Q4 Management comments.Q4 Management comments…pdf (947.9 KB)

August con call 2021

India is a net importer of HMDS and CMIC. Chemcon is the largest manufacturer of both the products in volumetric terms.

Chemcon is an import substitute

With a backward integration to reduce import of raw materials and a capex of 41crores in line to plant 8 and plant 9( p8 and p9), the company forsees sales of 120-160crores.

New products in the pipeline and new applications to the existing products. The company hopes to do better and supply to the U.S.

On the flip side

Chemcon sells its products per kg basis as per the conference call leaving the customer to negotiate on placing large quantities.

The realization of profits will not be in line with increasing sales. There will be flexibility in profits.

Why shouldn’t it be consistent profits with higher sales?

Just studying the company.

little disappointed

4 Likes

Bumpy ride continues… Co received communication from Gujarat Pollution Control Board, directing closure of plant. They have suggested that they plan to make a representation to GPCB on this.

Disclosure: Not invested, do not plan to invest.

It’s probably the dark horse of Chemical players. Valuations seem reasonable given the growth triggers are going to come in during H2.

- 1200 tons of CMIC production goes into trial run from next qtr and commercial production from Jan 2022.

- P10 coming online during 2023

- Business is targetting 100 crores of profitability by FY 23.

Execution has been hampered by a lot of events. If they execute as plan story should start playing out from Q4’22.

1 Like

Could anyone explain what is happening with this stock(Stock hit lifetime low as I am writing this post) ? Recent performance of stock seems bearish compared to other lister peers in same space.

1 Like

YoY revenue was same but volume of products were reduced by 20%…this may be reason

1 Like

Thanks for your response  @Krishna_Kumar

@Krishna_Kumar

Does this mean non core income or other income is more than previous quarters?

Seems because of higher price…

1 Like

@aman Yes, I read this in their concall transcript. Along with this, there were lot of positives on upcoming quarters. Meantime, Stock was going south  Hope upcoming quarters will be better

Hope upcoming quarters will be better

1 Like

I think profits are directly linked to volumes, so any price increase or decrease shouldn’t affect much the bottom line.

Volume need to increase, otherwise backward integration can increase bottom line in the future.

4 Likes

Ya I know, they mentioned this in their previous concall. However I was not able to understand the attached statement of the management.

