Chemcon Speciality Chemicals Ltd is in the process of listing right now, with IPO closing on 23rd Sep 2020. With Spec Chem being the flavor of the season, decided to have a in-depth look at this one to find if its a red herring just riding the wave, or if it can deliver true value over long term.

Company Background

Incorporated as Gujarat Quinone Private Limited at Vadodara, Gujarat on 15 Dec 1988. Current promotors incorporated Chemcon Engineers Pvt Ltd in April 1996. They acquired 100% in Gujarat Quinone and merged the 2 companies and renamed entity as Chemcon Speciality Chemicals (CSCL)

CSCL is engaged in the business of manufacturing, marketing and supplying of the Pharmaceutical Chemicals and the Oilwell Completion Chemicals.

CSCL is an ISO 9001:2015 certified company. Its manufacturing plant is located in Manjusar, near Vadodara.

Products & Applications

CSCL product portfolio consists of Pharmaceutical Chemicals, mainly HMDS & its ancillary chemicals and CMIC

Oilwell Completion Chemicals, namely Calcium Bromide (solution and powder), Zinc Bromide (solution) and Sodium Bromide (solution and powder)

HMDS is important intermediates for API of life saving Antiretroviral (ARV) drugs used to treat HIV / AIDS and Direct Antiviral Action (DAA) drugs for Hepatitis B & C

HMDS is also an key intermediate for 2nd Gen Cephalosporin antibiotics which are used to treat variety of conditions in Bronchitis, Ear infections, Skin infections, bacterial infections, and infections of ear, lung, throat and urinary tract

Similarly, CMIC too is an critical intermediate for API of HIV / Hepatitis B & C drugs

Its Bromide family of Oil well chemicals are used preparation of Oil wells during oil & gas exploration

Business Analysis

Since the company is in listing process right now, financial data is available only for limited period of FY17, FY18 and FY19 in DRHP document.

Although CSCL has a limited basket of products, it seems to be well positioned in the market for these products.

In HMDC, it is the ONLY manufacturer in India, and the 8th largest producer in the world, as of FY18

For CMIC, it is the LARGEST in India, and the 2nd LARGEST producer in the world

Thus, it has been very successful establish itself within its niche, within a relatively short period of time

Industry-wise Revenue

As of FY19, Pharma contributes almost 2/3 of the revenue and remaining 1/3 is contributed by Oil Well Completion Chemicals business

A minuscule part of revenue comes from other industries such as semi-conductor and rubber. A very small amount of revenue comes from services

Segment

% of FY 19 Revenue

% of FY 18 Revenue

% of FY 17 Revenue

Pharma Chemicals

62.99%

61.97%

46.89%

Oil Well Chemicals

35.42%

35.86%

50.53%

Others

1.59%

2.17%

2.58%

Product-wise Revenue

As of FY 19, almost 40% of its revenue comes from its biggest product, HMDS

Bromide family of products contribute about 35%

CMIC contributes about 15.65% revenue

Domestic Vs Export Revenue

Revenue from domestic sales in FY19 is 196 Cr (64.67%), up from 24.2 Cr in FY17 (26.95%)

Revenue from exports in FY19 is seen at 98 Cr (32.22%), up from 58.5 Cr in Fy17 (65.08%)

Between FY17 and FY19, CSCL has demonstrated a very strong growth in both domestic as well as exports sales

While its total revenue has grown to almost 4 times in these 2 years, its export sales have grown to over 1.5 times, while the domestic sales have grown almost by a massive 8 times in this short period

Market Share

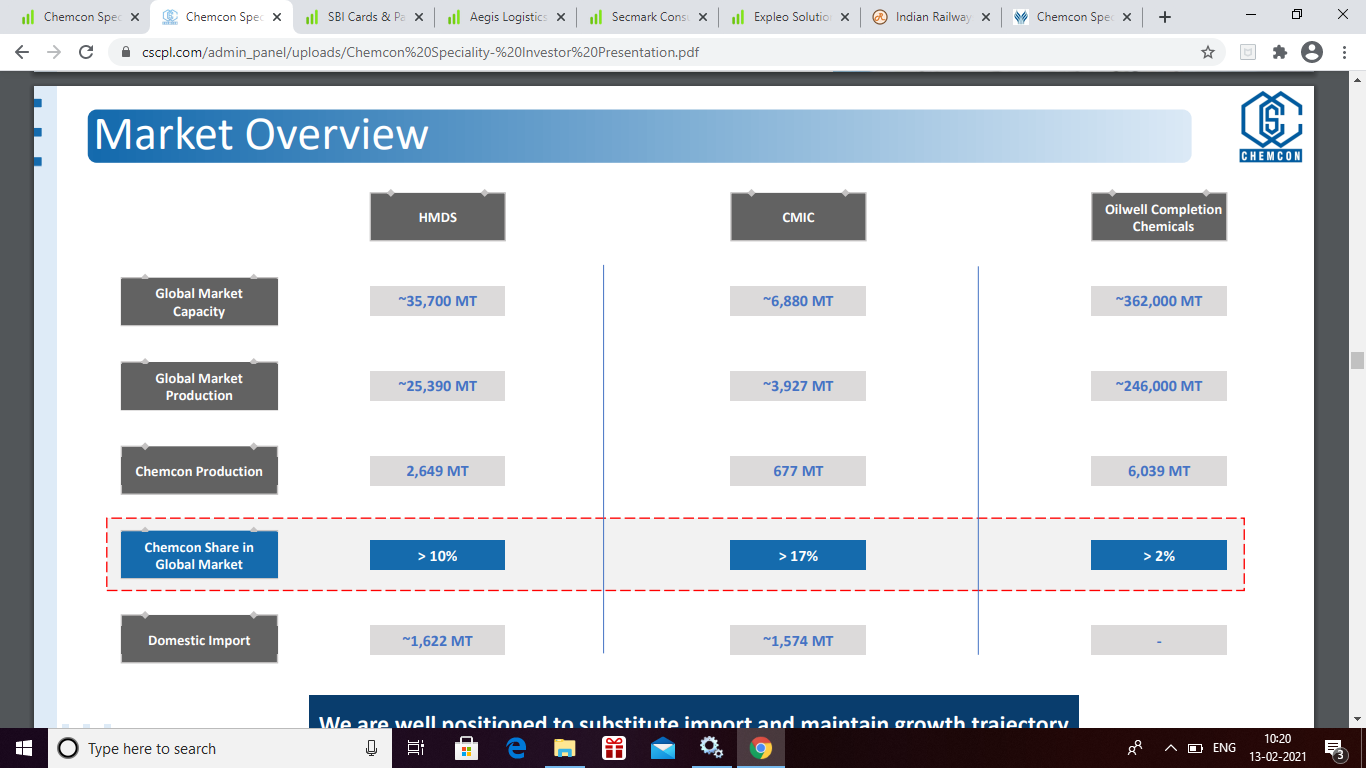

CSCL is India’s only HMDS manufacturer, and 8th largest globally. It has a global market share of 5.61% in HMDS. Its India market share in HMDS is 47.9%

