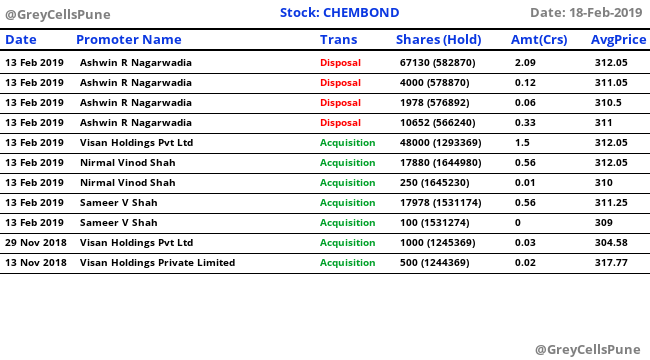

One of the promoters, Ashwin Nagaewadia sold around 83760 shares in open market today. Does anybody know who the buyer is and what is the need for selling such a huge qty of shares in the open market.

1 Like

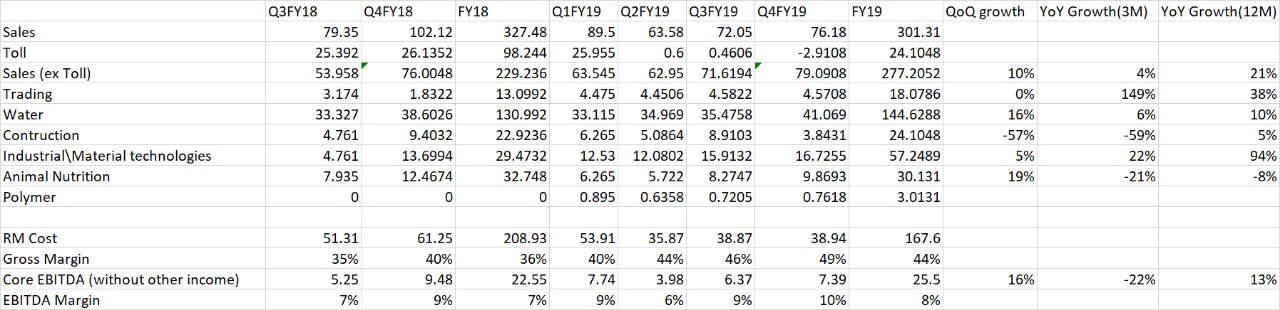

Todays quarterly results will give us a better idea of things to come,

There is other income of approx 200 lacs this qtr. Results good QoQ , but last qtr historically better.

Chembond Presentation for Q4:

