This should help you. http://www.chemcrux.com/about.php under promoters section.

1 Like

I’ve been following Chemcrux closely for about couple of weeks.

Read the 2019-20 Annual report today.

Key learnings from AR for me:

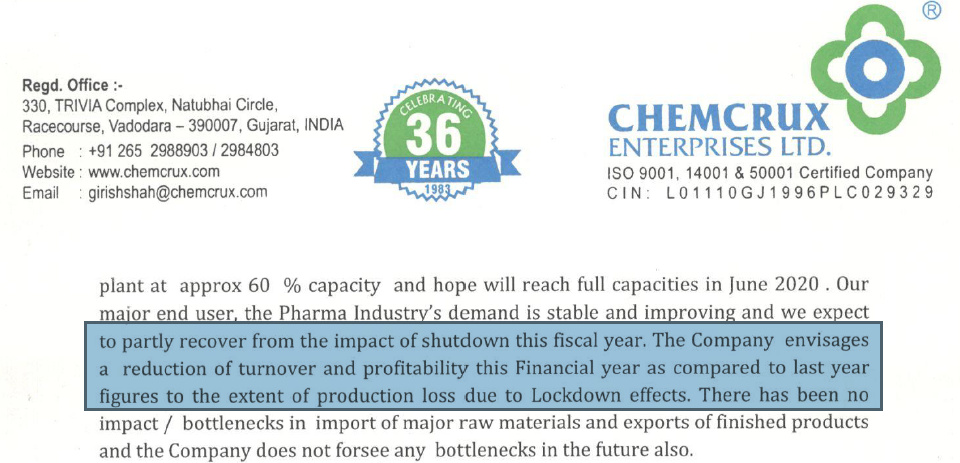

- For the current FY 2020-21, due to the global CoVID 19 pandemic situation resulting

into around two months complete / partial shutdown of operations, Company expects only marginal or no growth in turnover and revenue.

Sahil: This in turn implies that overall, modulo the 2 months lockdown, the company does expect growth in revenue. Im a bit puzzled by this because as per earlier posts company was already near 100% capacity utilization. The effective output for the 10 months would need to grow 20% for them to have same output as previous FY. Since the new capex will not come online for years, where would this growth come from? This seems puzzling to me. - The company expects secular growth for multiple years due to General global need to diversify the supply chain away from China, adding Tier 1, Tier 2 suppliers in India.

- The management talks about how Chemicals, among them speciality chemicals and among them API chemicals is a big opportunity space (200B$ in 2022) which is growing fast (expected CAGR of 6.4% between 2015 and 2022).

Sahil: The Fact that Chemcrux is a very tiny player in a large market means that they have enough and more room to grow and can comfortably continue to grow at even 2x or 3x industry growth for years to come, if not decade. - The company stresses on being a process-oriented company and thus its ability to maintain agility in terms of tackling appropriately various demand-supply conditions.

Sahil: While we have heard repeatedly about the company being process oriented, have we seen this in practice? Have we seen the company pivot away from products with bad demand-supply economics with agility in the past? Is the upcoming capex going to preserve this characteristic? - Volatility in the global prices of raw materials is also a major challenge

faced by the chemical industry. Sharp corrections in the crude oil prices and prices of various raw materials procured by the Company can influence bottomline.

Sahil: Going over screener data, it does appear like OPM has doubled from 12% to 25%. It is unclear to me what the mean OPM is and to what extent is it affected by crude oil prices.

My reasons for wanting to invest:

- With a 2.5x planned capex, there is clear growth visibility. Even conservatively, the earnings should become 3x over next 5 years.

- Company is largely poorly rated due to confluence off 3 factors IMO: Illiquidity, lack of trust in smaller companies, overall depressed valuations for smallcaps/midcaps.

- My analysis of end products reveals a clear growth of the overall industry.

My reasons for not wanting to invest:

- Inability to do position sizing: The fact that I need to buy 2000 stocks at once is a bit of a barrier. At this level, this would become my largest direct stock holding.

