Now Adani Enterprises is setting up a 2.0 MMTPA (1.0 MMPTA by FY25 and another 1.0 MMTPA by FY30) coal to PVC project at Mundra, Gujarat with an estimated investment of INR 29,200 cr. PVC grades such as suspension PVC(Resin), Chlorinated PVC (C-PVC) and Emulsion PVC (paste).

3 Likes

possible that these companies were using the carbide route to make PVC - Management Excerpt from one of the concalls (This is a very high percentage and what they have not even considered is the fact of a lot of carbide PVC plants getting stressed and dropping off the grid in China largely because of the mercury issue and also because of the carbon issue because these are essentially from coal.)

2 Likes

FY23 Q2

Results

Investor Presentation

Concall Transcript

- H1FY23 EBIDTA Margins 11% ( down from 19% ) , compression mainly due to high RM costs, energy costs and low realisations in PVC

- Volumes of all products witnessed an increase in H1-FY’23 compared to the volumes in the corresponding period last year

- Custom manufacturing will grow by 30% in FY23 (H1FY23 EBIDTA contribution from this segment is 65% vs 50% last year H1) , earlier guidance was 15% now revised to 30% due to more visibility

• Uncertainty in the pricing environment continues for Paste PVC and Suspension PVC (Mainly due to covid restrictions in China that lead to less consumption in China and the same is being dumped into other countries that lead to price erosion)

Expected to normalise by end of Q3 - Pre pandemic domestic PVC demand is 3.3 million tonnes, we are 15-17% away from these numbers, the demand will come back to this level and there is scope to grown beyond that (new capacities will come up in phased manner and those can be absorbed , will not have a situation of oversupply)

• Feedstock (EDC and VCM) prices have also dropped, albeit with a lag. The benefit will however be realized only once the PVC prices stabilize; expect price stability by end of Q3

• Custom Manufacturing business continued to see healthy demand in Q2-FY’23

• In Q2-FY’23, Other Chemicals(- Includes Caustic Soda, Chloromethanes, Refrigerant gases and Hydrogen Peroxide) delivered a 37% increase in revenues on y-o-y basis, primarily led by growth in terms of both volumes and prices of Caustic soda

• Cost of Power and Fuel increased by Rs. 132 Cr and by Rs. 61 Cr as compared to H1 and Q2 of FY’22, respectively. This is mainly due to increase in coal and natural gas prices

• In H1-FY’23, the company spent Rs. 115 Cr for capex. Both the Paste PVC and Custom Manufacturing expansion projects are on track

• With a healthy cash balance of Rs. 1,400 Cr, the company continues to be net cash positive on a consolidated basis - To onboard a new molecule it takes anywhere between 18-24 months

Key Triggers to watch out for

- Paste PVC Expansion project at Cuddalore on track ( Capacity 41,000 tonnes ) will come on stream by Q2FY24

- Multi purpose custom manufacturing plant phase 1 expansion is on track (due to high visibility on the product pipe line phase 2 expansion will also be clubbed with this and executed ) will come on stream by Q2FY24

- A key customer (global innovator) signed letter of intent to supply advanced intermediate for recently launched Active Ingredient (AI) (Appears to be agro chemical, from the management commentary this appears to be blockbuster molecule )

1/3 of the new custom manufacturing setup capacity will be used for this AI , rest of the capacity for other products (This is kind of Europe + 1 kind of relation )

Finance

- Finance costs have come down to 40 crores compared to 149 crore YoY

- Total capex spent on custom manufacturing is 310 crore ( Phase 1 - 260 crore , Phase 2 - 50 Crore now both are merged and executed as phase 1 , if required the capex for prposed phase 2 may even go further as well)

- Total cash on books ( 1400 crores of which 850 crores is with CCVL and 550 crores with holding company

- Long term debt 842 crores out of which 692 crores debt run till 2030 and another debt of 150 crore will be paid off in 4 years time

Edit on 17th Nov 2022 - New Capacities by other players

4 Likes

Thanks @Rafi_Syed. Based on this commentary, we should see another subdued quarter in terms of margins for Q3 but stable volume and a rebound once PVC prices stabilize. Power & fuel costs coming back to normal will add further impetus to margins.