It is also India’s top manufacturer of CMIC, and 2nd biggest globally. It has a global market share of 28% and domestic market share of 50.4%

In Oil well chemicals (Bromides), its market share is very small, 2.66%, though it is 6th largest manufacturer of such chemicals in the world. What is commendable though, is that till year 2013, CSCL did not even make these products, so it has done relatively very well to get this market share in a short span of 7 years.

Capacity & Utilization

CSCL has a total installed volumetric capacity of 236 KL. These are spread across 6 manufacturing plans at their single manufacturing site in Vadodara

Of the 6 plans, 1 is dedicated to making HMDS, 2 are for CMIC, 2 are for Oil Well Chemicals. One plant for HMDS was damaged in fire accident in 2018, and they are rebuilding it.

Total installed capacity is at 2400 MT for HMDS, 1800 MT for CMIC and 14,400 MT for Bromides solution and 600 MT for Bromides powder.

Current utilization (FY19) for HMDS is 93%, for CMIC is at 95% and for Bromides is at 57%

As per plan, IPO proceeds (fresh sale of 165 Cr) will be utilised for CAPEX for 3 new plants (46 Cr), shared infrastructure and Working capital (90 Cr)

All the 3 new plants will be dedicated to making of pharma chemicals i.e. HMDS & CMIC

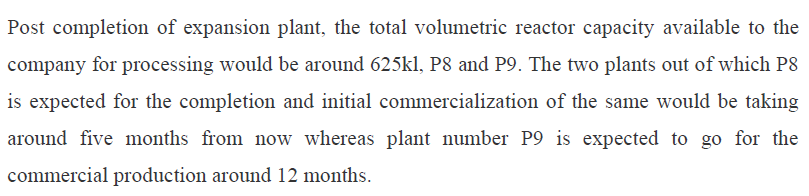

The new plants will add new volumetric capacity of 376 KL. Along with restoration of plant lost in fire incident, the total capacity will rise to about 625 KL, more than doubling from current installed capacity.

Growth Runway

As per Frost & sullivan report, HMDS demand in India is projected to grow at CAGR of 5.6% in next 3 years. India is currently net importer of HMDS, with 52% of its demand in 2018 met by imports, mainly from China. Chemcon is the only HMDS manufacturer in India. Hence, by substituting imports and catering to India’s HMDS market, Chemcon has an opportunity to grow at a CAGR of ~20% between 2018 and 2023 in the HMDS Segment.

India and China are the ONLY 2 countries in the world to make CMIC. India has 45% market share, and China has 55% market share of global production.

India has the largest demand for CMIC, with 65% of global consumption. This demand is growing very fast. CMIC is critical input for HIV / Hepatitis B life-saving drugs. Demand for these drugs has been rising due to lowing prices and rising demand for better healthcare.

As per Frost & Sullivan report, global demand for CMIC is predicted to grow at CAGR of 12.5% between 2018 and 2023, with demand in India expected to grow at 14% CAGR in the same period. Currently, India is a net importer of CMIC, with 50% of its demand being met through imports from China.

Chemcon being leading producer of CMIC in India, is well positioned to substitute imports from China and hence has an opportunity to grow at a CAGR of more than 25% in CMIC segment between 2018 and 2023.

With planned CAPEX will double the capacity in lucrative pharma chemicals (HMDS, CMIC). Thus, post-expansion, CSCL will be in great position to grow its revenue by meeting the rising demand of HMDS and CMIC

If CSCL is able to achieve its expected growth CAGR of ~20% over next 3 years in HMDS & CMIC segment (currently 62%+ of its revenue ~200 Cr), it can easily double its revenue from the pharma segment in this period, to about 400 Cr

Competitors

In HMDS, its leading competitors are Dow Chemicals (18.19% global market share), Xingyaqian Silicon (China, 20.68% market share), Zheijiang Sorbo (China, 10.22% share), Shin-Etsu (Japan, 10.44% share).

In CMIC segment, Shanghai Twisun leads with a global market share of 33.46%, followed by Chemcon, trailed by Anshul Speciality (India, 11.26% global share) and Inner Mongolia Saintchem at 14.8% share.

In Oil Well Chemicals segment, its biggest competitors are Israel Chemicals Limited, Albermarle, LANEXESS, TETRA and PPC.

However, since it has no competition from any of the global majors in India, it maintains massive market share in domestic markets (HMDS 47%, CMIC 50%), while rest of demand is met through imports.

With domestic demand expected to grow at healthy pace in both HMDS and CMIC, CSCL can continue to expand at a much faster pace by substituting imports

Competitive Moat

Substantial market presence in HMDS segment. India’s only producer of HMDS and 8th largest in the world

India’s largest and 2nd largest globally, with a dominant global market share of 28%

Speciality Chemicals industry has high barrier to entry due to several reasons

a. Involvement of complex chemistry in manufacture of products, which are difficult to commercialize on a large scale

b. Long gestation period to be enlisted as a supplier with the reputed customers of Pharma industry and Global chemical groups

Industry is highly knowledge intensive

Given the nature of the end application of products, the processes and products are subject to and measured against high quality standards and very stringent impurity specifications. These are extremely difficult to achieve for new entrants

Since the intermediates are used in API manufacturing, reworking of regulatory approvals required by them on change of suppliers is very time consuming and costly, resulting in customer sticking to proven suppliers, thus making it very difficult for new players to enter

Some of the products used in manufacturing of Speciality chemicals are corrosive and toxic, and handing these materials requires a very high degree of technical skill and expertise, the operations involving these have to be undertaken by well trained and experienced personnel, which is not easy to obtain.