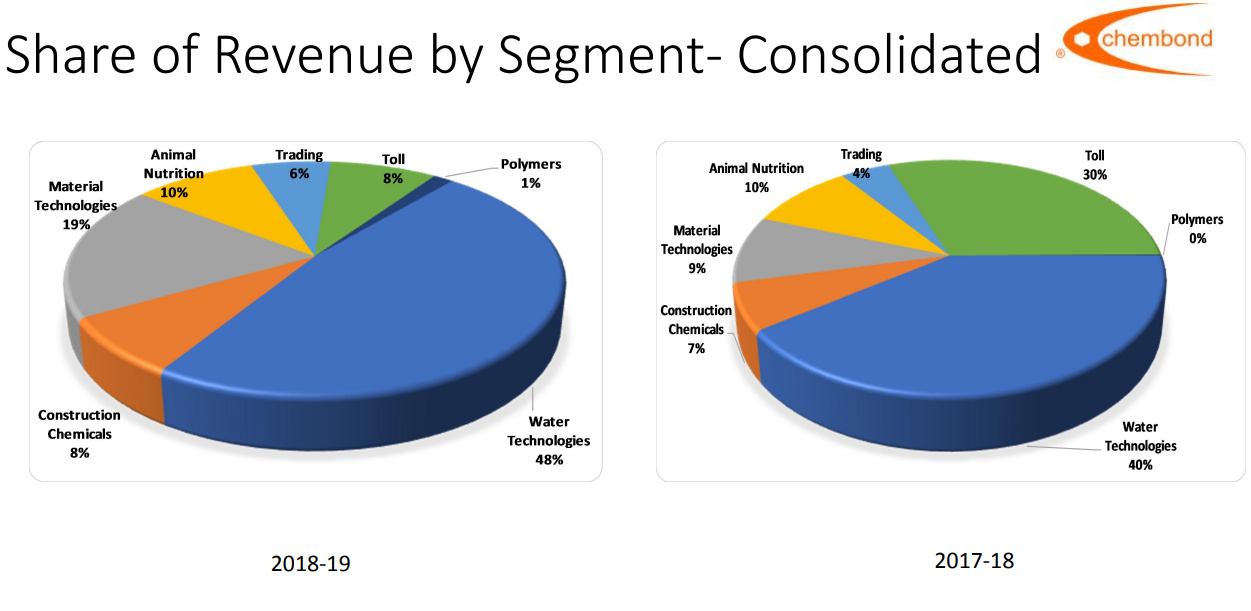

Sales breakup:

The operations seems to have stabilized and one can see GM & EBITDA margins improving every quarter for the last three quarters. GMs have moved up from 44% to 49% and EBITDA from 6% to 10% in last three quarters after the toll business moving out. The slowdown in the construction segment in Q4 is probably due to elections. Animal nutrition is another -ve, I expected this business to grow significantly but it had a degrowth this year. Another thing one needs to assess is how the material technology business is panning out since it also has a significant inorganic part coming from PSPL.

Overall the company looks set for a very good growth path next year.

3 Likes

Ashwin Nagarwadia spends time in the US and i think he is a NRI hence due to some compliance reasons he has had to dispose off some qty in regards to that. His intention was not to sell in the market and here anyways in this case promoters bought his stake out. This was the sole purpose to sell at this stage.

2 Likes

Any updates from the AGM will be appreciated.

What feel does one get from management ( talks and body language)?

Any updates on the polymer division will be appreciated

Thanks

Chembond Chemicals

AGM FY19 Notes

We have decided to divide our business into seven segments:

- Water

- Material Technologies

- Animal Nutrition

- Construction

- Polymers

- Industrial Hygiene - Calvatis

- Trading

Polyamides Segment

- When will the 1500 MT plant start its commercial productions? Can you give us an idea in terms of how we are going about booking our capacities for this project?

We have our pilot plant running. The next stage would have been a 1000 tonnes plant. Currently, we are focused on achieving utilisation of our existing pilot capacities.

Current utilisation of pilot plant: 50%.

We can go up to 60 tons comfortably.

At the same time, market dynamics are changing. Because one of the crude derived monomers has been in a short supply over the last 6 months. There had been an incident in US plant. The HMDA prices have shot up which is a one-off and because of that, we would not be comfortable starting up a 1000 tonnes capacity plant at the current margins. HMDA for years used to be very stable. So, until some new capacity comes on stream, which they say would be around 2020 or 2021, till then it might remain volatile like this.

RM:

- HMDA is being imported into the country. This monomer is made by 3 companies in the world: 2 in US and 1 in Europe.

- Sebacic acid (a derivative of castor oil) is being exported from here but then is coming back from China at very low prices. Most of the suppliers of sebacic are rather interested in exporting it due to duty drawback advantages.

We are: - watching the prices of these monomers

- filling up our existing capacity

- Simultaneously working on other polyamides

We have done the engineering but we haven’t started the project of 1000 tonnes. The reasons are: - One is the raw materials mentioned above.

- We were waiting for EC approval. Around 2 weeks ago we have been informed that the site is in the red zone and will not be approved despite getting project report verified and tested by a leading university So, we will look for another site for this project. All Zones in Gujarat except for Dahej, Villayat are right now in the red category which means that there is no expansion allowed. So, only renewables are being managed by them right now.

Project Development: - Products have been converted into monofilaments and they have already been supplied to 3 customers. Out of them, 2 have become regular customers who are consistently buying. We expect this trend to catch momentum.