Disc: Invested.

2 Likes

@shreyasnevatia - So, read Chemplast Sanmar DRHP and had several concerns and questions. Anlysis of the DRHP and associated questions below:

- In 2019, S-PVC business was demerged from Chemplast Sanmar Limited into Chemplast Cuddalore Vinyls Limited (“CVVL”). The ownership of the demerged entity went to Sanmar Engineering Services Limited (an entity owned by the Promoters + FIH Mauritius (assuming Fairfax)). Reason – to run commodity and specialty business separately. (page 165 of DRHP)

- In 2021, the same CVVL was then acquired by Chemplast Sanmar by paying Rs. 300 Crores to make it a WOS. (page 166 of DRHP)

- Now, Sanmar Engineering had taken a loan of Rs. 1220 Crores from HDFC Limited by pledging shares of CVVL. Now, 100% of shares held by Chemplast Sanmar in CVVL is pledged to HDFC Bank Limited for a loan of Rs. 1220 Crores availed by Sanmar Engineering Services Limited. (page 48, point 29 of DRHP)

Query – has this pledge been removed? Is it being disclosed? - In Dec 2019 – Chemplast Sanmar raised Rs. 1270 Crores by issuing NCDs for the following purposes: (Page 91 of DRHP)

(i) Repayment of Rs. 69.5 Crore borrowings (not sure who the lender was!)

(ii) Investment of Rs. 482.2 Crores in Sanmar Group International Limited (owned 100% by Sanmar Holdings Limited)

(iii) Funding of DSRA for Rs. 55.4 Crores (So, they were unable to even service the debt at this stage and they borrowed at 17.5% to do this!)

(iv) Repayment of advance to Sanmar Holdings Limited of 637.5 Crores (owned 100% by SESL)

Note – SESL ownership above.

Effectively, Sanmar Chemplast issued NCDs of Rs. 1270 Crores and appears to have paid Rs. 1119.7 Crores to Promoter entities!

**So payment to promoter entities through Sanmar Chemplast by Dec 2019 seems to be **

- Rs. 1119.7 Crores + 300 Crores = Rs. 1419.7 Crores

- The IPO

- NAV per share at IPO time is of Rs. Minus 139.15 (page 97 of DRHP)

- IPO is for Rs. Rs. 2550 Offer for Sale and Rs. 1300 Fresh Equity for repayment of NCDs.

(Wait, wasn’t the NCDs itself largely to make payments to the Promoter entities?)

Now after IPO, Promoter’s have earned

**- Rs. 1419.7 Crores + Rs. 2550 Crores = Rs. 3,669 Crores **

(Demerger & acquisition 300 + NCD 1119.7 + OFS 2550)

After IPO the debt has now zoomed to Rs. 925 Crores from nearly 80 in March 2020. For the CAPEX of course!

-

Now for TCI Sanmar Chemicals SAE – Egypt

Sanmar Holdings owns 99% of this company which as on March 2020 had a NAV of Rs. - 2494 Crores (Negative 2494 Crores) and had made large losses from 2018 to 2020 (page 194 DRHP)

Promoter guarantee given to secure the loans to this entity is to the order of USD 1.9 Billion + (say Rs. 14,000 Crores approx)

Has this been released or is there a chance this promoter guarantee could be invoked? And will it be promoter shares in Chemplast Sanmar or do they have other assets to cover the guarantee? -

Credit Rating

Lastly, the Credit Rating was changed from Negative to Stable by Brickworks rating prior to the IPO.

SEBI has banned Brickwork ratings I think in 2021!

I kind of didnt read beyond the DRHP. So, if the pledges and guarantees are disclosed on a continuous basis - then investors can take a well informed decision! If not!!!