Obtaining environmental clearances from government agencies to set up and expand capacities for manufacturing these chemicals is time-consuming and difficult process. Even for established players, obtaining permission often proves to be elusive. New players thus find it very difficult to get a foot-hold

Financials

Revenue is growing at a break-neck pace, rising almost 4x between 2017 and FY2019, at a CAGR of 83.95%, up from 89.8 Cr in Fy17 to 304 Cr in Fy19. DRHP document does not contain financials of FY20, but from unconfirmed data available on various sites, the revenue for Fy20 has fallen by about 10% to 266 Cr, even though PAT has improved to 48.8 Cr in FY20, compared to 43.08 Cr in Fy 19.

EBIDTA in the same period (FY17 - FY19) has grown from 86.6 million to 679.21 million at a CAGR of 180.06%. PAT has jumped from 28.24 million in FY17 to 430.41 million in FY19, growing at CAGR of 290.39%

Decent balance sheet, with negligible debt and leverage. Inventory levels have shot up, but given the explosive growth in sales in last 2 years, its in line. Similarly receivables have shot up almost doubling over last 1 year, but given that revenue has doubled too.

RoE and RoCE for FY19 are seen at 44.94% and 43.37%

Receivable days are pretty high at 106 days, almost doubling from 56 days seen in previous year. This is clearly a concern.

Cash flow from operations has declined slightly to 113.71 million, down from 139.97 in FY18. Decline has mainly been due to steep rise in Inventories and trade receivables

Promotors

Promoters of the CSCL are Kamalkumar Rajendra Aggarwal, Navdeep Naresh Goyal and Shubharangana Goyal. Promotor group consists of another 15+ names in what looks like extended family / associates

The promotors have a stake in another listed company in India - Overseas Synthetics Ltd, and several other unlisted ventures, 3 of which qualify by SEBI’s definition as Group companies.

All the 3 unlisted companies have very ordinary performance. One (dealing in industrial linings) has a revenue of 19 Cr and meagre PAT of 0.5 Cr, another one (dealing in technical textiles) has a revenue of 6 cr with a profit of 0.8 Cr. Third one (dealing in real estate), has zero sales and a small loss of 0.3 Cr. The listed entity Overseas Synthetics, has had zero sales for the last 4 years, and practically nothing for past 10 years!!

There are some negative observations relating to these companies. In SILPL, it has granted unsecured loans to another promoter venture without clarity of interest rate and repayment terms. In case of Supertech Fabrics, there is dispute / law suit contending the purchase of a land parcel. In Kana Real Estate, the networth of the company has been fully eroded.

There are couple of additional significant Red Flags about the promotors

Kamalkumar Rajendra Aggarwal, Shubharangana Goyal and Navdeep Naresh Goyal and certain members of the Promoter Group, namely, Naresh Vijaykumar Goyal and Minal Kamal Aggarwal (collectively, the “PG OSL Shareholders”), have filed a settlement application dated March 10, 2019 with SEBI in relation to their inadvertent failure to make certain disclosures required under the Takeover Regulations and the SEBI Insider Trading Regulations in relation to their holdings in Overseas Synthetics Limited (“OSL”), a company listed on BSE Limited, which is a member of the Promoter Group.

Further, pursuant to a criminal complaint (“Complaint”) filed by the Central Bureau of Investigation (Jaipur) (“CBI”), the CBI Special Court, Jaipur (“CBI Court”), vide an order dated December 24, 2018 (“CBI Court Order”), has convicted and sentenced inter alia a member of the Promoter Group, Naresh Vijaykumar Goyal (in his capacity as a director of Super Scientific Works Private Limited) to (i) rigorous imprisonment for two years with a fine of ₹10,000 for commission of offences under Section 120-B of the Indian Penal Code, 1860; and (ii) rigorous imprisonment for three years and fine of ₹ 20,000 each for commission of offences under Section 13(1)(d)(ii) of the Prevention of Corruption Act, 1988

So, other than the success of CSCL itself, the track record of the promoters across their other ventures is not too flattering, and can be termed as moderate at best. Probably, the presence of 2 non-promoter, whole-time Directors contributes immensely to the success of CSCL over last 20 years. Mr Himanshu Purohit, who holds a master’s degree in inorganic chemistry, has been with the company for last 20 years, and is currently Director – Production, taking care of critical functions such as Product Development, Production, and Material management. Similarly, Mr Rajesh Gandhi, CFO and Whole-time director, has been with the company for 20 years, and is in charge of key functions such as Finance & accounting, Export-Import, Compliance etc. Together, they seem to have played a key role in the success of CSCL.

Risks

Promotor Risk - With the red flags noted above, it remains to be seen whether the promotors are clean and also given the performance of other group companies, CSCL remains the only exception which is successful.

Raw material import risk: CSCL is heavily dependent on imports for its raw materials. As of FY19, 50.89% of company’s raw materials were imported. This exposes it to cost escalations due to currency exchange fluctuations. Also, a large part of its raw materials are sourced from china. Given the recent escalations in border dispute between India and China, any trade relationship breakdown / embargo between the two countries will have a big material impact on revenue and profitability of CSCL.

Product Concentration Risk : As of now, 40% of CSCL’s revenue comes from one product – HMDS, used mainly for its applications in pharmaceutical industry. Revenue of CSCL depends on success of its customers end-products. Any change in that will have a very big impact on CSCL’s revenue and profitability.

Industry Concentration Risk : CSCL relies on Pharma and Oil and Gas Exploration industry for almost all of its revenue. Any down-cycle or headwinds experienced by these industries will have a very massive impact on CSCL’s revenue and profitability.

Customer Concentration Risk: As we have already seen earlier in this analysis, CSCL has massive dependence on its top 5 and top 10 customers. Any negative turn in relationship with any of these customers will have an immediate large impact on revenue and profit of CSCL.

Regulatory / Environmental Clearance Risk : Obtaining environmental clearance in India is difficult. Any delays / problems in getting clearance for capacity expansion can have a direct and material impact on the growth and financial performance of CSCL.

Execution Risk : If CSCL fails to execute on its strategy, failing to utilise the growth potential, it may have a big impact on its financials.

Market Risk : If the growth in demand for CSCL’s customer’s end products does not rise as expected, it would have a significant impact on financial performance of CSCL.