- The key risk is management’s ability to execute the capex. There has been talk of the capex in some form for about a year now. Also, it is still at EC. The overall feeling I get is that at this junction, given how starved we are for capex and growth as a country, the capex should come through. Since you have commented on this earlier and since you have a lot of experience working with younger/smaller companies, @ayushmit i was wondering if you could guide us a bit regarding how EC approvals generally work (if you have any insight). Do they generally come through? Is it tough to get EC? Is it only a matter of time?

- With the global economy recovering and crude prices rising, margins would be under pressure. As company has also noted in their annual report.

Overall, i’m still building conviction to take a position of this size in a small company (the two factors together make me a bit uncomfortable). If the probability of capex being successful were to become higher that would certainly provide me higher comfort in investing in this company.

11 Likes

Above two observations itself is a testimony of the company being “process driven” not “product driven”. Let me elaborate, I am with Chemcrux since IPO in March 2017. During FY18, there was factory closure for around 2 months due to pollution issue despite that, I was pleasantly surprised with the topline and bottomline growth in FY18. There was no capacity addition during FY18, capacity was almost 100% utilised both in FY17 and FY18 (follow AR), so the increased topline despite 2 months production loss in FY18 is a great testimony of the company being “process driven”.

Since the last 3 years, the company being “process driven” is successfully ramping up value added products with better margin. During FY19, they added capacity in the same existing plant which further fueled growth.

In my view, even without the proposed new capacity, the stock is grossly undervalued because last year they shifted their storage area which opened up further capacity addition possibility within the same plant. I had visited their plant and noticed how merely shifting storage area opens up the possibility of incremental capacity.

In future, if they receive EC clearance for new plant that would be a huge added bonus, even without that the stock price is not fully discovered as the minimum lot size of 2000 qty translates minimum investment of approx 3 Lacs+ which itself pushing away a lot of investors. On top of it, very low volume (not even traded everyday) pushing away a lot of serious investors those want to take large position.

P.E re-rating is expected once the stock moves out from SME segment with no minimum purchase qty restriction, don’t know when it will happen but sooner or later happen for sure.

Disc - Invested since March 2017

8 Likes

I was wondering if there is any set/documented process for stocks to migrate from bse sme to full fledged listing. Is it based on market cap? Is it based on number of years listed or any other such quantifiable metric?

Thanks for sharing your perspective. I will go through previous years annual report to find the evolution of products created by company demonstrating the process oriented nature of the company.

@prasenjitp04 since you have visited the plant, I was wondering if you have had the opportunity to meet the management (like CEO CFO c*o) and what your impressions were , anything which stood out of the ordinary and such?

1 Like

Check out the BSE SME website for detailed criteria.

Yes, I know the entire top management and also the factory manager. Top management looked down to earth, humble and have deep technical expertise in the domain.

Corporate office is in Vadodara while factory is in Ankleshwar. Thus, separately visited the factory in absence of top management. Factory manager (Vipul) is associated with the company since few decades (forgot the exact year he told). As per him, in his multi decades association he never noticed any significant fall in demand for the products, rather enquiries always remain higher than the catered customers. Also they are passing any raw material price hike to the end customers since years. The challenge lies in the expansion due to the clearance requirement of multiple authorities.

12 Likes

Here are my Observations from FY 17,18,19:

Annual Report FY17 2:

- Our Company always strives to cater the customized demand and our main focus is to cater the need of the Pharmaceutical Industry, Dyes Industry, Pigments Industry and our company has achieved target revenues with high level of customer satisfaction.

- The Company is in the continuous process of improvement of the existing products efficiencies and to cater to the need of the emerging demand which is in synergy of chemistries handled by the company.

- As you are aware, our Company was incorporated in April 1996 to undertake the business of manufacturing or processing of Bulk Drug Intermediates like Para Chloro Benzoic, Ortho Benzoic Acid, and Lasamide etc.