4 Likes

Regarding the credit rating point

A recent update released by Chemplast sanmar on 24th Feb 2023, they have withdrawn credit rating from Brickwork Pvt limited.

Most of its past rating updates are now from CRISIL and India Ratings and research.

1 Like

The Custom Manufactured Chemicals Division of Chemplast Sanmar Limited has signed a Letter of Intent (LOI) with a global agrochemical innovator to manufacture a new pipeline Active Ingredient (AI).

- The LOI spans a 5-year period, and commercial supplies of the new product are expected to commence in CY 2025.

- The product will be manufactured in a recently commissioned production block.

- This marks a significant milestone for Chemplast Sanmar as it’s the first time they will be involved in the manufacture of an AI.

- It is the third LOI signed by the company in the past 12 months, indicating customer confidence in their research and development capabilities.

- The Custom Manufactured Chemicals Division specializes in manufacturing advanced intermediates for agrochemical, pharmaceutical, and fine chemical innovators.

- The division is well-equipped with state-of-the-art production blocks, Pilot, and R&D facilities, allowing them to handle a wide range of chemistries and processes.

- Chemplast Sanmar Limited is a part of the SHL Chemicals Group and is known for producing a range of specialty chemicals and other chemical products.

1 Like

Chemplast Sanmar Q2FY24 Concall Summary

1 Like

bro where do find old company drhp file i want parnax lab can guide me through it

Provisional add on pvc resin from china is imposed

1 Like

4 Likes

looks like management commentary on PVC is ambivalent…

Negatives:

-

the container scarcity in Q1 has eased.

-

weakness in Chinese economy meant unabated low priced imports from July.

-

decision on anti-dumping only by Q3

2 Likes

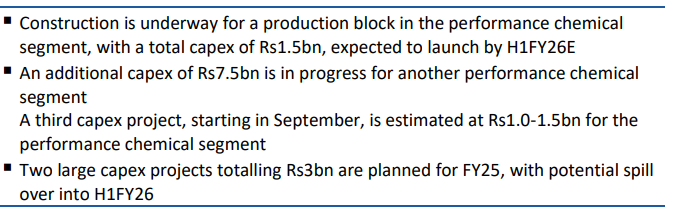

Chemplast Sanmar to invest Rs. 160 crore on capacity expansion of custom manufactured chemicals