Conclusion

Just looking at the business in isolation, CSCL has found itself a very profitable and unique niche. With critical end-use of its products and rising demand, it looks to be on a unhindered growth path for the next 2-3 years. It has got itself in leadership position in its product segment within India and has made an impact globally as well.

Growth Opportunity – With projections from Frost & Sullivan report indicating strong growth for its products in next 3 years, CSCL finds itself in an exciting space. Barring some extreme internal mismanagement or an external black swan event, it looks to be on track to achieve significant growth and leverage on the growth opportunity available to it.

Promotor / Management Quality : CSCL Promotor quality is not top-notch, with several of their side ventures not being successful. Presence of couple of red flags (indicated in this report earlier) does not inspire confidence either. Though they have been in this domain for many years, they have not demonstrated innovation. Hopefully, the professional executives in the management team continue to drive the company to success, as they have done in recent past.

Drop in Fy20 revenue, though small (about 10%), rising inventory days, rising receivable days etc are concerns, so those have to be closely monitored.

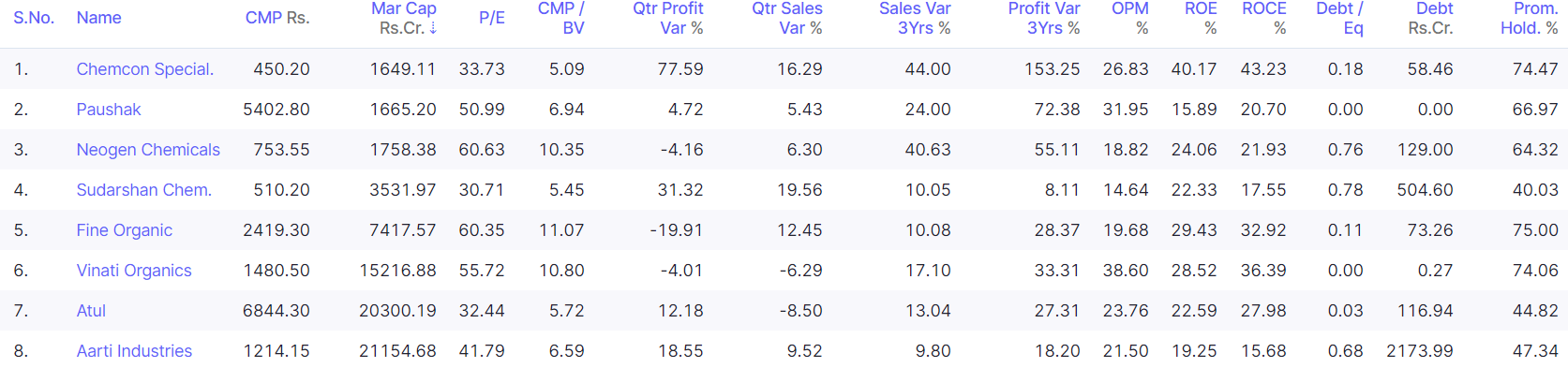

Basis of current valuation assigned for IPO, at Rs 340, the stock is fairly valued at PE of 22.15 on trailing FY20 earnings. Given that other peers in Spec Chem space are commanding richer multiples in excess of 30, and also given the current IPO frenzy, this is likely to see good listing gains.

I plan to take a very small tracking position, and will watch it closely to see how its plays out, especially given the growth potential of the products and the less than inspiring management.

Yes, Price to Book valuation is definitely high. Its a larger issue in a way, as to how market has been valuing the Spec Chem stocks in general in recent years. So Rossari, the other blockbuster IPO this year in spec chem space is being valued at 21.8 times book value, Vinati is sitting at 10.69 times, Alkyl Amines at 12.4, Black Rose at 9.79 and Navin, Aarti and Atul at relatively modest 7.6, 6.09 and 5.9 times book value respectively. Ideal situation would be to enter Chemcon (or any of the other names mentioned here) at much lower levels. Whether the market gives such an opportunity or not, only time will tell. I would prefer waiting for correction to enter at lower valuation.

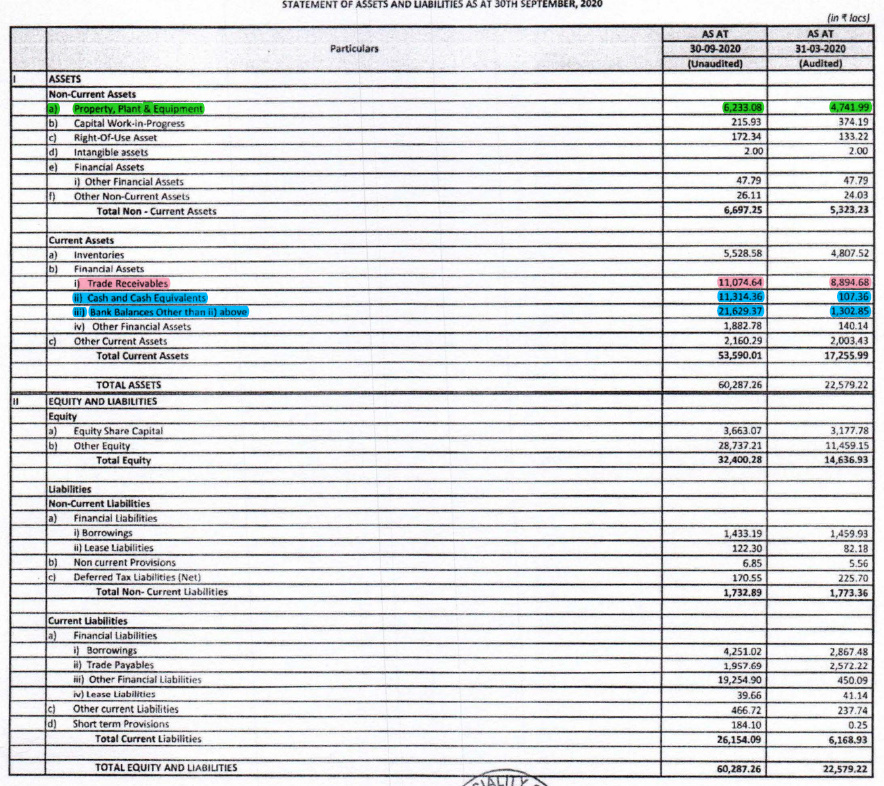

PPE has gone up from 47.5 Cr to 62 Cr, a rise of about 15 crores. Not sure what this is and where has it been spent. Cash flow statement validates the expenditure, but there are no specific details. Since the company got listed recently, there is no annual report of previous year to validate this from.