- Company being Process driven, rather than Product driven, gives strength to absorb sudden impacts, if any, on our various Product demands.

My Thoughts: there is a clear outline of products manufactured only to some extent: Para Chloro Benzoic, Ortho Benzoic Acid, and Lasamide. The benzoic acid part of the story has not changed.

Lasamide (C7H5Cl2NO4S) price in 2020 is 900-1000 Rs/KG. (Fun Fact, Lasamide can cause asthma if not handled well).

For comparison, price of Ortho Benzoic Acid is roughly 200-400 Rs/KG. This shows the existence of some value-added products indeed. I also went through a chinese Patent for How to prepare lasamide. I could not read it (not really) because google translation for PDF does not seem to work for this PDF/ I did use my phone’s google translate app to understand some of it. What is clear is that this is a result of the Chlorosulfonation process.

The price in US seems to be much higher. Although I do not know the authenticity of the website.

The additional question it raises is how the company is able to manufacture lasamide since it seems to be patented in 2015. Do they pay royalty to this chinese firm? Does the company use a process which is distinct/different from the patented process?

Annual Report FY18 3:

- Sahil: In this FY, company was only operational for 10 months due to reasons outlined in prasenjit’s previous post. The company put it as follows: “Your Company’s Revenue increased to Rs. 31.76 crore in FY18 as compared to Rs. 27.84 crore in previous year FY17 recording a remarkable growth of 14.06% (YoY) despite operational period of 10 months and volatile raw materials prices which have been well absorbed by higher sales volume and better product value realisation. “

- Your Company has progressively leveraged chemistry skills to produce higher value products, expanding capacities to optimal scale. The Company has placed a greater focus on better value added chemical processes.

Annual Report FY19 4:

- We plan to take our next step forward to expand capacities & diversify by creating additional production facility / acquisitions in domestic market. Keeping in view future expansion plans, Company has acquired land in GIDC, Ankleshwar, for warehousing.

- This will create space for further expansion in the existing plant. Company has also recently filed Environment Clearance application for further expansion of production capacity in the existing plant.

Overall Observations:

- Annual reports Do not have a lot of details.

- Annual reports are roughly the same over the years with some commentary on happenings of that year. I think this is also the par for the course for companies of this size.

@prasenjit I understand how the company was able to make up for the lost 2 months by essentially changing the product mix and going for higher margin value-added products. What i was wondering is whether there are any details available (either with you or publicly) about precisely what set of products in what proportion the company changed, in order to compensate for the loss of 2 months of revenue.

Overall, I can see the complexity in the value added products manufactured by the company. I wish the company would also disclose a little bit of information about how the product mix has evolved over the years, and such like, which provider deeper understanding of the company’s process driven culture.

As per the previously mentioned capex plan, which is available on EC website, I searched a bit for the specific products and used some average prices from zauba.com to project that IMO when the full capex happens (which takes capacity from 400 mtpm to 925 mtpm) it would increase sales from 55cr to 172cr. Here is the google sheet where I show my calculations.

Caveats on the Revenue Projection:

- Note that the revenue projection is based on a bunch of assumptions such as taking average price of individual products in a segment to arrive at average selling price of segment.

- Some prices on Zauba are out of date.

- I could not find prices for all products so had to make do with whatever i could find on zauba.com.

9 Likes

One of the criteria for transitioning to the Main Board is to have equity capital of more than Rs 10cr. Chemcrux is far lower than that. I don’t think the company is looking to transition any time soon. Investors can hope that the lot size is reduced.

1 Like

Hi Prasenjit,

Good to know about your insights on the company. Congratulations for picking the stock so early and doing good ground work. I have also been invested for sometime and what interested me here was the superb profitability the company has had along with really low valuations for last couple of years or so. Initially I was concerned if the same is temporary or if like other SMEs the nos have been bumped up however, the cash flows seem to be robust and the longer the company performs, it seems sustainable and gives comfort. Its interesting to see that unlike other API/intermediate companies, this one is getting majority sales from domestic market and its highly profitable. Based on some of my checks and insights, the company does has leadership in few products and has been able to innovate/early mover in few intermediates which were earlier imported from China and are very tough to make.