1 Like

Q2 results mindmap

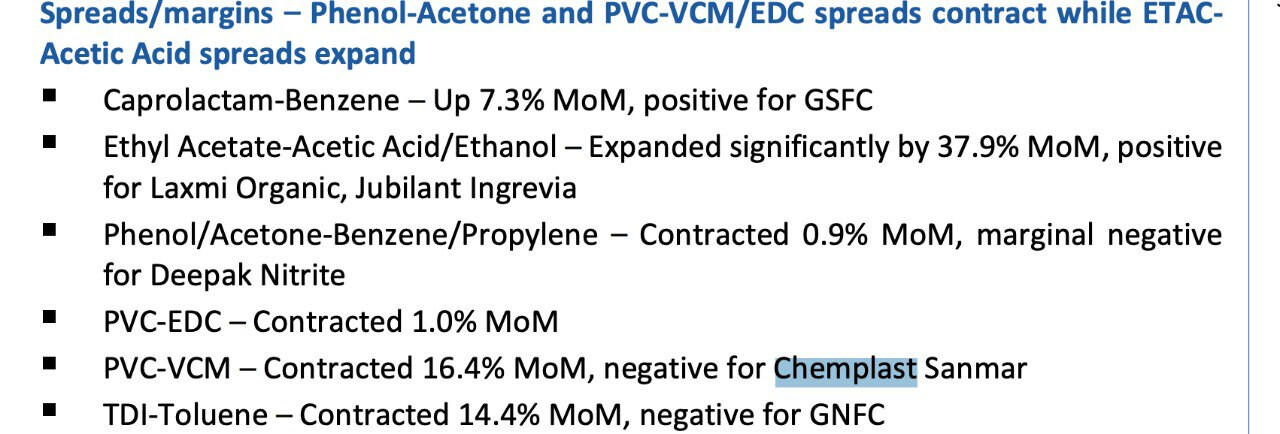

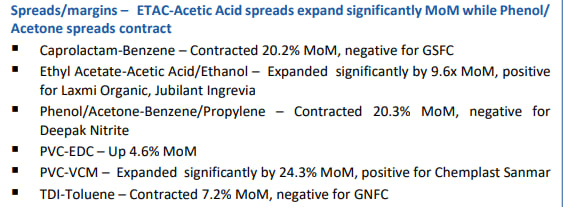

