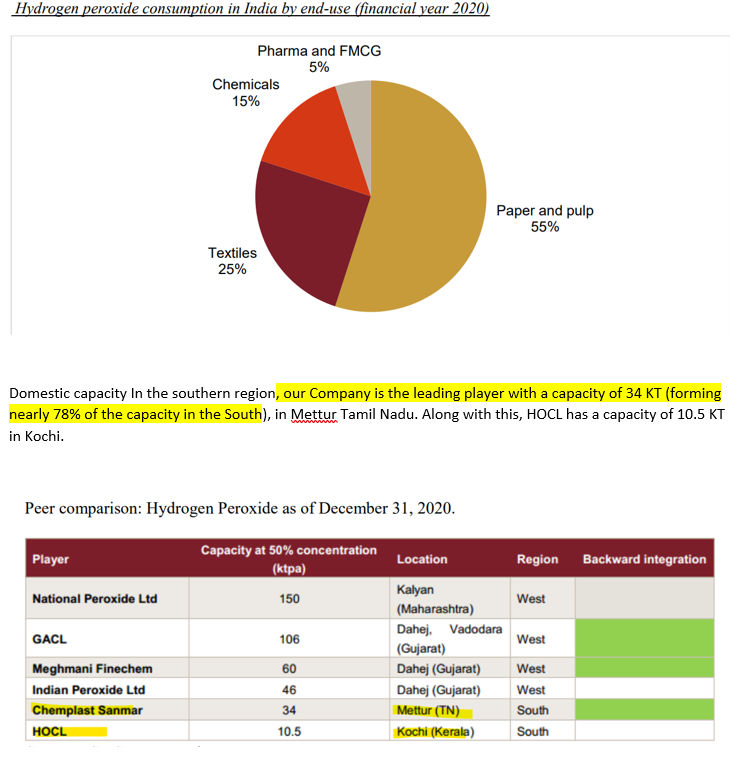

CSL is also the third-largest manufacturer of caustic soda and the largest manufacturer of hydrogen peroxide in the South India region

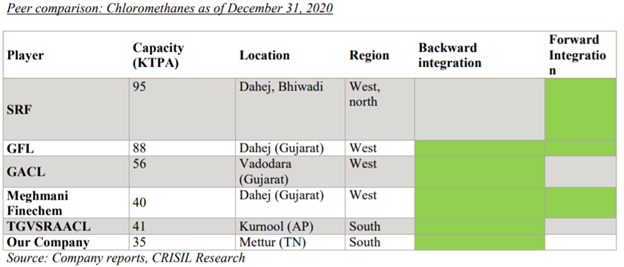

CSL is one of the oldest manufacturers in the chloromethanes market in India.

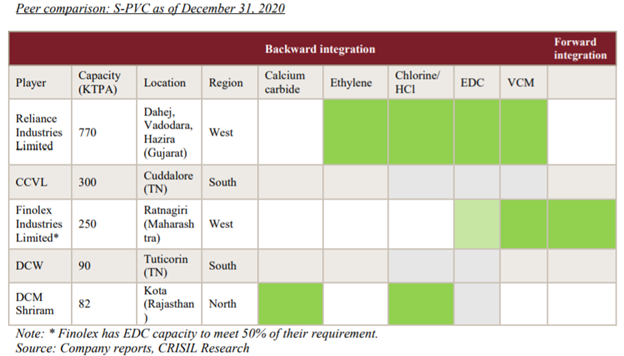

CCVL a 100% subsidiary of CSL, is the second-largest manufacturer of suspension PVC resin in India and the largest manufacturer in the South India region

Products:

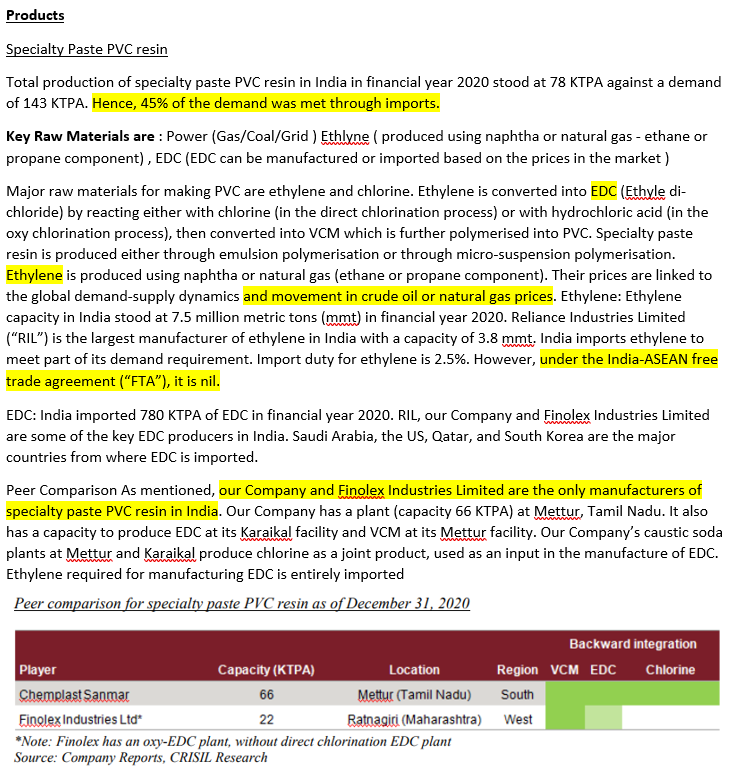

1. Specialty paste PVC resin

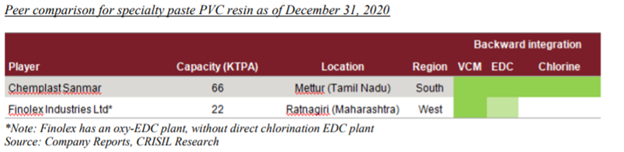

Specialty paste PVC resin is used to make flexible products (such as artificial leather, gloves, tarpaulins, conveyor belts, and coated fabrics). In India CSL and Finolex Industries Limited (Finolex Industries) are the only producers of specialty paste grade PVC resin.

Market size specialty paste PVC is 143 kilo-tons pa (ktpa) in 2020.

CSL capacity 66 ktpa, Finolex capacity 22 ktpa. Total production for 2020 was 78 ktpa and the rest was imported.

Demand is expected to grow 5-7% CAGR between financial years 2020 and 2025 to 182 KT. (CRISIL research)

CSL is planning to add a 35 KT capacity at Cuddalore, which is expected to come onstream in the financial year 2024.

Key growth drivers:

Low per capita consumption(0.1kg) compared to China(0.6kg), western Europe(2.4kg) and other countries

Lack of substitutes

The leather footwear market has significant growth potential

Automotive market recovering sharply

Government initiatives like Make in India to boost investment in artificial leather production

Usage of vinyl gloves rising rapidly post COVID-19 pandemic

CSL is better placed compared with Finolex with better backward integration.

2. Custom Manufacturing

Custom manufacturing is the exclusive manufacturing of non-commercially available molecules for a specific company.

The demand for custom manufacturing catered to by Indian manufacturers is likely to grow at around 12% CAGR between financial years 2020 and 2025, owing to higher penetration of pharmaceutical molecule or compound or API manufacturing

Key growth drivers

India to be a focus region as companies move away from China

Indian exporters to capitalize on global players de-risking their supply chains away from China