4 Likes

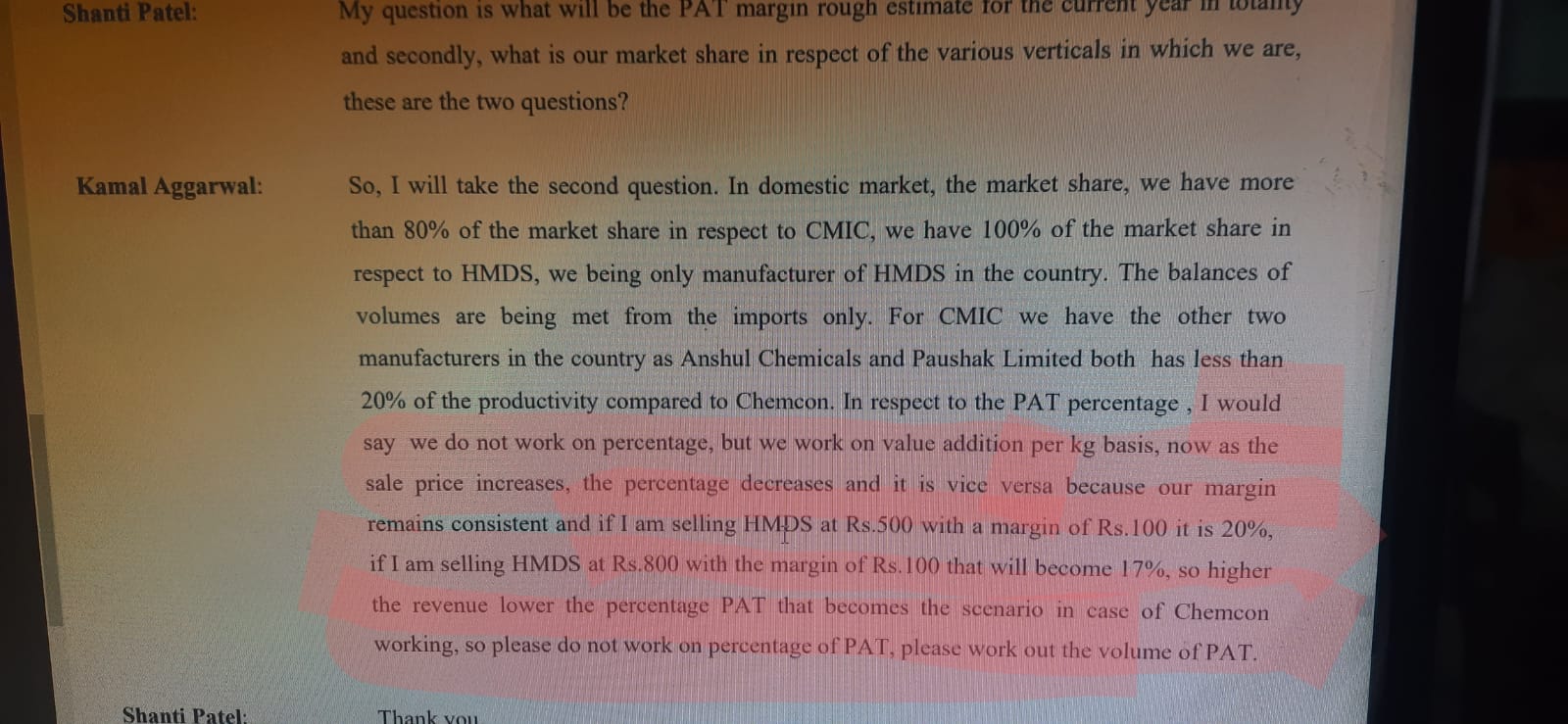

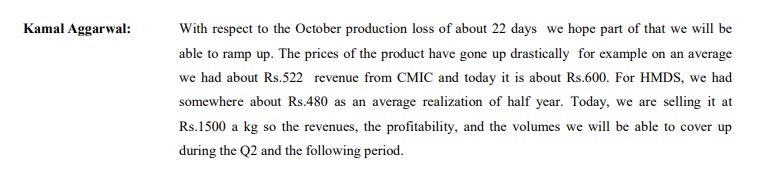

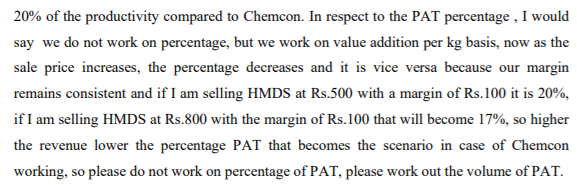

What management is saying here is, their profits are not tied up to revenue,

revenue can increase or decrease with end product realization changes(commodity nature).

They charge per KG or per Ton basis,

consider below ,

Suppose they sell HMDS at 100 per KG and margin is 20 per KG, now after few days HMDS prices increased in market place, it now sells at 200 per KG but their margin is still 20 per KG.

So irrespective of increase or decrease of market prices of HMDS, they earn 20 per KG.

So in case of this company always check volumes and not revenue.

10 Likes

did anyone attend the agm. If yes will be great if can share the notes

https://www.bseindia.com/xml-data/corpfiling/AttachLive/93a9afac-15d6-442f-9432-cade3296048c.pdf

All this land purchase is related party transactions

1 Like

Chemcon chemicals has given a bad performance in quarter Q2FY23, bith YOY and QOQ. Sales, net profit, Ebita, Ebita margins are all down in the current quarter significantly. In investor presentation, they have mentioned that this is attributed to soft demand from Pharma companies during this quarter. While they are aptly diversifying into other value products, and expansion is on track, it is not possible to understand whether the impact on sales and margins will continue in the coming quarters as well or the demand is likely to improve going forward. Promoters have to come clean on these issues to maintain the fair corporate governance rather than simply keepin patting their back for aggressive expansions that they are boasting off.