Chemical Pulse : Chemplast Sanmar +ve

Nov 2024

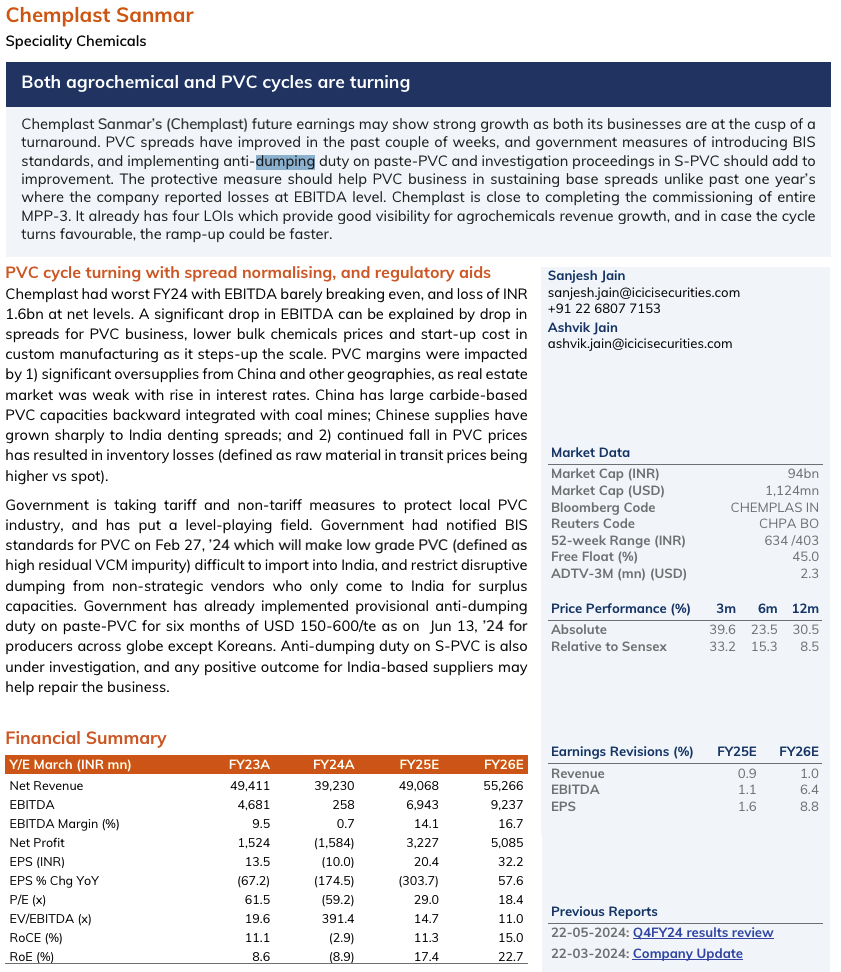