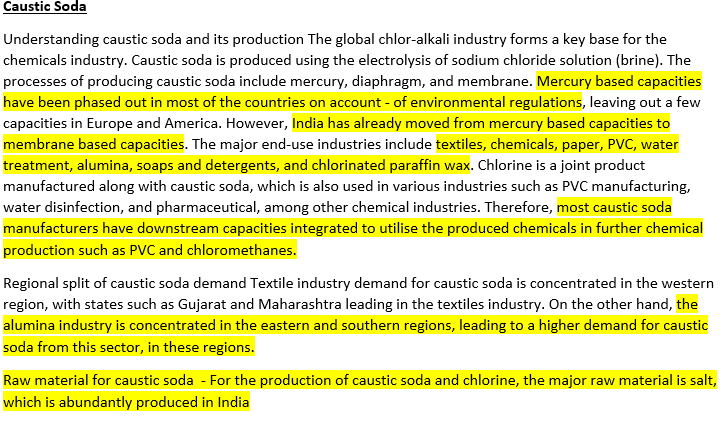

3. Caustic Soda

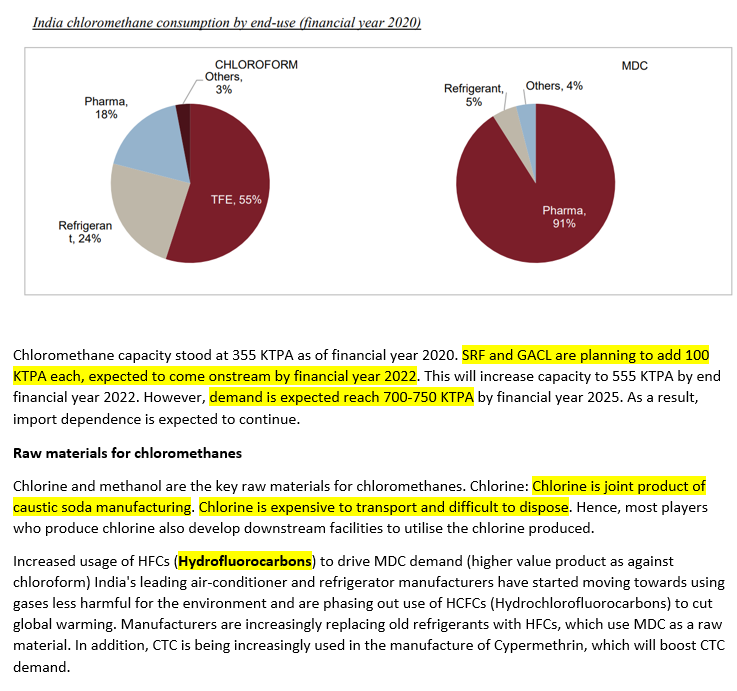

Caustic soda is used in major end-use industries include textiles, chemicals, paper, PVC, water treatment, alumina, soaps and detergents, and chlorinated paraffin wax. Chlorine and caustic soda are joint products and hence most caustic soda manufacturers have downstream capacities integrated to utilize the produced chemicals in further chemical products such as PVC and chloromethanes

Caustic soda demand is also determined by chlorine demand, and hence producers often have downstream integration for both caustic soda and chlorine as feedstock

Key growth drivers here are import duties and increased demand from paper and textiles.

4. Hydrogen peroxide

Hydrogen peroxide is mainly used in the pulp and paper industry for bleaching pulp and deinking recycled paper. It is also used in textiles, electronics, food and beverages, and healthcare industries.

As of the financial year 2020, demand for hydrogen peroxide stood at 320 KTPA. The hydrogen peroxide market has grown at a CAGR of 6.9% between financial years 2015 and 2020, led by growth in the paper and pulp segment, which forms 55% of the overall demand. Hydrogen peroxide demand to log 6-7% CAGR between financial years 2020 and 2025

Since hydrogen peroxide is a local product due to its high transportation cost, most players prefer to supply in their regional markets. CSL and HOCL are the only players operating in the South.

Key growth drivers here are import duties and increased demand from paper and textiles.

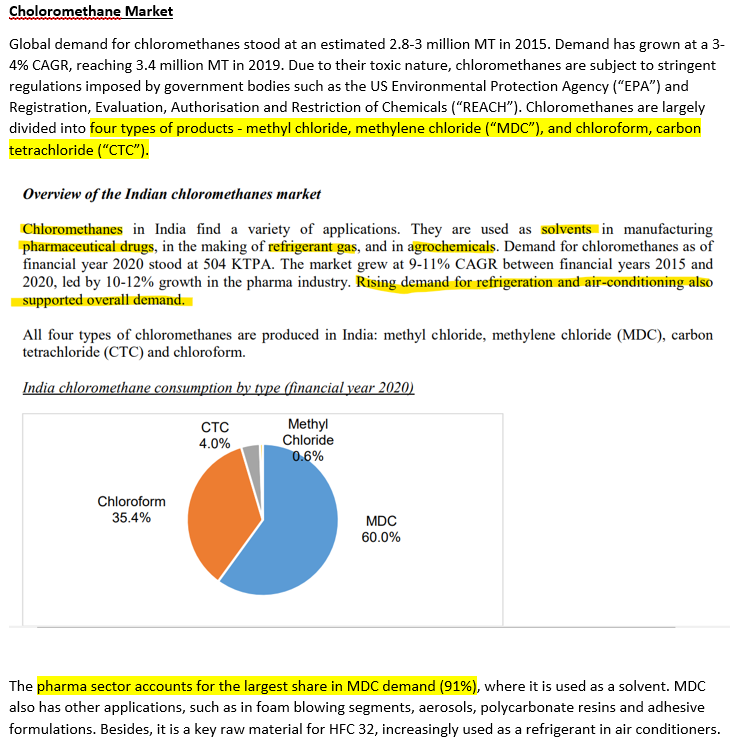

5. Chloromethanes

Due to their toxic nature, chloromethanes are subject to stringent regulations imposed by government bodies. global demand has grown from 2.8 - 3 mil MT in 2015 to 3.4 mil MT in 2019. Indian market size is 504 KTPA and it grew by 9-11% cagr between 2015-2020.

Chloromethanes market to grow at 8-9% CAGR through FY2025

Key Growth Drivers are Rapid growth in the pharma industry, Rising agrochemicals demand & Import duty on Chloromethanes

6. Suspension PVC Overview

S-PVC is used in both rigid and flexible applications. pipes, profiles, and roofing sheets are typical examples of rigid applications while flexible hoses, tubings, wires and cables, footwear, calendared sheets and films, extruded films are typical examples of flexible applications.

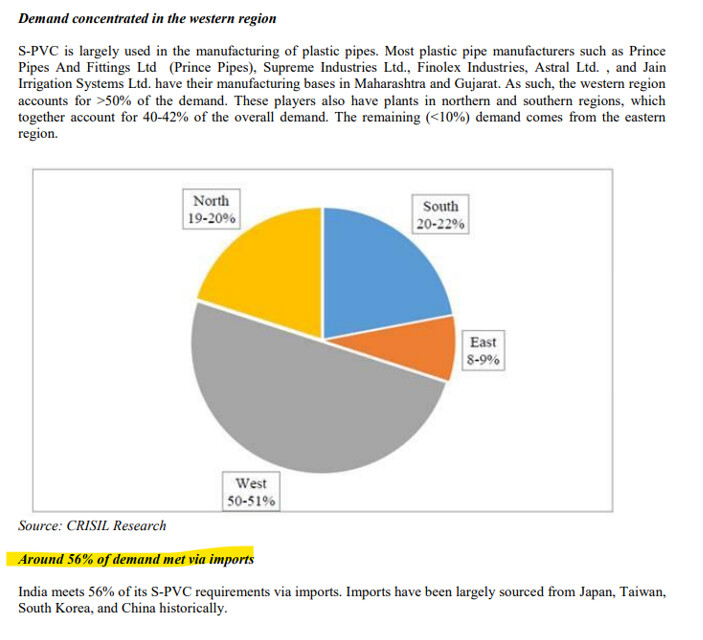

The market size was 46 MMT in 2019. Demand for S-PVC in the global market is largely linked to the construction industry and therefore economic development. India is one of the fastest-growing large markets for SPVC in the world.

CRISIL Research expects S-PVC demand to clock 7.5-8.5% CAGR over financial years 2021-2025.

Key Growth Drivers are Lack of viable substitutes driving demand, Low per capita consumption of S-PVC, growth in Irrigation, Urban infrastructure & Real estate.