- We are going ahead with the project. But most probably, we would first invest in a monofilament and packaging client before we go in for an intermediate plant at the approved capex which was done last year.

- The land portion will be significant in the upcoming capex. For the new land, we might end up buying more than we require as they sell those not on sq. m. basis but on the basis of parcel.

- New capacity will probably come around Gujarat and Rajasthan. Rajasthan accounts for 10-15% of castor produce and Gujarat accounts for 85% of it.

- Our focus initially was on Nylon 6,10 because that is green and is preferred by one large industry in India – the oral care industry. And it is currently being imported into the country. But due to the spike in HDMA prices, other nylons as well like 6,6 which use this monomer.

- We also have other products that will complement the polyamides (Nylon 6,10). We also make some grades of:

a. Engineering polymers (Nylon 6,6) – Big consumer: Automotive Industry which has switched to Nylon 6 which is cheaper.

b. Additives for ABS polymers

c. Nylon 6,12 – also used in brush bristles, tubing, injection moulding, coating etc.

It is a relationship business. So, certain suppliers are happily supplying to global companies who are manufacturers of these filaments and polymers. They don’t want to risk their business relationships with them. So, if they want to entertain us, it will not be at the cost of their existing customers.

About Nylons: - There are a few options available to customers. So, if it is not 6,10, they can use 6,12. If it’s neither of these, they can go to the extreme case of going to some conventional fibres.

- Cost-plus doesn’t work in nylon. If the customer like automotive industry feels it (Nylon 6,6) is expensive, they will switch over to cheaper grades like Nylon 6.

- What is the market size of polyamides in India? If it is possible, could you share the details of the market size with respect to end-user industries? Like Bristles market you mentioned in AGM to be around 4500 tonnes. Also, is the entire demand currently imported?

Assessment of the market size: It is not just the market for monofilament. It is of various sizes and different colours. We started with attempting to supply a particular size. The customers are now having newer requirements. So, we are adapting to those changes. We are finding out vicinities where we have the capability to make that kind of fibre in different shades. - What is basically preventing global players like BASF to set up a manufacturing facility in India, since they have huge production base for polyamide 6 and 6.6 in the Asia Pacific including 100,000 tonnes which they set up in China in 2015 and since India is the largest castor oil producer in the world?

They already have sufficient capacity there. They want to utilise that facility. They will make some other chemicals here. So, all of them are working on that model. On one particular location, they will scale up into global capacity in that product line in that country. We are able to compete with them but we are not happy with the margins. If we want to make and sell, we can sell but the profit won’t be significant for us to scale up our capacity.

Toll

-

In last AGM, you mentioned that you will be starting with the toll segment on your own. Since the operations have been shut down in June, we have not come across any growth in revenue whatsoever. Could you give us an update on our stance in this segment?

Our non-compete ended in May 2018 and we restarted the production in August 2018. So, currently we are at a capacity utilisation of 20% and it takes 35% utilisation to reach the breakeven levels. -

Do we have any running expenditures right now in Toll segment?

Tarapur plant where we used to do toll manufacturing of about 1000 tonnes for Henkel, is now being utilised at 20-30%. Variable costs have stopped but yes there are some fixed costs. We have felt it prudent to continue those costs because we want to cater to this business and we see the good potential.

Previous utilisation levels may take about two years. -

Are we going to do toll business through chembond material technologies that do defence and MRO already, or on standalone basis?

We started this under chembond material technologies (protochem earlier). (I couldn’t understand this part. Doubt: Sales given in Chembond material is 16.21 crores and Loss before tax is 1.03 crores. But segmental sales of toll itself is Rs. 24.1 crores. So, it couldn’t be a part of material technology subsidiary this year).

Metal treatment is operating under Chembond Material Technologies (Protochem Industries earlier). The industrial coatings will also become part of this subsidiary now and the subsidiary earlier named as chembond industrial coatings was renamed as Chembond Biosciences ltd. which will have animal nutrition as a primary operation.

Industrial Technologies

- Since the acquisition of PSPL and Gramos, how have the two subsidiaries grown?