@prasenjitp04 - i saw name of one of the investor - “Sushila Arvind Chheda” - any idea about them? are they related to valiant?

The EC approval has been pending for long and has been an overhang for the stock. Any thoughts as to how can the company grow if the don’t get approval? I understand that even for doing brown-field expansion they need approval?

Other concern I have is - other than the 2 key management people - who are the other key employees? I see very low salary etc and remains a concern for long term growth and sustainability.

I agree with @sahil_vi - that very little details are available about their products or clients and company needs to open up and share these details. I also don’t see investments in R&D etc or details on future products.

Disc: Invested in family accounts.

12 Likes

Just to add to a couple of questions as per my limited knowledge

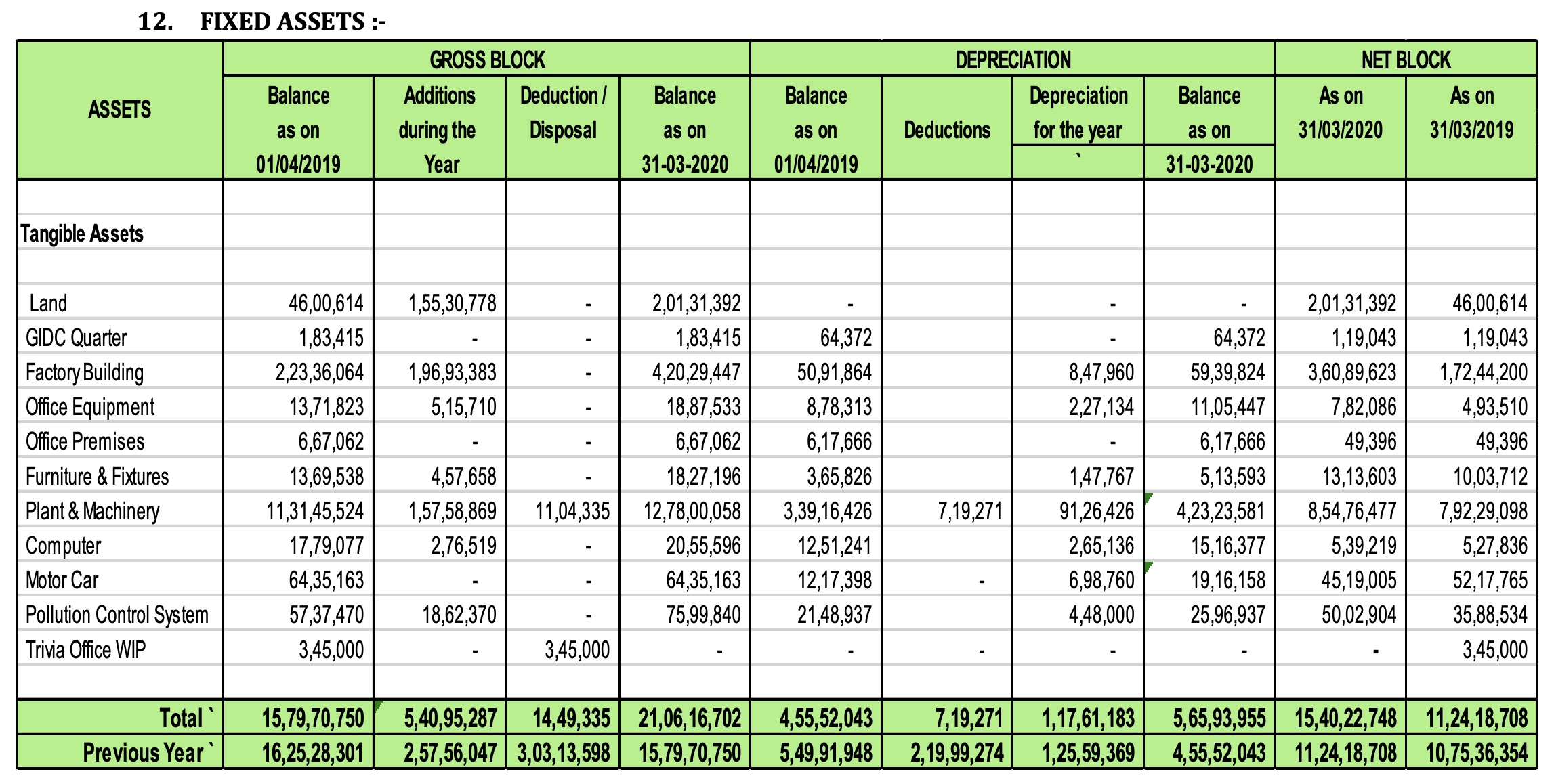

Going through note 12 of the balance sheet in AR 2019-20 we see:

it looks like the company quadrupled its land holding (50L to 2cr) and doubled its factory buildings in value from 1.7cr to 3.6cr. Could all of this be related to the capex they have been guiding for? If so, it appears that a lot of the physical assets (modulo the plant and machinery) have been acquired already.

All of this Fixed asset acquisition seems to show up in Asset Turnover Ratio as well, which has gone down from roughly 2.0 last year to 1.6 this year, meaning these are not productive assets (which makes me think that they are related to the planned capex).

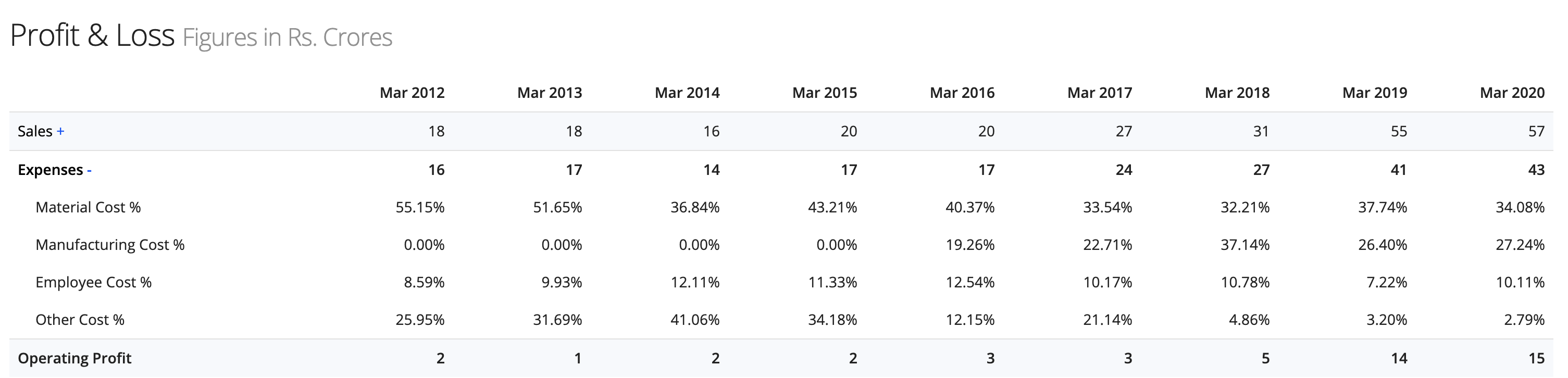

As per screener, the employee cost as a % of sales has remained somewhat stable at around 10% (it did dip to 7% in 2019):