Receivables are continuously mounting year after year, and now stand at 110 crores. Similar trend is seen in the past years too. Corresponding figures for FY17, FY18, FY19 and FY 20 are 22 Cr, 29 Cr, 64 Cr and 89 Cr respectively. Between FY17 to FY19, there was an explosive growth, where sales grew from 89 Cr in FY17 to 304 Cr in FY19, so there was some justification for receivables to grow. FY20 sales were down by about 14% to 262 Cr. H1 FY21 sales stand at 107 crores, compared to 154 Cr in H1 FY20, down by over 31%. When seen in this context especially, the steep increase in receivables (23.6%) in a span of 6 months is alarming.

Just to put the intensity of receivables in perspective - At 110 Cr, its practically at 42% of FY20 sales of 262 Cr. Worse still, for the current year, it exceeds the H1 revenue of 107 Cr!!

Though the receivables are rapidly going up, the payables are moving in the opposite trend. We see a reduction in payables from 25 Cr in Mar 2020 to 19 Cr in Sep 2020. So while company is increasing its receivables rapidly, its reducing its payables rapidly too. This will surely mean a marked increase in working capital requirements.

Debt stays steady at around 14 Cr, reducing marginally in last 6 months.

Cash & Cash Equivalent have increased from 1.07 Cr to 113.14 Cr. Similarly the next item, bank balances too shows a sharp jump from 13 Cr to 216 Cr. These spikes are primarily due to the IPO which company floated in last week of September 2020. The IPO collected about 318 Cr, of which promoters offloaded shares worth 153 Cr through OFS component, while there was a fresh issue of 165 Cr. So about 153 crores collected on behalf of the promoters’ OFS sale. Of remaining, 165 crores is to be utilized as proceeds from IPO. Of this, company’s plan is to utilize about 45 cr for expanding capacity, and about 90 Cr for working capital, and the remaining for other corporate purposes. The company got listed only on 1st October, hence the funds show up on the company’s books as of 30 Sep 2020.