In PSPL, we look more at gross margins. So, GM has been difficult for most of the year because of the crude and PVC crisis. But that has now come back to comfortable levels. PBT has come down because of two things:

a. RM costs

b. The delayed effect of passing on those costs to the customers

c. We are investing heavily in product development and R&D. This company was kind of stuck for almost 7-8 years. There was no development happening, no up-gradation of the plant. We acquired it for access into those markets. We have invested in R&D, safety and testing facilities. New Product development capabilities did not exist before us.

Animal Nutrition

-

Any specific reason for why was there a de-growth in this segment this year despite having such a lower base? The expectation was that this segment will grow faster than the rest of the company.

AR 2019: “The Animal Health & Nutrition business passed through a turbulent year with the poultry industry recording poor growth due to higher feed prices and other regional issues. Sales to some corporate customers were also lower due to a change in strategy.” -

There are tons of players in this segment out there. So, what are we offering that differentiates us?

We have a couple of niche products.

One is we are manufacturers. We have our own fermentation capacities. So, we make our own enzymes and probiotics. We will start making prebiotics. This is a very big part of the animal nutrition business.

Secondly, we have a very good Vitamin D molecule called Alpha D3. So, its absorption is better. Vitamin D3 in higher doses damages the kidneys. Our alpha D3 doesn’t do that. It had some trials conducted and their findings have been very favourable.

The formulation is not very easy. This is a very powerful substance. Chembond, for the past 5 years has been associated with Alpha D3. Others have tried to sell Alpha D3 but have not been very successful. -

What kind of growth can we expect from this segment in the next 2-3 years?

This year, it is growing in double digits and margins are going to be better. -

In AR you said, that you have invested in new segments in animal-like aqua. Can you please elaborate on what kind of investments have we done in it?

The investments have been done in people.

Water

- If we look at the financials of Chembond water technologies there has been a decreasing trend in the EBITDA margins of the company from 16-17% in 2012-13 to 11-12% in 2016-2017. Any specific reason for this? Could you give us the range within which you expect the future EBITDA margins to be?

Yes, Margins are getting back. So, GM has been maintained. Some of the investments that we made into people, lab facilities and some O&M contracts have to lead to a decrease in the bottom line. The margins aren’t really so much of a worry in this segment.

We lost OPAL but we just won MRPL again which is a 3-year contract. On infra side, opportunities exist but I think the framework is not yet ready from the government’s side. Timeline is a bit of question mark.

From our existing product line, two areas – coagulation and preservation are more focused.

We can assume 10-11-12% sales growth in this segment. While the opportunities grow, not everything that is an opportunity is in our domain of expertise. Second, we are not the only ones. As there will be more projects coming into this space, more bees will be attracted to this segment. I don’t want to be euphoric and make claims. So, we are ready – in terms of our team, distribution, some strengths than most of our competitors.

Volume growth will happen but value growth may not happen. - Any Reason for increase in sales of clean water and a huge jump in PBT margins from 3-5% to 16-25%?

We have been maintaining our stance in the equipment business to stay away from large corporates. Our target is an industrial consumer and our approach is to solve their problem rather than giving them a product.

We have combined two distribution into one and selling the chemicals as well as equipment through the same channel. That’s why you would observe such growth in numbers.

Industrial Hygiene - Calvatis

- Sales increased from 1.4 crores to 4.2 crores with PBT margins at 23%. How scalable is this?

Indian JV restricts us to go all over the world. We procured some clients and replaced Ecolab. We have been approved by another international brewery. We will keep adding customers from snacks and food industry.

Others

- What can we attribute the increase in employee cost to this year from 43 crores to 51 crores?

The increase in other expenditure and employee cost is majorly contributed by the material technologies and some by polymers and animal health.