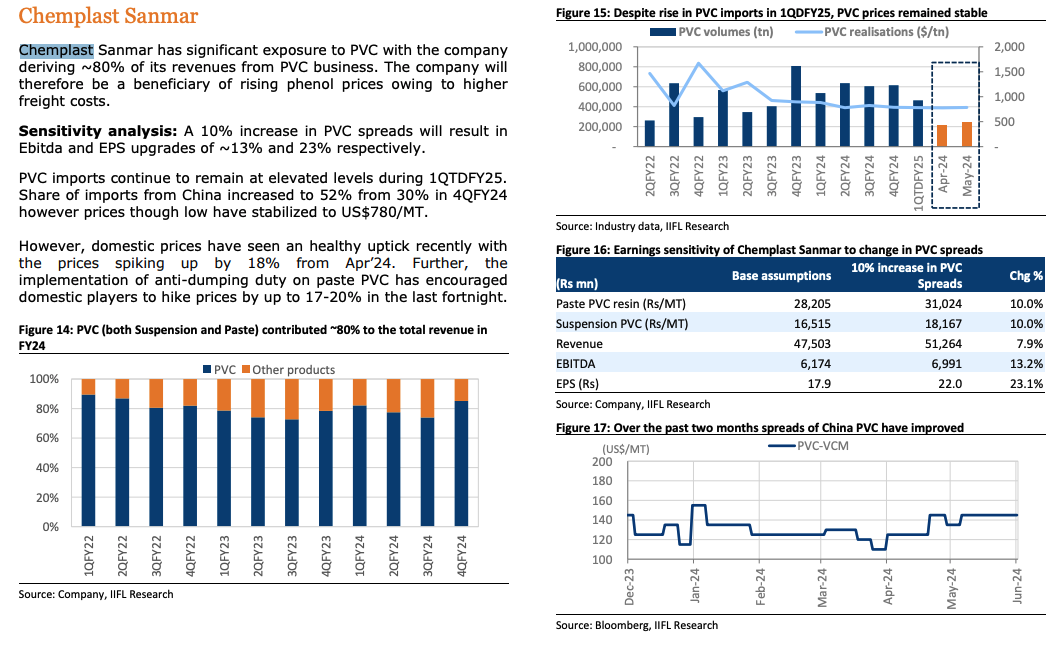

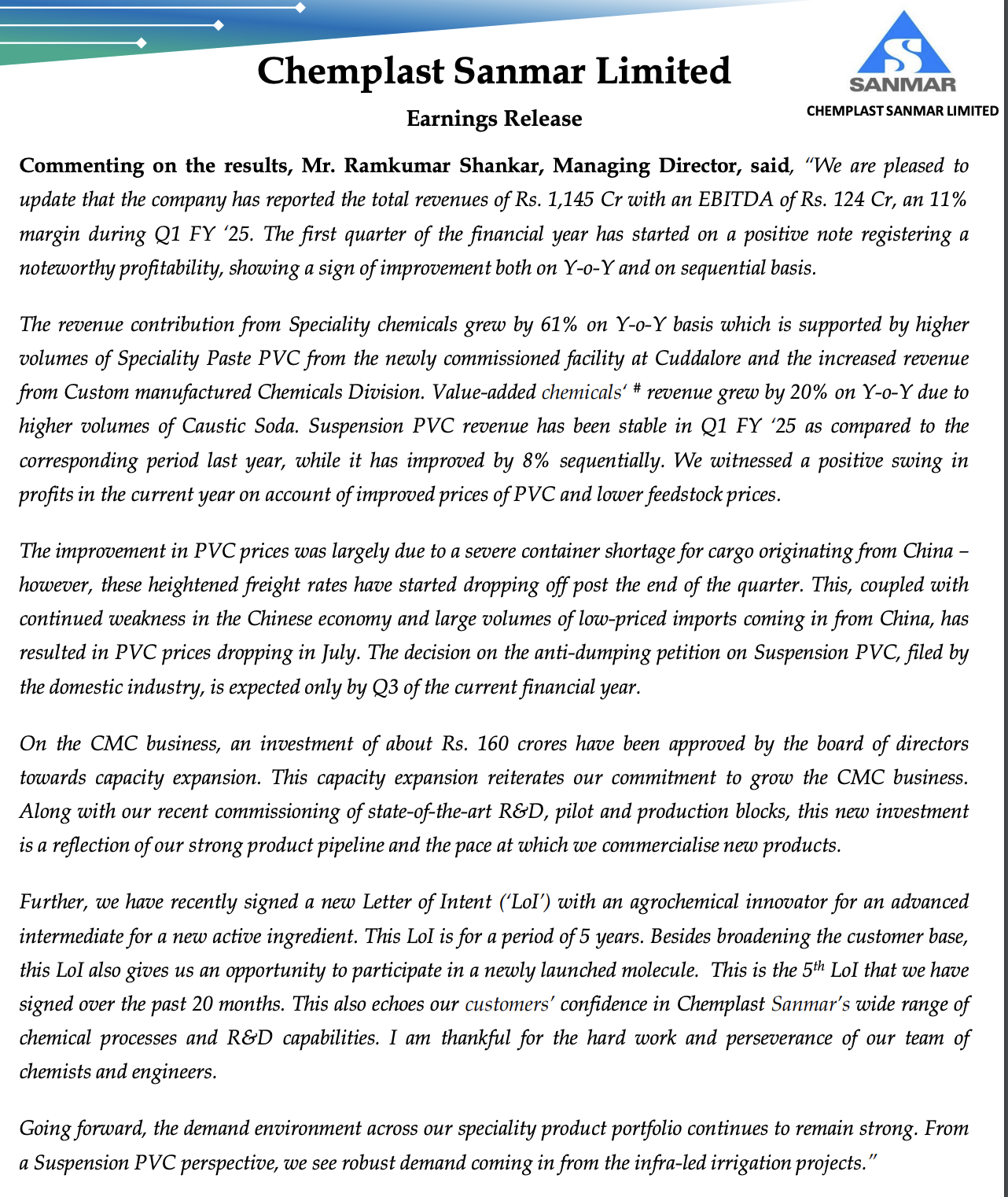

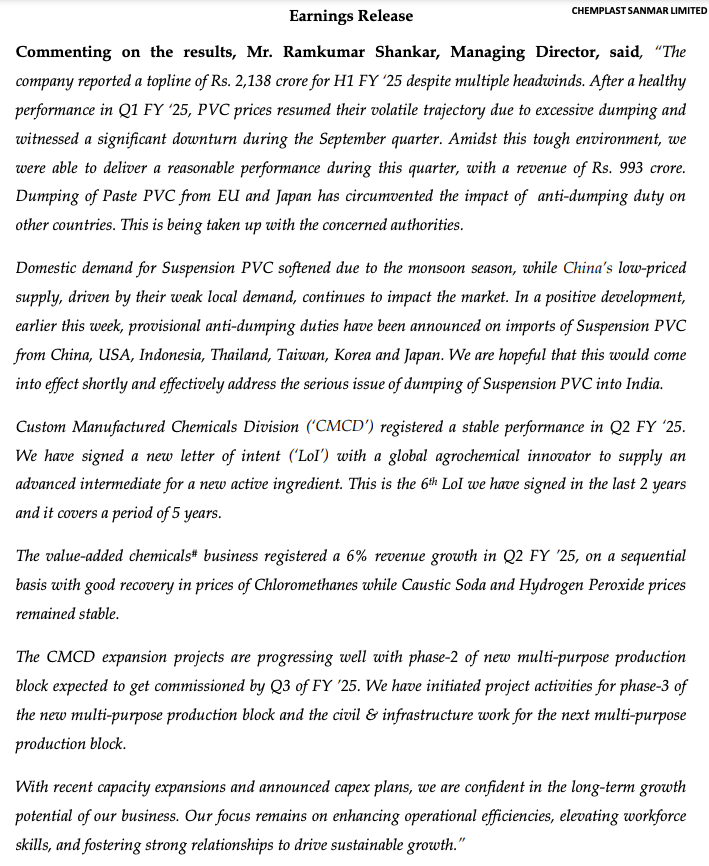