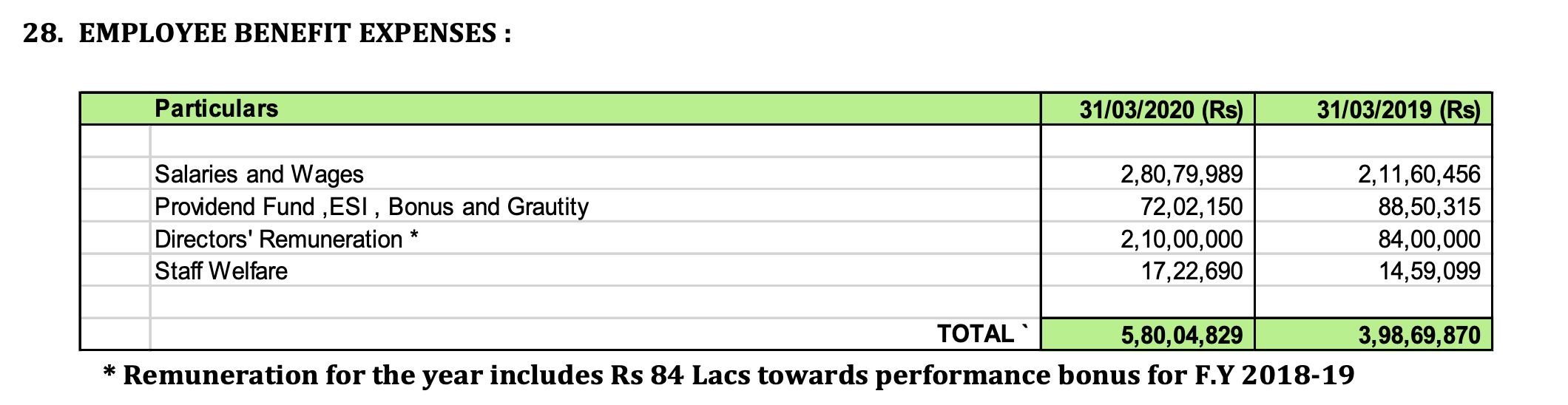

This is also visible in FY20 AR wherein employee costs are shown to jump roughly 40-50% compared to previous FY:

I Also compared the employee costs to other specialty chemical companies (listed as peers as per screener) and the percentages seem similar:

| Company | Employee Cost (% of Sales) |

|---|---|

| Chemcrux | 10.11% |

| Pidilite Industries | 13.79% |

| Aarti Industries | 5% |

| Sumitomo Chemical India Ltd | 10% |

| Vinati Organics Ltd | 6.35% |

| Godrej Industries Ltd | 6% |

| One caveat I’d add is that as per my understanding the salaries are a bit skewed wherein top management get much higher salaries than the rest of them. I believe this should be fixed in coming years as the company gets larger and is able to better balance out the salaries. |

6 Likes

True, this remains a concern. I asked this question during 2018 AGM but did not get a convincing reply. None of the next generation family members are involved in this. All board members are immediate family members of promoters with very little say in the operations.

Yes, nothing comes up in the AR. Though I wanted to but could not visit the plant during AGM visit due to less time, the customer list I have posted in the thread is sourced from some of the employees after talking to them. Otherwise there is nothing in the public domain.

It would be good to attend the online AGM this time and get some clarity on these questions.

Disc: Invested in 2017, sold all in Feb-2020. Reentered last month with a tracking position.

4 Likes

Yes, once equity capital reach 10cr+ then they can move to normal BSE segment with no limitation of minimum purchase quantity. There are two ways of it -

- Equity dilution through FPO or rights.

- More shareholder friendly way is bonus share issue. Many SMEs did that. Given the current reserves and surplus of Chemcrux, it won’t be a difficult task.

I don’t know when that happen, but sooner or later happen for sure and then the stock will command proper valuation.

Exactly, they carefully choose some import substitute niche products. Maybe this is the reason, factory manager (Vipul) told me that he never faced any demand concern or slowdown in enquiry. The challenge seems with the expansion not with the market demand.

No idea about them, but one interesting observation is, out of 49 Lacs odd shares, 73% is with promoters, 2% with me, 5% with my very close circle HNIs since 2017, another 3% closely held, leaving only 17% odd approx 8 Lacs shares, not sure out of that 8 Lacs shares how much is closely held! Wider equity base is required both for BSE main board migration and proper valuation. I will bat for bonus in the upcoming AGM.