9 Likes

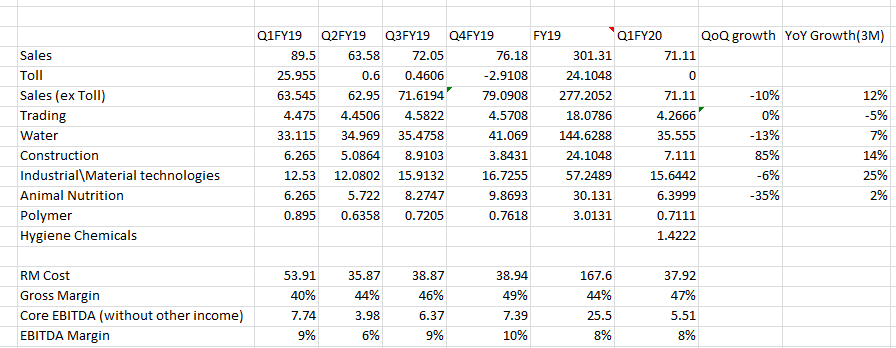

This is how the nos for various segments look this quarter. Hygiene chemicals is the calvatis subsidiary.

The YoY picture says that the topline growth of 12% (without toll) is steady. Animal nutrition is a seasonal play which is heavy Q3/Q4 and hence not much to infer from. The major growth is coming from industrial technology where they are adding newer clients. This should also be the segment where maximum operating leverage comes from. The mgmt said this segment will break even at 35% capacity utilization which they should be reaching by year end.

4 Likes

Result.

Revenue flat and PAT 155 Lakh vs 349 Lakh / EPS 1.14

There is higher tax outgo this quarter including deferred taxes.

Gets listed on NSE

Promoters are nibbling …buying small lots .

hi All

was taking a deep dive into chembond and was stuck at the below points -

- analysing its subsidiaries -

Apart from its standalone business, there are 10 subsidiaries in Chembond which are more important now given henkel was a part of standalone.

Of all the subsidiaries, the water technologies is the important one. below are its margins over the years -

| Water Technologies Limited | |||||||

|---|---|---|---|---|---|---|---|

| Particulars | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

| Sales | 75 | 86 | 94 | 103 | 123 | 133 | 124 |

| increase by | 16% | 9% | 9% | 19% | 8% | -6% | |

| PBT | 11 | 8 | 11 | 12 | 11 | 12 | 10 |

| PBT Margins | 15% | 9% | 12% | 11% | 9% | 9% | 8% |

the margins have been stable over the years, but not very high. Looking at ion exchange, their margins dont seem to be quite high too -

| 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | |

|---|---|---|---|---|---|---|---|

| ION Exch PBT margins | 1.9% | 3.0% | 4.0% | 5.3% | 6.3% | 8.8% | 8.8% |

there is one another subsidiary that has reported significant losses in FY20 -

Material Technologies Private Limited (formerly known as Protochem Industries)

| Particulars | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

|---|---|---|---|---|---|---|---|

| Sales | 6 | 8 | 7 | 9 | 17 | 16 | 42 |

| increase by | 44% | -18% | 29% | 95% | -3% | 159% | |

| PBT | -1 | 0 | - | 0 | 1 | -1 | -6 |

| PBT Margins | -27% | 1% | 0% | 2% | 5% | -6% | -14% |

I have been unable to figure out the reasons for such a significant loss in FY20, along with such rapid increase in revenues…

- difference in standalone and Consol Sales -

| Particulars | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

|---|---|---|---|---|---|---|---|

| All Subsidiaries (A) | 84 | 101 | 106 | 119 | 165 | 224 | 255 |

| Standalone (B) | 203 | 217 | 216 | 218 | 232 | 156 | 59 |

| Total Sales (A+B) | 287 | 318 | 321 | 338 | 397 | 380 | 314 |

| Consol Sales | 274 | 299 | 270 | 291 | 327 | 301 | 268 |

there is nearly a difference of 50 crores in almost all years, reasons for which i was unable to figure.