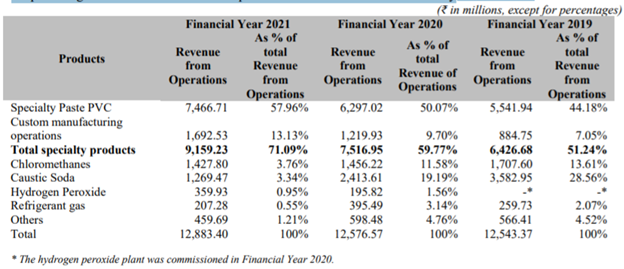

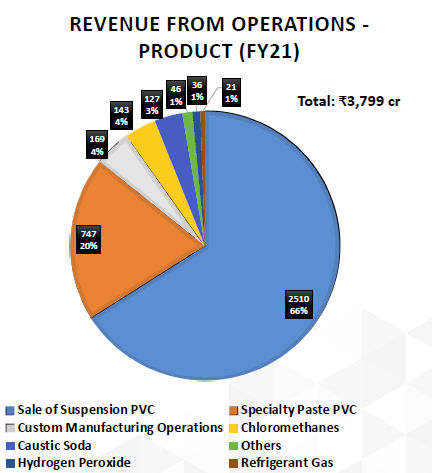

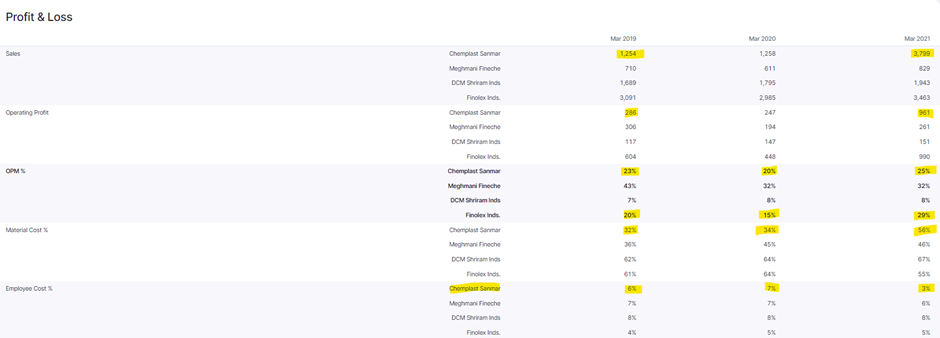

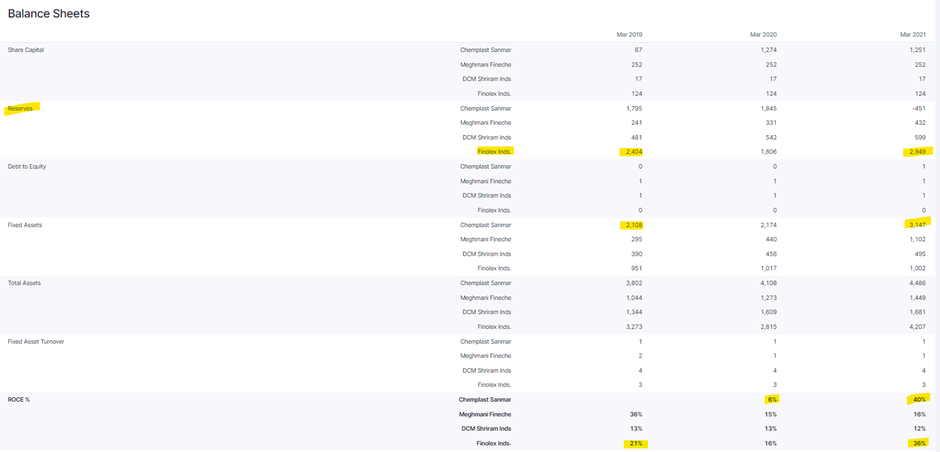

Segmental Revenue:

Revenues from the 100% subsidiary CCVL which manufactures Suspension PVC is a major part of the revenue which is 2510 Cr, 1878 Cr, 2051 Cr from years 2021, 20, 19.

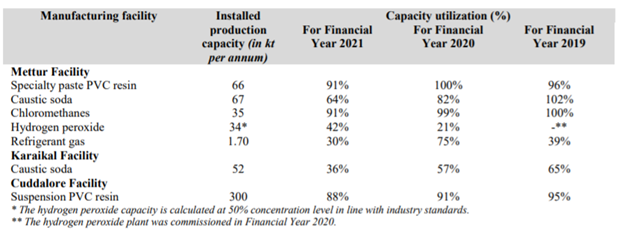

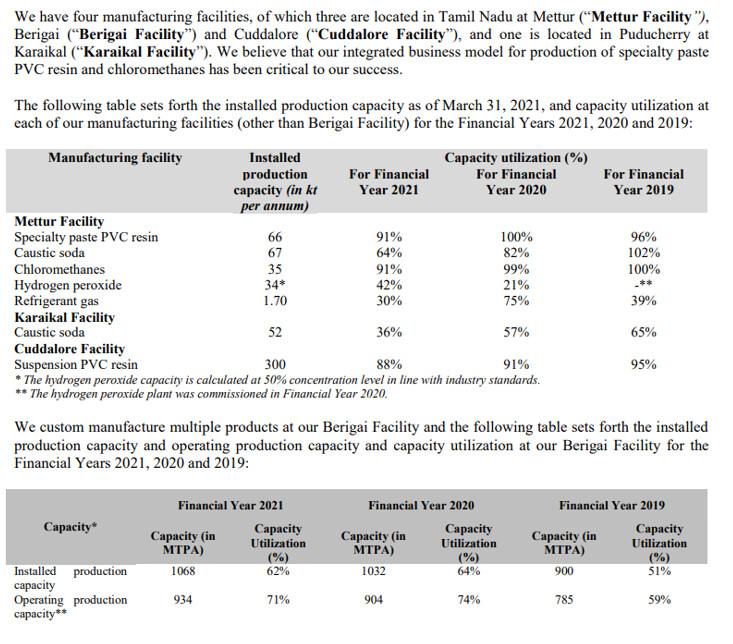

Manufacturing Plants:

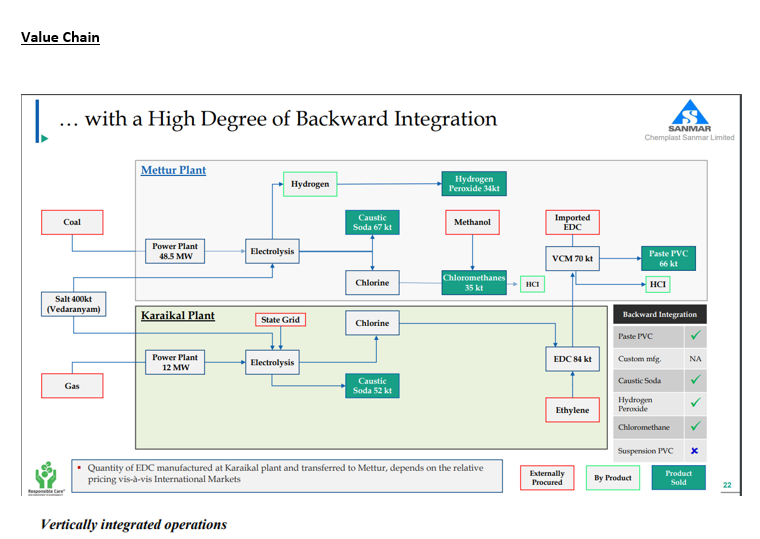

CSL has 4 manufacturing facilities, of which three are located in Tamil Nadu at Mettur (“Mettur Facility”), Berigai (“Berigai Facility”) and Cuddalore (“Cuddalore Facility”), and one is located in Puducherry at Karaikal (“Karaikal Facility”).

The Berigai plant is used for custom manufacturing.

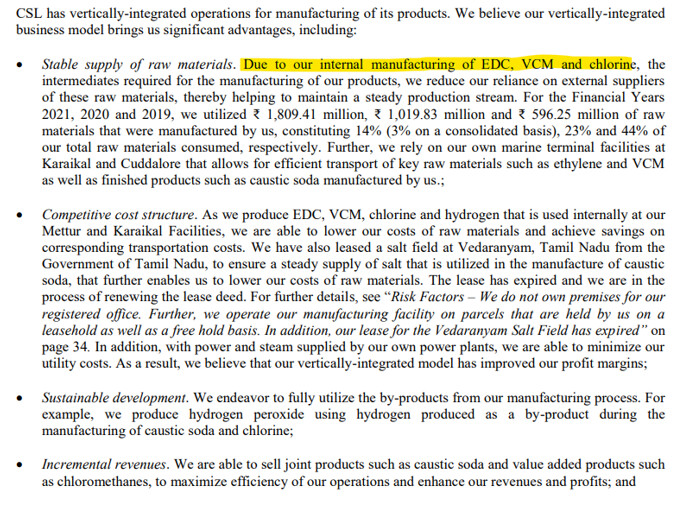

Competitive strengths

There are many competitive strengths mentioned in RHP but I believe CSL has a strong advantage in Specialty paste PVC resin

With only 2 manufactures in Indian for Specialty paste PVC and with backward integrated operations, CSL will have stable margins and with additional capacity at Cuddalore, it will capture more market share. With technical and raw material constraints there is a high barrier of entry in this segment. Captive power plants at 3 manufacturing plants can reduce power costs and ensure no interruptions Vertical integration that CSL has achieved is also a competitive advantage.

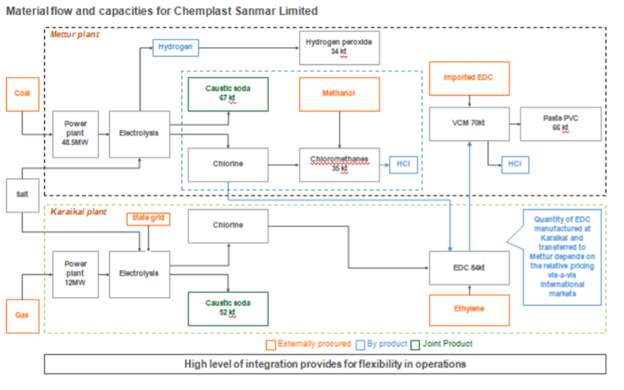

Picture depicting CSL’s integration of production

IPO and terms of the offer:

capital being raised: 3850 crores

fresh issue: 1300 crores, OFS: 2550 Crores

Recent developments:

In a recent exchange filing company declared that It has redeemed all its non-convertible debentures worth 1238 crores. and released all the pledged shares of CCVL which is a very positive news

Mutual funds like Mirae and SBI have significantly increased their stake post IPO. - very positive

Risks:

The majority of revenue & income for 2021 came from CCVL and it had a sudden boost to the profits. this could well be a one-time bump in earnings and CCVL might not be able to maintain the growth and margins. Link to CSL and CCVL Annual reports 2017-2021

Anyone tracking this stock can share their viewpoint and additional risks that need to be considered.