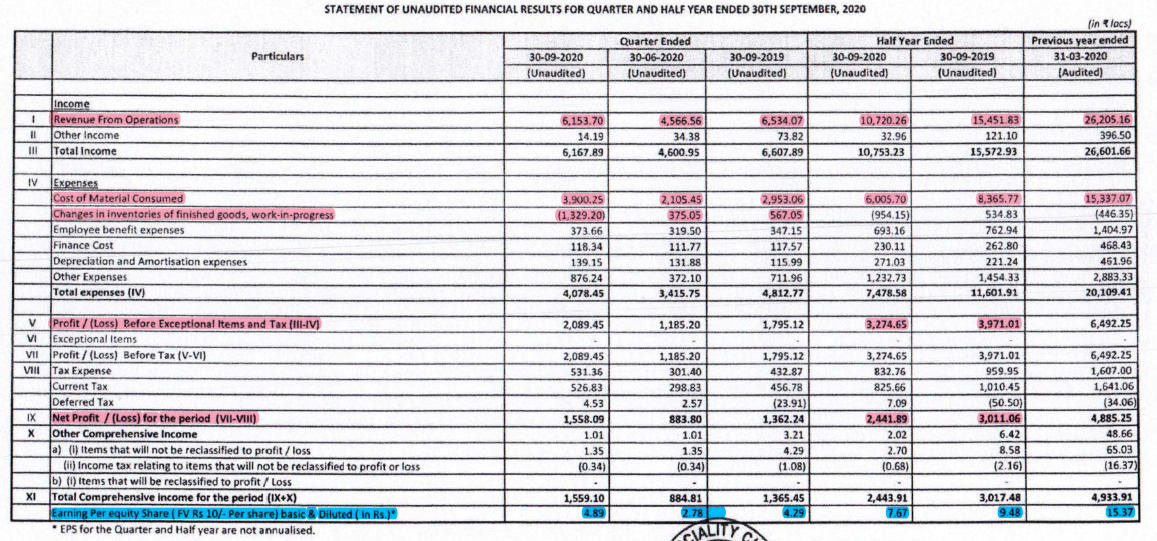

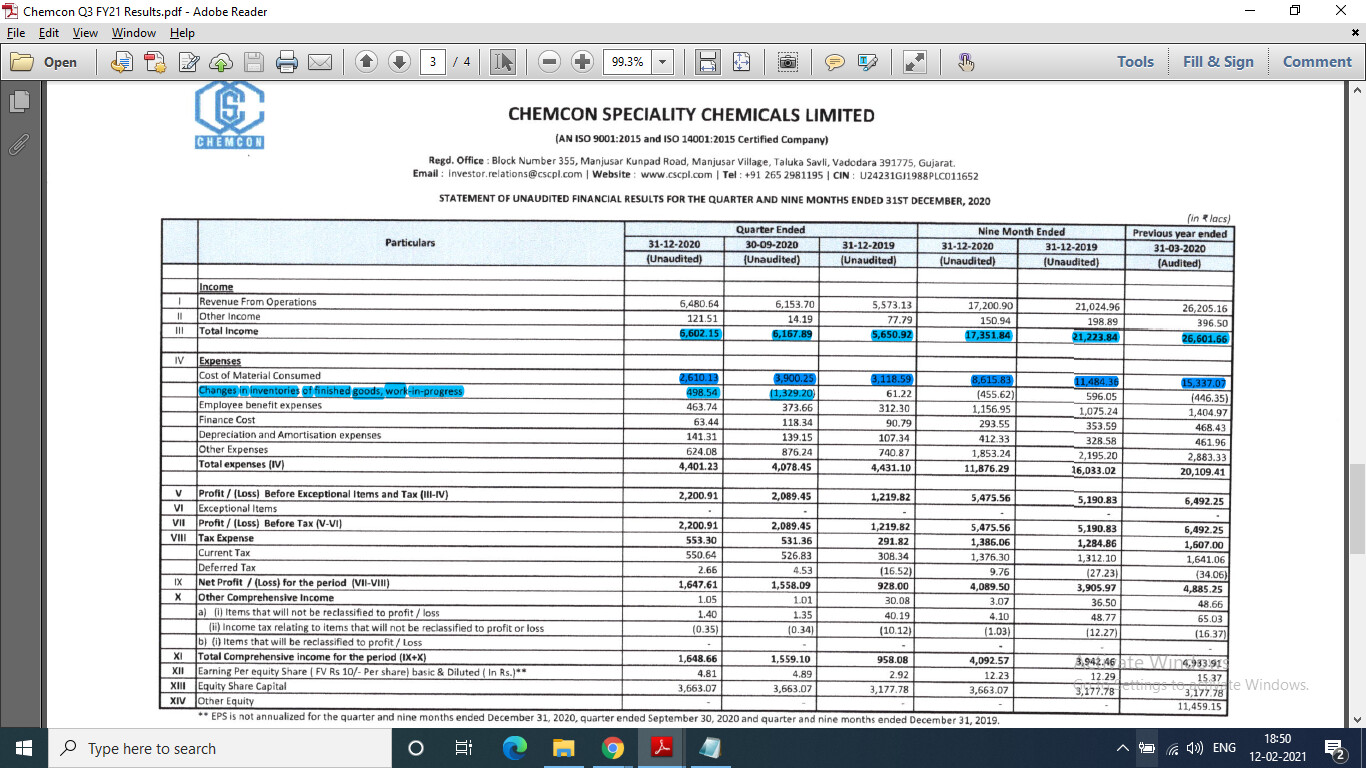

Revenue in Q2 stood at 61.53 Cr compared to 45.66 Cr in Q1 FY21. Optically, this looks good QoQ, but when compared YoY, it shows a decline of 5.8%. If we compare H1 FY21 to H1 FY20, decline is even more stark, with revenue falling by 30.6%. Company says that decline is due to disruption of operations due to Covid-19 pandemic. While it may be true to certain extent, we do see that most other spec chem companies have shown far more resilient revenues, even though they were hit by the same pandemic.

Another worrying trend seen in Q2 FY21 P&L is the steep rise in COGS. In Q2 FY20, the COGS was 29.53 Cr on a revenue of 65 Cr, where as the COGS seen in Q2 FY21 is 39 Cr on a revenue of 61.53 Cr. There is a big spike in COGS to the extent of almost 33% YoY. ChemCon has 2 main products HMDS and CMIC. The primary raw materials for these products is TMCS (Trimethlychlorosilane) and MCF (MethylChloroFormate) respectively. It would be worthwhile to check the price trend of these in international markets in 2020 to assess if this is truly due to RM cost going up, or due to some other inefficiencies in operations.

It must be noted here that Chemcon does not have any long-term purchase contracts with its suppliers, so any spike in prices of raw materials will immediately translate in higher costs for them. Also, it does not have long term supply contracts with its customers, so it may or may not be able to increase prices to its customers. In short, they will experience spikes in margins and profitability if the RM prices fluctuate.

PBT for Q2 FY21 stands at 20.89 Cr compared to 17.95 Cr in Q2 FY20. This is an optical play. How can PBT increase despite sharp increase in prices of raw materials? Its because there has been a sharp reduction in inventory to the tune of 13.29 crores, which boosts the PBT and the PAT.

PAT comes in at 15.58 Cr compared to 13.62 Cr in Q2 FY 20. The big change in inventory perks up the PAT, and it also perks up the EPS, which stands at Rs 4.89 for the quarter compared to Rs 4.29 for the same quarter in the previous year.

If the company picks up pace in H2, theoretically, it can still make up for lost ground. But it looks very unlikely that they will see any growth compared to last years revenue. At best, they may end up somewhere close to last years revenue, which of course will be considered below par, given the rich valuations that the company still commands, despite the rapid fall in share prices since the listing day.

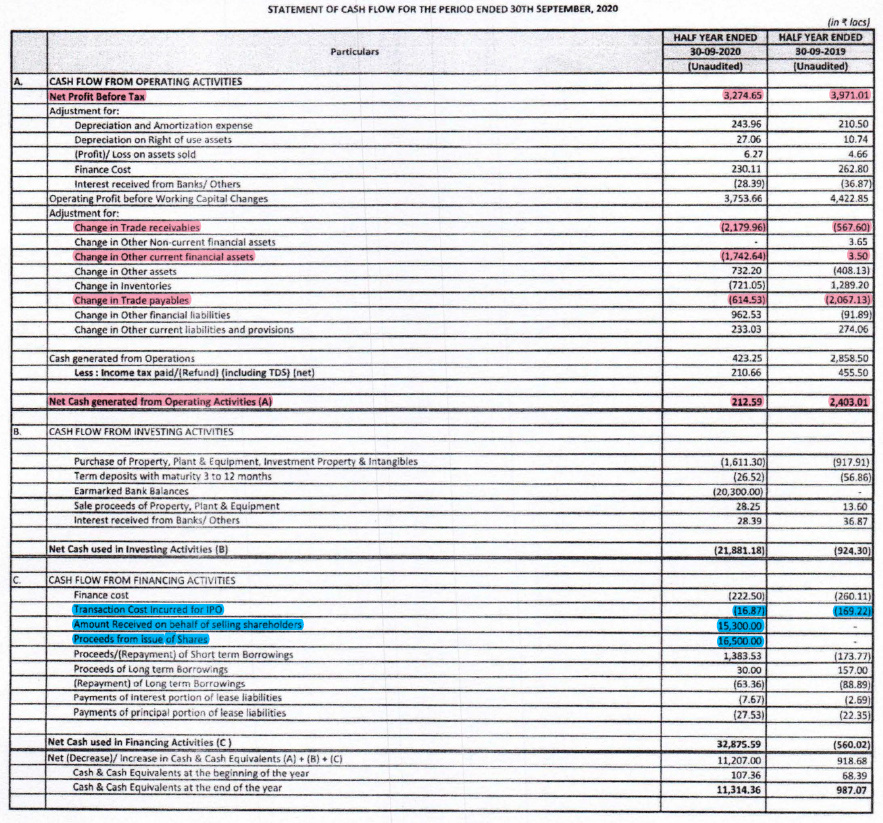

Cash Flow statement confirms the massive change in receivables to the tune of 21 crores. It also confirms the change in payables. There is also large reduction in current financial assets, about 17.4 Crores.