- Adjustments to net worth

there seems to be one shady transaction done by the company in its networth in the year they sold Henkel -

| Networth | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

|---|---|---|---|---|---|---|---|---|---|

| Opening NW | 62 | 72 | 81 | 86 | 95 | 206 | 230 | 248 | 261 |

| Profits | 13 | 7 | 8 | 12 | 154 | 19 | 22 | 17 | 2 |

| Dividends | -2 | -2 | -2 | -2 | -6 | -2 | -2 | -3 | -3 |

| Others | -1 | 4 | -1 | -1 | -36 | 7 | -1 | -2 | 8 |

| Closing NW | 72 | 81 | 86 | 95 | 206 | 230 | 248 | 261 | 269 |

the 36 crores you see in 2016 is as per me money taken out by the management of the company through converting an associate in the company. Does this make sense?

Found some good market share info -

In the cooling water treatment chemicals segment, Chembond stands first in the market, occasionally dropping to second place when its competitor with a similar market share moves ahead. Cooling water treatment chemicals are widely used in the fertilizer, refinery, power, petrochemical and metals industries. Within the fertilizer industry’s cooling water treatment chemicals market, Chembond holds a market share of 65–70%. Within the refinery industry, its share in private sector companies is approximately 50% and 15–20% in public companies. Similarly, in the steel industry, the company has a market share of 25–30% in the private sector and 15–20% in public sector companies. Revenue from the cooling water treatment chemicals segment in India is 60–65% of the company’s total revenue. Its market positioning as one of the top two enterprises in the Indian water treatment segment is indicative of the company’s strong market leadership and market share.

the second im assuming is ION exchange?

cant go ahead and invest unless these things are clear.

with 270 crores of revenue, this company is in way too many businesses.

Cheers,

Umang

4 Likes

I had initiated a tracking position in this company around a month back but i have sold out since then, the two main reasons that put me off were

- It has too many subsidiaries for a company of such small mcap, shows lack of focus on the part of management

- It has investments in shares of various companies and looks like they have been trading in stocks which is a big negetive

1 Like

Chembond chemical AGM 2023 notes:

Water treatment - gross margins are 47% , construction chemical -30%, Material technology-41%, Animal health-34%

- Water technologies grew by 26.5% - it comprises 50% of total group, Material technology-38% growth and is 30% of business, Animal health -6% contribution and had degrowth, Construction chemical contribution-5% and grew by 16%

- working capital increase- mainly due to increase in turnover. Net WC days we have improved our previous years

- There is plan to merge polymer with material technology is underway and may happen this year

- So many subsidiaries are there because 1) we did some acquisitions and it requires approval from customers and government authorities for it to merge 2) Some subsidiaries are due to legacy issues such as JV with MNC. We have started the process of simplification

- Water business- 50% of chembond consolidated. When we acquired JV partner stake it gave us more freedom to pursue strategies that we wanted to implement and it is bearing results. Industrial capex is helping the business growth on water treatment side. 12-15% growth is normal business growth. We have high gross margin but it is a service business hence employee cost is higher. 80% of employee cost is due to water business. This is why gross margin to EBIDTA margin translation is lower

- Positive for water business- RM cost is coming down. RM price increases pass on to customer trail by 2-3 quarters and we can see the same happening this year

- No change in manpower deployment strategies in water business

- On Industry level there is trend to moving to O&M model and we are positioning for that

- One change that we are driving is on technology front- operations are being digitized. they are both back and front end operations such as customer operating perimeters. We have digitized the safety and health segment

- Bio based products in water has been there for many years- but it has certain limitation. We have products in this segment but we do not see huge scale up

- Trend for recycling and reducing water usage is good for us as it requires investment by customer in water treatment

- We are increasing cross selling opportunities - that is helping us momentum in growth despite very strong competition

- We do not intend to get into membrane manufacturing business but will continue to innovate on chemicals side

- We are well positioned in all segments and will continue to grow but it may not be as high as last year

- Margins- if you look at 2 yrs ago margins were very low, then there was sudden spike price in RM but we passed on that with lag this year and hence margins improved. Margins may revert back

- Our gross margin are high and decent but EBIDTA is low as we continue to invest in business

- Challenges we see are - human resource will be challenge in 3-5 years. Keeping up with technology changes happening around world is a challenge and we are addressing both challenges by investing in both these areas ahead of curve