They did expansion in FY19 within the existing premise. More than EC approval, I am betting on prudent product mix which was the growth driver for the last many years. I know, after some point, any company can’t grow topline merely prefering higher value added products but still besides EC approval and further capacity expansion, I am hopeful about growth due to prudent product mix and value added products

Sanjay Marathe and Girish Shah - they are the driving force of the company and all key decision makers. Apart from them, in my view, all remaining employees are in normal payroll (as of now). Few employees are associated with the company for decades but they are neither decision maker nor have ownership interest.

The company is too small for separating R&D division or any such. One of the promoter, Sanjay Marathe has in-depth technical expertise, R&D and product selection might entirely coming from his brain. Another promoter Girish Shah also has in-depth technical know how but mostly oversee marketing, customer relation and all other matters.

Another point I like to share is that, I had interacted with a lot of SME companies in the last 3 years and found Chemcrux management (Mr Girish Shah) is the only one that consistently “UNDER PROMISE - OVER DELIVER” while other SME promoters always promise tall! If you follow post FY18 management commentary (check BSE announcement during May 2018), you will find they talked about 30% growth guidance in FY19 due to expansion. However, they outscored their own guidance with approx 75% topline growth in FY19. Further, in last year during company visit, Mr. Girish Shah told me don’t expect similar 75% growth in FY20, rather guidance was no such growth in FY20. However, in FY20 topline registered 4.5% growth with 14% jump in net profit! Again in FY21 guidance they mentioned about the probability of impact in profitability due to COVID-19 lockdown and all. Let’s see whether once again they can outscore their guidance.

As per my experience, it is next to impossible to predict growth correctly for any small business (not talking about large companies) due to the ever changing business dynamics. I can’t say with assurity how much my own business can grow in the coming years as there are always a lot of moving variables. So, apart from large established business (like RIL, TCS, Infy etc), guidance from any small company should not be considered seriously. However, while a small company like Chemcrux always outscoring its own guidance, it requires serious attention and offers testimony about the management quality!

Disc - Invested since 2017

18 Likes

I won’t hold my breath. Some managements are minimal. I don’t see the transition to the main board happening in the next few months. For that matter, I don’t expect even the current lot size to change (unless mandated by SEBI rules or exchanges). I could be wrong but this is my belief.

This forum and everyone’s contributions have been very useful in me reaching the decision to invest in Chemcrux.

As a shareholder, I plan to email the company with a few questions gathered from this thread:

If someone would like to add to the questions or suggest modifications, please reach out to me for edit access or tell me via the forum or PM.

5 Likes

Newbie to valuepickr & investing here. I have been following this thread closely for a month and trying to gather as much data as possible. During the process, the share price skyrocketed to ~190 levels from 130. Tried to enter with faith around 150, but the order was not executed due to limited sellers. (Still not invested). The two things i worry most in this company is the expansion plan execution. As someone has mentioned here, the technical expertise mostly comes from one of the founders. It’s too much of a reliance in a single person and hopefully they nurture a team to take the company ahead. Also i am not familiar how a process driven expansion will span out, and constant switching of products as per market need will scale out. Another matter of concern is the limited information on raw materials and customer profile. Reading through the thread, they seem to have sufficient pricing power.

5 Likes

Environment Clearance

The question of environmental clearance is an important one for Chemcrux (since as ayush rightly mentions in an earlier post, EC rejection would result in capex being delayed by 2-3 years at least). I dug into this in some detail today and there are some very interesting findings:

- I started by going through the environment clearance website going over all requests filed in all years in Gujarat for project type “Industrial Project 2” the type which chemcrux filed their EC request under. No requests have been approved since 2019. In the district Bharuch (where ankleshwar is) itself, 3 requests are pending. This gives us some idea about the state of environment clearance in Gujarat.