I don’t understand one thing, if they are import substitute products, why their capacity utilization levels are so poor?

1 Like

Interesting case of Partnership turned in to a listed company.

- Both Aggarwal and Gupta family holds equal nos of shares in the company. In the IPO Mr. Kamalkumar Rajendra Aggarwal and Mr. Naresh Vijaykumar Goyal sold 2250000 shares each.

| Aggarwal Family | No of Shares | Goyal Family | No of Shares |

|---|---|---|---|

| Kamalkumar Rajendra Aggarwal | 1,19,27,080 | Navdeep Naresh Goyal and Shubharangana Goyal | 62,33,500 |

| Rajveer Aggarwal | 25,32,800 | Navdeep Naresh Goyal | 23,74,666 |

| Minal Kamal Aggarwal | 14,40,000 | Shubharangana Goyal | 19,78,888 |

| Naresh Vijaykumar Goyal | 52,85,826 | ||

| 1,58,99,880 | 1,58,72,880 | ||

| Less IPO OFS | 2250000 | 2250000 | |

| Post IPO holding | 1,36,49,880 | 1,36,22,880 |

Now lets see how they are withdrawing remuneration.

| Director’s name | 2022 | 2021 | 2020 | 2019 | 2018 | |

|---|---|---|---|---|---|---|

| Kamalkumar Rajendra Aggarwal | 35.8 | 29 | 23.58 | 66.03 | 51.51 | |

| naresh Vijay Goyal | upto 15.02.2019 | 61.12 | 45.87 | |||

| Navdeep Naresh Goyal | 38.2 | 31.4 | 25.98 | 22.19 | 16.17 | |

| Rajesh Chimanlal Gandhi | 3.1 | 2.6 | 2.16 | 2.34 | 1.92 | |

| Himanshu Purohit | 3.1 | 2.6 | 2.16 | 2.34 | 1.92 | |

| Rajveer Aggarwal | 2.4 | 2.4 | 2.4 | 17.27 | 10.52 | |

| Total Remuneration in Mn | 82.6 | 68 | 56.28 | 171.29 | 127.91 |

As Mr Naresh Vijay goyal was involved in a criminal case, His name was removed from managment team. Even in the IPO it is mentioned that he’s not involved in the business activites.

His son Mr Navdeep Naresh Goyal, who is just 32 yrs old by qualification passed Higher

Secondary Examinations only but getting more remuneration than chairman & MD of the company who’s 60 yrs and having an experience of 26 yrs.

| Aggarwal Family | 38.2 | 31.4 | 25.98 | 83.3 | 62.03 |

|---|---|---|---|---|---|

| Goyal Family | 38.2 | 31.4 | 25.98 | 83.31 | 62.04 |

| Total Remuneration | 76.4 | 62.8 | 51.96 | 166.61 | 124.07 |

Aadha tera - Aadha mera.

12 Likes

Hi

Great Write up. Thanks first of all.

Whats your take right now?

Fixed Assets seem to be ramping up quite similar to that of between 2017 to 2019 when revenue and PAT explosed.

Q.1. Can similar trends expected?

Mcap 1000cr approx

bV 436 cr

FY23 PAT TTM would be approx 80-100 cr

Q.2. now given FA uptick, can Revenue and PAT shoot up 2x 3x similar to 17-19 trend, to say 200-300 cr by FY24-25?

( Loans 38 cr.

Cash n Bank is 200 cr approx) virtually half of BV is in Cash.

going forward BV can go upto 600-700 cr, if PAT picks up)

1 Like