- We acquired two businesses 5-6 yrs back and we are scouting for other new opportunities for acquisition

- Material technology- getting approval is a very long process and takes upto 2 years. We are at approval stage with many customers. current growth is result of efforts done 3-4 years before. We have strong pipeline for approval with new product/customers that will drive business growth in future

- We grow in MT side by both new customer acquisition and larger product basket with existing customer

- Lower growth in last 7-8 years has to be looked with context that we exited a JV business which was 185 Cr and we recouped same revenue and grew in a very competitive market. That in our view is good performance

- RM prices were volatile last year and have stabilized now. Our customers also keep track of RM prices and as they come down they ask for reduction which we have to give

- Metal treatment chemicals margins are higher than sealant as sealant is bulk chemical business

- Bio science business has been challenging for last 2-3 years as demand went down and feed cost sky rocketed. We had internal factors as well. We have complete range of product - dairy and poultry. Poultry is larger business-80%. We are focusing on larger cooperatives. While focusing on business hygiene we will focus on growing the business. Margins has improved and will improve further this year

- We put up presentation on website after quarter indicating numbers on each business

- Construction chemical- has been old business but we have not focused much on that while we try to learn from our past. we are very selective in choosing customer. It is highly organized at top end and highly unorganized at bottom end.

- we are very strong in certain segment of construction chemical and will continue to grow in that. There are many smaller players entering compromising quality which we will not do to gain topline

- Higher receivables are due to execution cycle and nothing more. We have a policy of provisioning and we provide for receivables beyond certain number of days

- Capex has happened in sealant business- based on customer demand and forecasted growth. It should be completed within this year. Next phase of capex in this segment next year. Metal treatment and water treatment capex too shall get completed this year.

- Pheroze Sethna- we are consolidating the businesses within metal treatment business and hence there is some loss

- Q4 is the strongest quarter for us. Q1 FY 24 was the best Q1 ever.

- Legal professional fee is higher due to people employed as consultant and nothing else. Legal fees is very small most of the expenses is part of professionals deployed as consultants

10 Likes

Any take on the Q2FY24 performance?

Revenue has stagnated for last 5-6 quarters but operating margins are improving. What could be the other income component as that is significant this quarter.

You wrote “Margins may revert back”? Does the management mean that margins will go back to 4-6% levels or stay at 7-8% or even improve? Needed the clarification. Thankyou

Chembond Chemicals Announces Demerger and Business Reorganization

• The Board of Directors of Chembond Chemicals Limited (‘CCL’) at its Board of Directors meeting

today approved:

![]() Demerger of the construction chemicals and water technologies businesses into Chembond

Demerger of the construction chemicals and water technologies businesses into Chembond

Chemical Specialties Limited (‘CCSL’).

![]() Amalgamation of Chembond Clean Water Technologies Limited into CCSL.

Amalgamation of Chembond Clean Water Technologies Limited into CCSL.

![]() Amalgamation of Chembond Material Technologies Private Limited, Phiroze Sethna Private

Amalgamation of Chembond Material Technologies Private Limited, Phiroze Sethna Private

Limited and Gramos Chemicals (India) Private Limited into CCL.

• Subject to shareholder, creditors, and regulatory approvals, the shareholders of CCL will get 2

(two) equity shares of CCSL for every 1 (one) equity share held by them in CCL.

• On the scheme’s effective date, the demerger will result in two distinct listed entities aligned

along business lines. As a part of the scheme, CCL will be renamed to Chembond Material

Technologies Limited and will house the metal treatment chemicals, sealants, coatings, industrial

adhesives, and the biotechnology businesses. Further, CCSL will be renamed to Chembond

Chemicals Limited and will house the construction chemicals, water technologies, cleaning and

hygiene and distribution businesses.

• The demerger is intended to allow room for both listed entities to obtain leadership positions in

their respective sectors and unlock value for CCL shareholders.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/25517598-def4-40a0-9971-070dc0733b47.pdf

4 Likes