Thanks for posting this. I have been following this company intermittently so it’s good to have some nice analysis.

My 2 cents

The debt of 1238 crores was at nose bleed levels of 17 percent or so. That alone saves an interest cost of 200 crores a year . Most of this should go to bottomline of all other things remain the same.

Mirae and Sbi bought in as anchor investors and immediately after ipo. They together hold more than 5 percent each. ( Could be wrong about actual percent but it is susbtantial enough to make a filing on stock exchange)

Disc: invested. small part of portfolio. Waiting for first quarterly result post listing

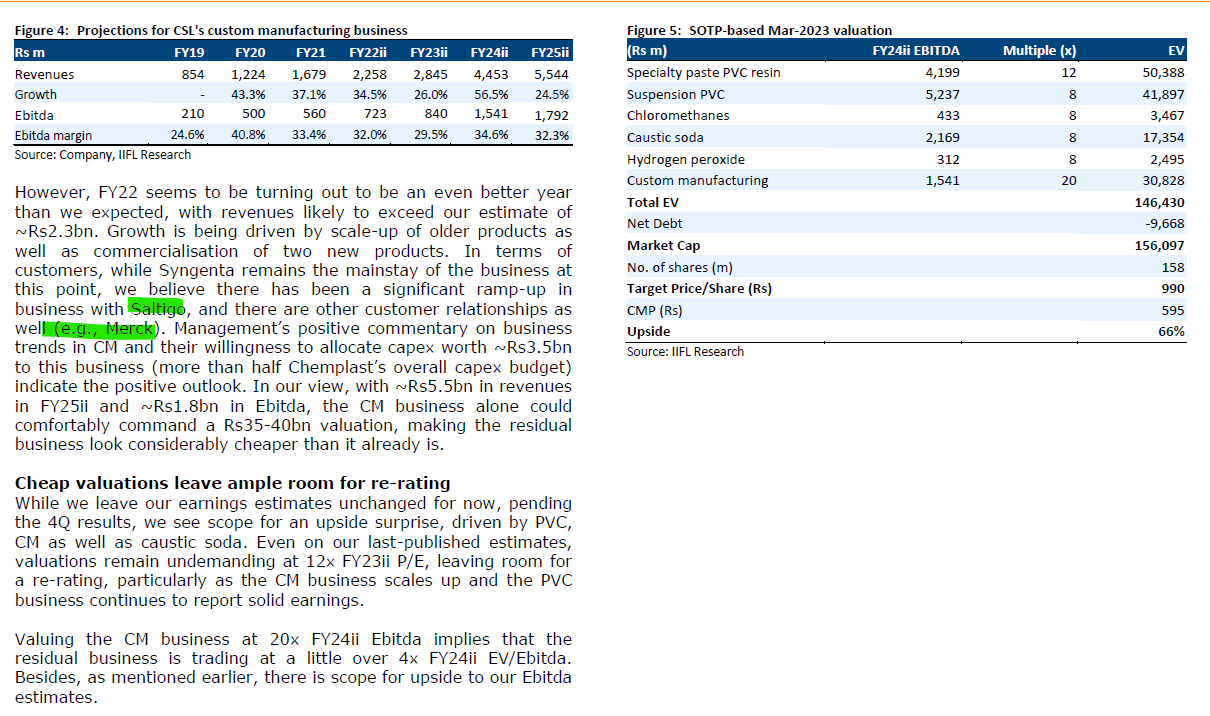

Below is the revenue breakup, if one considers the, CCVL numbers. So, suspension PVC & Specialty PVC resin contribute 86% of the numbers and should be our focus for now. Custom manufacturing will be a thing to watch out in future as bulk of new investments are going into it.

Capex of 256 cr in Specialty paste PVC & 340 cr in Custom Mfg. businesses has been announced.

FY21 had about 30-45 days of production loss due to covid, FY22 in comparison didn’t have any production loss. Plus the savings in interest cost as pointed out above by @Unknowninvestor . As per some scuttlebutt, demand and price scenario for suspension PVC remains strong.

Overall looks like on FY22 basis, the company looks reasonably valued.

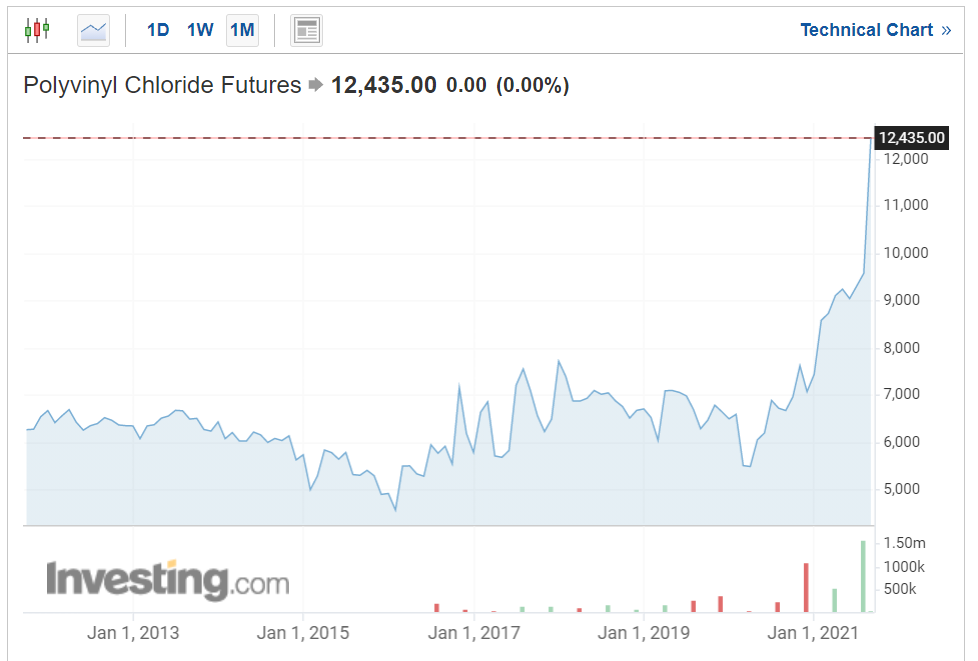

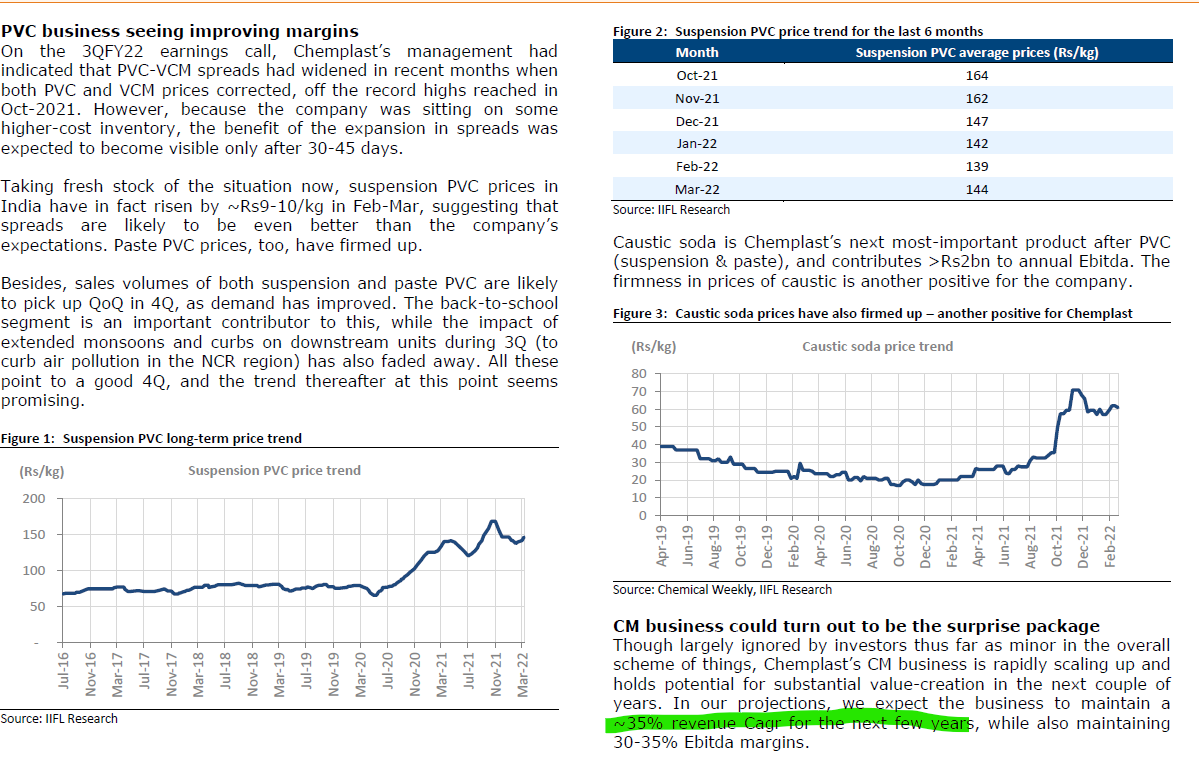

With PVC and Caustic soda prices at all-time highs, realizations and margins would improve significantly this year. Cant guarantee whether the prices will sustain at that high but they are not coming down anytime soon due to power shortage and a crackdown on chemical companies in china.