CFO has dipped to a mere 2.12 Crores, compared to a healthy 24 Crores from previous year. Its a massive drop. Almost all of the drop can be attributed to the 21 crore increase in receivables. That makes receivable a must watch figure in the next couple of quarters.

Lastly, we also see the IPO proceeds in CFF as well as 153 Cr received on behalf of the promoters OFS.

With this, its very important to watch out for the following in the next 2 quarters, and beyond that too

Whether the sales recover or does the damp performance continue?

Does the margin pressure continue due to higher raw material prices?

Receivables must come down to more realistic levels

Cash flow recover to healthy levels or not

If these do not improve in next couple of quarters, this could be negative for the company.

HMDS 131Cr (FY20) production 2649MT = 4.9 Lakh per MT ,

FY 21 capacity addition of 600MT=6004.9= 29.4 cr

additional revenue ==> 131 + 29.4 = 160.4 cr

total capacity = 4200+600=48004.9 ~ 235 Cr(Possible with 100% capacity utilization)

(New capacity is of high purity which might improve margin and realization.)

CMIC 34 Cr(FY20) at 677 MT ==> ~ 5 lakh per MT

Total Capacity = 1800 = 1800*5=90 Cr(with 100% utilization)

Bromides 88 Cr(FY20) for 6039 MT = ~1.45 Lakh per MT

Total capacity = 15000 ==> 217 Cr(100% utilization)

Others 9 Cr(FY20) == > 9 Cr(FY21)

Total = 217+235+90+9= 551 Cr

Conclusion: They have capacity in place problem is realizing the business. Global production is less than the global capacity so definitely there will be pressure. But with economy of scale and low labor cost they can prevail.

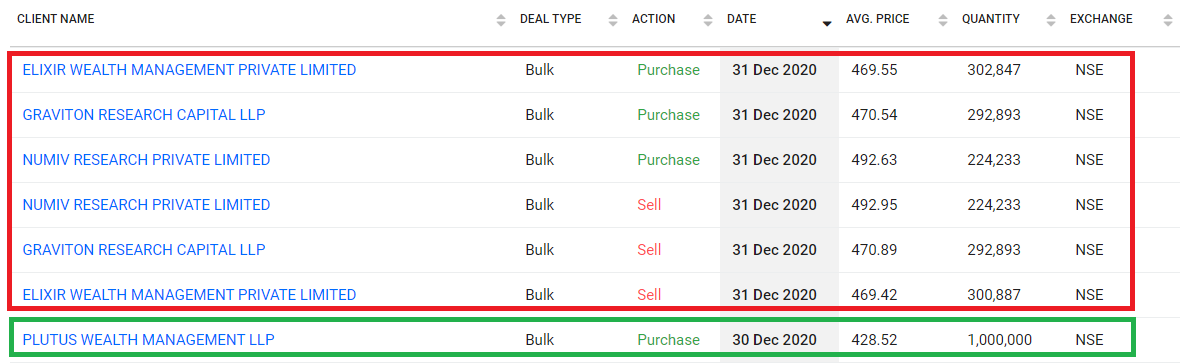

I dont know much about Technical analysis, but read that the stock witnessed a breakout yesterday. Has seen a very strong up move in the 2 trading sessions since yesterday.

A look at the bulk deals in the scrip also tells a story

There have been a spate of bulk deals yesterday, some with a very strange short term pattern (marked under red block), and onhuge one which seems to have caused the strong break out and price movement.

Though these short term signals are strong, will wait for the Q3 results to be out for clarity on the long term direction.

From the last investor call transcript, the management looks very confident of future growth. I think the company is in the right space to tap the opportunity. Even the past financial performance reflects the same.

There are a couple of Pros and many Cons in CSCPL as I fundamentally see it. It also appears to be over-valued at the moment.

Pros:

Net margin is improving

Anti-china sentiments can further CSCPL’s position in the domestic market as the replacement for imports

Clear opportunities in HMDS and CMIC.

New product launches, CBC and DHT, will help improve top line but this is not the focus as of now (November call transcript)

Planning to double PAT in 3-4 years!

Cons:

Cumulative Cash flow from operations is less than cumulative net profit when calculated for last 4 years

Account Receivables stood at more than 40% of FY20 sales! end of Q2 2020. This has now come down to ~30% as per the November call transcript.

Debtor days are increasing continuously from 68 to 124! (Can discount any rise after FY20 due to COVID)

Top 5 customers contributes > 55%

1.5% of all receivables are from related party as of November 2020 (~1.3cr out of 85cr outstanding in receivables)

The board doesn’t strike confidence. I didn’t find many remarkable individuals. Many of the independent directors have “loose” relation with promotors and directors like they are from the same college etc.

– Eg. There is one lady, “Neelu Shah”, who has only 5 years of sales experience, sitting on the board. I couldn’t find good credentials for her.

Disclosure - Had some positions. Exited in the recent rise. Planning to re-buy on dips to have some margin of safety.

Had a quick look, seems at best like a small reversal in de-growth trend seen since last year.

Revenue shows a growth of about 7% QoQ basis and about 16% on YoY basis. Though one should look at this growth in the larger context that revenue in FY20 had shown a decline of about 10+% on annual basis.

If one factors in, the disappointing numbers of Q1 and Q2 FY21, then despite this small rise in Q3, overall unless it delivers outstanding Q4 topline, there is a very realistic possibility that the full FY21 revenue may just be only marginally better than FY20 annual topline. If the revenue remains flat, that will mark 2 years in a row where the company will be struggling for growth, which does not bode well for a company that enjoys virtual monopoly in India in its leading products.

One positive factor is that COGS has come down sharply, suggesting drop in RM prices and easing pressure on margins. As stated in my post on Q2 results, in the absence of long term contracts with its RM suppliers as well as its customers, company will always be exposed to RM price fluctuations and thus will suffer from margin volatility. They must look to mitigate this in the long term interest of the company.

This quarter has been used to restore part of the inventory which was utilised in the previous quarter.

One of the main purpose of the IPO was to raise funds for capacity expansion. There seems to be very slow progress on this front. Of 41 cr earmarked for the CAPEX, only about 4 crores or roughly about 10% have been utilised in the 3 months since the IPO. Please note that the company does not need to spend any money on land, as the plants are to be setup on their existing site. So the planned CAPEX is only for civil and machinery / plant setup. Additionally, the company had already obtained quotations for Civil work, plant / machinery / equipment in late 2019, from leading vendors. Especially within this context, I think the progress appears extremely slow. Though its not clear what their implementation timelines are, if there is any delay it could lead to cost over-runs and will delay the revenue growth even further.