- This seemed to be a bit surprising to me (No EC in last 1.5 years) and hence I googled a bit about Ankleshwar a bit. A few good readings that I found on the subject are summarized in the following points:

- Bharuch district and ankleshwar in specific has been a place caught between tug of war between industrialists and the NGT (National Green Tribunal) and Gujarat Pollution Control Board (GPCB). It has been this way for some years at least, with the Indian Drug manufacturers Associated creating a presentation in 2015 demonstrating what steps they had taken to reduce the pollution in Ankleshwar, requesting GPCB to lift the ban on expansion/diversification of APi manufacturers in Ankleshwar.

- In 2018 when NGT via its report published the CEPI (Comprehensive Environmental Pollution Index) for highly polluted zones in India. Ankleshwar was 88/100 (above 60 is considered to be dangerous) was one of the worst polluted places in India.

- As per this TOI article in sep 2019, bharuch district and ankleshwar in specific has been a place caught between tug of war between industrialists and the NGT (National Green Tribunal) and Gujarat Pollution Control Board (GPCB). The NGT report in 2019 had ankleshwar’s CEPI score at 80 (which is a reduction from the 88 last year) but the score was still above the NGT recommended level of 60.

- As per this recent July 2020 article in Business Today this kind of a tussle between industrialists and NGT has been happening all over the country. Supreme Court was hearing a case involving MOEF on one side and NGT on the other. The case involves a May 14, 2002 circular issued by the Ministry of Environment and Forests (MoEF) allowing “ex post facto” (retrospective) environmental clearances (ECs) to polluting industries. About the 2002 circular, the Pune bench of the National Green Tribunal (NGT) first held in January 2016, that it “is illegal, void and inoperative”. The MoEF and the affected industries challenged the NGT order in the SC. The top court’s April 2020 order upheld the NGT’s ruling that the circular granting ex post facto environment clearance is “unsustainable in law”. The apex court declaring “ex post facto” environment clearance illegal is just one part of its order. It struck down two other key orders of the NGT: (i) revocation of green clearances and (ii) immediate closure of the polluting industries (three pharmaceutical companies operating in Gujarat). Why? It said: “The directions of the NGT for the revocation of the ECs and for closure of the units do not accord with the principle of proportionality.”

- As per what I can see online, the AQI for ankleshwar is not that bad. It is at 55. It has been similarly low for about a month. This reduction could possibly be due to the lockdown (it is likely most industries are operating at < 100% capacity utilization). One will have to monitor this over the next few months to understand how the situation is on the ground in terms of pollution levels.

the TL;DR is that this is a highly complex issue with ankleshwar at the center of it. As an aside, I had observed earlier how Chemcrux had adopted the Green color very much for their AR since FY19. In fact environment and energy conservation find special mention in their AR in last few years. This is (as far as I can tell) representative of the management’s focus on ensuring full compliance with all environment regulations.

Based on my findings, I’ll appropriately modify the questions I seek to ask the management.

As of right now I won’t modify my investment. Chemcrux is a good company for investing in. This specific capex might face EC headwinds, but it is difficult to stop a small company which wants to do capex from expanding. The long term investment thesis is still valid, this investigation just highlights the focus that current systems have on being environment friendly and how companies need to adapt in order to comply with existing regulations.

20 Likes

hi

i would like to add that

- As per EIA notification of 2006 which lays down the process for obtaining an EC. A project is issued a ToR ( terms of reference ) by expert appraisal committee for which a project needs to prepare a EIA draft.

a EIA report is used for conducting public consultation with the communities who would get affected by the project. The concerns raised during the consultation are incorporated into the EIA report.along with mitigation measures for those concerns before finalizing the report.

Any project needs to carry out the public consultation process as per the EIA notification, which consists of two elements- conducting an onsite public hearing and inviting written responses from other stakeholders. The list of public hearings are on the GPCB website.

1 Like

The recent update about chemcrux on GPCB

Minutes_498th_SEIAA_Meeting chemcrux.pdf (62.4 KB)

6 Likes

Hi All, What does “Terms of Reference” order means?