However one question remanins unanswered for me regarding the PVC plant shut downs across the world.

Structural changes in the specialty paste PVC resin market

The specialty paste PVC resin market has been undergoing structural changes globally with many plants witnessing permanent shutdowns. Some of the key plant shutdowns were:

LG Chem -90 KTPA in Korea – 2019;

Dongxing Chemical Co. Ltd. – 100 KTPA in China – 2019;

Vinnolit – 100 KTPA in UK and Germany – 2020; and

Formosa Plastics Corp- 65 KTPA in Delaware, USA –2018.

When I searched regarding the closure of these plants, reasons varied from lack of profitablility to environmental reasons. If pollution is the reason for shutdown, i have 2 questions

What is CSL doing to tackle the pollution issue

If the Indian Govt tries to curb pollution, will CSL be a likely target

The 30-35% volumes growth in both suspension & paste PVC looks good but has to be seen in the context of loss of production of about 30-45 days in H1 FY21. So just recovery of that production itself should give 25% extra volume production for H1 and only the rest should be seen as additional growth YoY, which comes to 10-15%

I am estimating PAT of at least 650-700 cr. for FY22. So at 11k cr. Mcap it’s trading at ~16-17x current year and i think earnings can surprise on upside.

FY23 growth prospect looks promising with 10% capacity increase in suspension PVC & ~45% in paste PVC coming onstream by end of this year. Further to that CMS should start making meaningful contribution.

Revenue from operations at 1671 cr. is up 80% YoY and 74% QoQ

PAT at 151.34 cr. is up 424% QoQ vs losses posted in Q2’20

Q2 EPS at 10.51 H1 EPS at 12.95

Long term debt reduced from 2024 cr. to 832 (IPO proceeds payment)

This should help reduce the interest outgo of 250 cr in H1 to somewhere below 100 cr. in H2.

They are net debt free if you consider cash and cash equivalents available. Ideally net interest should be quite low and in the range of 30-40 cr for H2.

Low per-capita consumption compared with other regions the per capita consumption of specialty paste PVC resin in India is 0.1 kg compared with China’s 0.6 kg and Western Europe’s 2.4 kg. Thus, the Indian market is fairly underpenetrated and has significant potential for demand growth in the coming years.

Lack of substitutes Application of specialty paste PVC resin in leather cloth and other end uses has no major substitutes, which is a key factor driving demand growth, going forward.

Leather footwear market has significant growth potential

Automotive market recovering sharply

Government initiatives like Make in India to boost investment in artificial leather production

Vinyl gloves rising rapidly post COVID-19 pandemic

Upcoming Capacities (CAPEX)

Received the environmental clearance for our proposed Specialty Paste PVC expansion. Received clearance for 70ktpa, but as of now, they are going ahead with 35 ktpa expansion as Phase 1.

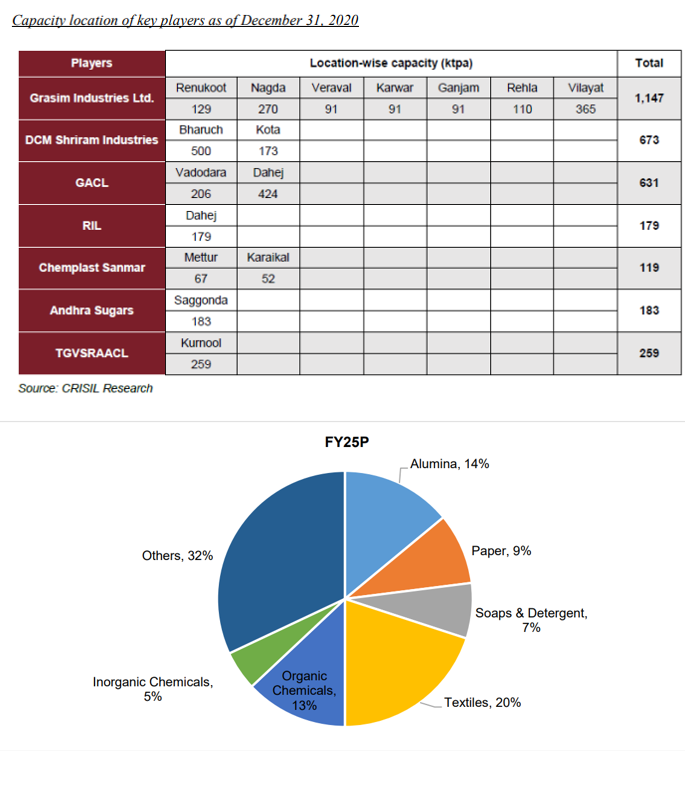

Alumina : Caustic soda demand from the alumina sector is expected to clock a robust 7-8% CAGR between financial years 2020 and 2025. Alumina production is expected to increase following the expansion of refinery capacity by players such as Vedanta, Hindalco, and Balco, and a gradual ramp-up of capacity. Import substitution of alumina, growth in domestic aluminium consumption, and rising aluminium exports should propel caustic soda demand over the next five years.

Textiles : Cotton yarn production is expected to clock 2-3% CAGR over the next five years, versus approximately 1% over the past five years, even as demand for man-made and blended yarn is expected to exceed that for cotton yarn. Meanwhile, production of Viscose Staple Fibre is expected to log a healthy 7% CAGR, driven by Grasim’s capacity expansions. Therefore, overall demand for caustic soda from the textiles segment is expected to log 4-5% CAGR.

Paper : Caustic soda demand from the paper segment is expected to post 2-3% CAGR, led by its increased usage in packaging for end-use industries such as household appliances, fast-moving consumer goods, readymade garments and e-commerce.

Chemicals : Demand from the organic chemicals segment is expected to clock 3-4% CAGR, driven by healthy demand growth from end-user industries such as dyes and paints. Further, export markets are providing opportunities for domestic chemical manufacturers. Demand from the inorganic chemicals segment is expected to grow at a relatively tepid pace (vis-à-vis the organic chemicals segment), due to stricter environmental norms. Overall, demand for caustic soda from the chemicals segment is expected to log approximately 2.5% CAGR

Soaps and detergents : Caustic soda demand from this segment is expected to clock 4-5% CAGR, driven by increasing hygiene awareness amid the COVID-19 pandemic, increasing penetration in rural areas, and a rise in per capita consumption.

Hydrogen peroxide is mainly used in the pulp and paper industry for bleaching pulp and deinking recycled paper. It is also used in the textiles, electronics, food and beverages, and healthcare industries. Along with peroxyacetic acid, hydrogen peroxide is one of the important components in manufacturing peroxide-based disinfectants. It is also used in various municipal and industrial applications.

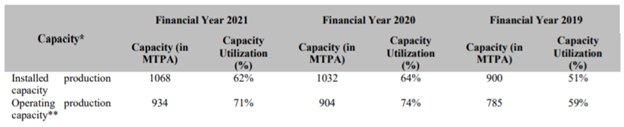

Suspension PVC (S-PVC) is made either through mass or bulk polymerisation or through suspension polymerisation. S-PVC is used in both rigid and flexible applications. pipes, profiles and roofing sheets are typical examples of rigid applications while flexible hoses, tubings, wires and cables, footwear, calendared sheets and films, extruded films are typical examples of flexible applications.

Global demand for S-PVC was 41 mmt in financial year 2015, which increased at a 3.1% CAGR over 2015-19 to 46 mmt in 2019. Demand for S-PVC in the global market is largely linked to the construction industry and therefore economic development. In recent years, S-PVC consumption has been concentrated in the developing Asian economies such as China, India, Vietnam, and Indonesia. By region, China accounts for more than 40% of global S-PVC consumption. India is one of the fastest growing large markets for SPVC in the world while other major consuming regions are other Asia-Pacific countries, North America, Western Europe, and the Middle East and Africa (“MEA”).

CSL has four manufacturing facilities, of which three are located in Tamil Nadu at

Mettur (“Mettur Facility”)

Berigai (“Berigai Facility ”)

Cuddalore (“Cuddalore Facility ”), and

one is located in Puducherry at Karaikal (“Karaikal Facility ”).