Q2FY25 results review

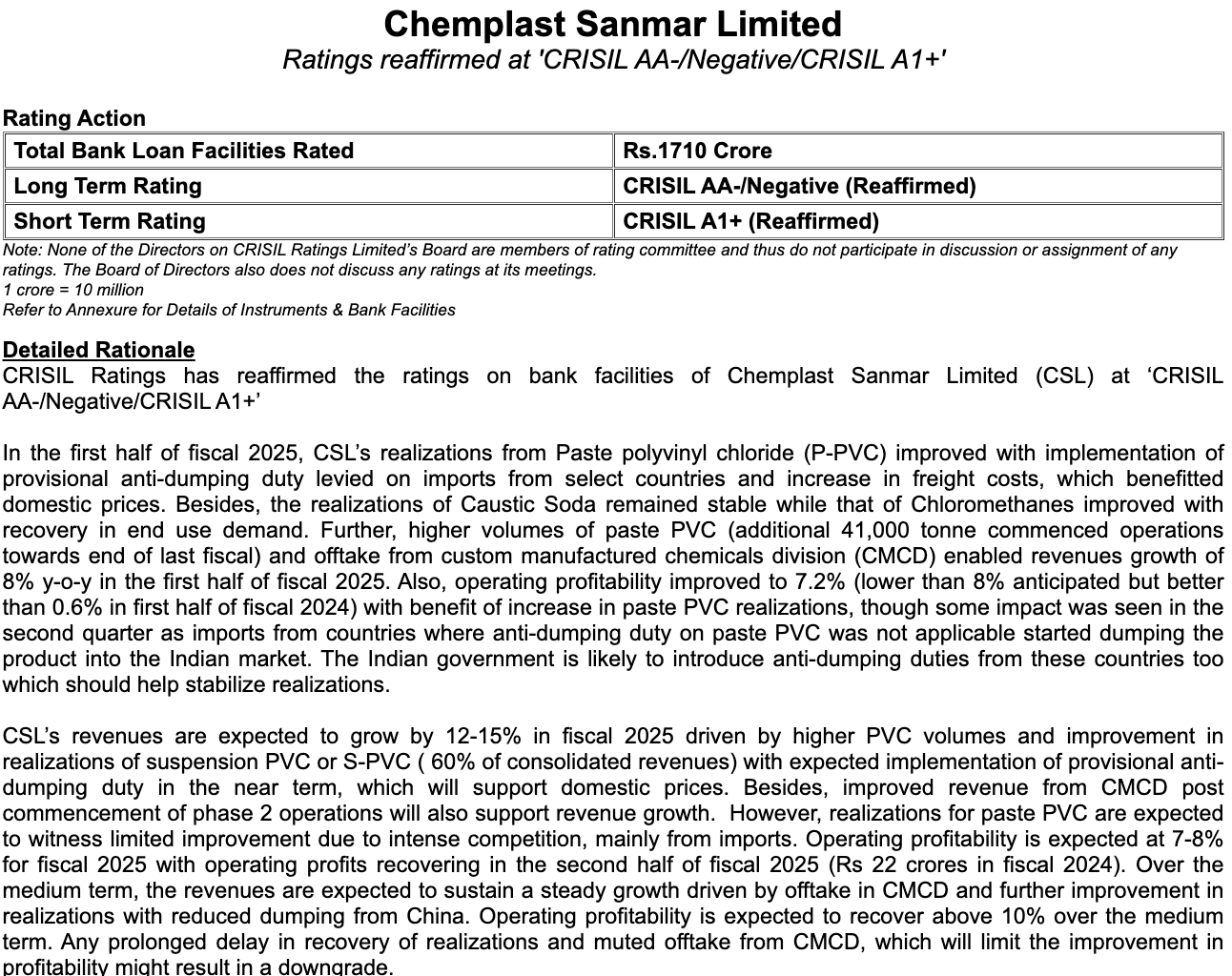

Chemplast credit rating upgrade

2 Likes

1 Like