As per the data shared by the company, they are running at near peak installed capacity utilisation for their 2 leading products (93% for HMDS & 95% for CMIC). One of their HMDS plant was damaged in fire accident in FY 2018. The fact that one of your key product plants gets destroyed in fire, and you delay rebuilding it for almost 3 years… this itself raises a concern about the management priorities. Even if it takes 12 to 18 months for settling insurance claims, the damaged plant could have been rebuilt in 3 years. Further, slow implementation of the expansion project, especially with funds lying in the bank is an even bigger concern. Seen in the context that the revenue growth had been stuttering at best in past 2 fiscals, you wonder about the mechanics of the decision making.

Since balance sheet data is not available, not sure if the situation has improved on the abnormally high receivables levels seen in Q2. Similarly, cash flow trend remains to be seen.

So in summary, continuing from the questions raised in my post on Q2 results

With this, its very important to watch out for the following in the next 2 quarters, and beyond that too

Whether the sales recover or does the damp performance continue?

Revenue shows a decent improvement. Lets see how the trend continues in next quarter.

Does the margin pressure continue due to higher raw material prices?

Positively, the COGS shows a downward trend, helping shore up the margins. This however, needs long-term mitigation through long-term purchase contracts with vendors.

Receivables must come down to more realistic levels

In absence of Balance sheet data, remains to be seen.

Cash flow recover to healthy levels or not

Remains to be seen.

We need to closely observe how things shape up in the next quarter… following remain key observables

Trend in revenue

Trend in margins

Receivables position

Cash flow position

Expansion Project implementation

Disclosure: Not invested, but very closely monitoring

Please check their Investor presentation, worldwide production(of company products) is already more than the demand so expansion does not make sense.

While economy of scale might help but demand shall be there.

Ideally with lower RM prices, bottom line should have seen significant improvement in this quarter… however, part of the gains there flow into the increase in inventory to the tune of about 5 cr. Other than COGS, most of the expenses are more or less flattish, hence on a higher revenue and lower COGS, net profit could have been higher, but for the change in inventory. The problem however is in the long run… every upward swing in RM prices will squeeze the margins for them, due to the fact that neither they have long term procurement agreement with their vendors, nor do they have significant pricing power with their customers. For them to have predictability and stability in margins, they need have a mitigation strategy in place.

The reason I stress more about revenue growth for Chemcon is because almost 2/3 of their revenue comes from Pharma industry… and they have grown significantly in last 3 years prior to IPO based on pharma products. Given the world we have seen in last year, all strong pharma companies have grown much faster than their past averages. So why not Chemcon? ARV products have been a raging success for several companies like Laurus Labs, Hetero, Aurobindo, and its important to note that all of them are Chemcon’s customers. So the same product category is driving explosive growth for Laurus / Hetero but not for Chemcon? I will be honest to say that my knowledge in this sector is very limited, so the reasons may be very obvious to people who know, but not to me. There has to be something missing here that we cant decipher or are not aware of.

@ankit_tripathi since I have not seen the presentation you are referring to, cannot comment on it… will be happy to look at it if you can share a link…but yes, you could be right, that the current production / supply of Chemcons products may be larger than demand… having said that, that does not necessarily mean that a company cannot expand its business, or should not expand its capacity. That will be taking a very narrow view of the given data. Let me elaborate on this, and for this I will paste some lines from my very first post on this thread.

As per Frost & sullivan report, HMDS demand in India is projected to grow at CAGR of 5.6% in next 3 years. India is currently net importer of HMDS, with 52% of its demand in 2018 met by imports, mainly from China.Chemcon is the only HMDS manufacturer in India. Hence, by substituting imports and catering to India’s HMDS market, Chemcon has an opportunity to grow at a CAGR of ~20% between 2018 and 2023 in the HMDS Segment.

India and China are the ONLY 2 countries in the world to make CMIC. India has 45% market share, and China has 55% market share of global production.

India has the largest demand for CMIC, with 65% of global consumption. This demand is growing very fast. CMIC is critical input for HIV / Hepatitis B life-saving drugs.

As per Frost & Sullivan report, global demand for CMIC is predicted to grow at CAGR of 12.5% between 2018 and 2023, with demand in India expected to grow at 14% CAGR in the same period. Currently, India is a net importer of CMIC, with 50% of its demand being met through imports from China.

Please refer to the above points… There is strong growth projected in these products, not just in India but globally too. Now, its possible that projection for growth could go totally wrong, so lets just ignore them for now… In both these products, India is a net importer by a massive margin. This despite Chemcon being India’s ONLY producer of HMDS and 8th largest globally… and India’s largest producer of CMIC and 2nd largest globally. Given its market leadership position within India, and given all the anti-china rhetoric in recent past (and the china + 1 strategy) expanding market share aggressively through import substitution should be well within its reach.

What stops it? Current capacity utilization. Capacity utilization in FY19 for HMDS is 93%, for CMIC is at 95% and for Bromides is at 57%. If this data is true, then capacity expansion is the only logical way ahead. Besides, the IPO event is barely 4 months old… so if the company did not have plans to expand, why would it launch an IPO with one of the stated objectives for fund raise being capacity expansion? Hope this clarifies.

Probably you are missing few facts. Also I suggest you to have a look at their last investor con call and the last investor presentation for better perspective. Also Q3 investor call is scheduled on Feb 16th.

CSCPL replied about the increasing account receivables and increasing debtor days. PFB their response:

Working capital intensity remains high in our business which reflects in our financial statements. Our accounts receivables has increased in line with our growth in business. Infact this is one of the reasons of IPO Fund raise is augment long term working capital.

Further in our business many of the raw materials are required to be imported. In view of the anticipated challenges in raw material sourcing during pandemic, the company had built an inventory of raw materials resulting in higher inventory days during H1FY21. Further large part of H1FY21 sales took place in Q2FY21 and therefore the debtor levels appear high which is anticipated to normalize in the coming quarters. Finally the pandemic has caused all suppliers to extend credit period to clients which has resulted in slow realization of debtors. The company is confident on debtor recovery and manages prudent risk management strategy to realize its monies.