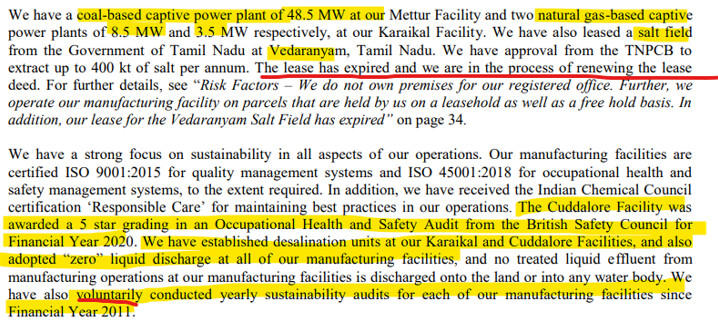

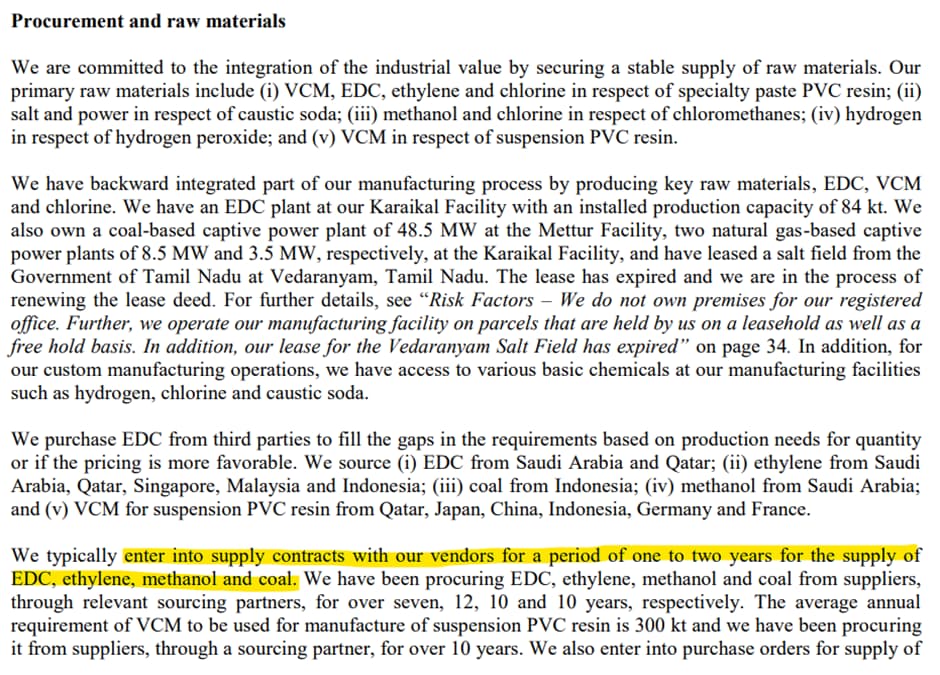

It has a coal-based captive power plant of 48.5 MW at its Mettur Facility and two natural gas-based captive power plants of 8.5 MW and 3.5 MW respectively, at Karaikal Facility

It has also leased a salt field from the Government of Tamil Nadu at Vedaranyam, Tamil Nadu and has an approval from the TNPCB to extract up to 400 kt of salt per annum. Capex

Going forward, CSL is proposing to expand its operations by

(i) increasing the installed production capacity of specialty paste PVC resin by 35 kt;

(ii) setting up a multipurpose facility with two blocks for custom manufacturing operations; and

(iii) increasing the installed production capacity of suspension PVC resin by 31 kt by de-bottlenecking the suspension PVC resin plant. It also intends to improve its operational efficiencies in its manufacturing process at the Karaikal Facility by de-bottlenecking the caustic soda plant

Sustainability

The Company has strong focus on sustainability in all aspects of its operations. Manufacturing facilities of CLS is certified ISO 9001:2015 for quality management systems and ISO 45001:2018 for occupational health and safety management systems, to the extent required. In addition, it has received the Indian Chemical Council certification ‘Responsible Care’ for maintaining best practices in its operations. CSL is a part of the SHL Chemicals Group, which in turn is a constituent of the Sanmar Group, one among the oldest and most prominent corporate groups in the South India region. Fairfax India Holdings Corporation (“Fairfax ”), a well-known international investor led by Mr. Prem Watsa, based in Canada, has invested, through FIH Mauritius

Investments Limited, in the SHL Chemicals Group since 2016.

Valuations

A cursory look at RHP reveals that CSL paid ₹15 per share of ₹1 face value and not ₹5. Current IPO price of ₹540 is ₹5 face value. In essence the delisting price was ₹75

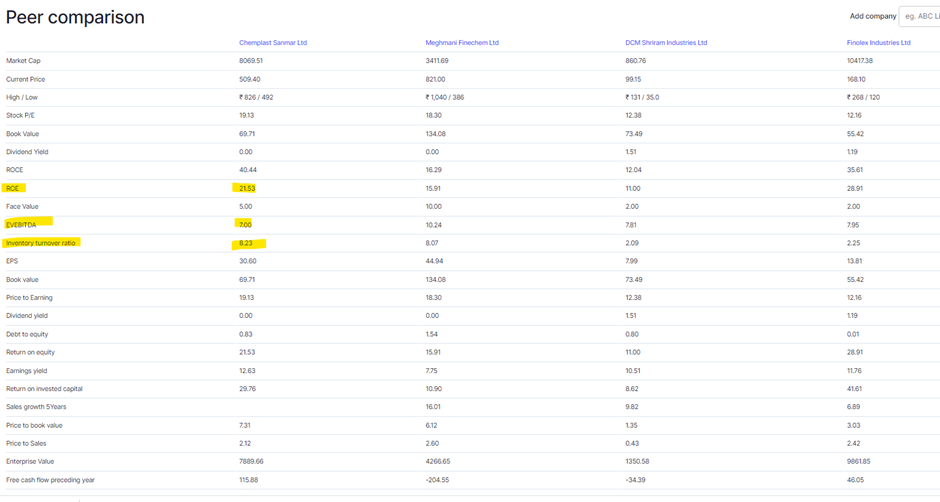

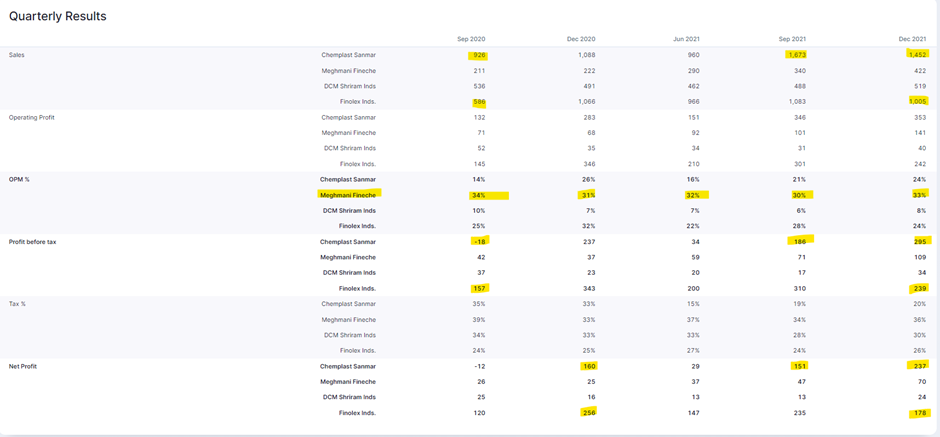

We don’t have apple to apple comparison here but picked some where they treat as peers.

