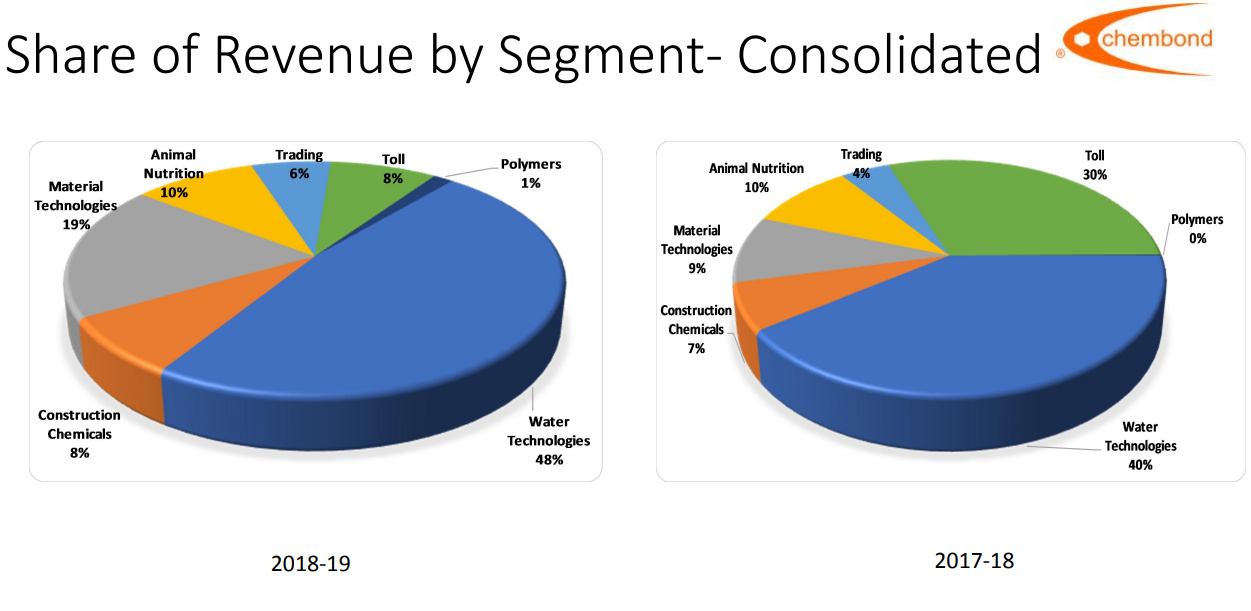

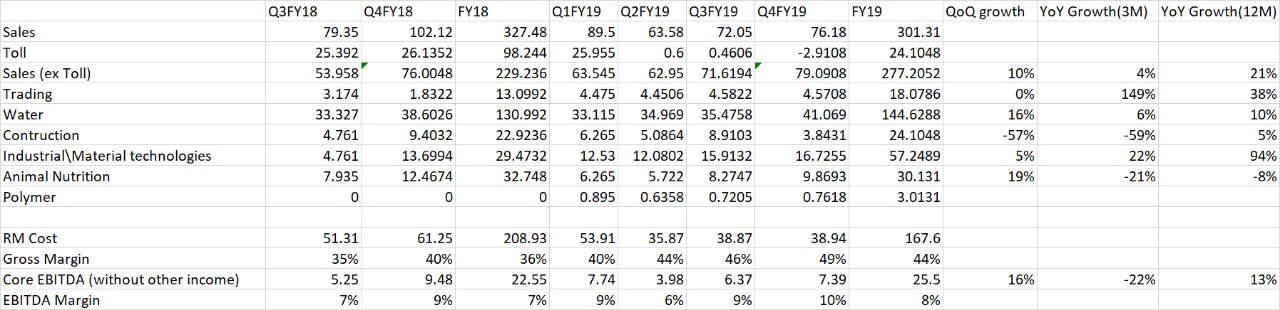

Chembond Presentation for Q4:

Sales breakup:

The operations seems to have stabilized and one can see GM & EBITDA margins improving every quarter for the last three quarters. GMs have moved up from 44% to 49% and EBITDA from 6% to 10% in last three quarters after the toll business moving out. The slowdown in the construction segment in Q4 is probably due to elections. Animal nutrition is another -ve, I expected this business to grow significantly but it had a degrowth this year. Another thing one needs to assess is how the material technology business is panning out since it also has a significant inorganic part coming from PSPL.

Overall the company looks set for a very good growth path next year.