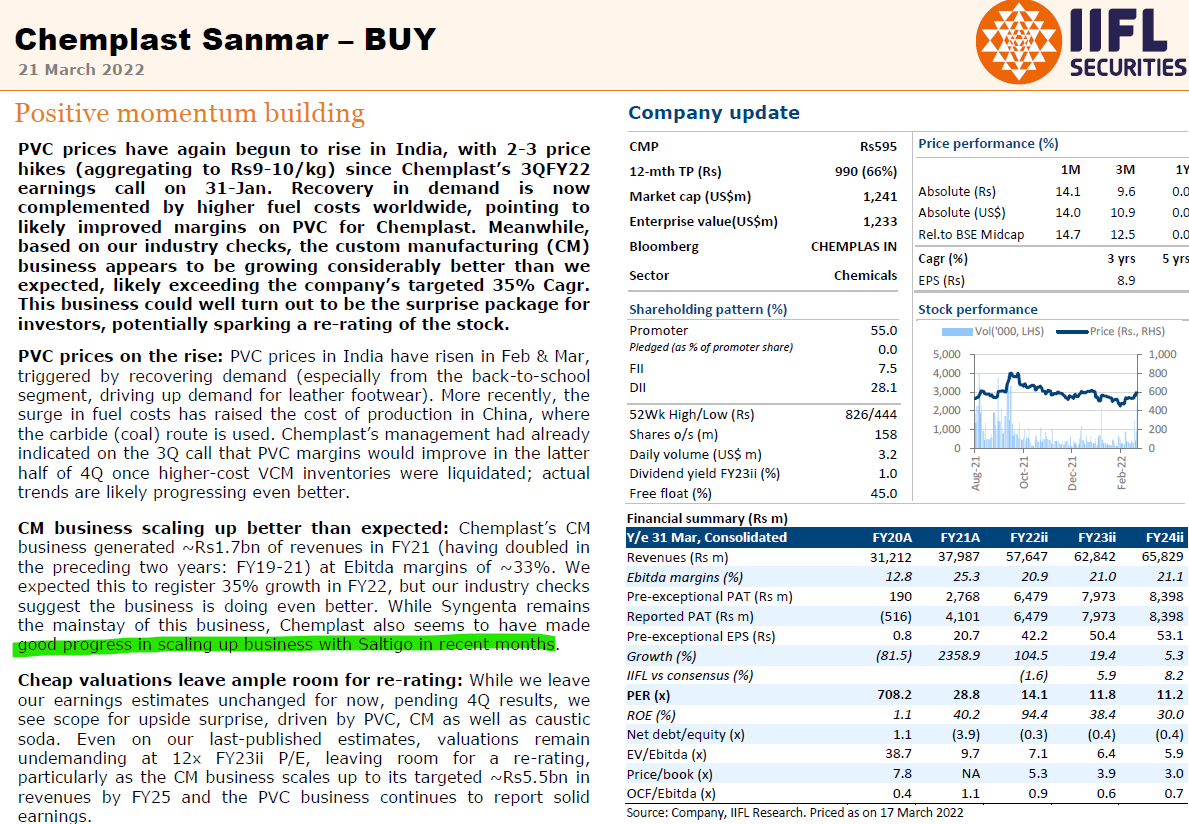

2012 Avatar of CSL did not have a custom manufacturing business. Current avatar houses custom manufacturing business. A segment growing at 35% CAGR. (Source: RHP)

Industry Structure

2012 import duty for PVC resins - 5%

2021 import duty for PVC resins - 10%

Structural changes in the specialty paste PVC resin market

The specialty paste PVC resin market has been undergoing structural changes globally with many plants

witnessing permanent shutdowns. Some of the key plant shutdowns were:

LG Chem -90 KTPA in Korea – 2019;

Dongxing Chemical Co. Ltd. – 100 KTPA in China – 2019;

Vinnolit – 100 KTPA in UK and Germany – 2020; and

Formosa Plastics Corp- 65 KTPA in Delaware, USA –2018.

As a result, India’s imports of specialty paste PVC resin have shifted from South Korea (which held 44% share in imports in financial year 2016) to countries like China, Japan and Taiwan in financial year 2020. South Korea’s share fell to 7% in financial year 2020, post shutdown of the LG Chem speciality paste PVC plant and tightness in supply

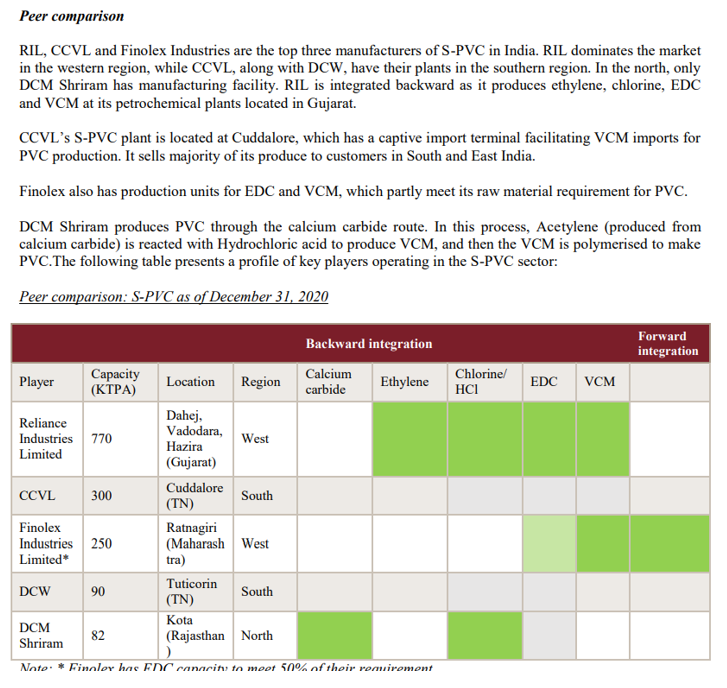

Domestic Competition

Reliance is strong in the north

Chemplast Sanmar is strong in South

Specialty paste PVC resin is used to make flexible products (such as artificial leather, gloves, tarpaulins, conveyor belts and coated fabrics). Suspension PVC is largely a basic product while specialty paste PVC resin is a specialty product. In India**, CSL and Finolex Industries Limited (Finolex Industries) are the only producers of specialty paste grade PVC resin.**

What is the cost difference between imported product and domestically sourced product?

Check the gross margins, recently too much price run up of Caustic Soda , so the current margins are sustainable ?

Lack of raw material availability and technology creates barriers to enter specialty paste PVC resin market – Key Raw material is Gas / Coal, I don’t understand this .

Custom manufacturing – Is this not lumpy in nature ?

From the below graph we can understand EDC is imported but in RHP says different thing,

Finolex is using the entire capacity for captive consumption ?

Ethylene is converted into EDC (Ethyle di-chloride) by reacting either with chlorine (in the direct chlorination process) or with hydrochloric acid (in the oxy chlorination process)

What are the advantages of making EDS via Direct Chlorination vs Oxy Chlorination process ?

Key things to look in chemical companies

All the plants are equipped with zero liquid discharge systems

Plants are strategically located at the ports and Multi Plant setup

Access to key raw material - salt (Leased land from government at the sea port )

Sea water is used in the plant so less dependency on the ground water / other sources of public water supply

Industry scuttlebutt says Sanmar is very respected group

Total capex of around Rs. 340 Crores to 350 Crores over the next three years period

Received Env. clearance received for the capicity of 70,000 tonnes of suspension PVC - First phase is doing expansion of 35,000 (Expected to come up by FY24 - October 2023) at CCVL Cuddalore

Expanding custom manufacturing business with the addition of new multipurpose facilities thereby bringing in new products which are in the pipeline. Planning detailed engineering and ordering is already in progress for the first phase of expansion (This is done in phased manner 10% capacity addtion at a time )

Given the make or buy economics in ethylene dichloride we have now optimized our production of caustic soda and EDC and another aspect of growth which is very imminent is a de-bottlenecking of a suspension PVC capacity by 10%. This is expected to come fully online by the first quarter of FY23. This is a phased de-bottlenecking part of which is already completed.

Debt

Chemplast Sanmar prepaid its NCDs in the month of August using IPO proceeds and our subsidiary, CCVL, had renegotiated its term interest from 11.75% to 8.75% in Q2 FY22. Thus, our finance cost for the quarter came down significantly to Rs. 37 Crores from Rs. 113 Crores on year-on-year basis.

Risks

PVC import duty for the current budget and then that may impact the premium that the domestic players are able to charge related to the imported PVC

This is a very hypothetical situation, I do not think we need to spend too much time on that, it is just that they had made a request, it does not mean that it is going to happen, but all that I like to say here is this,

PVC duties went up from 7.5% to 10% as recently as in 2019 and this was done after a lot of deliberation and discussion and for very valid reasons, essentially PVC is a very, very strategic commodity, which

goes into very important sectors like construction, like agriculture and water conveyance and therefore it is always better not to be over-dependent on imports for such a strategic commodity. Given that the

government also realized the factor costs in India were much higher than in comparable countries and therefore to encourage for the manufacturer of PVC in India factor to give this increase in duty and this

happened just as recently as in 2019 and equally importantly this 10% is not high, it is quite comparable with levels of tariffs that are prevailing in other countries, which are comparable to India at the stage of

development that we are in, therefore we are quite confident that there is absolutely been no change since 2019 on this front and we see no reason why there would be any changes in duty

The antidumping duty that we have is on two countries, which is basically US and China, this ranges from around 2% to 10% in the case of the US and 4% to 10% in the case of China, actually I have just

converted this into a percentage actually denominated in specific dollars per ton and it defers given who the exporter is. This is expiring on February 13, 2022, and we do not expect any great impact because

there is no impact really largely because, a) as far as the US is concerned even now the FAS Houston prices for PVC from the US is already higher than the CFR India prices and therefore given that and the

time involved in shipping PVC all the way from the US to India very high logistics costs, non-availability of containers, etc., US is really not a threat in fact we do not see much material coming in from the US to

India and as far as China is concerned here again we do not believe that it is going to be a threat, the way these things normally work is that whenever there is antidumping duty in-force on a specific company

that company normally reduces its price to factor in the antidumping duty and the others on whom there is no antidumping duty gets the benefit as a higher price now when the antidumping duty is removed the

general practice is for this company also to raise the price to the same level as the others, they do not need that money on the table, so we do not think that this will impact the market at all.

Industry Structure / Supply - Demand

PVC supply demand in India is concerned you know by 2026, the demand is expected to grow to around 4.5 million tonnes and with the current capacity of around 1.5 million tonnes that would mean a gap of 3 million tonnes as far as suspension PVC is concerned, so this is a huge gap, now any new capacity that comes in is actually welcome because once new capacity comes in even the downstream producers tend to increase their capacities because they have no confidence of availability of material, so even that 4.5 million tonnes would go up even more given the fact that the per capita consumption of PVC in India is far lower than the rest of the region. For instance in India it is around 2.4 to 2.5 kilos whereas in China it is in of excess of 10 kilos where the other Southeast Asian countries are anywhere between 4.5 to almost 8 kilos. So we are way behind and supply side security would also give the confidence to downstream producers to expand, so we do not see any impact as it is of any new capacity coming in other than a positive impact even the capacity that is announced can come in by only around 2025 or 2026 because it takes that kind of a time to build for a new Greenfield plant unlike Brownfield expansion like us, so that is how the market would absorb this additional capacity.

As far as our own expansions are concerned we are always focused on growth opportunities on various front, and we are always looking at that. Our current focus is on growing our specialty chemical’s size and increasing the contribution of specialty chemicals to our overall portfolio. In this regard, we have already announced, as I was also mentioning in my opening remarks, we are already working on this

Specialty paste PVC expansion as also the Custom Manufactured Chemicals expansion. In the Suspension PVC, we are doing a small de-bottlenecking which will 10% and that will come in quite early within the next 3 to 4 months. Having said that, any futures expansions are things like that would be dependent on like you also said the feedstock tie-up, these are all capital intensive if we decide to integrate on the feedstock ourselves, then that would mean far more capital commitment so that is something that we will look at the right time.

CSM

We did commercialize 2 new molecules in fact on one of them the campaign got over and we actually have a repeat order for the next campaign on hand and the second molecule we are in the process of making shipment and that campaign will get done sometime this quarter and also the pipeline is very strong I know we have a number of products that we are working on the various stages of commercialization and we are making good progress on those aspects.

Comparison Imported vs Domestic Pricing

See if you take for instance suspension PVC the normal premium is around $30 a tonne over import priority price and if you look at paste PVC it could be anywhere from $50 to $100 a tonne in terms of import parity, but when prices by themselves are very high at that point in time the premiums are moderated, it would be a little too much to add a premium on top of what is already a very high price level and these things vary a little bit but normally their average is around these levels you would find that could be an opportunity there.

Backward Integration / Asset Light Model

First of all good afternoon and thank you for your kind words, as far as EDC and VCM are concerned as you know EDC is one step before VCM in terms of value chain. So from EDC you make VCM and then from VCM we make the PVC and if you have to invest in the manufacture of VCM itself it is capital

intensive because you will need to setup even if it is based on imported EDC or imported ethylene if we

have that you will still need significant capex for investing in the VCM production facility so obviously

the value addition would be more, you would be captured a bit more of the value chain, but then you

would also have to invest lot more in that, whereas if you are importing VCM and making PVC it is an

asset like model like mentioned in the last call as well while the margins would be lower the investment is far-far lower, so it is kind of a toss-up between the capital investment and operating margins, so we have chosen to do it through the VCM route largely to reduce the time to market and also because that would give us a better return on capital and that was how we have done it and for the last 12 years we have been successful as well in setting up a supply chain that meets our requirements, any further investment we would need to then look at how much VCM was available or whether to go through the integrated route itself and that is something that like I said we would take a decision at the appropriate time. As far as the Paste PVC is concerned incidentally we have 100% of the VCM manufactured in-house, so there we are fully integrated.

How much is the ROC difference between, if I really look at the spread between going for EDC to

Suspension PVC and VCM to PVC so what kind of ROC difference and how much additional capacity is

required?

Today, let me give you very, very rough rule of thumb numbers for setting up maybe 300,000 tonnes

PVC plant based on imported VCM, which is more or less of Brownfield site like us, I m not talking

about a completely Greenfield site which could be much higher, the Brownfield site like us, which

already has a marine terminal, the pipeline, VCM storage tank and all that, that could cost may be around $100 to $125 million, but an equivalent 300,000 tonnes VCM plant could cost anywhere between $250 to $300 million so this is again these are all very rough numbers which also equally depends on the geography where you are setting it up, but that kind gives you an idea of the difference in capital investment that is required for the integration that you are seeking and today’s prices EDC prices are pretty high at around $850 a tonne whereas VCM prices are at $1100 a tonne so that advantage is not so much seen for a new plant

Plant Shutdown

In early February there is a shutdown (12 days ) that we are anyway taking which is an annual shutdown that we take during which we will also be lining up some of the de-bottlenecking equipment whatever is being put in so that will anyway be there

Captive Power

Today coal accounts for around 40% of our total power mix and we also have some portion coming in

through gas and some portion is through the grid so we buy the grid power. In our subsidiary company,

Chemplast Cuddalore Vinyls Limited, we are working with somebody on group captive power project on

the solar front which could account for 25% of the CCVL requirement so we are constantly looking at it.

We also have some windmills of our own but those are not too significant, but yet we are looking at

means where we can reduce the proportion of coal in the overall mix.

Key Industry Learnings

Around 60% of the total leather cloth industry is concentrated around NCR region

This is the pact that impacted the shutdowns in China and else where

" From DRHP :

The processes of producing caustic soda include mercury, diaphragm, and membrane. Mercury based capacities have been phased out in most of the countries on account - of environmental regulations, leaving out a few capacities in Europe and America. However, India has already moved from mercury based capacities to membrane based capacities. The major end-use industries include textiles, chemicals, paper, PVC, water treatment, alumina, soaps and detergents, and chlorinated paraffin wax. Chlorine is a joint product manufactured along with caustic soda, which is also used in various industries such as PVC manufacturing, water disinfection, and pharmaceutical, among other chemical industries. Therefore, most caustic soda manufacturers have downstream capacities integrated to utilise the produced chemicals in further chemical production such as PVC and chloromethanes.

"

The Minamata Convention on Mercury is an international treaty designed to protect human health and the environment from anthropogenic emissions and releases of mercury and mercury compounds. The convention was a result of three years of meeting and negotiating, after which the text of the convention was approved by delegates representing close to 140 countries on 19 January 2013 in Geneva and adopted and signed later that year on 10 October 2013 at a diplomatic conference held in Kumamoto, Japan. The convention is named after the Japanese city Minamata. This naming is of symbolic importance as the city went through a devastating incident of mercury poisoning. It is expected that over the next few decades, this international agreement will enhance the reduction of mercury pollution from the targeted activities responsible for the major release of mercury to the immediate environment.

Studied the idea, initially I thought why aren’t the expanding massively given the supply/demand deficit is structural in nature. And a lot of capacity based on mercury in China is slated to go out of production.

Then why aren’t they expanding massively, given they do 40%+ ROCE?

Simple reason is the supply side and the strength of the competition.

Reliance is the largest player in Suspension PVC with a capacity of 7.7 Lakh tonnes per annum+its fully backwards integrated. Moreover, Adani is expanding and creating a fully integrated PVC complex with 2million tonnes per annum capacity.

When you are competing with giants, multiple is likely to remain depressed. The ROCE, thus looks too good to be true…

+The capacity expansion being announced by Reliance in UAE is likely to be used to export additional PVC to India.

One rule for investing in India:- Never compete with Reliance.

While the company has posted good results and their con call transcripts also indicate good potential in mid term, do you know any reason why the stock is getting hammered even more than usual(compared to other chemical stocks) ?FII’s have increased stake last quarter as well . As I see it by next quarter result ,their PE would be below 7 even if the current price holds .Considering more than half their business is specialty chemical with good tailwind, this constant dwindling of price seems inexplicable to me. Could you please share your thoughts on this ?

Disc: Invested

a decade back the company delisted its share from the exchange and offered minority shareholders a raw deal. During the last crisis they were over leveraged and were at the risk of going bankrupt. They delisted the company at INR 50 i think. Now they relisted the business back at 500 and change so in effect made 10x their money over the last decade or so.

That is well known . But inbetween fairfax has rescued the company,they have 25% stake .Surely they were aware of it ? The entity that delisted is not really the same as this one contains other busnesses .Also institutions hold more than 30% stake and FII holdings increased past 2 quarters .I understand that this kind of old news can be used to scare away most retailers but that can not have a fundamental impact on the business .

Its not exactly the same entity that is listed again, lots of changes happened to the Company in the years it remained private, They divested few businesses and they started new lines of business, came back profitable and also they reduced their debt through IPO proceeds.